Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

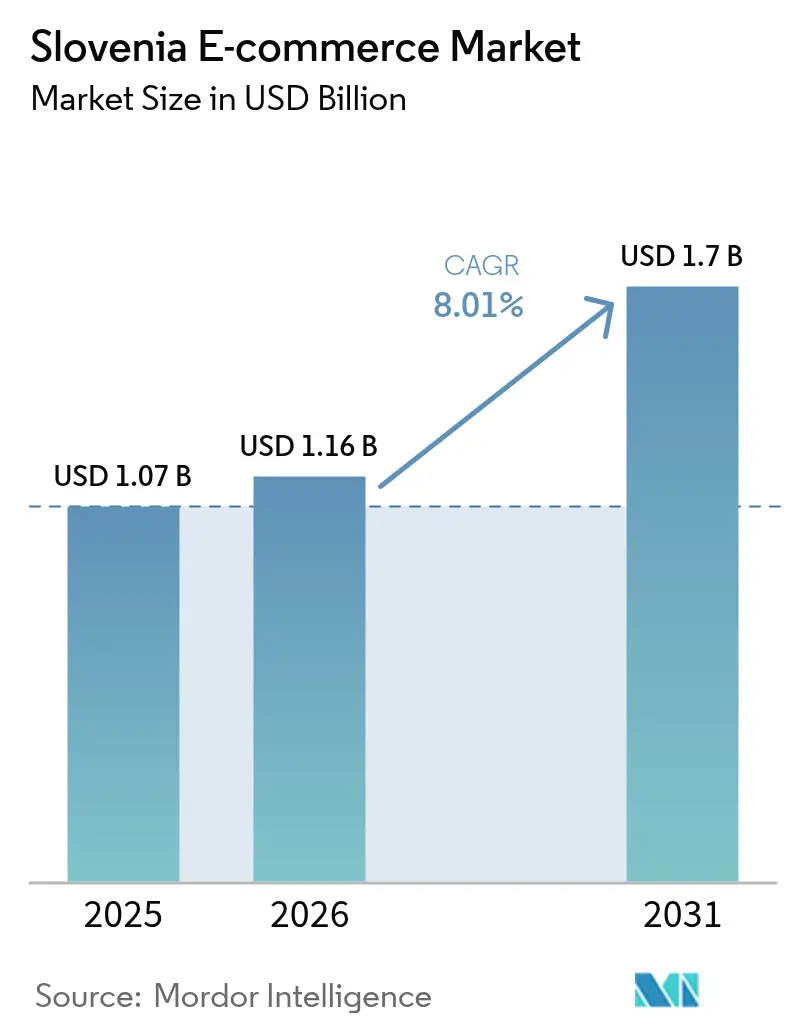

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.7 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

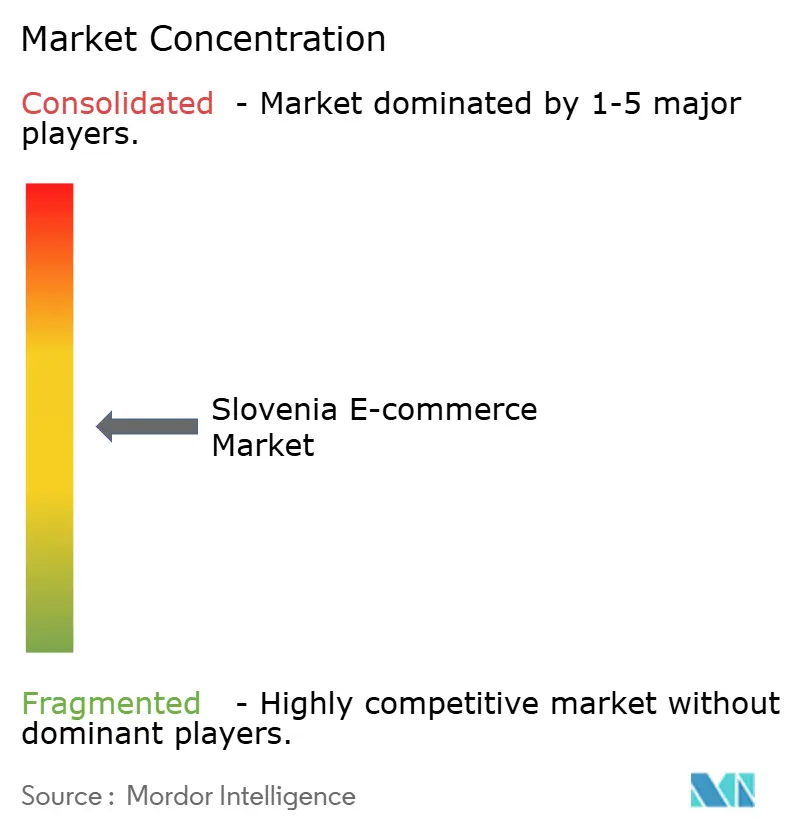

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Slovenia E-commerce Market Analysis by Mordor Intelligence

The Slovenia e-commerce market size was valued at USD 1.07 billion in 2025 and estimated to grow from USD 1.16 billion in 2026 to reach USD 1.7 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031). Faster broadband roll-outs, a 90% internet-user base among residents aged 16–74, and rising disposable incomes are driving the momentum. Mobile devices now originate more than 75% of site visits, prompting merchants to rebuild digital journeys around thumb-friendly interfaces and single-click payments. Domestic platforms still capture 77% of transactions, yet cross-border orders are climbing as EU Digital Single Market rules trim delivery frictions. Competitive intensity is escalating as global giants such as Amazon and AliExpress enter a landscape already contested by regional firms like About You and local leader Mimovrste. On the operations side, partnerships such as Pošta Slovenije–China Post are turning logistics sophistication into a key source of advantage. Although thin warehousing capacity and rural cash-on-delivery habits curb margins, EU-funded gigabit projects are laying the infrastructure for long-term growth in the Slovenia e-commerce market.[1]Statistični urad Republike Slovenije, “Spletno nakupovanje, 2023,” Statistični urad Republike Slovenije, stat.si.

Key Report Takeaways

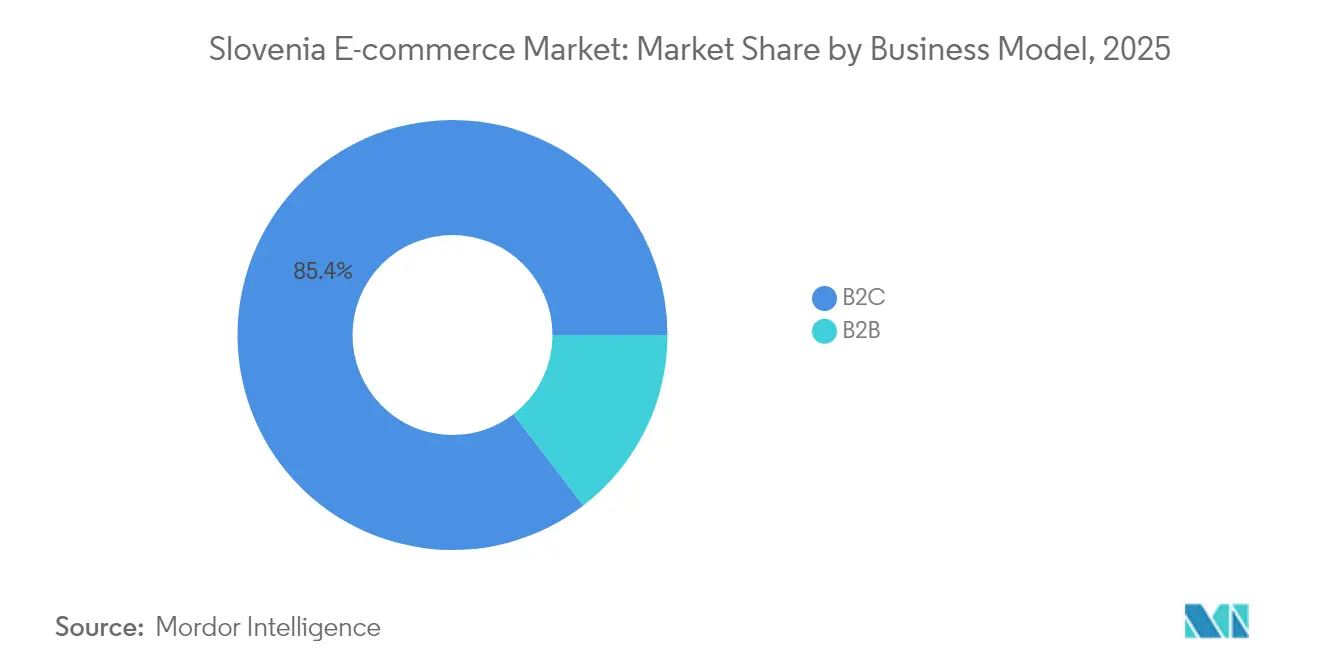

- By business model, the B2C segment commanded 85.42% revenue share in 2025, while B2B is projected to expand at a 9.54% CAGR through 2031.

- By device type, mobile commerce captured 74.88% of the Slovenia e-commerce market share in 2025 and is advancing at a 9.18% CAGR through 2031.

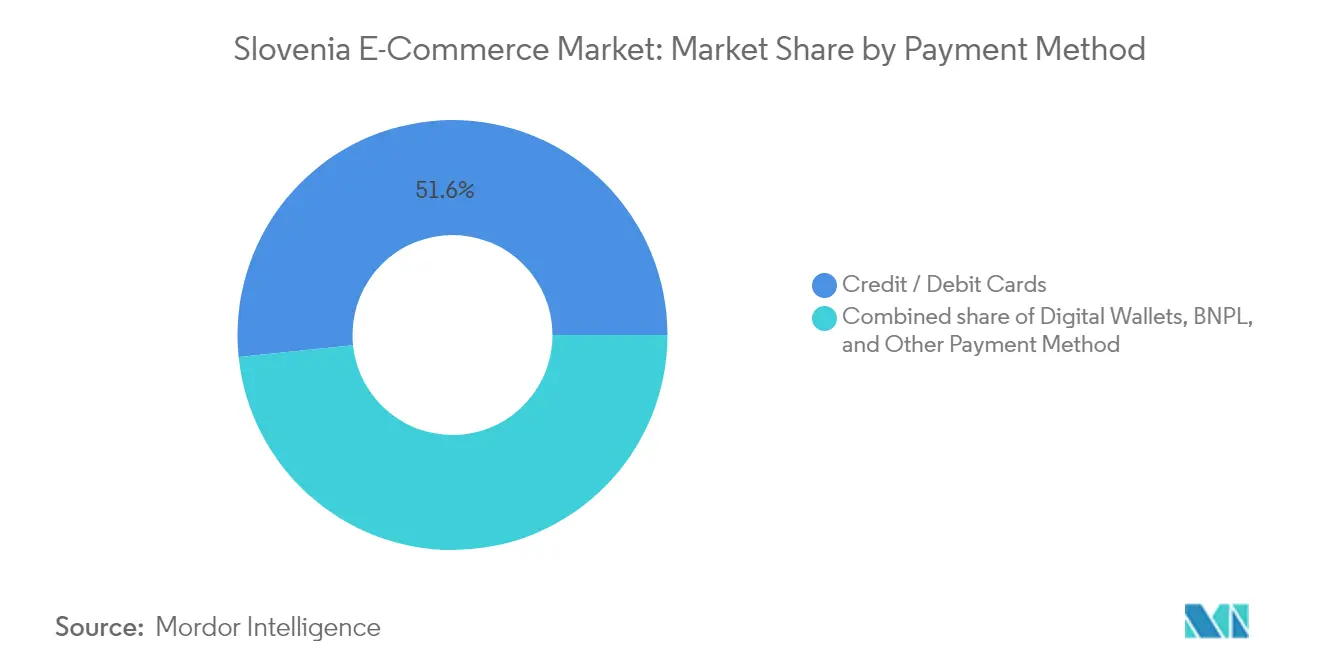

- By payment method, credit/debit cards led with 51.63% share in 2025; digital wallets exhibit the fastest trajectory at 10.39% CAGR to 2031.

- By product category, fashion & apparel secured 28.74% of 2025 revenue, whereas food & beverages is forecast to post a 12.22% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Slovenia E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated rollout of same-day delivery networks concentrated around Ljubljana | +1.8% | Urban centers, primarily Ljubljana with expansion to Maribor and Celje | Medium term (2-4 years) |

| Surge in mobile-only shoppers among Gen-Z & Millennial cohorts (≥70% of online traffic) | +2.1% | National, with higher concentration in urban areas | Short term (≤ 2 years) |

| Government-subsidised digital vouchers for SMEs adopting e-commerce platforms | +1.2% | National, with emphasis on less developed regions | Medium term (2-4 years) |

| Rapid penetration of BNPL (Buy-Now-Pay-Later) solutions led by Klarna & Leanpay | +1.5% | National, with higher adoption in urban centers | Short term (≤ 2 years) |

| Growth of cross-border shopping via EU Digital Single Market logistics corridors | +0.9% | National, with concentration along major transportation routes | Medium term (2-4 years) |

| EU cohesion-fund grants upgrading broadband to >1 Gbps in rural Slovenia | +0.6% | Rural regions, particularly in Alpine and eastern areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated rollout of same-day delivery networks

Same-day delivery is redefining service benchmarks in the Slovenia e-commerce market. Micro-fulfilment hubs positioned around Ljubljana shrink delivery windows below three hours, nudging consumers toward higher purchase frequency and bigger baskets. Logistics specialists are replicating the model in Maribor and Celje, widening the service footprint to roughly half the population. The April 2024 Pošta Slovenije–China Post alliance boosts cross-border parcel velocity, enabling Chinese sellers to treat Slovenia as a Central-European gateway. Retailers respond by integrating inventory visibility across stores and dark warehouses, reducing stock-outs and raising conversion rates. As service expectations climb, smaller merchants are outsourcing fulfilment to third-party logistics providers to stay competitive in the Slovenia e-commerce market.

Surge in mobile-only shoppers

Mobile screens now dominate the Slovenia e-commerce market, with 75.43% of traffic arriving via smartphones in 2024. Gen-Z and Millennials drive this shift, bypassing desktops altogether and elevating swipe-able interfaces as table stakes. Conversion funnels increasingly leverage biometric log-ins and digital wallets, trimming checkout steps to a few seconds. Retailers optimize search results for vertical scrolling patterns and embed shoppable videos to capture short attention spans. Mobile-driven demand concentrates order peaks in evening hours, prompting adaptive staffing in fulfilment centers. This behavioral sea change is pressuring legacy merchants to migrate from responsive sites to progressive web apps that mimic native-app speed without the download hurdle, preserving share in the Slovenia e-commerce market.

Government-subsidised digital vouchers

Digital vouchers worth EUR 1,000–9,999 (USD 1,083–10,815) co-finance website launches, cybersecurity upgrades, and marketing campaigns for SMEs. By lowering upfront technology outlays, the program has enrolled micro-enterprises in remote regions that previously lacked online channels. Voucher recipients must shoulder 40% of project costs, ensuring skin in the game while accelerating digital skills. Early beneficiaries report revenue lifts of 12–15% within one year, according to ministry monitoring. Platform vendors partner with local chambers of commerce to pre-package compliant SaaS storefront bundles, shortening deployment cycles to weeks. The subsidy pipeline consequently enlarges the addressable merchant base and injects fresh inventory into the Slovenia e-commerce market.[2]Government of the Republic of Slovenia, “Gigabit Infrastructure Development Plan 2030,” Government of the Republic of Slovenia, gov.si.

Rapid penetration of BNPL solutions

Klarna and home-grown Leanpay push flexible instalments to the mainstream, lifting conversion on higher-ticket items such as consumer electronics by double digits. BNPL apps increasingly double as discovery channels, recommending curated catalogues and steering demand toward partner merchants. Credit-risk algorithms that tap open-banking data enable near-instant approvals, marginalising traditional revolving credit cards. However, rising BNPL penetration raises regulatory oversight on responsible lending, compelling providers to invest in transparency dashboards and repayment-reminder tooling. Merchants welcome the uplift in average order value but face higher interchange fees, which they offset through pricing levers. Payment innovation thus reinforces spend velocity in the Slovenia e-commerce market. [3]European Commission, “Voucher Schemes in Member States,” European Commission, ec.europa.eu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile fulfilment costs for dispersed Alpine populations | -1.2% | Alpine regions and rural areas | Medium term (2-4 years) |

| Sub-scale domestic warehousing capacity versus seasonal demand spikes | -0.9% | National, with concentration in logistics hubs | Short term (≤ 2 years) |

| Low online basket value vs. Western Europe, squeezing retailer margins | -0.7% | National | Medium term (2-4 years) |

| Persistent preference for cash-on-delivery outside urban centres | -0.5% | Rural and suburban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High last-mile fulfilment costs

Mountainous terrain inflates route length and limits drop density, adding up to 30% on delivery expenses relative to Ljubljana. Couriers experiment with crowd-shipping, tapping commuters and retirees for parcel hand-offs, yet adoption remains patchy due to privacy worries and technology gaps. Retailers set higher free-shipping thresholds for remote postcodes, dampening basket growth. Drone pilot programs are under regulatory review but face payload limits. Until cost curves bend, fulfilment surcharges undermine price parity and restrain penetration in outlying districts of the Slovenia e-commerce market.

Sub-scale domestic warehousing capacity

Peak-season surges strain Slovenia’s modest inventory footprint, triggering stock-outs or costly short-term leases. Legacy facilities lack automation, resulting in lower pick rates and channel-wide delays. Investors now channel capital into multi-tenant warehouses with mezzanine floors and robotics-ready layouts, but capacity will trail demand through 2026. Merchants hedge by holding safety stock in neighbouring Austria and Italy, elongating replenishment cycles. These inefficiencies shave margin headroom in the Slovenia e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B momentum accelerates digital diversification

The B2C arm dominated revenue in 2025, holding 85.42% of spend as local shoppers embraced mobile-led convenience. This dominance lifted the Slovenia e-commerce market size for consumer retail to USD 0.91 billion, yet the corporate channel is gaining ground. The B2B sector is forecast to grow at 9.54% CAGR, outpacing headline expansion. Digital vouchers and favourable tax credits encourage SMEs to streamline procurement via online portals, trimming transaction overheads and broadening supplier options. Early movers in manufacturing tools and hospitality supplies record double-digit online conversion, signalling a structural shift toward platform purchasing.

Rising cross-border trade integration gives Slovenian exporters a cost-effective path to reach EU partners, underpinned by harmonised invoicing standards. Multi-language catalogues and embedded financing differentiate B2B platforms chasing higher-margin niches. As procurement officers prioritise speed and transparency, sellers deploy punch-out catalogues and API connections for real-time stock levels. This interoperability deepens wallet share and boosts the Slovenia e-commerce market in the enterprise segment.

By Device Type: Mobile commerce shapes the engagement blueprint

Smartphones generated 74.88% of traffic and 67.23% of sales in 2025, making mobile the undisputed gateway to the Slovenia e-commerce market. It has highest growth rate of 9.18%. Responsive layouts now give way to progressive web apps that pre-cache images for sub-second load times on 4G and emerging 5G networks. Retailers embed virtual try-ons and AR sizing guides to counter return risks, particularly in fashion and furniture. Meanwhile, desktops retain relevance for complex B2B configurations and multi-item cart assembly, indicating a bifurcated device journey.

Device convergence drives omnichannel behaviours: shoppers scan QR codes in physical stores to access richer online assortments, then finalise payment through mobile wallets. Push notifications re-engage dormant carts, leveraging precise geo-fencing to time offers during commute hours. Voice commerce remains nascent but is expected to capture incremental share as Slovene-language assistants reach critical accuracy. Consequently, mobile optimisation remains mission-critical for sustained growth of the Slovenia e-commerce market size in the years ahead.

By Payment Method: Digital wallets and BNPL recast checkout economics

Card rails still dominate with 51.63% share, yet wallet transactions surge as Apple Pay, Google Pay, and local schemes integrate instant SEPA transfers. Wallets post a forecast 10.39% CAGR, tightening settlement cycles and reducing chargeback exposure. The Slovenia e-commerce market share of BNPL climbed steadily, hitting mid-single-digit penetration within electronics and home appliances. Providers extend loyalty programmes, offering cashback on punctual instalments to reinforce repayment discipline.

Merchants deploy payment-orchestration platforms that route transactions dynamically to the lowest-cost processor, shaving fee expense. Strong Customer Authentication (SCA) mandates elevate the role of frictionless biometrics to maintain conversion parity with one-click cards. As digital wallets absorb identity and loyalty credentials, checkout flows compress to two taps, strengthening user lock-in across the Slovenia e-commerce market.

By B2C Product Category: Food & Beverages surges on delivery density

Fashion & apparel kept the revenue crown with 28.74% share in 2025, but food & beverages races ahead at a 12.22% CAGR. Regional grocers expand dark-store networks within a 10-kilometre radius of dense districts, slashing delivery windows below 60 minutes. Temperature-controlled tote systems preserve freshness, encouraging consumers to migrate weekly shops online. Electronics stay resilient as gamers and remote workers upgrade hardware, while homeware benefits from AR layout tools that shortcut the imagination gap.

Subscription beauty boxes combine AI-driven skin diagnostics with personalised replenishment schedules, lifting repeat rates. Toy and DIY categories leverage influencer tutorials and user-generated reviews to unlock cross-sell synergies. As assortment breadth widens and logistics performance solidifies, category diversification broadens the Slovenia e-commerce market’s addressable wallet share.

Geography Analysis

Proximity to major EU trade corridors bestows Slovenia with cross-border leverage, but internal demand still anchors the Slovenia e-commerce market. Metropolitan Ljubljana accounts for roughly 40% of national online spend, propelled by higher purchasing power and same-day fulfilment saturation. Maribor and Celje follow, aided by university demographics and growing warehouse clusters along the A1 motorway. Alpine municipalities exhibit lower order frequency due to delivery surcharges and patchy broadband, yet forthcoming fibre projects aim to close the gap.

EU cohesion funds of EUR 147 million (USD 159 million) earmarked in 2025 target fibre backbones and 5G rollout across underserved valleys, catalysing digital adoption. The RUNE rural network’s 1,600 km optical build will bring gigabit speeds to 52,000 homes, creating new demand pockets. Improved connectivity underpins video-rich product pages and live-shopping events, previously bandwidth-constrained.

Cross-border flows through the Port of Koper and rail links to Austria shorten inbound transit times for international sellers, enhancing category diversity. Slovenia’s inclusion in major international parcel networks positions it as a springboard for Central-European distribution. Domestic merchants leverage the same lanes to reach Italy, Croatia, and Hungary within 48 hours, monetising scale despite the country’s small population. This logistical fluidity cements Slovenia’s strategic role and sustains long-run growth in the Slovenia e-commerce market.

Competitive Landscape

Fragmentation defines the Slovenia e-commerce industry, with no single player holding more than mid-teens revenue share. Local players Mimovrste leads electronics and general merchandise through a blend of broad assortment and local service innovations such as the Smart! unlimited-delivery scheme. BigBang.si and Mercator.si follow, each leveraging offline footprints to offer click-and-collect options. International entrants Amazon, AliExpress, and Temu compete heavily on price breadth, forcing domestic operators to refine differentiation around customer service, faster delivery, and curated assortments.

Fashion competition tightened after Zalando’s EUR 1.1 billion (USD 1.19 billion) acquisition of About You, pooling inventory depth and marketing muscle. This consolidation raises customer-acquisition costs for smaller boutiques, prodding them to specialise in niche labels and local designers. Logistics capabilities emerge as a battleground; Pošta Slovenije’s partnership with China Post grants domestic sellers faster customs clearance and end-to-end tracking, while DHL’s takeover of IDS Fulfilment enriches value-added services such as returns processing and SME onboarding.

Investment flows signal confidence in the sector’s upside. Advance Capital Partners’ buyout of tourism operator Unitur integrates online booking engines with physical leisure assets, pointing to omnichannel synergies. InterCapital’s expansion into Slovenia supplies fresh capital for start-ups innovating in payment orchestration, last-mile robotics, and cross-border compliance. These moves collectively intensify rivalry yet lift customer expectations, fuelling advancement across the Slovenia e-commerce market.

Slovenia E-commerce Industry Leaders

Mimovrste d.o.o.

Merkur Trgovina d.o.o.

Big Bang d.o.o.

Petrol d.d.

Lekarna Nove Poljane

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Advance Capital Partners acquired Unitur, linking hospitality assets with online booking engines to capture bundled travel-plus-leisure demand and cross-sell ancillary services.

- May 2025: DHL bought IDS Fulfilment, extending flexible warehousing, returns management, and SME onboarding tools, reinforcing its value proposition in the Slovenia e-commerce market.

- April 2025: The Ministry of Cohesion and Regional Development allocated EUR 147 million (USD 159 million) to high-speed internet infrastructure, unlocking new rural customer pools and stimulating platform expansion.

- August 2024: Telemach Slovenia agreed to acquire telecom rival T-2, signalling potential bundled broadband-plus-e-commerce offerings that could reshape traffic acquisition dynamics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Slovenia's e-commerce market as all value generated when goods or services are ordered via digital interfaces and paid for online or on delivery, irrespective of fulfillment mode. Revenue streams cover both B2C and B2B transactions that originate within Slovenia's borders, are billed in any currency, and are recorded net of VAT.

Scope exclusion: Pure digital-content subscriptions, informal peer-to-peer swaps, and in-app micro-payments that never reach a checkout screen are omitted.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed logistics integrators, e-tail founders, payment specialists, and digital-marketing agencies across Ljubljana, Maribor, and Celje. Guided conversations validated consumer conversion rates, SME onboarding costs, and expected BNPL penetration, bridging gaps that static datasets could not fill.

Desk Research

We began with broad desk work drawing on open data from the Statistical Office of the Republic of Slovenia, Eurostat's ICT use surveys, the Ministry of Digital Transformation's fiber rollout briefs, and trade association updates from Ecommerce Europe. Company filings and investor decks supplied fresh GMV splits, while news archives on Dow Jones Factiva and shipment tallies on Volza helped ground cross-border volumes. These and many other secondary sources informed baseline indicators, trend breakpoints, and regulatory context.

A second sweep targeted category fingerprints such as card-versus-wallet payment shares, parcel drop density, and average transaction values published by Bank of Slovenia, Pošta Slovenije, and telecom regulator AKOS. The list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

We applied a top-down build anchored on official web-sales turnover, reconstructed through production and trade data before being further filtered through shopper penetration and purchase frequency. Supplier roll-ups and sampled ASP × parcel volumes offered bottom-up cross-checks that nudged totals where misalignments appeared. Key variables like smartphone penetration, cross-border order share, delivery-network reach, disposable income per capita, and digital-wallet adoption shape yearly values. Forecasts run on a multivariate regression with scenario overlays that incorporate macro trends and expert consensus. Any blind spot in sub-segments is adjusted using proxy ratios from proximate EU markets of similar size.

Data Validation & Update Cycle

Outputs pass three analyst reviews, variance thresholds trigger re-checks with interviewees, and currency conversions are frozen at yearly average rates. We refresh the model each year and issue interim updates when material events, policy shifts, tax rate changes, or landmark M&A occur.

Why Mordor's Slovenia E-commerce Baseline Commands Reliability

Published estimates often diverge because firms carve different boundaries, pick unlike base years, or stretch local data with aggressive regional multipliers. Our disciplined scope selection and annual refresh cadence keep our baseline anchored in locally reported web sales that are then reconciled with operator level insights.

Key gap drivers include whether B2B transactions are counted, if returns are netted, the mix of goods versus services, and how foreign-currency flows are restated. Some publishers lean on straight-line extrapolations from older Statista panels, while others apply global ASP curves that overlook Slovenia's higher average basket.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.07 B (2025) | Mordor Intelligence | - |

| USD 0.60 B (2024) | Regional Consultancy A | Excludes B2B flows and nets out marketplace commission, leading to smaller base |

| USD 0.97 B (2024) | Trade Journal B | Uses Statista revenue only, assumes flat cross-border share, no primary validation |

These comparisons show that by blending official turnover data with ground-level interviews, Mordor Intelligence delivers a balanced, transparent figure clients can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How fast is the Slovenia e-commerce market expected to grow between 2026 and 2031?

It is projected to expand at an 8.01% CAGR, rising from USD 1.16 billion in 2026 to USD 1.7 billion by 2031.

Which business model is expanding the quickest in Slovenian online retail?

The B2B segment is set to grow at 9.54% CAGR, benefiting from government vouchers that subsidise SME digital upgrades.

What share of online orders originates from mobile devices?

Smartphones generated 74.88% of e-commerce traffic in 2025 and are forecast to sustain a 9.18% CAGR through 2031.

Which payment method is gaining momentum most rapidly?

Digital wallets are the fastest-growing option, recording a projected 10.39% CAGR and challenging the 51.63% card share.

Why is food & beverage the breakout product category?

Investments in same-day grocery delivery, particularly around Ljubljana, are pushing the category to a 12.22% CAGR up to 2031.

What infrastructure projects support future e-commerce penetration in rural Slovenia?

EU-funded fibre deployments aim for 100 Mbps coverage by 2025 and gigabit speeds by 2030, widening access for 52,000 rural households.

Page last updated on: