Polyvinylidene Fluoride (PVDF) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

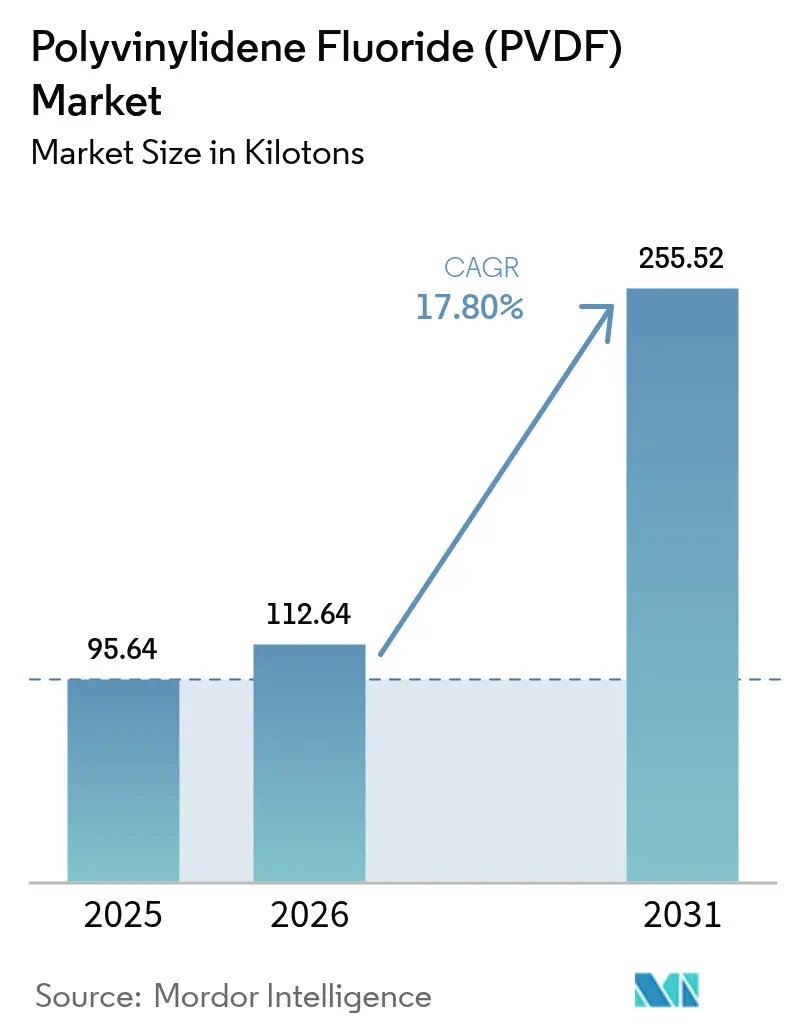

| Market Volume (2026) | 112.64 kilotons |

| Market Volume (2031) | 255.52 kilotons |

| Growth Rate (2026 - 2031) | 17.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyvinylidene Fluoride (PVDF) Market Analysis by Mordor Intelligence

The Polyvinylidene Fluoride Market size is projected to be 95.64 kilotons in 2025, 112.64 kilotons in 2026, and reach 255.52 kilotons by 2031, growing at a CAGR of 17.80% from 2026 to 2031. Government incentives for electric-vehicle batteries, sovereign semiconductor programs, and green-hydrogen infrastructure are synchronizing to lift baseline consumption across every major region. Integrated fluorochemical producers are scaling captive vinylidene fluoride (VDF) output to buffer feedstock risk even as non-integrated converters seek long-term supply contracts that stabilize raw-material costs. Regulatory divergence—tightening PFAS rules in North America and Europe versus capacity-first policies in Asia-Pacific—creates flexible pricing corridors that favor suppliers able to switch volumes across continents. Intensifying competition from water-borne binders and alternative fluoropolymers is real, yet current technical limitations at high voltage and temperature preserve PVDF’s dominance in premium battery chemistries and semiconductor clean-room plumbing.

Key Report Takeaways

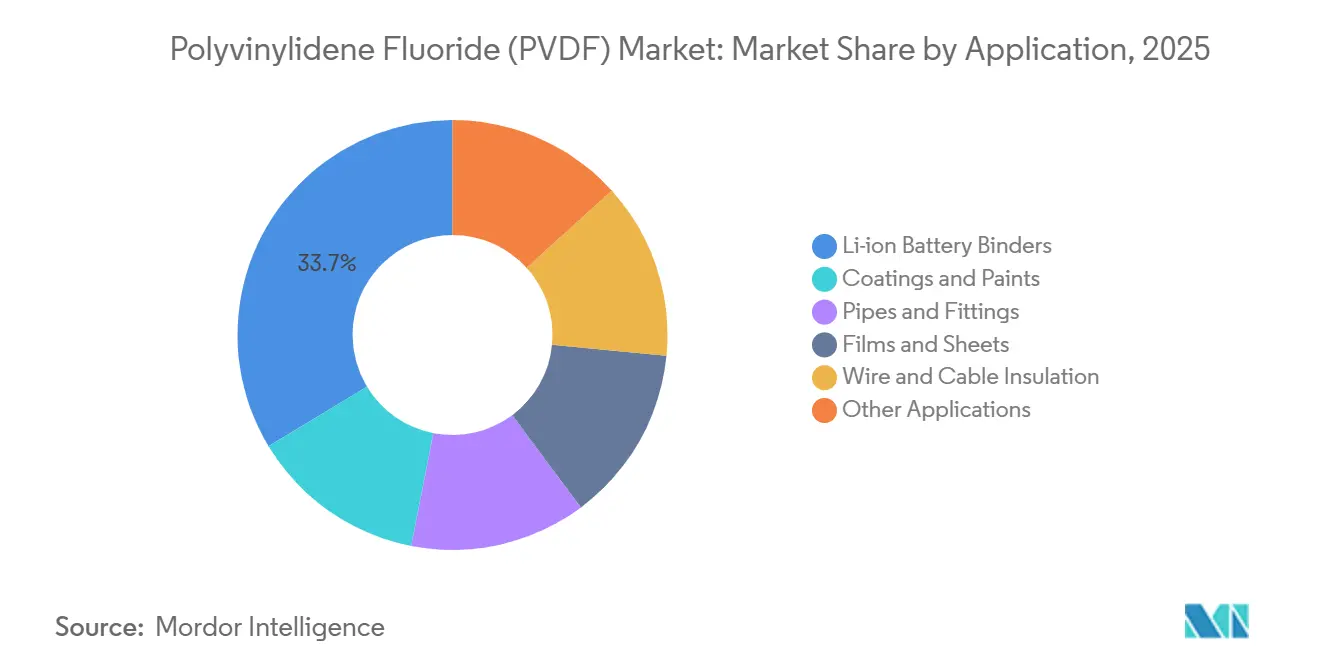

- By application, Li-ion battery binders accounted for a 33.65% share in 2025; the segment is forecast to advance at a 29.18% CAGR through 2031.

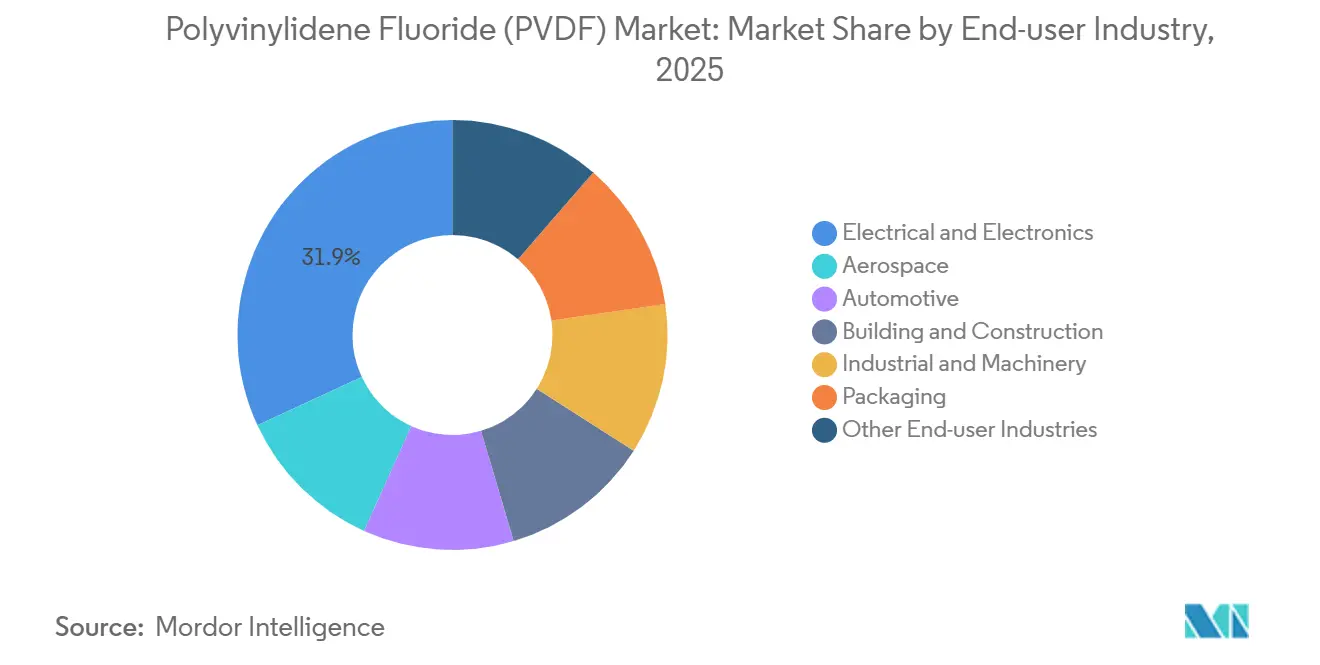

- By end-user industry, electrical and electronics led with 31.90% share in 2025, while automotive is projected to grow at a 26.12% CAGR through 2031.

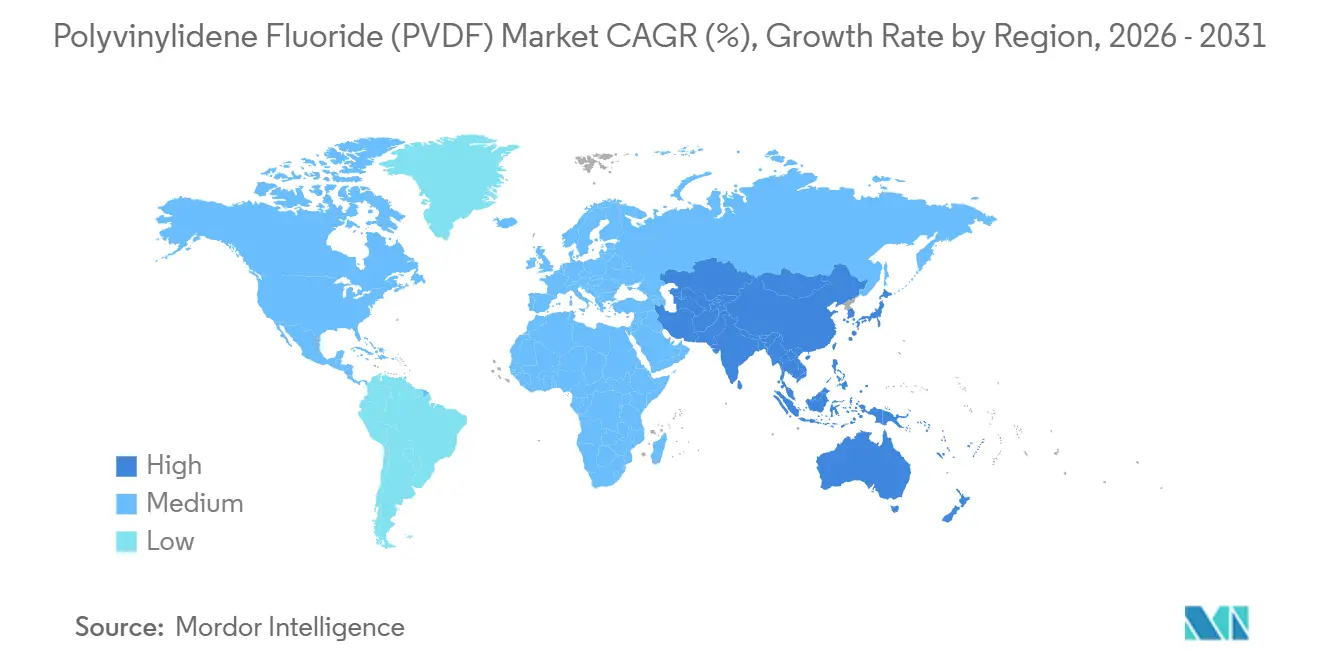

- By geography, Asia-Pacific commanded a 56.15% share in 2025 and is set to progress at a 20.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyvinylidene Fluoride (PVDF) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-battery production surge | +8.2% | APAC core (China, South Korea, Japan), spill-over to North America and EU | Medium term (2-4 years) |

| Demand for chemical-resistant architectural coatings | +2.1% | Global, with concentration in the Middle East, Southeast Asia industrial corridors | Long term (≥ 4 years) |

| Semiconductor clean-room capacity build-out | +3.5% | APAC (Taiwan, South Korea, Japan), North America (Arizona, Ohio), EU (Germany) | Medium term (2-4 years) |

| Water-treatment membrane retrofits in Asia | +1.8% | APAC (China, India, Southeast Asia), Middle East, GCC states | Long term (≥ 4 years) |

| Rapid adoption of PVDF-lined electrolyzers for green-hydrogen | +2.4% | EU, North America, APAC (Australia, Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Battery Production Surge

Global lithium-ion cell capacity is expected to grow significantly by 2030, requiring PVDF binder at today’s loading rates. High-nickel NMC and NCA cathodes demand molecular-weight ranges above one million daltons, a specification that water-borne binders cannot yet match over extended cycling. The U.S. Inflation Reduction Act steers domestic cell plants toward regionally made PVDF, opening doors for Arkema’s Pennsylvania line.

Demand for Chemical-Resistant Architectural Coatings

Facades treated with PVDF coatings boast lifespans of 20 to 30 years, even when exposed to intense UV rays and corrosive environments. Demand in the region surged, spurred by projects like Saudi Arabia's NEOM and the industrial corridors of the UAE, with specifications aligning with ASTM D3359 and D4214 standards. Leading the market, Syensqo's Hylar 5000 and Arkema's Kynar 500 capitalize on decades of field data, a resource newer suppliers haven't yet acquired. Meanwhile, solvent-borne variants grapple with tightening VOC regulations in California and various EU nations. This regulatory pressure is steering formulators towards water-dispersible PVDF emulsions, which offer a slight trade-off in durability for enhanced compliance.

Semiconductor Clean-Room Capacity Build-Out

Set to commence full production in 2026, Taiwan Semiconductor Manufacturing Company's Arizona plant has chosen PVDF pipes and fittings for its wet-process loops. The U.S. CHIPS and Science Act allocated a substantial amount for semiconductor fabs. In a show of confidence, industry giants Intel, Samsung, and Micron collectively unveiled plans for new facilities, slated between 2024 and 2026, each projected to require PVDF. Meanwhile, Japan's Rapidus, bolstered by significant subsidies, is poised to demand even more supply as its construction phase reaches its zenith.

Rapid Adoption of PVDF-Lined Electrolyzers for Green Hydrogen

Proton-exchange membrane stacks operate in corrosive conditions, running below pH 2 and at temperatures reaching 90 °C, which typically damage most metals and plastics. Currently, PVDF accounts for a significant portion of stack costs. However, its acid resistance and mechanical strength play a pivotal role in shaping total-cost-of-ownership models. The U.S. Hydrogen Shot initiative targets a price of hydrogen by 2031. This goal necessitates keeping equipment capital costs within a specific range. As a result, suppliers are in a race to qualify lower-cost PVDF grades, all while ensuring they don't compromise on the essential 10-year durability. Meanwhile, Europe's Hydrogen Backbone has laid out plans for pipelines, with the majority specifying compressors lined with PVDF.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material (VDF) price volatility | -3.1% | Global, with acute impact on non-integrated producers in North America and EU | Short term (≤ 2 years) |

| PFAS-related regulatory scrutiny in EU and US | -2.7% | EU, North America, with spillover to export-oriented APAC producers | Medium term (2-4 years) |

| Emerging water-borne binder chemistries eroding PVDF share | -1.5% | APAC entry-level EV segment, North America cost-sensitive applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

In Asia, VDF spot prices climbed in early 2025 after two Chinese hydrofluoric-acid outages, slicing converter margins. Integrated players cushioned the spike through captive fluorspar mining, while European merchant producers swung to operating losses. With China controlling a significant portion of global fluorspar, geopolitical friction remains a headline risk[1]U.S. Geological Survey, “Mineral Commodity Summaries: Fluorspar,” usgs.gov.

PFAS-Related Regulatory Scrutiny

By 2028, the European Chemicals Agency's proposed universal PFAS restriction could ban specific PVDF grades from coatings and textiles, shifting those volumes to Asia[2]U.S. Environmental Protection Agency, “PFAS National Primary Drinking Water Regulation,” epa.gov. In April 2024, the U.S. Environmental Protection Agency imposed a limit on PFOA and PFOS in drinking water, leading to supply-chain audits that strain smaller producers. Compliance costs, covering emissions monitoring and research into alternative chemistries, could reinforce the competitive edge of established players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Battery Binders Dominate, Membranes Accelerate

Li-ion battery binders commanded 33.65% of the polyvinylidene fluoride (PVDF) market share in 2025, and this slice is expected to expand at a 29.18% CAGR through 2031. The market size for battery binders in the PVDF sector is set to expand, driven by the need for polymer stability above 150 °C in high-nickel cathodes, which are sensitive to thermal drift. While coatings stand as the second-largest application, stringent solvent regulations in mature regions limit their growth. In contrast, pipes and fittings, especially those associated with semiconductor and chemical plants, are witnessing more consistent gains. PVDF films, used in photovoltaic backsheets and lithium separators, hold potential but are challenged by the cost-effectiveness of polyethylene in budget-conscious solar initiatives.

The rising adoption of membranes in desalination and industrial water treatment is bridging the gap. Significant facilities utilize PVDF hollow fibers annually. Meanwhile, retrofits in Indian municipalities, driven by the Jal Jeevan Mission, have spurred additional annual demand. Despite competition from alternative fluoropolymers in specialized areas, PVDF's unique blend of chemical resistance, weldability, and enduring creep strength ensures its continued prominence on specification lists.

By End-User Industry: Automotive Surges, Electronics Holds Share

The Polyvinylidene Fluoride (PVDF) market size allocated to automotive is set to more than triple by 2031 on a 26.12% CAGR, reflecting cathode-binder needs in EV gigafactories across China, South Korea, and North America. Electrical and electronics retained 31.90% of the 2025 volume thanks to semiconductor, circuit board, and consumer device demand. Building and construction rely on PVDF-coated cladding and corrosion-proof piping in coastal skyscrapers, while industrial machinery specifies the polymer in pumps and valves carrying acids and caustics.

Aerospace and pharmaceutical packaging carve out lucrative niches in the market. Aircraft manufacturers, adhering to FAA standards, trust low-smoke PVDF wire insulation, using over 200 km of it for each wide-body jet's cabling. In the pharmaceutical realm, blister packs leverage PVDF’s moisture barrier properties and chemical inertness, ensuring shelf lives extend beyond three years. Such specialized applications provide a buffer against fluctuations in feedstock costs, safeguarding profit margins.

Geography Analysis

Asia-Pacific held 56.15% of the Polyvinylidene Fluoride (PVDF) market volume in 2025 and is tracking a 20.25% CAGR through 2031. Notably, China produced a significant volume of lithium-ion cells, utilizing a substantial amount of binder. Meanwhile, India's ambitious semiconductor incentive is set to draw in PVDF pipes and filters for new fabs slated to come online by 2027. South Korea's exports of lithium-ion cells surged, with industry giants strategically diversifying their PVDF sourcing to mitigate geopolitical risks.

North America accounted for a notable share of the global demand in 2025. Thanks to the Inflation Reduction Act’s domestic-content stipulations, Arkema’s Marcus Hook site emerged as the region’s sole integrated supplier, transitioning from VDF to PVDF. This strategic positioning allows them to command a premium over imports, which are subject to tariffs. Canada's strategy on critical minerals aligns seamlessly with the construction of U.S. gigafactories. At the same time, Mexico's automotive sector, boasting a significant base, is pivoting towards hybrid drivetrains. These drivetrains necessitate PVDF for coil-winding insulation and battery enclosures.

Europe secured a notable share of the PVDF volume in 2025. However, uncertainty surrounding the PFAS policy has created a rift in the market. While the demand for PVDF in semiconductors and medical devices continues to rise, there's apprehension over discretionary coatings, which might face a ban by 2028 under the draft PFAS legislation. In a move towards sustainable practices, Germany is piloting pyrolysis projects aiming for a significant recovery of VDF from scrap PVDF, marking a significant stride towards circular supply chains. Meanwhile, the smaller yet rapidly expanding segments in South America and the Middle East-Africa are leveraging PVDF for critical applications. These include subsea cables, desalination plants, and hydrogen pipelines, all of which are pivotal to Saudi Arabia and the United Arab Emirates' Vision 2030 aspirations.

Competitive Landscape

The polyvinylidene fluoride is moderately consolidated. In 2024, Chinese players boosted their nameplate capacity and managed to undercut global prices through strategic tolling agreements. The focus of intellectual property has shifted to particle-size distribution and dispersion stability. Emulsions below 200 nm are now enabling thinner cathode coatings, leading to an increase in energy density. Recycling emerges as the next big challenge: currently, only a small percentage of end-of-life PVDF is salvaged. However, if depolymerization methods are successfully scaled, they could potentially reduce virgin feedstock costs.

Polyvinylidene Fluoride (PVDF) Industry Leaders

Arkema

Syensqo

Dongyue Group

Kureha Corporation

Zhejiang Juhua Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Syensqo signed multi-year contracts to supply its battery-grade Solef Polyvinylidene Fluoride (PVDF) to automotive OEMs and battery manufacturers. Solef PVDF, a thermoplastic fluoropolymer, plays a vital role in lithium-ion batteries, enhancing the adhesion of separators to electrodes and the performance of binders.

- February 2025: Arkema announced plans to increase its PVDF capacity by 15% at its Calvert City, Kentucky, facility, supported by an investment of approximately USD 20 million. This move aims to cater to the surging demand for domestically produced high-performance resins, pivotal for lithium-ion batteries, and to address the expanding needs of the semiconductor and cable sectors.

Global Polyvinylidene Fluoride (PVDF) Market Report Scope

Polyvinylidene Fluoride (PVDF) is defined as a high-performance thermoplastic fluoropolymer known for its outstanding chemical resistance, thermal stability, and piezoelectric properties in its 𝛽-phase. It is widely used in industries such as aerospace, automotive, and electronics due to its durability, weatherability, and critical role as an electrode binder in Li-ion batteries.

The market is segmented by application, end-user industry, and geography. By application, the market is segmented into Li-ion Battery Binders, Coatings and Paints, Pipes and Fittings, Films and Sheets, Wire and Cable Insulation, and Other Applications (e.g., Membranes). By end-user industry, the market is segmented into Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-user Industries. The report also covers the market size and forecasts for the market in 20 countries across the major regions. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Li-ion Battery Binders |

| Coatings and Paints |

| Pipes and Fittings |

| Films and Sheets |

| Wire and Cable Insulation |

| Other Applications (Membranes, etc.) |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| Italy | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Li-ion Battery Binders | |

| Coatings and Paints | ||

| Pipes and Fittings | ||

| Films and Sheets | ||

| Wire and Cable Insulation | ||

| Other Applications (Membranes, etc.) | ||

| By End-user Industry | Aerospace | |

| Automotive | ||

| Building and Construction | ||

| Electrical and Electronics | ||

| Industrial and Machinery | ||

| Packaging | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyvinylidene fluoride market.

- Resin - Under the scope of the study, virgin polyvinylidene fluoride resin in the primary forms such as powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms