Polyvinyl Alcohol (PVA) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

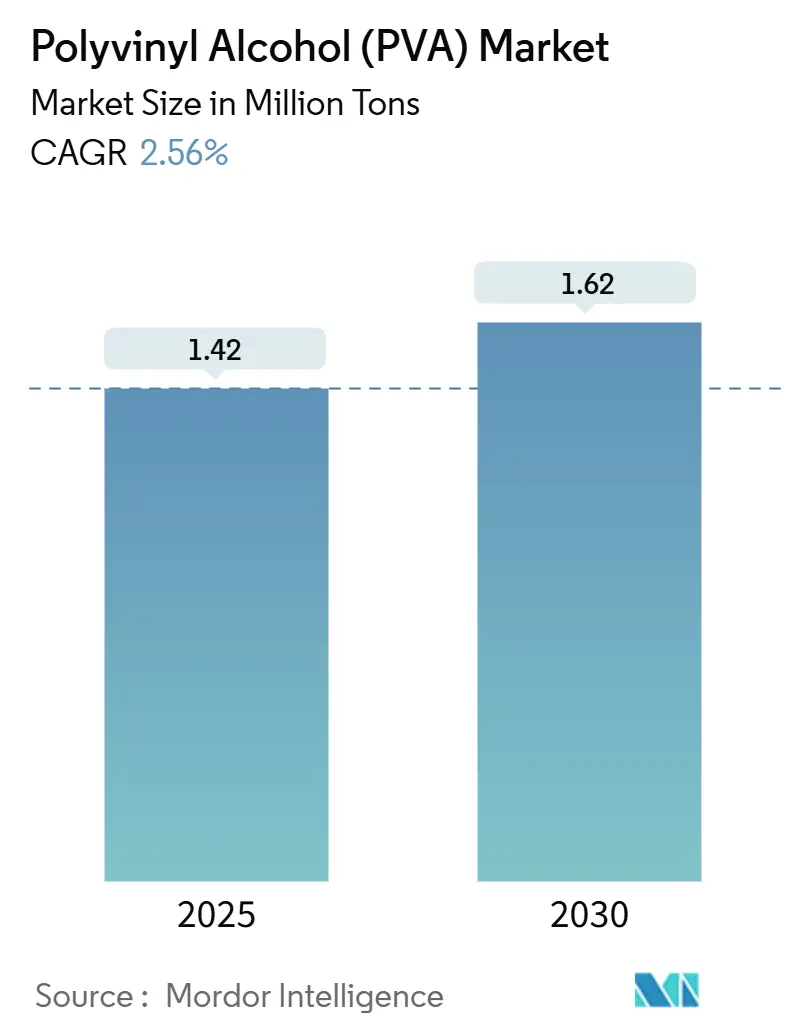

| Market Volume (2025) | 1.42 Million tons |

| Market Volume (2030) | 1.62 Million tons |

| Growth Rate (2025 - 2030) | 2.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polyvinyl Alcohol (PVA) Market Analysis by Mordor Intelligence

The Polyvinyl Alcohol Market size is estimated at 1.42 Million tons in 2025, and is expected to reach 1.62 Million tons by 2030, at a CAGR of 2.56% during the forecast period (2025-2030). Demand is underpinned by sustainability mandates in packaging, expanding construction activity, and steady uptake in detergent pods, emulsion polymers, and technical textiles. Water-soluble films are accelerating most rapidly as brand owners replace legacy plastics, while partially hydrolyzed grades dominate volumes by balancing solubility with mechanical strength. Asia-Pacific retains its leadership position thanks to large-scale capacity, proximity to raw materials, and a robust downstream manufacturing base. Price volatility in vinyl acetate monomer (VAM) continues to pressure producer margins, prompting strategic moves toward higher-value PVA formats and supply-chain integration.

Key Report Takeaways

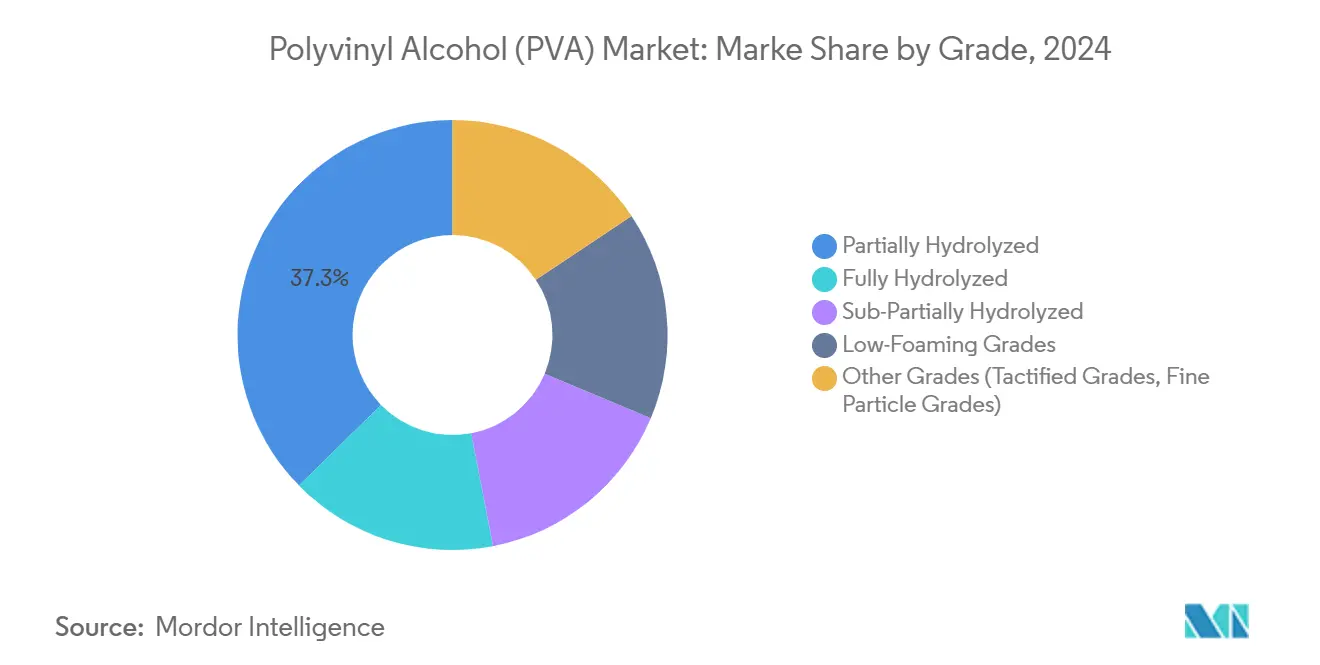

- By grade, partially hydrolyzed PVA held 37.34% of the polyvinyl alcohol market share in 2024 and is expanding at 2.96% CAGR through 2030.

- By form, powders accounted for 54.15% of the polyvinyl alcohol market size in 2024, whereas water-soluble films are advancing at 3.31% CAGR.

- By application, polymerization additives led with 24.45% revenue share in 2024; developing applications are set to grow at 4.44% CAGR to 2030.

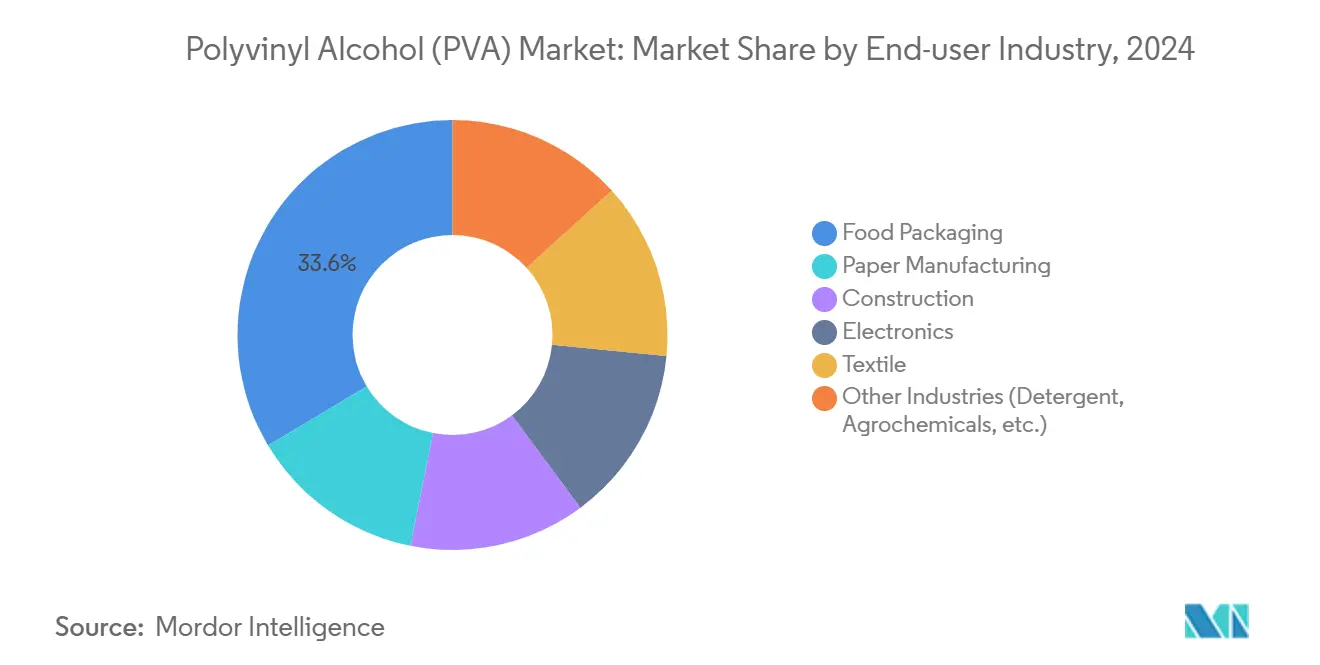

- By end-use industry, food packaging captured 33.59% revenue in 2024 and is rising at 2.97% CAGR, the fastest among all industries.

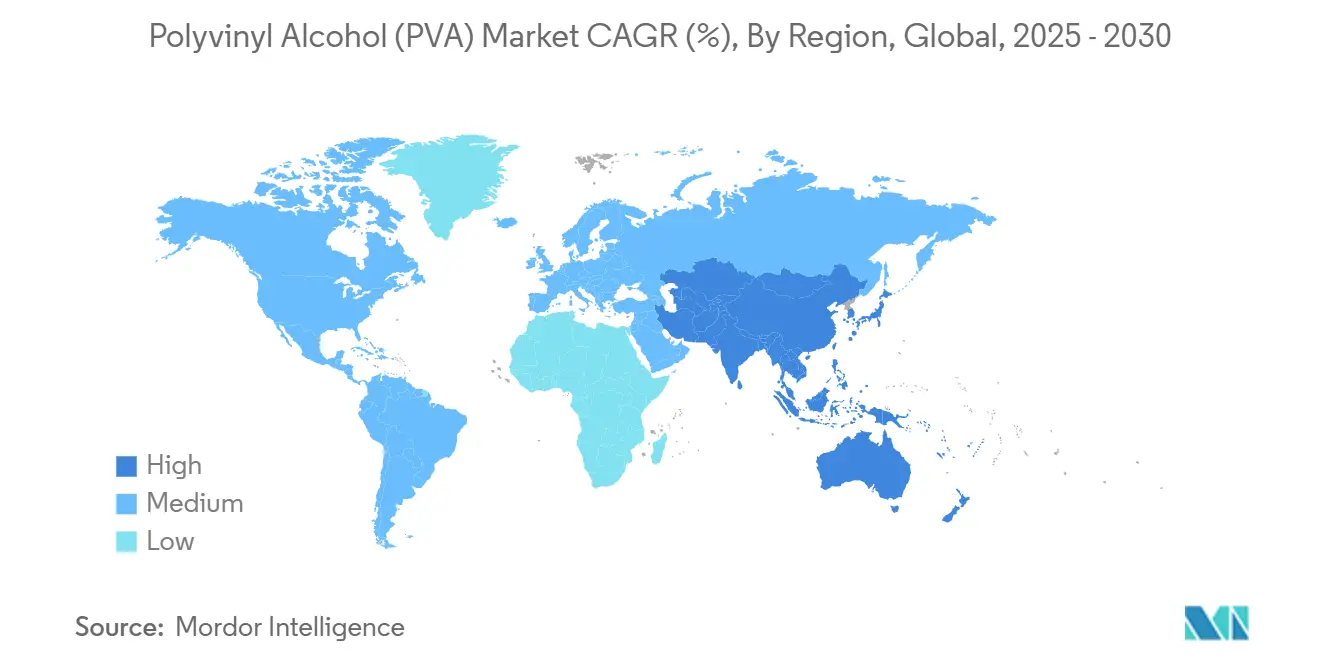

- By geography, Asia-Pacific commanded 47.51% of the polyvinyl alcohol market in 2024 and is growing at a 2.89% CAGR.

Global Polyvinyl Alcohol (PVA) Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on Market CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand From the Food Packaging Industry | +0.8% | Global, with acceleration in Europe and North America | Medium term (≈3-4 yrs) |

| Increasing Usage in the Construction Industry | +0.5% | Asia-Pacific, North America | Long term (≥5 yrs) |

| Growing Demand in Detergent Pods and Water-Soluble Films | +0.7% | Europe, North America, with emerging adoption in Asia-Pacific | Short term (≤2 yrs) |

| Increasing Demand for Emulsion Polymers | +0.4% | Global, with a concentration in Asia-Pacific | Medium term (≈3-4 yrs) |

| Rising Utilization from the Textile Industry | +0.3% | Asia-Pacific, particularly China, India, and Southeast Asia | Medium term (≈3-4 yrs) |

Source: Mordor Intelligence

Growing Demand from the Food Packaging Industry

Brand owners are switching to PVA-based materials to meet stricter sustainability targets and consumer preferences for low-impact packaging. The polymer provides excellent oxygen and grease barriers, extending shelf life and reducing food waste. Recent multi-layer PVA-cellulose composites meet TAPPI T 559 cm-12 for oil resistance without relying on PFAS, showcasing their regulatory advantage. PVA’s compatibility with circular-economy recycling streams further differentiates it from conventional plastics. These strengths position the material as a preferred substrate in fresh-produce wraps, microwave-safe films, and lightweight barrier structures.

Increasing Usage in the Construction Industry

PVA fibers are increasingly blended into concrete, where they raise tensile strength by up to 38% and flexural strength by 66%, improving structural durability in bridges, tunnels, and high-rise projects. Lightweight concrete formulations as low as 1.0 g/cm³ density have been achieved using PVA under high-temperature curing, cutting transport loads and embodied carbon. Infrastructure spending in Asia and government green-building incentives in North America support long-term growth. Contractors value PVA’s crack-bridging ability, which lowers maintenance costs over a structure’s life cycle.

Growing Demand in Detergent Pods and Water-Soluble Films

Unit-dose cleaning products rely on PVA films that fully dissolve during wash cycles, giving consumers a no-mess, exact-dose format while eliminating outer plastic wrappers. Concerns about microplastic release are sparking parallel research and development; for example, Dirigo Sea Farms is scaling kelp-based pod substrates for a 2026 launch[1]Maine Public, “Amid concern over microplastics, a Maine company creates a kelp-based laundry pod alternative,” mainepublic.org. This competitive pressure is nudging PVA suppliers toward faster-dissolving and higher-purity grades that pass stringent wastewater assessments.

Increasing Demand for Emulsion Polymers

PVA is widely used as a protective colloid in vinyl acetate ethylene (VAE) and other emulsion systems. Capacity expansion of 70 kilotons at Celanese’s Nanjing site underscores rising demand for redispersible polymer powders (RDP) used in tile adhesives and self-leveling floors. Paint and coating producers also leverage PVA-stabilized emulsions to achieve low-VOC profiles, aligning with tightening building-code requirements. This dynamic strengthens forward integration opportunities between PVA producers and downstream adhesive formulators.

Restraint Impact Analysis

| Restraints | (~) % Impact on Market CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Vinyl Acetate Monomer Prices in China | -0.6% | Global, with highest impact in Asia-Pacific | Short term (≤2 yrs) |

| Availability of Suitable Alternatives | -0.4% | Europe, North America | Medium term (≈3-4 yrs) |

| Limited Recycling Infrastructure for PVA Films | -0.2% | Emerging economies | Long term (≥5 yrs) |

Source: Mordor Intelligence

Volatile Vinyl Acetate Monomer Prices in China

Rapid capacity additions alongside demand swings have made VAM pricing unpredictable, eroding margins for commodity-grade producers. Chinese PVA plants, responsible for a large share of global output, face cost spikes that ripple through export markets. Integrated chemical majors are countering volatility by adding acetyl-chain capacity in other regions, such as Celanese’s 1.3-million-ton acetic acid project in Texas. Still, near-term cost instability deters capacity debottlenecking and prompts a shift toward higher-margin specialty grades.

Availability of Suitable Alternatives

Bio-based polymers are winning share in applications where full biodegradation is mandated, and recyclable polyethylene blends threaten PVA in certain barrier-film niches. Laundry-pod markets may also pivot to alginate or kelp films as environmental scrutiny intensifies. As converters test drop-in substitutes that meet the same barrier and sealability thresholds, PVA suppliers must accelerate material improvements and demonstrate end-of-life advantages to preserve incumbent positions.

Segment Analysis

By Grade: Versatility Propels Partially Hydrolyzed Leadership

Partially hydrolyzed grades captured 37.34% of the 2024 volume, giving them the largest polyvinyl alcohol market share and the fastest 2.96% CAGR outlook. Their balanced solubility lets converters fine-tune viscosity in adhesives, paper coatings, and textile sizing. Fully hydrolyzed variants serve niche electronic and pharmaceutical binders that require higher crystallinity. Low-foaming and fine-particle products are gaining popularity where defect-free coatings and high surface area are essential.

The polyvinyl alcohol market benefits from producers tailoring degree-of-polymerization and hydrolysis to specific end uses. Specialty chemistries provide moisture sensitivity control, permit higher solids processing, and enable faster film formation. As raw-material prices fluctuate, margin resilience hinges on differentiated grades that solve customer pain points and deliver consistent batch-to-batch quality.

Note: Segment shares of all individual segments available upon report purchase

By Form: Powder Dominance Paired with Film Acceleration

Powder remains the workhorse with 54.15% of the 2024 volume. Its long shelf life, easy re-dispersion, and lower freight costs suit bulk applications such as construction admixtures and paper surface sizing. Films, however, are the fastest growing at 3.31% CAGR as sustainability pressures favor water-soluble unit doses and PFAS-free barrier wraps. The polyvinyl alcohol market size for film formats will expand substantially as e-commerce and convenience packaging proliferate.

Granules provide dust-free handling in automated compounding lines, while fibers open high-margin routes in cement reinforcement, ropes, and filtration media. Kuraray’s KURALON exemplifies technical fibers that deliver tensile strength, alkali resistance, and bonding capability to concrete and geotextiles. Form diversification improves portfolio resilience by balancing commodity volumes with specialty niches.

By Application: Developing Uses Outpace Traditional Segments

Polymerization additives led 2024 volume at 24.45%, relying on PVA’s colloidal stabilization during emulsion polymer production. Yet developing applications such as bioelectronics, fuel-cell membranes, and advanced hydrogels are rising at 4.44% CAGR, showing the polyvinyl alcohol market’s ability to capture cutting-edge technologies. Controlled amorphous-crystalline transitions now support miniaturized hydrogel sensors and flexible circuits[2]Nature Communications, “Control of polymers’ amorphous-crystalline transition enables miniaturization,” nature.com.

PVB interlayers for safety glass, adhesives for wood lamination, and sizing agents for warp-yarns remain significant, underscoring PVA’s multifunctional heritage. The polyvinyl alcohol market size for fuel-cell membranes is small today, but can grow as methanol-resistant blends offer cost-effective alternatives to Nafion. Portfolio breadth lets suppliers cross-pollinate process expertise and secure enduring customer partnerships.

By End-Use Industry: Food Packaging Leads a Market Shift

The food sector accounted for 33.59% of 2024 demand and posts the fastest 2.97% CAGR as retailers champion recyclable or compostable packs. The polyvinyl alcohol market provides oxygen and grease barriers that allow thinner laminates, weight reduction, and PFAS-free performance. Construction occupies a rising share as fiber-reinforced concrete and RDP-modified mortars improve workability, crack resistance, and water impermeability.

Paper manufacturing continues to leverage PVA for surface sizing that boosts printability and scuff resistance. Textiles benefit from efficient warp sizing that cuts yarn breakage and water consumption. Electronics, detergents, and agrochemicals absorb the balance, with unit-dose formats and controlled-release coatings highlighting PVA’s dissolution benefits. These heterogeneous outlets buffer the market from single-sector cyclicality and underpin steady long-term growth.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific generated 47.51% of global PVA demand in 2024 and is growing at a 2.89% CAGR. China anchors regional dominance with integrated acetyl chains and large construction activity, even though VAM price swings squeeze margins. Japan supplies premium resins and fibers, while South Korea and Southeast Asia add incremental capacity aimed at export markets.

In North America, the United States benefits from shale-derived feedstocks, high building-renovation activity, and ongoing reshoring of specialty film production. Europe’s market is shaped by strict environmental directives demanding recyclable or biodegradable materials. Germany leads consumption thanks to its chemical and automotive base, while the United Kingdom, France, and Italy prioritize medical and specialty film uses.

Smaller but growing adoption is seen in Brazil, where infrastructure repair is accelerating, and Saudi Arabia, which aligns PVA investments with broader petrochemical diversification plans. Regional differences in feedstock economics, regulatory frameworks, and downstream integration create a diverse demand map that seasoned producers navigate through localized supply chains and technical service hubs.

Competitive Landscape

The polyvinyl alcohol market is highly consolidated. Kuraray, Sekisui Chemical, and Nippon Synthetic Chemical maintain strong shares through vertical integration, proprietary technology, and a focus on high-margin niches. Strategic shifts prioritize sustainability credentials and specialty applications over pure tonnage. Mergers and partnerships focus on technology access and regional footprint expansion rather than pure capacity plays.

Polyvinyl Alcohol (PVA) Industry Leaders

-

SEKISUI CHEMICAL CO., LTD.

-

KURARAY CO., LTD.

-

Chang Chun Group

-

WANWEI CHEMICAL SUPPLY CHAIN CO.,LTD

-

Nippon Chemical Industrial CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: KURARAY CO., LTD., raised PVOH resin prices by JPY 30 (~USD 0.21) per kg in Japan and by at least USD 220 per ton across Asia-Pacific, the Americas, the Middle East, and Africa; Europe prices increased by EUR 200 per ton.

- May 2024: WANWEI CHEMICAL SUPPLY CHAIN CO., LTD., launched a new PVA product that broadens its materials portfolio in China

Global Polyvinyl Alcohol (PVA) Market Report Scope

Polyvinyl alcohol (PVA) is a colorless, hydrophilic water-soluble synthetic polymer and poses effective film-forming and adhesive properties. It is manufactured by polymerizing vinyl acetate monomer, followed by hydrolysis, and finds its application in various end-user industries like paper, food packaging, textiles, etc. The polyvinyl alcohol (PVA) market is segmented by grade, end user, and geography. The market is segmented by grade: fully hydrolyzed, partially hydrolyzed, sub-partially hydrolyzed, low foaming grades, and other grades. By end user, the market is segmented into food packaging, paper manufacturing, construction, electronics, textile manufacturing, and other end users. The report also covers the market size and forecasts for the polyvinyl alcohol market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD million).

| By Grade | Fully Hydrolyzed | ||

| Partially Hydrolyzed | |||

| Sub-Partially Hydrolyzed | |||

| Low-Foaming Grades | |||

| Other Grades (Tactified Grades, Fine Particle Grades) | |||

| By Form | Powder | ||

| Granules | |||

| Flakes | |||

| Films (Water-Soluble) | |||

| Fibers | |||

| By Application | Polymerization Additives | ||

| Polyvinyl Butyral | |||

| Adhesives | |||

| Textile | |||

| Paper Pulp and Coating | |||

| Developing Application | |||

| Other Application | |||

| By End-Use Industry | Food Packaging | ||

| Paper Manufacturing | |||

| Construction | |||

| Electronics | |||

| Textile | |||

| Other Industries (Detergent, Agrochemicals, etc.) | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Nordic Countries | |||

| Turkey | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| Qatar | |||

| United Arab Emirates | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle-East and Africa | |||

| Fully Hydrolyzed |

| Partially Hydrolyzed |

| Sub-Partially Hydrolyzed |

| Low-Foaming Grades |

| Other Grades (Tactified Grades, Fine Particle Grades) |

| Powder |

| Granules |

| Flakes |

| Films (Water-Soluble) |

| Fibers |

| Polymerization Additives |

| Polyvinyl Butyral |

| Adhesives |

| Textile |

| Paper Pulp and Coating |

| Developing Application |

| Other Application |

| Food Packaging |

| Paper Manufacturing |

| Construction |

| Electronics |

| Textile |

| Other Industries (Detergent, Agrochemicals, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

How big is the polyvinyl alcohol market today?

The market stands at 1.42 million tons in 2025 and is projected to reach 1.62 million tons by 2030, reflecting a 2.56% CAGR.

Which segment leads the polyvinyl alcohol market?

Partially hydrolyzed grades lead with 37.34% share and also record the fastest 2.96% CAGR during 2025-2030.

Why is Asia-Pacific dominant in the polyvinyl alcohol market?

The region holds 47.51% of global volume due to integrated acetyl supply, large downstream manufacturing, and growing construction and packaging demand.

What drives PVA adoption in food packaging?

PVA offers strong oxygen and grease barriers, compatibility with recyclable structures, and compliance with PFAS-free regulations, enabling shelf-life extension without environmental trade-offs.

How are volatile VAM prices affecting producers?

Price swings compress margins for commodity grades, prompting investment in upstream acetyl capacity and a pivot toward higher-margin specialty PVA products.