Polyvinyl Alcohol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 1.46 Million tons |

| Market Volume (2031) | 1.67 Million tons |

| Growth Rate (2026 - 2031) | 2.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyvinyl Alcohol Market Analysis by Mordor Intelligence

The Polyvinyl Alcohol Market size is projected to expand from 1.42 million tons in 2025 and 1.46 million tons in 2026 to 1.67 million tons by 2031, registering a CAGR of 2.72% between 2026 to 2031. Current demand is anchored in food-contact films, construction sealants, and detergent pods, while feedstock-price swings moderate headline growth. Brand owners in North America and Europe reward biodegradable film innovations, whereas Asia-Pacific benefits from integrated coal-to-acetylene production routes that compress costs. Emerging uses in drug-eluting stents, 3D-bioprinting, and seed coatings widen the application canvas and support value-added pricing. Competitive strategies revolve around capacity additions for specialty grades, vertical integration to hedge vinyl-acetate-monomer volatility, and patent activity targeting hybrid PVA-cellulose composites.

Key Report Takeaways

- By grade, partially hydrolyzed captured 37.51% of the polyvinyl alcohol market share in 2025, advancing at a 3.01% CAGR through 2031.

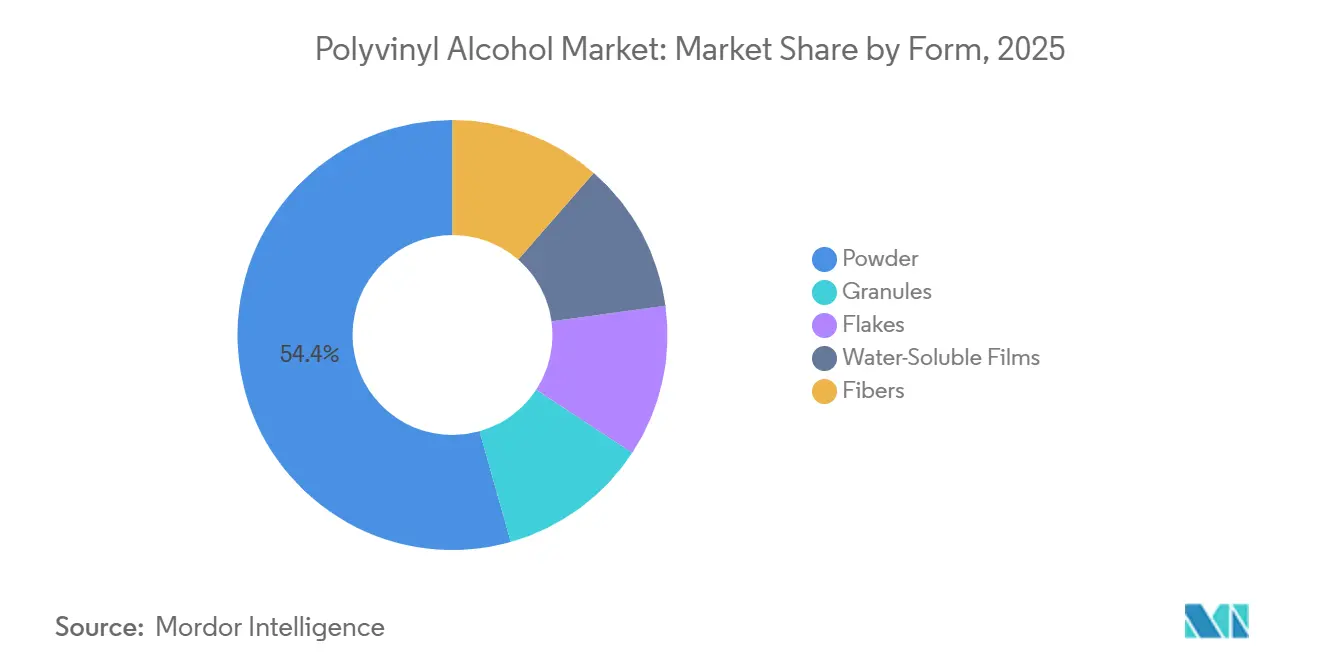

- By form, powder held 54.36% of 2025 volume, while water-soluble films recorded the fastest forecast pace at 3.41% CAGR through 2031.

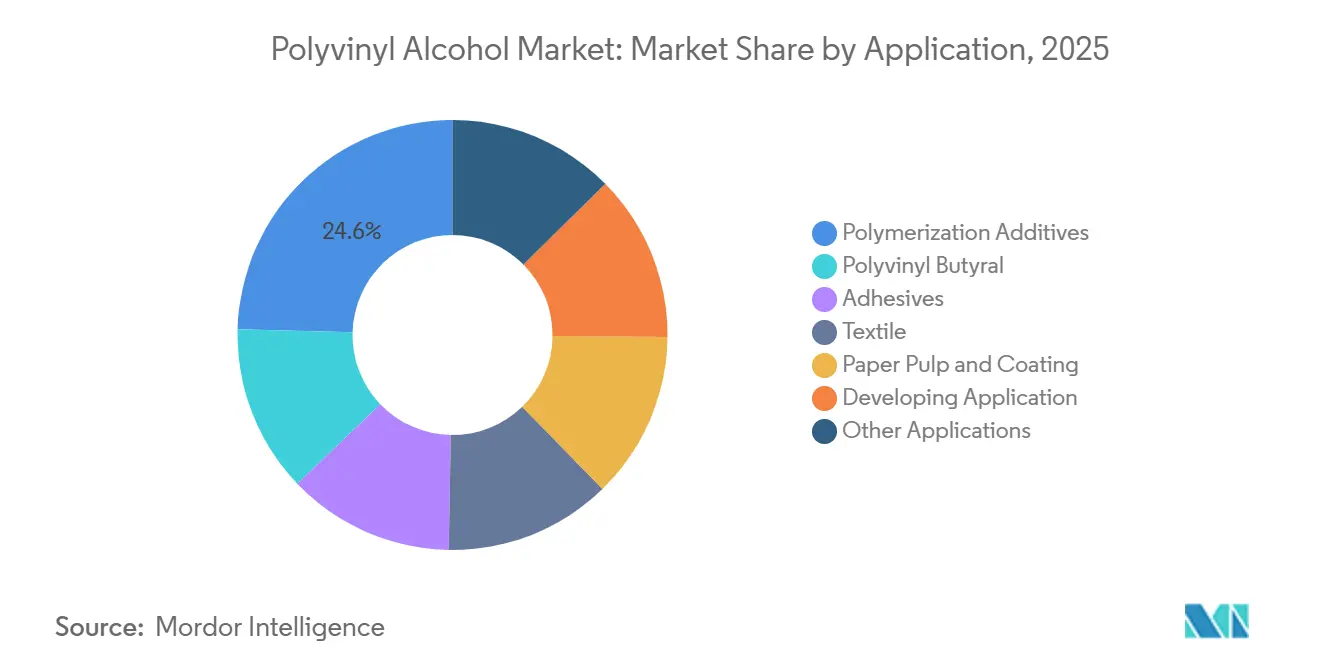

- By application, polymerization additives led with 24.58% in 2025, while the developing application is projected to expand at a 4.52% CAGR to 2031.

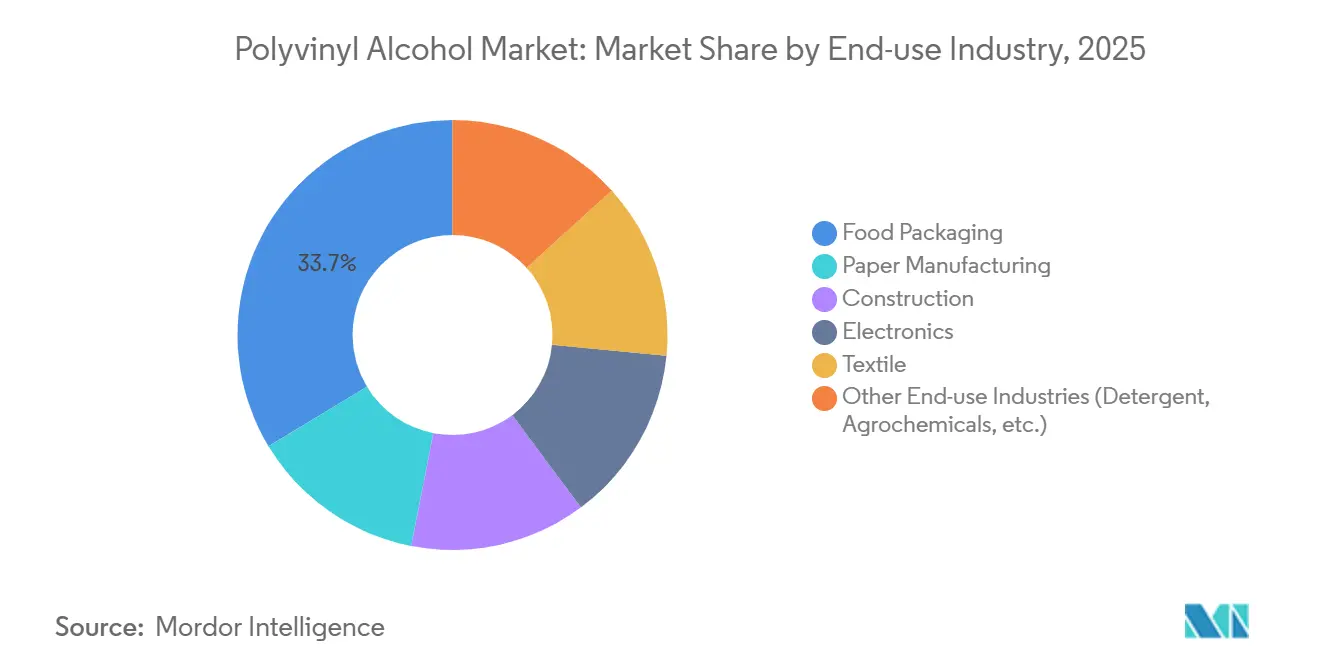

- By end-use industry, food packaging led with 33.67% contribution in 2025 and is projected to expand at 3.04% CAGR to 2031.

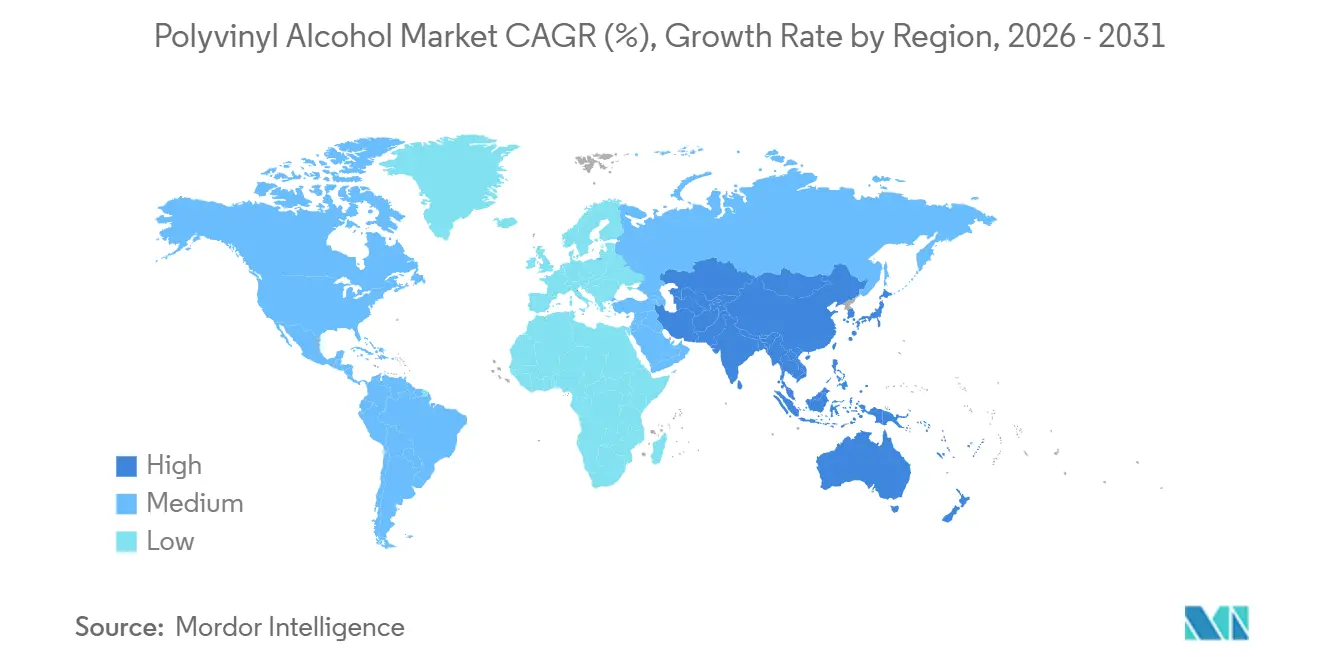

- By geography, Asia-Pacific dominated with 47.72% volume in 2025 and is set to grow at a 2.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyvinyl Alcohol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand from Food-Packaging Industry | +0.8% | Global, with concentration in North America, EU, and APAC urban centers | Medium term (2-4 years) |

| Increasing Usage in Construction Sealants and Mortar | +0.5% | APAC core (China, India), spill-over to Middle East infrastructure projects | Long term (≥ 4 years) |

| Surging Adoption in Detergent Pods and Water-Soluble Films | +0.7% | North America and EU, emerging in Latin America | Short term (≤ 2 years) |

| Expansion of PVA-Based Emulsion Polymers for Water-Borne Coatings | +0.4% | Global, regulatory-driven in EU and California | Medium term (2-4 years) |

| Emergence of PVA-Based Biodegradable Agricultural Films | +0.3% | APAC (India, Vietnam, Thailand), pilot programs in Mediterranean EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Food-Packaging Industry

Single-serve convenience formats reshaped purchasing choices. Dishwasher-tablet wraps, coffee pods, and sauce sachets jointly held 33.67% of end-use volume in 2025. Updated U.S. FDA food-contact protocols in 2024 fast-tracked approvals for PVA films with antimicrobial nanoparticles, lifting agency submissions by 22% in 2025. Japan’s health ministry halved approval lead times, spurring domestic uptake in bento-box liners and noodle-packet films [1]Ministry of Health, Labour and Welfare Japan, “Packaging Film Approval Streamlining,” mhlw.go.jp . German and Dutch grocers reported a 12-15% consumer premium for dissolve-in-sink packaging, validating price-elastic demand.

Increasing Usage in Construction Sealants and Mortar

Partially hydrolyzed PVA improves rheology and crack resistance in tile adhesives and self-leveling compounds. China’s 2024 low-VOC mandate for public infrastructure lifted construction-grade PVA offtake 9% in 2025. India’s affordable-housing drive adopted PVA fibers to cut rebar costs, while Middle Eastern mega-projects specified PVA-modified sealants able to absorb daily thermal swings from 50 °C to 15 °C.

Surging Adoption in Detergent Pods and Water-Soluble Films

Water-soluble PVA films enable pre-measured doses that avoid overdosing. Procter & Gamble disclosed a 34% U.S. share for Tide Pods in 2025 and is piloting similar films for softeners. Europe’s 2025 Packaging Waste Regulation exempts compliant PVA films from producer fees, saving EUR 120 million annually for early adopters. Unilever converted 40% of its European detergents portfolio, removing 2,800 tons of plastic waste.

Expansion of PVA-Based Emulsion Polymers for Water-Borne Coatings

Tighter VOC caps forced paint makers toward water-borne latexes. California’s South Coast AQMD halved VOC limits in 2024; formulators compensated by raising PVA solids to maintain film integrity. The EU Industrial Emissions update in 2025 drove PPG and Axalta to debut low-foaming PVA basecoats for automotive refinish lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Vinyl-Acetate-Monomer (VAM) Prices Squeezing Margins | -0.6% | Global, acute in regions without integrated VAM-PVA production (Europe, North America) | Short term (≤ 2 years) |

| Availability of Bio-Based and Petro-Based Substitutes (PLA, EVOH) | -0.4% | EU and North America, brand-driven in premium packaging | Medium term (2-4 years) |

| Limited Recycling Infrastructure for PVA Films in Emerging Economies | -0.2% | Southeast Asia, sub-Saharan Africa, rural Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Vinyl-Acetate-Monomer Prices Squeezing Margins

Spot VAM swung 18% in 2025, narrowing non-integrated producers’ gross margins by 12-15% and prompting temporary shutdowns. Integrated Chinese firms enjoyed a USD 180 per-ton cost edge, boosting exports 23%.

Availability of Bio-Based and Petro-Based Substitutes (PLA, EVOH)

Retailers mandate bio-content thresholds that favor PLA, while EVOH outperforms on oxygen-barrier metrics. Kuraray’s EVAL holds 40% share in barrier films, yet PVA keeps an edge in water-soluble and cold-water roles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Hydrolysis Levels Dictate Solubility Profiles

Partially hydrolyzed captured 37.51% of 2025 volume, expanding at 3.01% through 2031 as textile mills favored its dual cold- and hot-water solubility. Fully hydrolyzed variants underpin detergent-pod films; Kuraray’s POVAL 205 with 98.5% hydrolysis became the reference grade in 2025. Specialty innovations include super-low-foaming types for high-speed inkjet coating and thermally reversible gels for reusable cold packs. Collectively, advanced grades increase average selling prices and stabilize margins.

Manufacturers tailor viscosity, molecular weight, and functional groups. Mitsubishi Chemical launched a PVA with surface tension of 28 dynes/cm in 2025 for defect-free optical-film coating. Sekisui’s thermally reversible gels liquefy above 60 °C then resolidify, finding new use in data-center thermal buffers. These developments maintain customer lock-in and underpin the polyvinyl alcohol market’s shift toward value-added niches.

By Form: Water-Soluble Films Outpace Traditional Formats

Powder retained 54.36% share in 2025, driven by on-site dissolution needs in adhesives and textiles. Water-soluble films, however, will post a 3.41% CAGR to 2031 as pod and agrochemical-sachet demand widens. Japan VAM & Poval’s 2025 tri-layer film dissolved 30% faster in cold water, cutting cycle times for detergent plants. Granules serve dust-free construction job sites, while fibers reinforce concrete and asphalt; Kuraray’s Kuralon fiber replaced steel in Japan’s maglev tunnel shotcrete, lowering weight 40%.

Film producers manage plasticizer ratios for balance between tensile strength and dissolution. Flake forms, produced via drum drying, cater to automated dosing in paper mills. Physical format choice therefore dictates reachable applications and pricing power within the polyvinyl alcohol market.

By Application: Developing Segments Offer Highest Growth

Developing Application will grow at 4.52%, the highest among segments. Abbott’s PVA-coated coronary stent achieved 94% 12-month patency in 2025 trials. Organovo sourced ultra-pure PVA for sacrificial bioprint supports that dissolve post-processing, freeing delicate tissue scaffolds. Polymerization additives, 24.58% share in 2025, continue to stabilize vinyl-acetate emulsions essential in low-VOC paints.

Polyvinyl butyral interlayers in laminated glass consume moderate demand; automotive lightweighting sustains demand. Adhesives and textile sizing face slower growth due to digitalization and synthetic-fiber penetration, yet they remain volume mainstays. The application mix underscores the polyvinyl alcohol market’s resilience through diversification.

By End-use Industry: Food Packaging Leads Volume and Growth

Food packaging led with 33.67% of volume in 2025, advancing at 3.04% to 2031. Finish brand’s PVA-wrapped dishwasher tablet gained substantial European share within six months. Keurig’s compostable coffee pod pilot registered 95% consumer acceptance. Construction captured moderate demand, driven by Asia-Pacific infrastructure, while electronics tied to display-panel output. Other end-use industries including agrochemicals and detergents filled the rest.

The diverse end-use footprint buffers cyclical swings; regulatory tailwinds in packaging and construction offset maturing segments in paper and textiles, sustaining the polyvinyl alcohol market trajectory.

Geography Analysis

Asia-Pacific dominated with 47.72% volume in 2025 and is forecast to expand at 2.92% CAGR. China’s 850,000-ton integrated capacity enjoys USD 180/t cost advantages vs. ethylene routes, allowing aggressive commodity pricing. India’s 2025 offtake jumped due to housing construction and textile sizing. Japan exported high-viscosity grades for optical films. Southeast Asia posted detergent-pod demand growth as multinationals localized production.

In North America, streamlined FDA clearances accelerated film approvals, and Procter & Gamble’s pod shift added demand. Canada piloted PVA seed coatings with 10% germination uplift in saline soils. Mexico enjoyed moderate growth in PVA-modified mortars tied to near-shoring construction.

Europe is prioritizing biodegradable films under its 2025 waste regulation, driving import growth from Japan[2]European Commission, “Extended Producer Responsibility Exemptions,” europa.eu. South America and the Middle East and Africa commanded demand as infrastructure and agricultural trials multiply. Petrobras tested PVA drilling-fluid additives, while Saudi Arabia’s NEOM project specified PVA sealants for glass façades, underscoring emerging regional niches.

Value Chain Analysis

The polyvinyl alcohol (PVA) value chain begins with vinyl acetate monomer (VAM) procurement and conversion to polyvinyl acetate (PVAc), followed by hydrolysis (alcoholysis) into PVA. Industrial production largely uses dry alcoholysis routes to limit byproduct formation, but producers still balance cost and quality through catalyst selection, alkali handling, methanol recovery, and effluent treatment, which in turn affect grade purity, viscosity, and hydrolysis level requirements for food-contact films, detergent pods, coatings, and construction formulations.

In the midstream, major manufacturers including Kuraray, SEKISUI Specialty Chemicals, Mitsubishi Chemical, Chang Chun, Anhui Wanwei, and Sinopec Sichuan Vinylon supply PVA in powders, granules, and specialty film formats, often alongside application support for dissolution behavior and processing windows. Downstream, converters and compounders convert resin into water-soluble films, fibers, adhesives, mortar modifiers, and coating intermediates, distributing via direct contracts and regional chemical distributors. Bottlenecks tend to cluster around VAM price volatility (18% spot swings cited for 2025 in the RD context), logistics disruptions that raise trans-continental freight costs, and limited availability of specialty grades such as optical-film and low-foaming types, which pushes producers toward vertical integration and more localized production footprints (for example, Kuraray adding European production of specific POVAL grades in Frankfurt in 2025).

Competitive Landscape

Top five producers - Kuraray, SEKISUI CHEMICAL CO., LTD., Anhui Wanwei, Sinopec Sichuan Vinylon, Chang Chun - control roughly 72% of capacity, evidencing moderate concentration. Kuraray’s 2025 patent for PVA-cellulose nanocrystal composites lifts tensile strength 40% without losing solubility, targeting rigid packaging that PET currently owns. Mitsubishi Chemical’s captive VAM integration buffered earnings amid 2025 feedstock spikes.

Chinese entrants leverage coal-acetylene integration to win price-sensitive adhesive and textile deals. Dow’s 2025 Vietnamese circular-recycling venture demonstrates cost-saving hydrolysis for film waste. Specialty suppliers such as Polysciences serve high-purity niches at USD 180/kg, capturing healthcare customers where batch consistency is critical.

Technology bifurcation is visible: leaders adopt continuous reactors that cut energy 15%, while laggards still run batch lines. ISO 50001 certifications increasingly sway multinationals’ procurement. Overall, premium margins accrue to integrated or specialty-grade innovators, while commoditized supply faces persistent pressure across the polyvinyl alcohol market.

Polyvinyl Alcohol Industry Leaders

SEKISUI CHEMICAL CO., LTD.

KURARAY CO., LTD.

Chang Chun Group

Anhui Wanwei Updated High Tech Material Industry Co Ltd

Sinopec Sichuan Vinylon Works

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Specialty-grade and application-led upgrading offers the clearest opportunity, since buyers pay for predictable dissolution, low-foaming behavior, and high purity rather than commodity pricing. Optical-use PVA film for display and panel applications is a specific focus: Kuraray disclosed an expansion plan at its Saijo Plant in Japan adding 38 million square meters per year (announced in 2025), and Mitsubishi Chemical announced additional optical PVOH film capacity in Ogaki City, Japan (October 2024), with commissioning targeted for the second half of fiscal 2027. These announcements reflect end-user qualification timelines and the importance of high-viscosity, defect-control performance in electronics supply chains.

Cost and security-of-supply gaps also remain relevant in regional production hubs and alternative production routes designed to reduce exposure to VAM swings. China continues to add scale and deepen integration, and 2026 funding and construction updates point to that direction: Ningxia Shuangying New Material Technology started building a 100,000-ton/year PVA project in Pingluo Industrial Park (March 2026), with trial production planned for late November 2026, while Wanwei High-Tech revised a private placement plan in July 2026 (2.3 billion yuan) to support a 200,000-ton/year ethylene-based functional PVA resin project and a 30 million square meter high-generation panel PVA optical film project. On the demand side, water-soluble film adoption in detergents and packaging is reinforced by the RD context, including Europe’s 2025 Packaging Waste Regulation exemption for compliant PVA films and brand-owner conversions in detergents, which supports film-grade capacity additions, improved cold-water dissolution, and certified mass-balance supply chains that help win procurement in regulated markets.

Recent Industry Developments

- April 2026: Sekisui Specialty Chemicals announced a global price increase for Selvol Polyvinyl Alcohol and related Selvol product lines, effective April 15, 2026, with region-specific uplifts across the Americas, Asia, and EMEA. The announcement indicated renewed pass-through of input and operating cost pressure into contract pricing, tightening the economics for film converters and adhesive and coating formulators. It also highlighted supplier leverage in specialty and service-intensive PVA grades, where switching costs are higher.

- June 2025: Kuraray announced an expansion of optical-use poval film production facilities at its Saijo Plant in Ehime Prefecture, Japan, adding 38 million square meters per year of capacity with completion scheduled for December 2027. The project ties PVA supply more directly to the electronics value chain, where optical film quality and stable qualification are critical. It also reinforces differentiation away from commodity resin into specification-driven, higher-margin film applications.

- February 2024: Kuraray commenced production at a new polyvinyl alcohol film plant in Poland, strengthening its regional supply position for European customers. Local film manufacturing shortens lead times and reduces exposure to long-haul logistics volatility for converters serving detergent pods and packaging formats. The facility also supports a broader strategy of localized production footprints for PVOH film applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the polyvinyl alcohol (PVA) market is defined as demand for PVA resin sold into downstream manufacturing and formulation uses, captured as market volume for traded material across major consuming regions.

Scope exclusions: This sizing does not count internal captive transfers inside integrated producers when the same material would otherwise be counted again downstream.

Segmentation Overview

- By Grade

- Partially Hydrolyzed

- Fully Hydrolyzed

- Sub-Partially Hydrolyzed

- Low-Foaming Grades

- Other Grades (Tactified Grades, Fine Particle Grades)

- By Form

- Powder

- Granules

- Flakes

- Water-Soluble Films

- Fibers

- By Application

- Polymerization Additives

- Polyvinyl Butyral

- Adhesives

- Textile

- Paper Pulp and Coating

- Developing Application

- Other Applications

- By End-use Industry

- Food Packaging

- Paper Manufacturing

- Construction

- Electronics

- Textile

- Other End-use Industries (Detergent, Agrochemicals, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- Qatar

- United Arab Emirates

- Egypt

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand map for PVA and to set realistic boundaries around what gets counted as market consumption. We referenced public sources such as UN Comtrade trade statistics (for cross-border PVA resin flows), USGS materials data (for broader resin and chemicals context), World Bank macro indicators (for country level demand drivers), and publications from chemistry and materials journals that discuss PVA properties and use patterns.

To keep the model grounded, we also reviewed supplier and distributor materials such as annual reports, investor presentations, product technical data sheets, and reputable press coverage on capacity changes and plant outages. In a few cases, a paid subscription for company financials and a shipment-level import export database were used to confirm corporate footprint and cross check the direction of trade flows. The desk sources listed here are illustrative, and many additional public documents were used for cross checks and clarification.

Primary Interviews and Surveys

Primary work focused on validating how PVA moves from producers to converters and formulators, and how buying patterns differ by grade and end use. We spoke with participants from manufacturing, distribution, and large end users to confirm utilization trends, typical contract timing, and the most common substitution points that affect real demand.

Coverage was spread across APAC, EMEA, and the Americas so the model reflects both high volume production hubs and import dependent markets.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 20% | APAC: 37% |

| Mid tier: 49% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 22% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing starts from a top-down build where production, trade, and apparent consumption are reconstructed by region, and then filtered through PVA specific loss factors and downstream usage patterns. Once the regional totals were formed, we corroborated them with selective bottom-up checks such as sampled supplier volume disclosures, channel checks on traded material, and a price-per-ton sanity test to ensure totals stay within realistic ranges.

Key inputs used in the market model included operating rates and capacity additions for PVA and upstream vinyl acetate monomer, import export flows for PVA resin, the share of demand linked to water soluble film and packaging uses, construction and textile activity signals in major consuming countries, and observed price movements that influence restocking cycles. Where supplier level detail was limited, we filled gaps using regional trade balances and expert guided assumptions on interregional shipments.

For forecasting, scenario analysis was used, with a base case tied to expected capacity ramp ups, steady end use growth, and normalized trade patterns. The range cases were built around faster or slower uptake in packaging and film applications and different assumptions on operating rates, which were then aligned with what interviewees saw as plausible.

Data Validation & Update Cycle

Outputs were checked against independent signals like regional net trade direction, announced capacity timelines, and whether implied consumption growth matches the pace of key end uses. Any large variances were traced back to the specific input that caused them, and then reworked with a second analyst review before sign off.

The report is refreshed on an annual cycle, and interim updates are made when material events occur, such as major plant shutdowns, new capacity starts, or sharp shifts in trade policy. Before delivery, we do a final pass on the latest news and public data releases so clients receive an updated view.

Mordor Intelligence's Polyvinyl Alcohol Pva Market Size Versus Other Published Estimates

It is normal to see different market sizes for PVA because publishers do not always use the same boundary, and they may also choose different base years and unit systems. Some sources publish only value numbers, while others prioritize volume, which can widen the spread when price assumptions move quickly.

By tracking traded consumption in tons and then refreshing price-per-ton assumptions with recent contract and spot checks, Mordor Intelligence keeps the PVA total tied to measurable supply-demand signals rather than broad revenue pooling across adjacent polymers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.46 M (2026) | |

| Global Consultancy A | USD 1.21 B (2025) | Published in value terms and anchored to a different base year, which means the implied price-per-ton and timing of price cycles can shift the total even if volume demand is similar. |

| Industry Publisher B | USD 1.24 B (2025) | Uses a value-based definition with its own grade and end-use grouping, and the 2025 starting point can capture a different pricing environment than a volume-first model. |

Taken together, the main takeaway is that year choice, unit system (value versus tons), and how pricing is applied across grades can move the headline number. Our approach stays repeatable because the totals can be rechecked from trade, capacity, and consumption logic, and then adjusted only when the underlying signals change.

Key Questions Answered in the Report

How large is the polyvinyl alcohol market in 2026?

The polyvinyl alcohol market size reached 1.46 million tons in 2026 and is forecast to reach 1.67 million tons by 2031.

Which region leads global demand?

Asia-Pacific commands 47.72% of volume in 2025 thanks to China’s integrated production corridors and Japan’s specialty-grade exports.

What is the fastest-growing application for PVA?

Developing Application advances at 4.52% CAGR through 2031 on the back of stents, bioprinting, and binder roles.

How are feedstock swings influencing margins?

Vinyl-acetate-monomer prices moved 18% in 2025, compressing non-integrated producers’ margins by up to 15%, while integrated players stayed insulated.

Page last updated on: