Polyvinylpyrrolidone Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

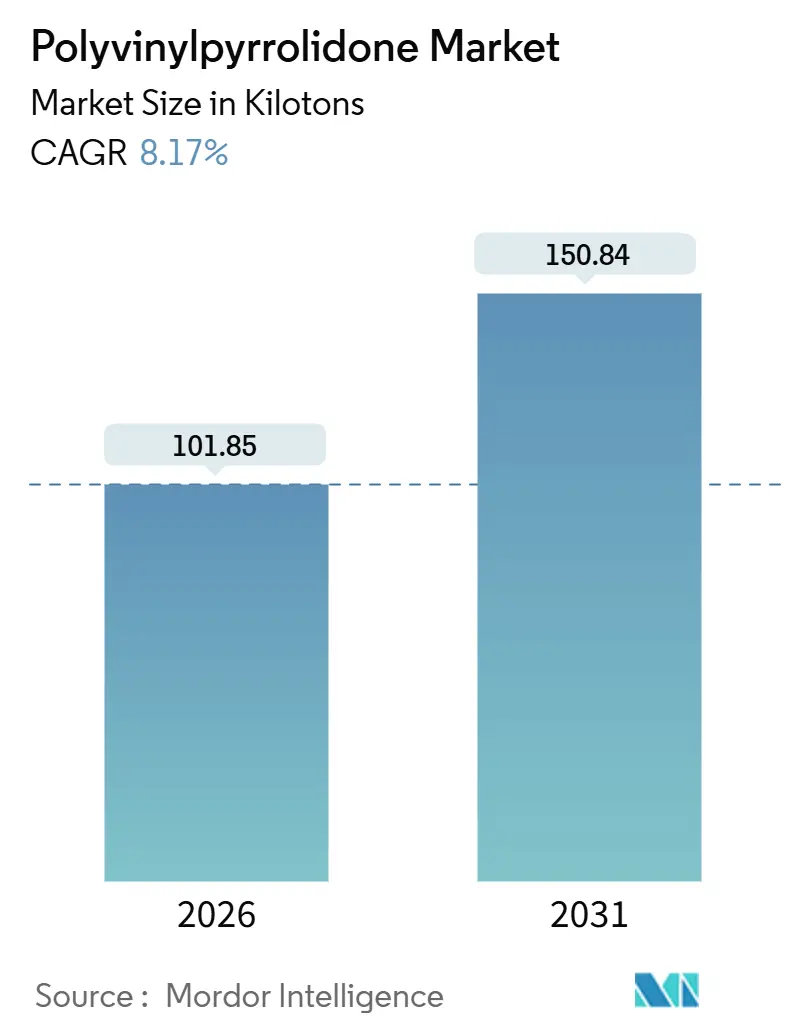

| Market Volume (2026) | 101.85 kilotons |

| Market Volume (2031) | 150.84 kilotons |

| Growth Rate (2026 - 2031) | 8.17% CAGR |

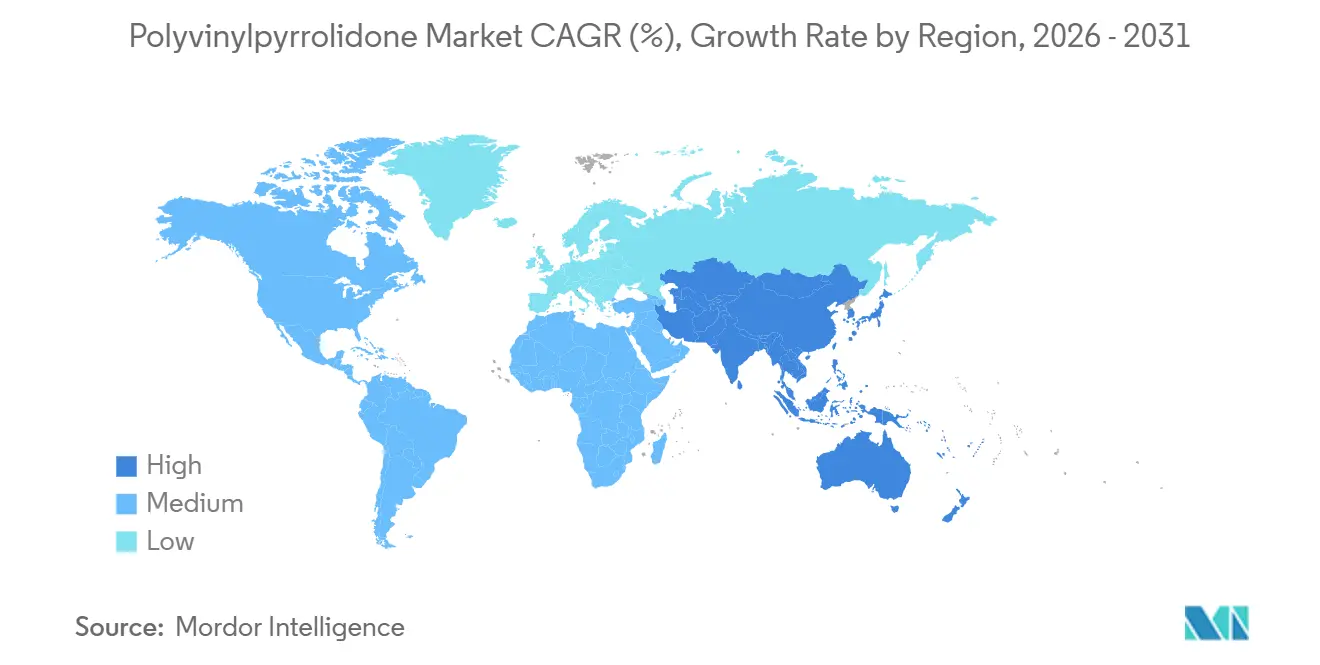

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyvinylpyrrolidone Market Analysis by Mordor Intelligence

The Polyvinylpyrrolidone Market size is estimated at 101.85 kilotons in 2026, and is expected to reach 150.84 kilotons by 2031, at a CAGR of 8.17% during the forecast period (2026-2031). The upward curve reflects tightening residual-monomer limits that oblige excipient suppliers to retrofit purification trains, steady share migration toward spray-dried grades optimized for direct compression, and rising demand for K-value variants suited to controlled-release tablets. Supply-side capacity additions cluster in Asia, where vertically integrated plants curb feedstock risk, while downstream users in North America and Europe pursue silicone-free personal-care reformulations that depend on water-soluble PVP copolymers. On the risk ledger, acetylene-based N-vinylpyrrolidone costs track crude-oil swings, and emerging scrutiny of aquatic persistence signals potential producer-responsibility levies in Europe. Moderate consolidation persists because monomer backward integration remains capital-intensive, yet price competition in commodity grades has intensified as Chinese entrants elevate nameplate output by double digits.

Key Report Takeaways

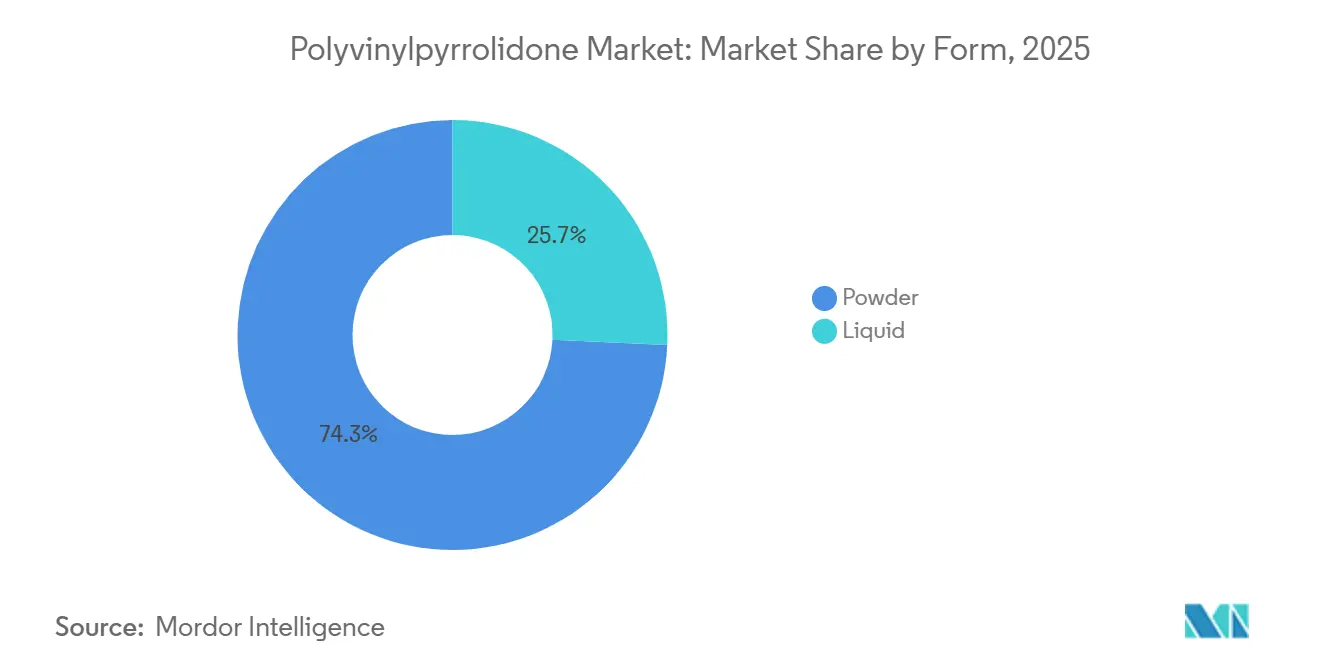

- By form, powder captured 74.26% revenue share in 2025 and is projected to expand at an 8.72% CAGR to 2031.

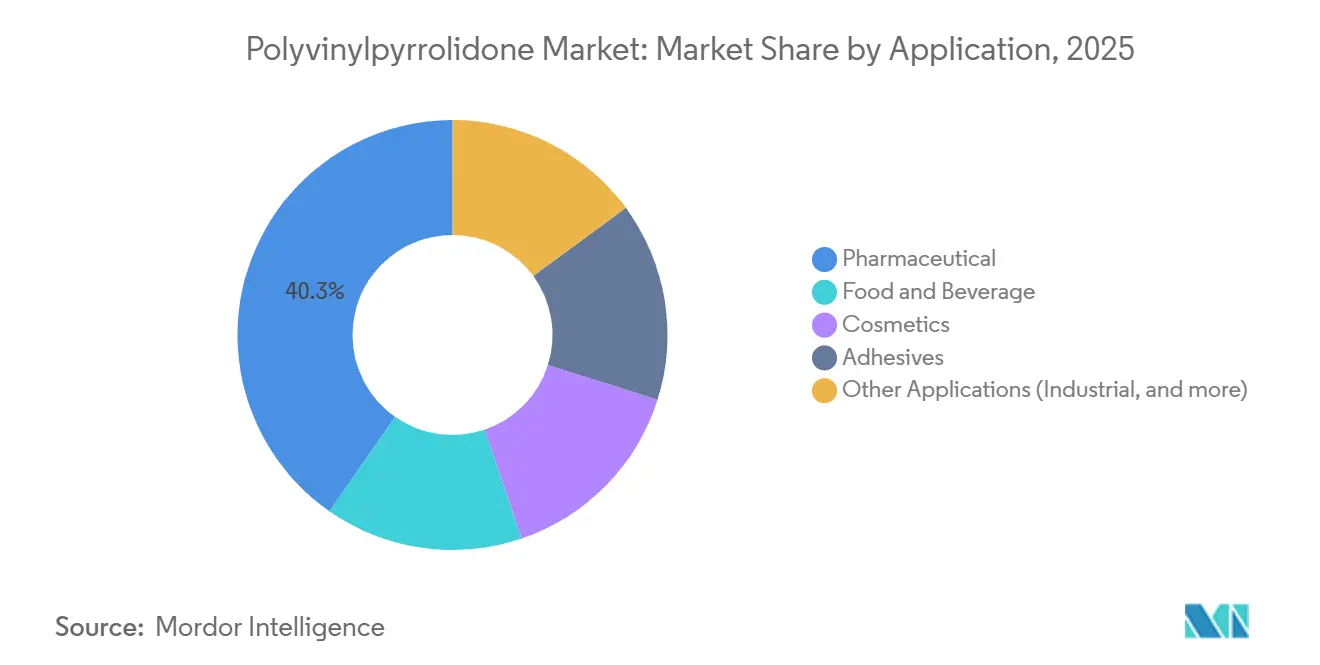

- By application, pharmaceuticals led with 40.28% of polyvinylpyrrolidone market share in 2025, while the segment is advancing at an 11.87% CAGR through 2031.

- By geography, Asia-Pacific accounted for 39.27% of the polyvinylpyrrolidone market size in 2025 and is progressing at an 11.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyvinylpyrrolidone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating demand for high-purity excipients in solid-oral pharmaceuticals | +2.80% | Global, with concentration in Asia-Pacific (China, India) and North America | Medium term (2-4 years) |

| Rising consumption of hair-styling and personal-care formulations | +1.60% | North America, Europe, and urban Asia-Pacific markets (South Korea, Japan) | Short term (≤ 2 years) |

| Adoption of PVP binders in 3D-printed pharmaceuticals | +0.90% | North America and Europe, early-stage adoption in Japan | Long term (≥ 4 years) |

| Use of PVP dispersants in battery-recycling slurry processes | +0.40% | Asia-Pacific (China, South Korea) with spillover to Europe and North America | Long term (≥ 4 years) |

| Shift toward water-soluble, biodegradable adhesives in flexible electronics | +0.70% | Asia-Pacific core (South Korea, Japan, China), spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Demand for High-Purity Excipients in Solid-Oral Pharmaceuticals

Tablet manufacturers must now meet residual N-vinylpyrrolidone limits of ≤10 ppm, ≤400 ppm peroxides, and ≤500 ppm aldehydes, thresholds that force investment in vacuum stripping, peroxide quenching, and real-time spectroscopy. Asian contract development and manufacturing organizations (CDMOs) ramp output for global generics and routinely specify PVP batches with a K-value coefficient-of-variation below 3%, a standard unattainable without inline viscometry[1]International Council for Harmonisation, “Q8 Pharmaceutical Development,” Ich.org. Compliance costs elevate delivered-price differentials between pharma- and industrial-grade material by up to 15%, yet also erect barriers to entry, bolstering returns for integrated suppliers. North American specialty-pharma firms widen adoption of K-90 and K-120 matrices to refresh product life cycles under the FDA’s quality-by-design ethos. Medium-term growth, therefore, hinges on API manufacturing expansions in India and China, along with western reformulation activity.

Rising Consumption of Hair-Styling and Personal-Care Formulations

Cosmetic chemists favor vinyl pyrrolidone/vinyl acetate and vinyl pyrrolidone/DMAPA copolymers to secure humidity-resistant hold without the rigid film associated with acrylates. BASF’s Luviskol and Luviset lines provide K-values from 12-90 that let formulators balance strength and wash-off characteristics. The European CosIng database lists PVP as unrestricted, yet clean-beauty retailers pressure brands to migrate toward water-based systems, accelerating demand in North America and Europe[2]European Commission, “CosIng Cosmetic Ingredient Database,” Ec.europa.eu. Urban Asia follows, propelled by K-pop-inspired styling regimens that value strong yet flexible hold. The effect should crest within two years as reformulation cycles close and inventories refresh.

Adoption of PVP Binders in 3D-Printed Pharmaceuticals

Additive-manufactured tablets require excipients that present narrow glass-transition windows and predictable melt rheology. PVP grades with K-values 25-90 deliver Tg 110-180°C and support fused-deposition modeling while forming amorphous dispersions that raise API bioavailability. FDA approval of Spritam in 2015 validated the regulatory path, yet commercial adoption remains gated by equipment costs and the absence of harmonized good-manufacturing-practice rules. University consortia continue material testing while Ashland and Aprecia target an NDA filing by late 2026. Uptake will materialize first in North America and Europe once process validation templates mature.

Shift Toward Water-Soluble, Biodegradable Adhesives in Flexible Electronics

Wearable sensors and foldable displays need adhesives that bond substrates without outgassing. PVP’s hydroxyl-rich backbone bonds well to metal oxides and decomposes harmlessly in physiological fluids within weeks, matching the lifecycle goals of transient electronics. Samsung Display and LG Display pilot PVP layers in foldable OLED stacks to mitigate delamination, and Japan’s METI funds research on PVP dielectrics for farm-use biosensors. Long-term CAGR uplift stems from South Korean, Japanese, and Chinese display capacity expansions and U.S. medical-device ventures that seek biodegradable implant adhesives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in N-vinylpyrrolidone monomer prices | -1.40% | Global, with acute exposure in regions dependent on acetylene feedstock (Asia-Pacific, Europe) | Short term (≤ 2 years) |

| Stringent pharmacopeial residual-monomer and peroxide limits | -0.90% | Global, particularly impacting pharmaceutical-grade producers in North America, Europe, and India | Medium term (2-4 years) |

| Dust-explosion compliance capex for ATEX-rated handling systems | -0.50% | Europe (ATEX Directive 2014/34/EU), with spillover to North America (NFPA 652 standards) | Medium term (2-4 years) |

| Environmental scrutiny over aquatic persistence of PVP | -0.60% | Europe and North America, with emerging regulatory attention in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in N-Vinylpyrrolidone Monomer Prices

The Reppe process links NVP costs to acetylene, formaldehyde, and ammonia, and therefore to crude oil and electricity. Winter curtailments in Shanxi and Inner Mongolia pushed spot acetylene up 18-22% in 2025, lifting NVP offers globally. Europe felt parallel shocks as gas-price spikes after Nord Stream capacity loss added EUR 0.80-1.20 per kg to monomer costs, compressing pharma-grade margins by up to 10 points. Vertical integration shields BASF and Kuraray, but smaller converters ride the price roller coaster, weakening cash flows and deferring capex.

Stringent Pharmacopeial Residual-Monomer and Peroxide Limits

European Pharmacopoeia 11.0 halved the monomer limit to 10 ppm, compelling vacuum-stripping at sub-1 mbar and temperatures below 90°C to avoid polymer scission. Added stabilizers to quench peroxides, introducing trace metals that require ion-exchange clean-up, boosting variable costs by USD 0.40-0.60 per kg. Indian excipient makers supplying 35% of global generics saw operating margins slip 5-7% as they upgraded analytics capacity, driving consolidation toward scale players capable of high-performance liquid chromatography release tests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Performance Bolsters Handling Efficiency

Powder grades led the polyvinylpyrrolidone market with a 74.26% volume stake in 2025 and are forecast to grow at 8.72% through 2031. Spray drying of K-30 yields spherical particles that flow easily into direct-compression presses, lowering cycle time and reducing dust-explosion risk under ATEX rules. Drum-dried K-90 and K-120 remain essential for controlled-release matrices but require extra handling steps that push cost per finished kilogram higher. Continuous-manufacturing adoption further favors free-flowing powders because gravimetric feeders operate more consistently at bulk densities between 0.3-0.5 g cm⁻³.

Liquid formulations serve injectables and aerosol hair sprays where a pre-dissolved polymer shortens make-ready time. Despite 30-40% higher freight cost per active kilogram, injectable producers value the absence of particulates and reduced microbiological risk during sterile filtration. Battery-recyclers piloting water-based hydrometallurgical flowsheets also prefer liquid binders for easier dispersion of cathode fines. Yet preservative content in liquid grades collides with clean-beauty label constraints, limiting broader cosmetics growth.

By Application: Pharmaceuticals Accelerate on Generics and Controlled-Release Needs

Pharmaceutical excipients commanded 40.28% of the overall 2025 volume and are projected to rise at 11.87%, the fastest application CAGR. The polyvinylpyrrolidone market size for pharmaceuticals is on track to hit 76.2 kilotons by 2031 as CDMOs in India and China scale output to supply biosimilars and high-potency oral solids. K-90 and K-120 grades, priced 25-30% above K-30, enable 8-12-hour release profiles that extend drug life cycles and justify premium pricing. Regulatory hurdles under ICH Q3C demand solvent limits that smaller entrants struggle to meet, further entrenching incumbent suppliers.

In food and beverage, PVPP’s unique polyphenol selectivity stabilizes beer and white wine without stripping aroma, and FDA 21 CFR 173.55 caps usage at 60 g hL⁻¹ for beer, ensuring safety compliance. Craft breweries in the United States deploy PVPP to clarify hazy IPAs while preserving hop oils, a style that grew 18% in 2025. In cosmetics, formulators replaced volatile organic solvents with PVP copolymers for humidity resistance; counterpressure from botanical gums will temper future growth. Industrial uses, including battery binders, are pacing ahead as European gigafactories trial water-based slurries to meet ESG targets.

Geography Analysis

Asia-Pacific controlled 39.27% of the 2025 demand and is forecast to climb at 11.45%. China supplies 45% of global generic APIs, and provincial subsidies for excipient parks lower land and utility costs by up to 40%, deepening regional competitive advantage. India commissioned 25 new tablet-compression lines between 2024-2025 and remains the fastest-growing importer of pharmaceutical-grade PVP. South Korea’s and Japan’s display industries divert incremental tonnage to foldable OLED adhesive, while ASEAN contract manufacturers expand cosmetic exports that embed PVP copolymers for North American brands.

In North America, FDA draft guidance on continuous manufacturing encourages direct-compression formulations that rely on spray-dried PVP, benefiting BASF’s Geismar and Ashland’s Wilmington plants. Canada’s cannabis edibles segment uses PVP to bind compressed tablets for dose uniformity under Health Canada rules. Mexico’s generics growth surpasses USD 2.1 billion in exports and draws on PVP-bound tablets to satisfy bioequivalence tests across Latin America.

In Europe, REACH registration above 1,000 t/y costs more than EUR 500,000, favoring established suppliers. Germany anchors pharmaceutical-grade demand, yet tablet production migrates eastward for cost reasons. Post-Brexit U.K. labeling divergence adds GBP 15,000-25,000 per excipient SKU, complicating supply chains. Nordic innovators boost demand for PVP in solid shampoo bars and powder cleansers that save water.

Brazil’s generic sector imports PVP from Indian suppliers to meet Anvisa bioequivalence criteria, while Saudi Arabia approved 12 new tablet lines that specify PVP K-30 under Vision 2030 diversification. South Africa leads African hair-care adoption of PVP copolymers for relaxers, and local pharmacies in Nigeria experiment with powder PVP for extemporaneous capsules despite electricity constraints.

Competitive Landscape

The Polyvinylpyrrolidone market is moderately consolidated. Entry barriers stem from the USD 15 million-plus price tag of monomer purification lines and the need for GMP-audited analytics. BASF invests heavily, adding 3,000 t/y at Ludwigshafen for pharmaceutical-grade K-90 and K-120 completion by 2027. Ashland partners with Aprecia to co-develop PVP filaments for 3D-printed tablets, illustrating the pivot toward high-margin applications. Technology trends bifurcate: Western incumbents pilot continuous K-value monitoring and supply-chain transparency under 2024 IPEC guidance, whereas Chinese firms accelerate nameplate capacity to chase volume in cosmetics and industrial grades.

Polyvinylpyrrolidone Industry Leaders

Ashland

BASF

Boai NKY Pharmaceutical Co., Ltd.

Nippon Shokubai Co., Ltd.

KURARAY CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Researchers unveiled a novel drug delivery system in a study. The system, harnessing the properties of a zirconium metal organic framework, sodium alginate, and polyvinylpyrrolidone, aims to fine-tune drug release dynamics. The innovative blend targets drug delivery in a pH-responsive manner and boosts stability.

- September 2025: PharmaExcipients AG explored the reworking potential of polyvinylpyrrolidone (PVP) K-25 at varying concentrations. The research centered on the physical properties of the mixtures and the resultant paracetamol tablets. The data from tests underscored PVP K-25's efficacy as a binder, highlighted by the consistent physical properties of both the mixtures and the final paracetamol tablets.

Global Polyvinylpyrrolidone Market Report Scope

Polyvinylpyrrolidone is a nonionic water-soluble polymer with good solubility in water and various organic solvents, good affinity to various polymers and resins, high hygroscopicity, good film formation properties, superior adhesiveness to various substrates, chelate/complex formation property.

The polyvinylpyrrolidone market is segmented by form (powder and liquid), application (pharmaceuticals, cosmetics, food and beverage, adhesives, and other applications), and geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The report offers market size and forecasts for the polyvinylpyrrolidone market in volume (tons) for all the above segments.

| Powder |

| Liquid |

| Pharmaceutical |

| Food and Beverage |

| Cosmetics |

| Adhesives |

| Other Applications (Industrial, etc.) |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| By Application | Pharmaceutical | |

| Food and Beverage | ||

| Cosmetics | ||

| Adhesives | ||

| Other Applications (Industrial, etc.) | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global PVP demand be by 2031?

Forecasts indicate consumption will reach 150.84 kilotons by 2031, reflecting an 8.17% CAGR from 2026.

Which segment adds the most incremental volume?

Pharmaceuticals will supply the largest absolute increase, expanding at 11.87% per year as generics and controlled-release formats multiply.

Why are powder grades preferred in tablet manufacturing?

Spray-dried powder flows consistently into direct-compression presses, lowers dust-explosion risk, and aligns with continuous-manufacturing protocols.

What is driving Asia-Pacific’s leadership?

China’s integrated monomer plants, India’s expanding CDMOs, and South Korea and Japan’s flexible-display investments propel regional demand growth above 11%.

How will 3D-printed drugs affect PVP suppliers?

Binder volumes are small today, but FDA-cleared pathways and ongoing partnership activity suggest a niche high-margin outlet that could gain momentum after 2026.

Page last updated on: