Polyurea Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

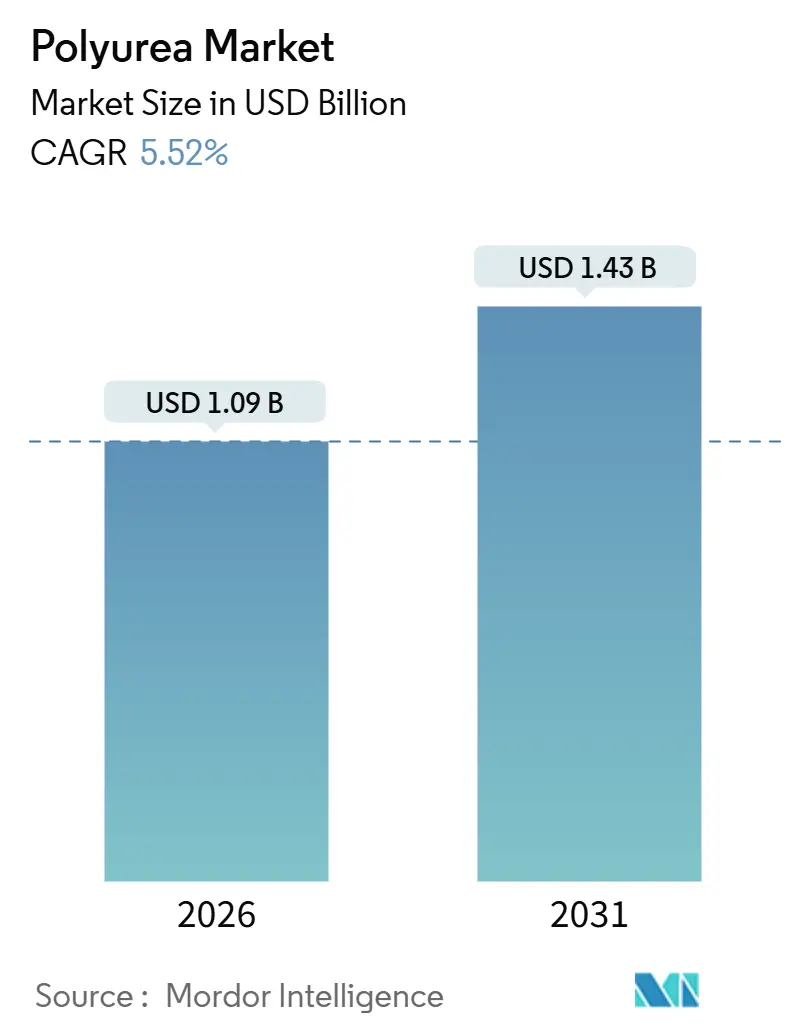

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

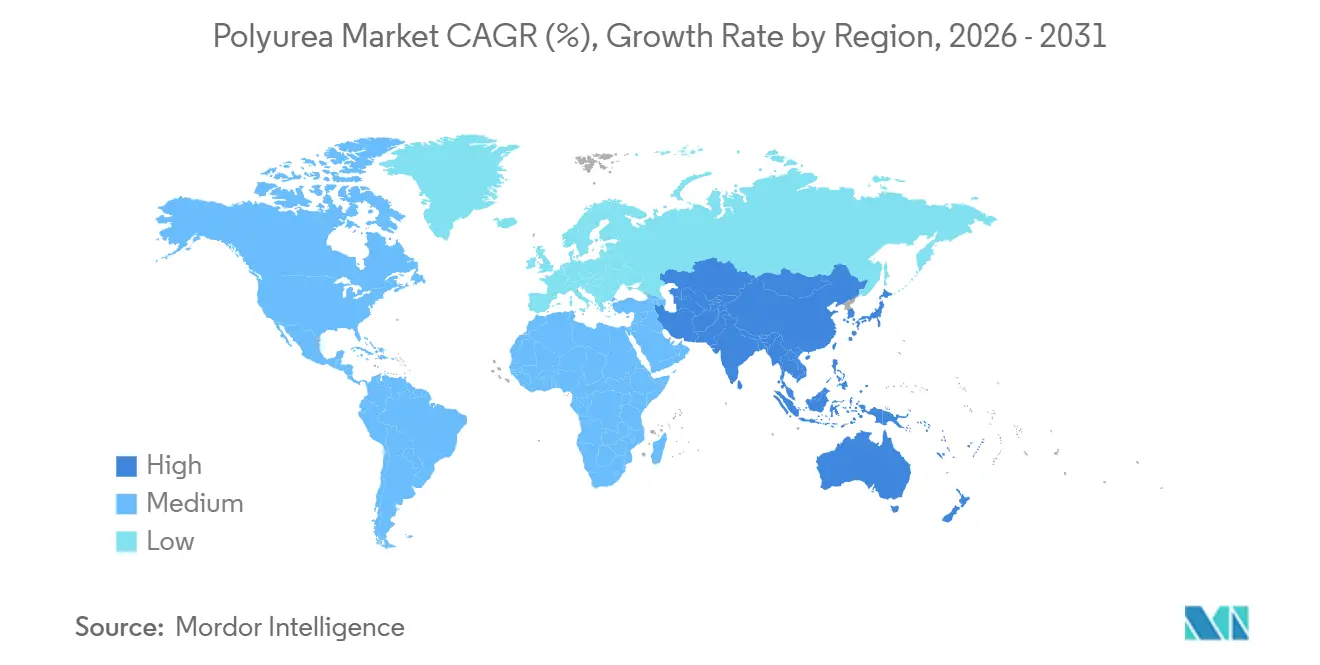

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

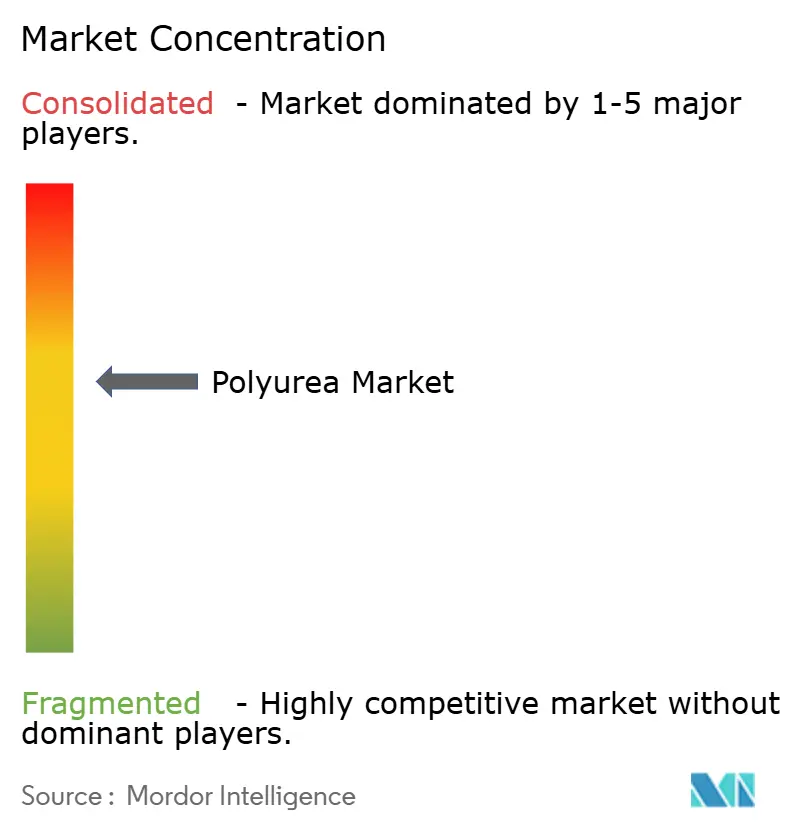

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyurea Market Analysis by Mordor Intelligence

The Polyurea Market size is estimated at USD 1.09 billion in 2026, and is expected to reach USD 1.43 billion by 2031, at a CAGR of 5.52% during the forecast period (2026-2031). The polyurea market is gaining momentum because asset owners now value rapid return-to-service more than lowest upfront cost, a shift that favors sub-second-gel polyurea over epoxy and traditional polyurethane systems. Oil and gas midstream operators are channeling refurbishment budgets toward corrosion-control programs as pipelines installed during the 1970s and 1980s approach end-of-design life. Automotive OEMs are adding polyurea to electric-vehicle battery packs to block thermal-runaway propagation and moisture ingress, while infrastructure owners specify the technology to keep bridges, water-treatment assets, and metro corridors in service during rehabilitation. Supply-side initiatives such as BASF’s 2025 capacity expansion in China and PPG’s roll-out of energy-curable backers confirm that producers view the polyurea market as a structurally growing space poised to replace slower-curing chemistries.

Key Report Takeaways

- By chemical structure, aromatic polyurea captured 66.89% polyurea market share in 2025 and aliphatic polyurea is forecast to progress at a 6.12% CAGR through 2031.

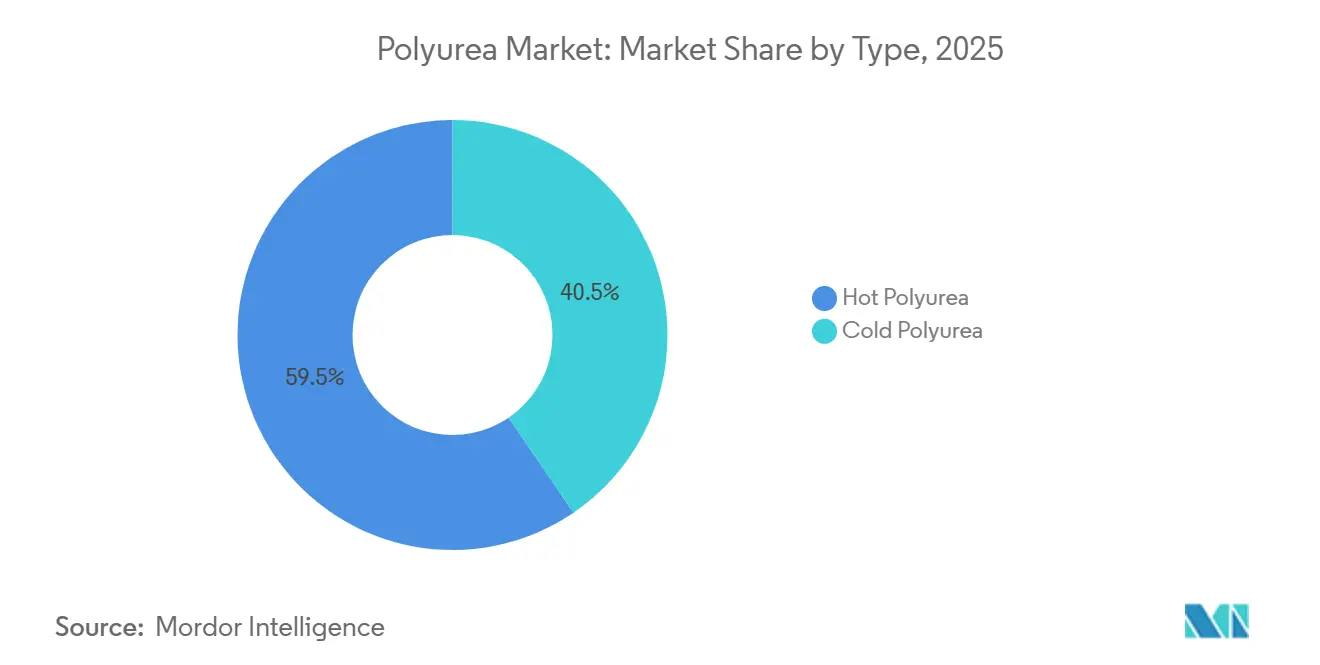

- By type, hot polyurea controlled 59.51% of the polyurea market size in 2025, while cold systems are advancing at a 6.67% CAGR to 2031.

- By product form, coatings led with 64.71% of the polyurea market size in 2025; sealants are the fastest-growing form at 7.12% CAGR.

- By end-use industry, construction dominated with 40.32% of 2025 revenue and energy and power is on track for a 7.21% CAGR through 2031.

- By geography, North America accounted for 40.92% of the 2025 value, whereas the Asia-Pacific is expanding at a 7.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyurea Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from infrastructure rehabilitation | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Surge in corrosion-control spending by oil and gas midstream operators | +0.9% | North America, Middle East, Asia-Pacific | Medium term (2-4 years) |

| Rapid adoption in EV battery-pack protection | +1.4% | Asia-Pacific, Europe, North America | Short term (≤ 2 years) |

| Mainstream shift from epoxy/polyurethane to fast-return polyurea coatings | +1.1% | Global | Medium term (2-4 years) |

| Regulatory push for VOC-free protective coatings | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Infrastructure Rehabilitation

Aging civil infrastructure drives owners to polyurea because projects can reopen within hours, not days. Dubai’s 2025 Hatta Dam pipeline restoration lined 24 kilometers of tunnels with polyurea and maintained service continuity. Thames Water in the United Kingdom used chemistry to waterproof valve chambers in dense urban corridors and limit excavations.[1]Teknos, “Case Study: Hatta Dam Pipeline Rehabilitation,” teknos.com The United States still faces a USD 2.6 trillion funding gap for bridges, culverts, and tunnels; polyurea extends asset life by two to three decades without lane closures, reducing indirect costs that often exceed material premiums threefold. The formulation’s tolerance for damp surfaces and low-temperature cures widens the seasonal work window, which is critical in cold-climate markets. As cities earmark stimulus funds for fast-track bridge deck overlays, polyurea is positioned as the only membrane that meets overnight-reopening requirements.

Surge in Corrosion-Control Spending by Oil and Gas Midstream Operators

Midstream pipeline networks installed between 1970 and 1985 are reaching critical maintenance thresholds. Polyurea membranes eliminate pinholes and prevent cathodic disbondment more reliably than fusion-bonded epoxy wraps, especially on girth welds and complex geometries. TIB Chemicals’ PROTEGOL polyurethane pipeline coatings demonstrated field success on North American retrofits and underscored polyurea’s chemical compatibility with sour gas. Operators now bundle inline inspection, grit blasting, and polyurea over-sprays into single mobilizations to reduce downtime. API 1169 inspection standards increasingly reference seamless membranes for external protection, a wording that implicitly favors polyurea systems. Because polyurea cures within seconds at ambient pipe temperature, crews can backfill trenches on the same shift, cutting restoration expenses by 20% relative to epoxy.

Rapid Adoption in EV Battery-Pack Protection

Electric-vehicle assembly plants have integrated polyurea into battery enclosures to meet flammability and impact-absorption targets without extending cycle time. Huntsman’s POLYRESYST S4010C, launched in February 2025, meets UL 94 V-0 and adds less than five minutes to takt. Covestro’s Baydur PUL 4201 enables sub-5-minute demolding cycles and bonds to aluminum, composite, or thermoplastic housings with no primer. OEMs report 10% weight savings versus steel skid plates, while elongation surpasses 250%, which improves drop-test performance. As global EV production targets 30 million units by 2030, battery manufacturers view polyurea as a low-cost insurance policy against warranty claims linked to coolant leaks or thermal events. Government safety agencies in China, Korea, and the European Union are drafting protocols that will formalize such protective measures, further institutionalizing demand.

Mainstream Shift from Epoxy/Polyurethane to Fast-Return Polyurea Coatings

Manufacturing plants frequently shut down production areas for less than one shift when recoating surfaces. Polyurea floors accept foot traffic within one hour and vehicular loads inside four hours, compressing shutdown windows by up to 90%. Food processors, pharmaceutical cleanrooms, and semiconductor fabs—where downtime costs can top USD 150,000 per hour—recoup polyurea’s 20-30% material premium in a single maintenance event. The chemistry cures at 95% relative humidity and sub-freezing temperatures, mitigating expensive dehumidification. Contractors also cite lower odor and zero-VOC benefits, enabling adjacent line operations to continue. Consequently, construction end-users, who already account for 40.32% of polyurea market demand, are substituting epoxy with polyurea for parking decks, cold-storage floors, and secondary containment basins.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in isocyanate and amine feedstock prices | -0.8% | Global | Short term (≤ 2 years) |

| Short pot-life raises applicator skill and equipment cost | -0.5% | Global | Medium term (2-4 years) |

| Emerging PFAS-like substance bans impacting certain chain extenders | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Isocyanate and Amine Feedstock Prices

BASF announced a USD 0.10/lb price hike for North America in July 2024 to offset inflation and logistics pressures[2]BASF, “North America Polyurethane Systems Price Adjustment,” basf.com. Smaller formulators without integrated feedstock assets either pass costs to customers or forfeit margin, slowing adoption in residential waterproofing, where acrylic membranes remain stable. Contracting firms ask for 60-day price holds that many suppliers cannot honor, complicating tender processes. Volatility has also squeezed working capital because contractors must pre-buy raw materials to lock pricing, tying up cash on the application side as well.

Short Pot-Life Raises Applicator Skill and Equipment Cost

Two-component polyurea gels in 5-15 seconds, so plural-component rigs operate at 2,000 psi and cost USD 15,000-50,000. Poor mixing produces pinholes or delamination, incurring expensive rework. Rhino Linings, Nukote, and SPI Coatings conduct certification courses, but Southeast Asia and Latin America still lack an applicator base. Cold-pour variants extend pot life to 10-20 minutes yet give up seamless finish and shore hardness. Emerging markets with low wage rates accept longer cures from epoxy, slowing polyurea penetration. Equipment financiers offer leasing solutions, but interest rates above 9% in several developing countries deter uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Structure: Aromatic Dominance with Aliphatic Gaining UV-Stable Applications

Aromatic grades delivered 66.89% polyurea market share in 2025 and benefitted from raw-material savings of 20-30% versus aliphatic analogs. Aromatic formulations line tanks, secondary containments, and buried concrete because UV exposure is limited. Their lower cost keeps total installed pricing competitive, which is essential for large-surface municipal projects in North America and Europe. However, ultraviolet light yellows and chalks aromatics, so asset owners must overspray topcoats or accept aesthetic degradation on facades.

Aliphatic polyurea is growing at a 6.12% CAGR thanks to parking decks, bridges, and external building skins that require color stability. PPG’s July 2024 DuraNEXT launch added UV-curable clearcoats that maintain gloss on coil-coated metal, confirming demand for exterior-grade clusters. Hybrid aromatic-aliphatic blends deliver adequate color retention at a 10-15% cost premium, offering a middle path for bridge owners who want a decade-long repaint window. Cost declines for aliphatic isocyanates are projected as new Asian capacity comes online, gradually narrowing the price gap that underpins aromatic leadership.

By Type: Hot Spray Systems Lead, Cold Pour Expands in Niche Segments

Hot polyurea systems held 59.51% of the polyurea market size in 2025 because high-pressure rigs can apply more than 1,000 ft² per hour with seamless results. Offshore wind blade erosion shields, bridge-deck membranes, and bulk tank linings specify hot-spray because membrane cohesion must be absolute. Component temperatures run at 65-75 °C to cut viscosity and atomize heavy pre-polymers that deliver tensile strengths above 25 MPa.

Cold-pour systems are posting a 6.67% CAGR on the promise of ease of use. Contractors without plural-component equipment can hand-trowel or low-pressure-spray EV battery packs, secondary containments, or HVAC ducts. Huntsman’s POLYRESYST S4010C cold-cure provides sub-5-minute demolding, enabling inline automotive coating. The downside remains surface finish and slightly lower mechanical properties, yet incremental research and development is closing the gap. Lower rig investment is especially attractive in India, Indonesia, and Brazil, where infrastructure budgets reward technologies that fit within modest capex envelopes.

By Product Form: Coatings Dominate, Sealants Surge in High-Movement Joints

Coatings accounted for 64.71% of the 2025 volume because polyurea’s abrasion resistance, chemical tolerance, and zero-VOC profile make it the default protective membrane across civil works. BASF’s Elastocoat surfaces container ships and wastewater basins, proving versatility across marine and municipal domains. Linings remain vital for interior pipe and tank surfaces, but grow slowly given cyclical capital spending in chemical processing.

Sealants are rising at 7.12% CAGR due to ±50% joint-movement capability, outclassing polyurethane at ±25% and silicone at ±35%. Bridge expansion joints in seismic zones, curtain-wall perimeters on super-tall structures, and airport runways now specify polyurea to safeguard life-cycle costs. Cartridge-dispensed formats bring polyurea technology to general contractors, widening market reach beyond specialized applicators. Integration of color packs and low-odor packages is removing the last usability hurdles, broadening uptake in vertical facade joints and high-traffic plazas.

By End-Use Industry: Construction Leads, Energy and Power Accelerates

Construction delivered 40.32% polyurea market share in 2025 because bridge decks, parking structures, and concrete floors demand membranes that cure in sub-freezing conditions and resist salt, abrasion, and vehicular loads. Dubai’s Hatta Dam project validated tunnel overlays that kept water flowing during lining. Automotive end-use continues to climb on EV battery protection and underbody coatings, integrating directly into robotic paint shops without new booths.

Energy and power is the fastest-growing vertical at 7.21% CAGR as offshore wind farms coat blades against rain erosion and UV degradation, and solar farms seal panel frames against moisture ingress. Rain-impact erosion extends blade life by five-plus years, avoiding USD 300,000 replacement components. Polyurea also lines lithium-ion storage containers, providing dielectric barriers that double as fire-retardant layers. With global renewables capacity heading toward 11,000 GW by 2030, this vertical will outpace construction on a proportional basis even if absolute size remains lower until the next decade.

Geography Analysis

North America controlled 40.92% of the 2025 value, supported by mature applicator networks and high labor costs that tilt cost-of-downtime equations in favor of rapid-cure chemistries. The Infrastructure Investment and Jobs Act directs USD 110 billion toward bridge and highway repair, ensuring steady demand for deck overlays and expansion-joint sealants. Canada’s municipal infrastructure bank also funds culvert relining, while Mexico’s industrial-park boom pushes demand for chemical-resistant floors in electronics and automotive corridors. BASF, Covestro, Huntsman, and PPG run integrated resin facilities across Texas, Louisiana, and Ontario, allowing just-in-time shipment of pre-polymers and curatives, which reduces lead times to three days for most projects.

Asia-Pacific is generating the fastest revenue expansion at a 7.93% CAGR through 2031. China’s Belt and Road corridor, India’s dedicated freight rail system, and Korea’s USD 20 billion EV battery supply-chain buildout are channeling large coating budgets. BASF’s 2025 move to raise Caojing resin capacity to 18,800 tons per year underpins regional supply. Government-sponsored metro expansions in Delhi, Chennai, and Guangzhou have specified polyurea for tunnel waterproofing owing to rainfall-induced ground settlement events. Southeast Asian contractors remain equipment-price sensitive, so cold-pour variants see heightened uptake. Regional specialty suppliers are partnering with Japanese trading houses to train applicators and accelerate specification writing.

Europe maintains a mature yet profitable market, rooted in VOC caps and refurbishment cycles for legacy infrastructure. Germany’s autobahn bridge retrofits and the Nordic region’s climate-adaptation programs employ polyurea for frost-resistant deck coatings. Maritime refurbishment in Spain and Italy is steady as shipyards invest in quicker turnaround for cruise vessels that lost revenue during pandemic shutdowns. Middle East states are adopting polyurea for desalination plant linings and tank farms; Saudi Arabia’s Aramco and ADNOC in the UAE are already piloting spray systems. South America shows localized demand tied to Chilean copper-mine expansion and Brazilian offshore developments.

Regulatory Landscape

Polyurea adoption in protective coatings and containment is shaped by chemical control regimes and environmental-performance documentation. In Europe, the REACH framework governs registration and safe use of relevant isocyanates, amines, and additives across the supply chain, affecting SDS content, downstream user obligations, and substitution discussions when substances face tighter scrutiny. In the United States, polyurea-related substances can fall under TSCA new-chemical review pathways, and EPA determinations (for example, polymer exemption criteria under 40 CFR 723.250 referenced in TSCA Section 5 determinations) influence how suppliers structure polymer chemistries and documentation for market access.

At the application level, water and soil protection rules and VOC limits drive specification and permitting. Germany's Federal Water Act (WHG) and related water hazard class practices (WGK) frame how formulations used near water, groundwater, and soil are classified and handled on sites such as tanks, secondary containment, and wastewater assets. Environmental product declarations and standardized LCA reporting are becoming more common in procurement, with EPD International validating an EPD for solvent-free polyurea resins on May 30, 2025 under EN 15804 and ISO 14025, which improves supplier positioning when public and infrastructure buyers request verified environmental documentation.

Value Chain Analysis

The polyurea value chain starts with upstream petrochemical feedstocks and specialty intermediates converted into the A-side isocyanate component (often MDI-based) and the B-side amine-terminated resin blend, which may include chain extenders, pigments, fillers, and performance additives. Integrated producers such as BASF, Covestro, and Huntsman supply key intermediates and prepolymers, while a broad layer of formulators tailor aromatic and aliphatic systems for hot-spray and cold-pour use cases. Supply tightness and trade frictions around MDI can transmit into coating-system pricing and availability, shaping formulators' raw-material strategies and inventory policies.

Midstream activity centers on blending, packaging, and distribution through direct-to-applicator channels and regional stocking distributors, followed by downstream application that is highly dependent on equipment and labor. Because polyurea cures extremely fast, plural-component proportioning equipment and certified applicator capability are central to delivering performance, which makes training and certification programs (for example, those run by major applicator networks) an important service layer. End users span infrastructure rehabilitation, oil and gas corrosion control, industrial flooring, and automotive protection, and purchase decisions often bundle materials with surface preparation, inspection, and QA documentation, particularly in secondary containment and other regulated environments.

Competitive Landscape

The polyurea market is moderately consolidated, with the top five players accounting for a significant market share, though dozens of regional formulators fill niche gaps. BASF, Covestro, Huntsman, and PPG leverage integrated isocyanate production and global logistics to buffer feedstock price swings. BASF’s turnkey Elastocoat lines offer warranties supported by in-house MDI and polyol manufacturing, an advantage small-volume blenders cannot replicate. Huntsman collaborates with Graco on smart-spray guns that embed RFID cartridges to calibrate mix ratios, curbing rework costs.

Technology innovation now centers on robotic spray arms that use lidar to map surface topography and adjust spray paths in real time, trimming wasted material. Self-healing polyurea under study at the University of Stuttgart embeds micro-capsules that release amine curatives under stress, extending membrane life in seismic zones. Hybrid polyurea-polyurethane films balance cost and elongation, aiming at parking decks where owners accept a small cure-time trade-off for lower installed cost. Suppliers slow to deliver PFAS-free chain extenders risk premature obsolescence in North America and Europe as regulators ratchet restrictions between 2026 and 2028.

Polyurea Industry Leaders

PPG Industries Inc.

The Sherwin-Williams Company

BASF SE

Huntsman International LLC

Rhino Linings Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are most visible where owners pay for downtime and where specifications reward fast return-to-service, seamless membranes, and low-VOC profiles. Public infrastructure programs provide an addressable pipeline for bridge decks, tunnels, and water assets, and the United States Infrastructure Investment and Jobs Act allocation of USD 110 billion toward bridge and highway repair is a concrete example of funded work that aligns with polyurea's rapid cure and rehabilitation benefits. The market also has whitespace in expanding applicator capacity and certification coverage in regions that are equipment cost sensitive, where cold-pour variants and distributor-led training can broaden adoption beyond specialist crews.

On the product side, EV battery protection, offshore and renewable-energy assets, and higher-performance sealants create room for differentiated formulations that address fire, moisture ingress, and joint-movement demands without adding cycle time. Huntsman's February 2025 launch of POLYRESYST S4010C for EV battery-pack protection and BASF's 2025 China capacity expansion signal continued supplier focus on higher-value niches. At the same time, 2026 raw-material actions and supply disruptions underline the need for resilience, since MDI price increases by major suppliers and reported capacity tightening during scheduled maintenance windows have pushed more formulators to qualify alternate sourcing, optimize hybrid formulations, and prioritize projects with clear life-cycle and downtime payback.

Recent Industry Developments

- June 2026: The Sherwin-Williams Company and Do it Best Group announced a long-term strategic partnership to strengthen the paint category for independent retailers, with Sherwin-Williams taking on expanded manufacturing and brand responsibilities. The move broadens Sherwin-Williams' reach through an established dealer network and supports more consistent supply and service levels for contractors that also purchase high-performance protective systems.

- February 2025: BASF expanded production capacity for key polyurea-related chemistries in China, strengthening regional supply for coatings and infrastructure applications. Additional local capacity improves lead times and supports specification-driven projects in Asia-Pacific that require tight delivery windows.

- July 2024: PPG introduced DuraNEXT energy-curable primers, basecoats, and clearcoats for coil-coated metal, emphasizing rapid cure and solvent-free formulations. This reinforces the industry shift toward faster, lower-emission coating systems and adds adjacent technology options that can be paired with exterior-grade polyurea requirements such as UV-stable topcoat systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from polyurea materials sold as pure or hybrid systems that cure mainly through an isocyanate-amine reaction, and are used as protective coatings, linings, or sealants across end-use industries.

Scope exclusions: It excludes polyurea-thickened greases, polyaspartic blends sold as separate chemistries, captive in-house consumption, and application equipment.

Segmentation Overview

- By Chemical Structure

- Aromatic

- Aliphatic

- By Type

- Hot Polyurea

- Cold Polyurea

- By Product Form

- Coatings

- Linings

- Sealants

- By End-use Industry

- Construction

- Paints and Coatings

- Automotive

- Industrial

- Maritime

- Other End User Industries (Energy and Power, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting shape of demand and supply, and then to anchor model inputs that can be checked year to year. We mainly referred to public and official sources such as the US Census Bureau construction spending series, Eurostat construction output indicators, UN Comtrade trade flows for relevant chemicals, and worker-safety and environmental references from US agencies like the US EPA and OSHA.

To translate these signals into a workable market model, we also reviewed company annual reports, investor presentations, product technical datasheets, and association websites that track coatings and waterproofing practices. In a few cases, paid subscriptions for company financials and patent databases were used to cross-check product activity and corporate exposure to polyurea, which helps reduce blind spots from disclosures that focus only on sales narratives. The desk sources listed here are illustrative only, and we also consulted many other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with formulators, raw material participants, applicators or contractors, distributors, and large end users, so we could confirm what is actually being specified and purchased. Since polyurea demand is global, feedback was balanced across APAC, EMEA, and the Americas to test assumptions on price movement, adoption in waterproofing and industrial protection, and the split between pure and hybrid systems.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 36% |

| Smaller Players: 22% | Managers: 54% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where construction and industrial activity indicators are mapped to polyurea use cases, then adjusted using trade and production signals to keep the demand pool realistic. Once the demand pool is set, we apply market-specific variables such as waterproofing and rehabilitation activity, industrial maintenance intensity, infrastructure protection spending, adoption of fast-cure spray systems, and average selling price ranges by formulation type.

Those totals are then checked with selective bottom-up approximations, mainly through sampled supplier and channel discussions, plus average selling price times volume logic for common application types. This helps confirm that the final number is not being driven by a single unstable assumption. Where direct volume information is patchy, gaps are handled by using proxy indicators such as construction repair cycles and industrial capex patterns, then re-tested with primary feedback before finalizing. For forecasting, scenario analysis was used so the base case reflects expected construction cycles and industrial maintenance spending, and the key drivers are refreshed based on expert expectations for adoption and pricing over the period.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, where model outputs are compared against trade movements, construction and industrial indicators, and the pricing direction heard in primary calls. If a region or year shows an unusual jump, we re-check inputs, revisit scope boundaries, and re-contact sources when the variance cannot be explained through a clear market development.

Before sign-off, the work is reviewed in steps so calculation logic, currency handling, and assumptions are consistent across regions and time periods. The report is refreshed annually, and interim updates are made when material changes occur, including major capacity moves, regulation shifts affecting usage, or sharp feedstock-driven price swings. Right before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Polyurea Market Size Compared Against Other Published Estimates

Published market sizes for polyurea can look far apart because the market boundary is not always applied the same way, and the timing of the current-year estimate differs by publisher. Differences also show up when one study leans more on application spend proxies, while another leans more on material outputs and trade, which can shift the total depending on how imports, exports, and captive use are handled.

Key gaps usually come from what is counted as polyurea versus adjacent chemistries, whether application equipment and services are included, and how hybrid systems are treated when products are positioned as coatings versus broader waterproofing solutions. By tracking first point of sale revenues from formulators and refreshing scope checks each update, Mordor Intelligence keeps the polyurea total centered on two-component polyurea systems and avoids inflating the market with greases, polyaspartic-only products, or applicator equipment.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.09 B (2026) | |

| Global Consultancy A | USD 0.89 B (2024) | Uses an earlier base year and a broader proxy-led demand build tied to infrastructure spend, and the inclusion line between polyurea and adjacent waterproofing chemistries is not clearly stated in the public summary. |

| Market Publisher B | USD 0.91 B (2024) | Relies on a 2024 snapshot and segment framing that can mix product groups, which may undercount later adoption in fast-growing APAC markets and can also shift totals depending on how hybrid systems are classified. |

Across the table, the spread is largely explained by base year choice and scope discipline, followed by how adoption and pricing are carried forward between updates. When the market is tied to clear inclusion rules and then checked against trade, end-use activity, and interview feedback, the final estimate becomes easier to trace and repeat with each refresh cycle for planning decisions.

Key Questions Answered in the Report

What is the current value of the polyurea market?

The polyurea market size is estimated at USD 1.09 billion in 2026.

How fast is global demand for polyurea growing?

The market is forecast to post a 5.52% CAGR and reach USD 1.43 billion by 2031.

Which end-use industry is expanding the quickest for polyurea?

Energy and power lead with a 7.21% CAGR through 2031, driven by offshore wind and solar applications.

Why are hot-spray polyurea systems dominant?

Hot-spray rigs apply seamless membranes at high speed and captured a 59.51% share in 2025.

What factor most limits polyurea adoption in emerging markets?

High equipment cost and short pot-life that demand skilled applicators still curb penetration.

Which region is expected to register the highest growth through 2031?

Asia-Pacific is advancing at a 7.93% CAGR, underpinned by large infrastructure programs in China and India.

Page last updated on: