Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

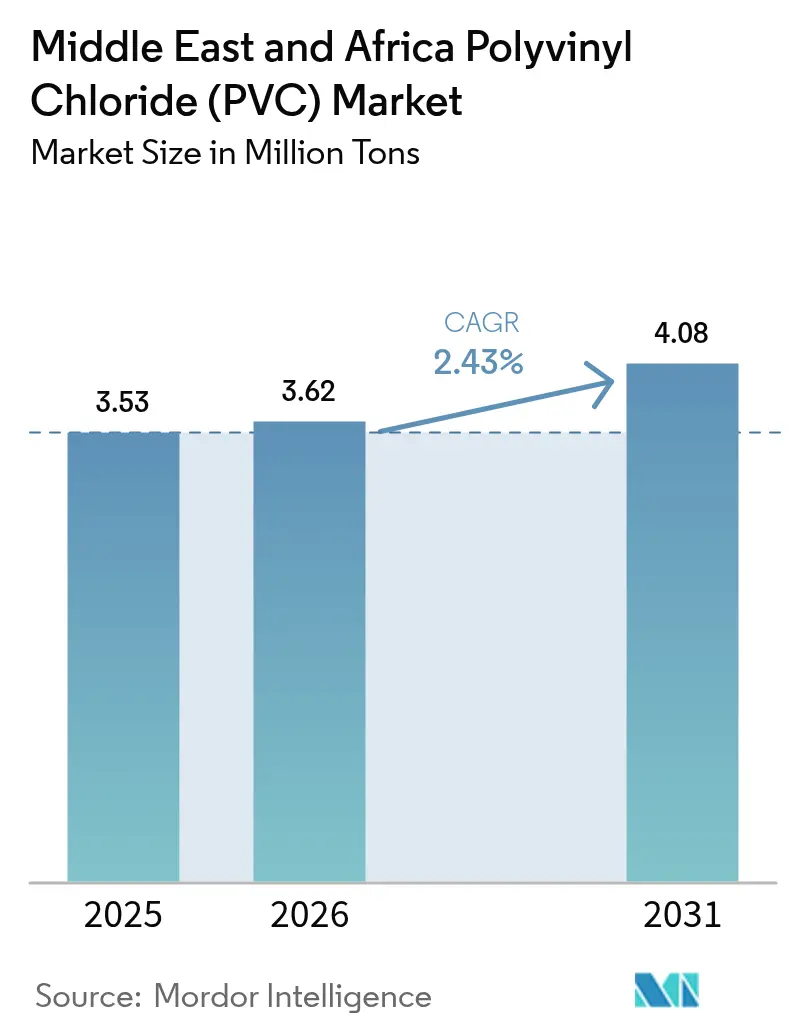

| Base Year Market Size (2025) | 3.53 Million tons |

| Market Volume (2026) | 3.62 Million tons |

| Market Volume (2031) | 4.08 Million tons |

| Growth Rate (2026 - 2031) | 2.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Polyvinyl Chloride (PVC) Market Analysis by Mordor Intelligence

The Middle-East and Africa Polyvinyl Chloride Market size in 2026 is estimated at 3.62 million tons, growing from 2025 value of 3.53 million tons with 2031 projections showing 4.08 million tons, growing at 2.43% CAGR over 2026-2031. Robust sovereign-backed infrastructure programs, massive desalination investments, and rising renewable-energy spending sustain this steady trajectory. Rigid PVC grades dominate volume thanks to pipes, fittings, and structural profiles specified across Gulf Cooperation Council (GCC) “Vision 2030” projects, while bio-based alternatives gain momentum as Environmental, Social, and Governance (ESG) rules tighten. Nigeria’s accelerating power-sector overhaul and Egypt’s petrochemical corridor amplify regional demand diversity. Local-content mandates in Saudi Arabia and the United Arab Emirates (UAE) reshape supply chains, encouraging in-region compounding and shortening lead times. Simultaneously, volatile ethylene and chlorine costs compress margins, prompting producers to expand feedstock integration and circular PVC technologies.

Key Report Takeaways

- By product type, rigid PVC held 57.70% of the Middle-East Africa Poly Vinyl Chloride (PVC) market share in 2025; bio-based PVC is forecast to grow at a 2.71% CAGR through 2031.

- By application, pipes and fittings commanded a 45.70% share of the Middle-East Africa Poly Vinyl Chloride (PVC) market size in 2025, while wires and cables are projected to expand at a 2.59% CAGR.

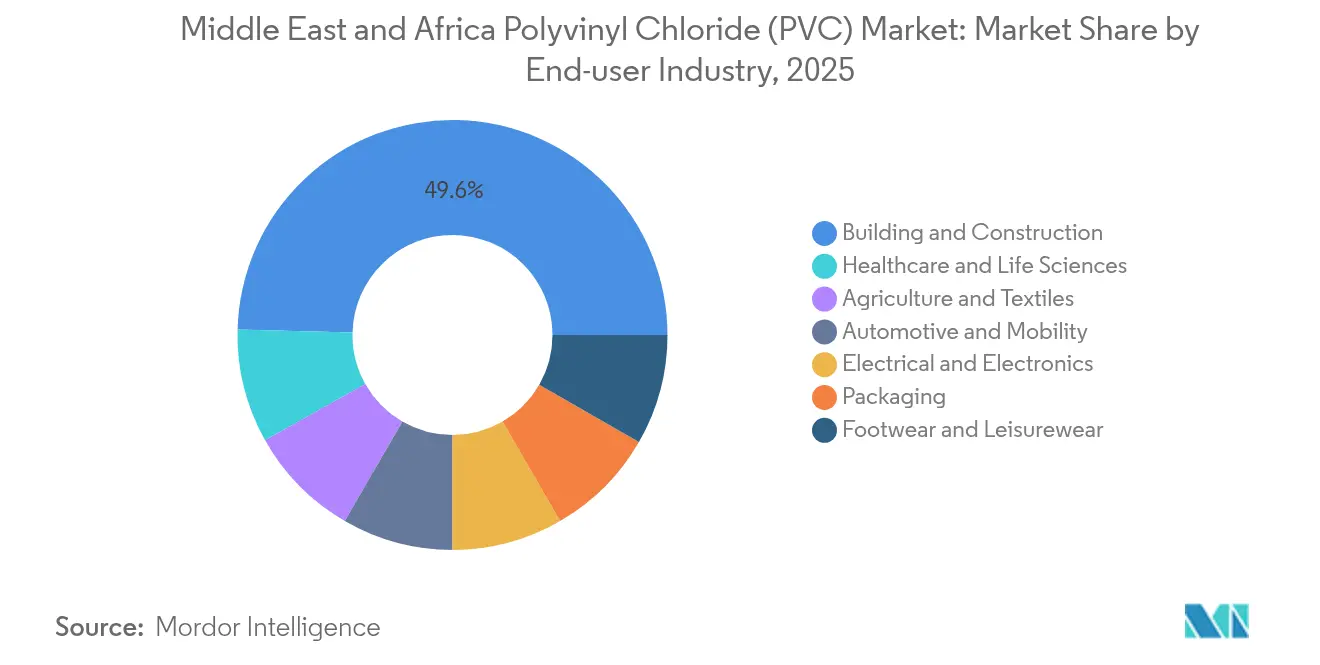

- By end-user, the building and construction sector captured 49.60% of the Middle-East Africa Poly Vinyl Chloride (PVC) market size in 2025; healthcare and life sciences are projected to advance at a 2.66% CAGR through 2031.

- By geography, Saudi Arabia led with a 23.90% revenue share in 2025, whereas Nigeria is poised for the fastest growth, with a 2.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East and Africa Polyvinyl Chloride (PVC) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming public-sector infrastructure programs | +0.8% | Saudi Arabia, UAE, Qatar, Egypt | Long term (≥ 4 years) |

| Rapid expansion of desalination and water-reuse pipe networks | +0.6% | GCC, Morocco, South Africa | Medium term (2-4 years) |

| Grid-hardening and renewable-energy cabling demand surge | +0.4% | Gulf and North Africa | Medium term (2-4 years) |

| Medical-grade PVC capacity build-out in healthcare corridors | +0.3% | UAE, Saudi Arabia, Egypt, South Africa | Long term (≥ 4 years) |

| Local-content mandates driving in-region compounding | +0.2% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Public-Sector Infrastructure Programs Drive Sustained PVC Demand

Multi-billion-dollar national visions underpin a robust order book for the Middle-East and Africa Poly Vinyl Chloride (PVC) market. Saudi Arabia allocated USD 1.2 billion to water infrastructure in 2024, and NEOM’s multi-decade build-out signals prolonged offtake for conduits, profiles, and cladding. Egypt’s USD 10.9 billion Suez Canal Economic Zone petrochemical complex deepens downstream PVC utilization in utilities and industrial structures. Long-term funding structures insulate volumes from oil-price cycles, anchoring a predictable baseline for producers.

Rapid Expansion of Desalination Networks Accelerates Pipe Demand

Water-scarce GCC and North African states are scaling desalination capacity, a pipe-intensive endeavor. Veolia’s USD 320 million award in the UAE and Morocco’s 822,000 m³/day Atlantic facility both specify high-pressure, saltwater-resistant PVC piping[1]Staff Writer, “UAE-Morocco venture to invest USD 25 bln green hydrogen project,” Zawya, zawya.com. The International Desalination Association expects regional capacity to climb 50% by 2030, translating directly into sustained rigid-grade consumption.

Grid-Hardening and Renewable-Energy Cabling Surge

Solar and wind rollouts involve the installation of thousands of kilometers of insulated cabling. Egypt’s 10 GW West Suhag wind project alone requires extensive underground PVC conduits[2]“10 GW wind farm in Egypt takes major step towards construction,” Infinity Power, weareinfinitypower.com. Smart-grid retrofits across the UAE and Saudi Arabia further boost demand for UV-stable conduit systems, driving the Middle-East Africa Poly Vinyl Chloride (PVC) market toward higher-value electrical grades.

Medical-Grade PVC Capacity Build-Out in Healthcare Corridors

Special-economic zones such as Dubai Science Park and NEOM’s Life Science sector are lining up DEHP-free tubing, IV-bag, and diagnostic-grade PVC lines. Regulatory convergence around ISO 10993 biocompatibility and USP Class VI certification pulls regional compounders into higher-margin niches, supporting incremental growth for the Middle-East Africa Poly Vinyl Chloride (PVC) market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating ESG pressure and PVC phase-out clauses | -0.4% | Gulf states with green-building mandates | Medium term (2-4 years) |

| Volatile ethylene and chlorine feedstock pricing | -0.3% | All production hubs | Short term (≤ 2 years) |

| Upcoming bans on lead-based stabilizers | -0.2% | GCC, North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating ESG Pressure and PVC Phase-Out Clauses Challenge Growth

Green-building certifications, such as LEED and local schemes like Dubai’s Al Sa’fat, discourage chlorine-based polymers, pressuring conventional grades and nudging the Middle-East and Africa Poly Vinyl Chloride (PVC) market toward bio-based variants. The European Union’s 0.1% lead-stabilizer cap, effective November 2024, requires exporters to accelerate the development of non-lead formulations, thereby increasing compliance costs.

Volatile Ethylene and Chlorine Feedstock Pricing Pressures Margins

Occidental Petroleum and Westlake Chemical each flagged higher ethylene costs as a drag on 2024–2025 earnings. With crude-linked pricing formulas and electricity-intensive chlorine electrolysis, cost pass-through remains uneven, squeezing margins across the Middle-East Africa Poly Vinyl Chloride (PVC) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid Strength, Bio-Based Momentum

Rigid grades accounted for 57.70% of the Middle-East and Africa Poly Vinyl Chloride (PVC) market size in 2025, driven by pipeline and construction orders. Bio-based PVC advances 2.71% CAGR as builders seek ESG-compliant alternatives. Capacity additions by integrated producers help maintain a balanced regional supply, but the faster adoption of recyclable additives could shift the share toward low-carbon formulations after 2028. The segment’s pricing premium supports visibility in the Middle East Africa Poly Vinyl Chloride (PVC) market.

Second-generation bio-routes using non-food biomass cut cradle-to-gate emissions by up to 90%, helping GCC megaprojects meet Scope 3 targets. Rigid’s resilience, meanwhile, hinges on desalination pipelines and high-rise facades that demand corrosion resistance and structural rigidity. As lead-free stabilizer technologies mature, rigid grades should defend volume even under stricter codes.

By Application: Pipe Dominance, Cable Upswing

Pipes and fittings contributed 45.70% of the Middle-East Africa Poly Vinyl Chloride (PVC) market share in 2025; electrical wires and cables are projected to rise at a 2.59% CAGR to 2031. Desalination and municipal water grids lock in baseline demand, while smart-city fiber-to-the-home rollouts and renewable interconnects lift cable volumes. Films and sheets remain steady in agro-cover and packaging niches. Bottles, profiles, and hoses collectively expand in tandem with domestic consumer spending across North Africa.

By End-User: Construction Core, Healthcare Sprint

Building and construction retained 49.60% of the Middle East Africa Poly Vinyl Chloride (PVC) market size in 2025, anchored by long-dated GCC megaprojects. The healthcare and life sciences sector, the fastest-growing user at a 2.66% CAGR, benefits from new sterile-packaging plants and regionalized medical-device supply chains. Automotive interiors, footwear, and flexible packaging provide diversification but lack scale to displace construction’s primacy before 2030.

Geography Analysis

Saudi Arabia held 23.90% of the Middle East Africa Poly Vinyl Chloride (PVC) market in 2025, supported by Vision 2030 capital expenditure on water infrastructure and mixed-use giga-projects. UAE volumes trail closely, leveraging Veolia’s USD 320 million desalination build and solar-park cabling needs. Qatar, Kuwait, and Bahrain collectively grow in tandem with petrochemical expansions linked to the construction of new ethane crackers.

Nigeria’s 2.51% CAGR through 2031 reflects USD 10 billion annual renewables investment to achieve 10 GW by decade-end. Egypt’s Suez and West Suhag megaprojects underpin steady gains, although EU anti-dumping duties redirect some exports toward domestic consumption. Morocco and South Africa raise rigid-grade imports for desalination and mining upgrades, respectively. Smaller markets such as Oman and Algeria provide incremental upside as pan-African trade corridors mature.

Competitive Landscape

Regional supply is moderately fragmented. Feedstock integration and recycling technologies dominate strategic spending as producers target reductions in Scope 1 and Scope 2 emissions. White-space entrants focus on medical-grade and bio-based PVC, capitalizing on untapped margin pools and regulatory tailwinds. Chemplast Sanmar’s USD 121 million expansion underscores this migration to higher-value formulations. Local-content rules bolster domestic compounding, but capital-intensive chlorine-alkali lines remain clustered within established petrochemical zones. Overall, disciplined capacity additions and differentiated product strategies help stabilize the Middle-East Africa Poly Vinyl Chloride (PVC) market against feedstock swings.

Middle East and Africa Polyvinyl Chloride (PVC) Industry Leaders

SABIC

Egyptian Petrochemical Co.

Sasol

Westlake Chemical Corporation

The Sanmar Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Qatar Vinyl Company, a joint venture of Mesaieed Petrochemical Holding Company, Qatar Petrochemical Company (QAPCO) Q.P.J.S.C, and QatarEnergy, announced to launch of the country’s first PVC plant in Mesaieed in September, with a design capacity of 350,000 tons/year. Europe is expected to be the primary destination for exports.

- September 2024: Egyptian PVC producers Egyptian Petrochemicals Co. (EPC) and TCI Sanmar Chemicals (S.A.E.) announced their prices for September amid soft market sentiment. EPC maintained its price at EGP 49,000/ton (USD 1007/ton) for PVC K67-68, while TCI Sanmar reduced prices by EGP 1,000/ton (USD 21/ton), offering PVC K67-68 at EGP 48,100/ton (USD 867/ton) and PVC K70/K58 at EGP 52,100/ton (USD 939/ton).

Middle East and Africa Polyvinyl Chloride (PVC) Market Report Scope

Polyvinyl chloride (PVC) is a high-strength thermoplastic material widely used in various applications, such as pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses, and tubings. PVC-based pipes and fittings accounted for a major application share by volume and value, followed by profiles, hoses, and tubing. The Middle East & African polyvinyl chloride (PVC) market is segmented by product type, stabilizer type, application, end-user industry, and geography. By product type, the market is segmented into rigid PVC, flexible PVC, low-smoke PVC, and chlorinated PVC. By application, the market is segmented into pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses and tubings, and other applications. By end-user industries, the market is segmented into building and construction, automotive, electrical and electronics, packaging, footwear, healthcare, and other end-user industries. By geography, the market is segmented into Saudi Arabia, South Africa, Qatar, Egypt, United Arab Emirates, and Rest of Middle East & Africa. The market sizing and forecast for each segment are given by volume (in kilo ton).

By Product Type

| Rigid PVC |

| Flexible PVC |

| Low-smoke Zero-Halogen PVC |

| Chlorinated PVC (CPVC) |

| Bio-based PVC |

By Application

| Pipes and Fittings |

| Films and Sheets |

| Wires and Cables |

| Bottles and Containers |

| Profiles, Hoses and Tubing |

| Others (toys, fabrics, 3-D printing) |

By End-user Industry

| Building and Construction |

| Automotive and Mobility |

| Electrical and Electronics |

| Packaging |

| Footwear and Leisurewear |

| Healthcare and Life Sciences |

| Agriculture and Textiles |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| South Africa |

| Egypt |

| Nigeria |

| Morocco |

| Rest of Middle-East and Africa |

| By Product Type | Rigid PVC |

| Flexible PVC | |

| Low-smoke Zero-Halogen PVC | |

| Chlorinated PVC (CPVC) | |

| Bio-based PVC | |

| By Application | Pipes and Fittings |

| Films and Sheets | |

| Wires and Cables | |

| Bottles and Containers | |

| Profiles, Hoses and Tubing | |

| Others (toys, fabrics, 3-D printing) | |

| By End-user Industry | Building and Construction |

| Automotive and Mobility | |

| Electrical and Electronics | |

| Packaging | |

| Footwear and Leisurewear | |

| Healthcare and Life Sciences | |

| Agriculture and Textiles | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Morocco | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

How large is the Middle East Africa Poly Vinyl Chloride (PVC) market in 2026?

It stands at 3.62 million tons and is on track to reach 4.08 million tons by 2031.

Which segment uses the most PVC across the region?

Pipes and fittings dominate with a 45.70% share, reflecting sustained water infrastructure spending.

Why is bio-based PVC growing faster than traditional grades?

ESG mandates and upcoming lead-stabilizer bans are pushing builders toward low-carbon, compliant alternatives, which are expanding at a 2.71% CAGR.

Which country shows the highest growth momentum?

Nigeria leads with a 2.51% CAGR, as it invests USD 10 billion annually to meet its 10 GW renewable energy targets.

What main risk threatens producer margins?

Volatile ethylene and chlorine prices, tied to crude oil swings, compress spreads and increase cost-pass-through pressure.

Page last updated on: