Polyolefin (PO) Shrink Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.55 Billion |

| Market Size (2031) | USD 10.8 Billion |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polyolefin (PO) Shrink Films Market Analysis by Mordor Intelligence

The Polyolefin Shrink Films Market size is expected to grow from USD 8.16 billion in 2025 to USD 8.55 billion in 2026 and is forecast to reach USD 10.8 billion by 2031 at 4.79% CAGR over 2026-2031. Growth reflects the material’s versatility, rising preference for recyclable solutions, and the steady replacement of PVC in food-contact applications. Surging e-commerce volumes, brand demand for 360-degree graphics, and the rapid roll-out of automation-ready thin-gauge cross-linked grades are expanding addressable use-cases for the polyolefin shrink film market. Across regions, Asian manufacturers scale capacity to serve export-oriented consumer goods, while North American converters emphasize tamper-evident wraps that build consumer trust. In Europe, policy pressure accelerates adoption of films containing post-consumer recycled (PCR) feedstock, encouraging proprietary blends that match both performance and recycling targets.

Key Report Takeaways

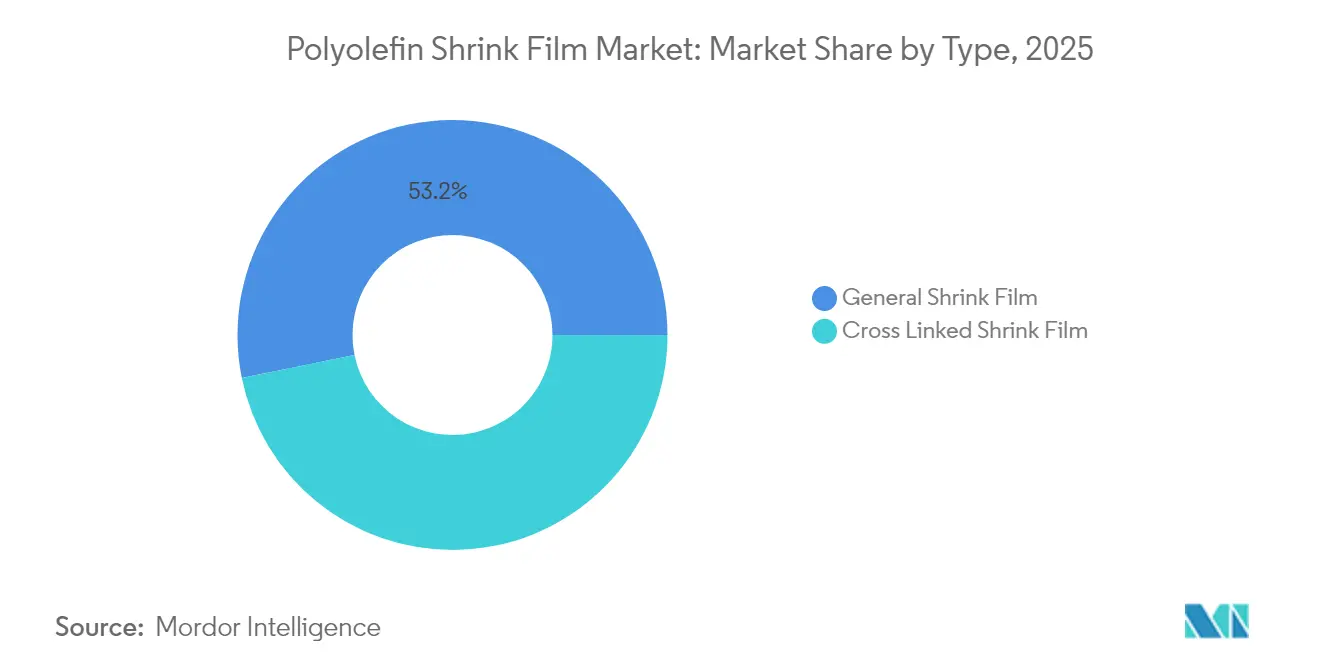

- By type, general shrink film led with 53.20% of polyolefin shrink film market share in 2025; cross-linked grades are projected to post a 6.55% CAGR through 2031.

- By material type, polyethylene controlled 56.40% of polyolefin shrink film market share in 2025, while polypropylene is set to register a 6.92% CAGR to 2031.

- By layer structure, multilayer constructions captured 51.40% share of the polyolefin shrink film market size in 2025 and are forecast to expand at a 6.62% CAGR to 2031.

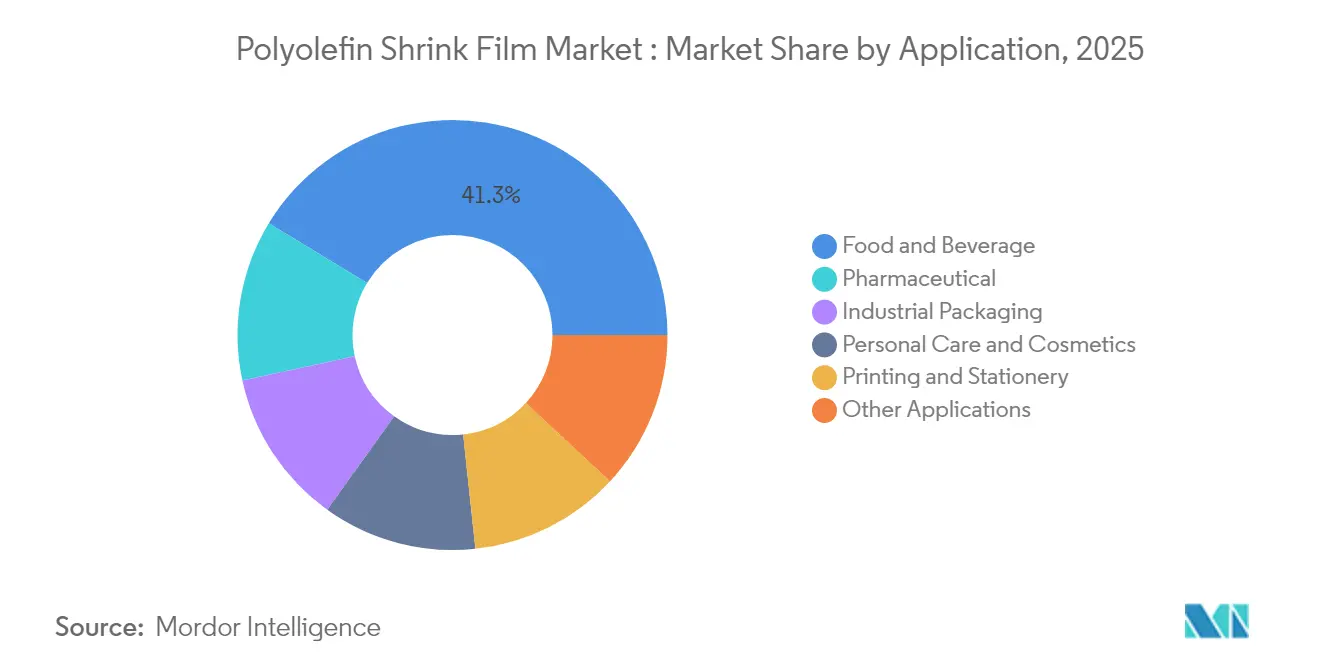

- By application, food and beverage accounted for 41.30% share of the polyolefin shrink film market size in 2025, whereas pharmaceuticals will advance at an 8.47% CAGR between 2026 and 2031.

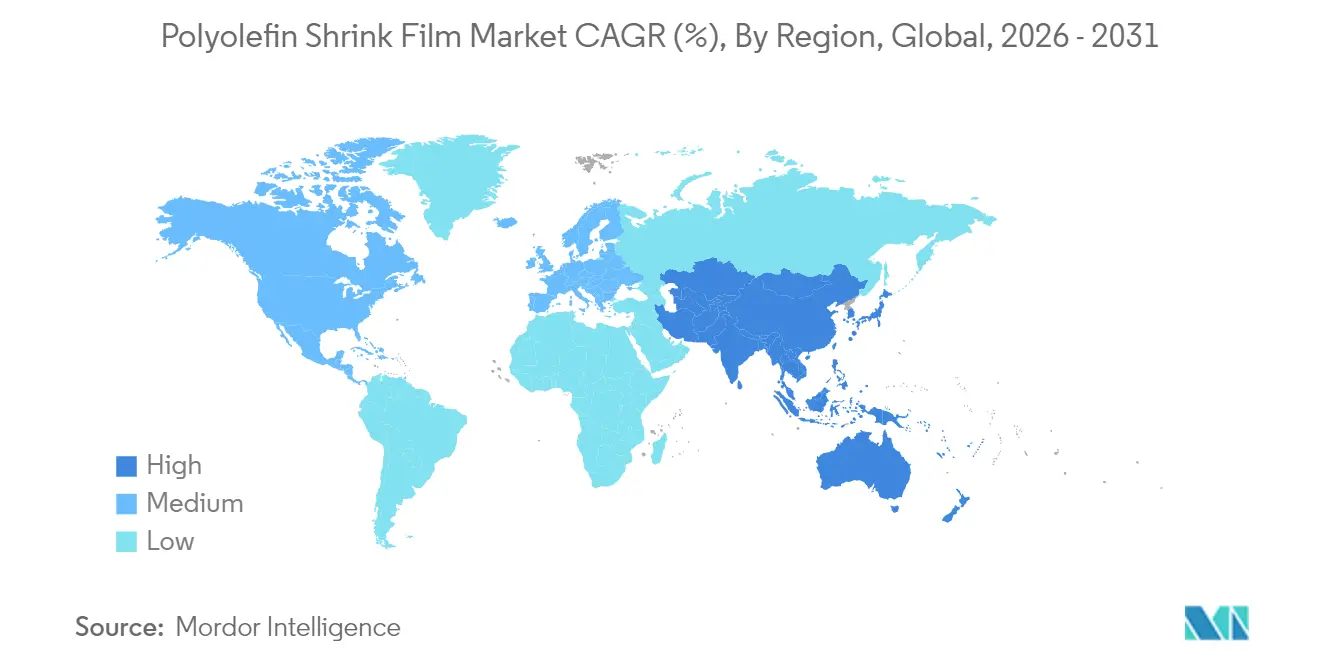

- By geography, Asia Pacific commanded 37.60% of polyolefin shrink film market share in 2025 and is poised for 6.82% CAGR growth through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyolefin (PO) Shrink Films Market Trends and Insights

Driver Impact Analysis*

| Driver | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce demand for tamper-evident wrap accelerating small-pack use in North America | +1.2% | North America, with spillover to Europe | Medium term (3-4 yrs) |

| Shift from PVC to eco-safer POF in European food-contact films | +0.9% | Europe, with global adoption following | Long term (≥ 5 yrs) |

| Demand for High-Quality Printing and Branding | +0.7% | Global, strongest in North America and Europe | Medium term (3-4 yrs) |

| Cost-Effectiveness Compared to Alternatives | +0.6% | Global, particularly impactful in emerging markets | Short term (≤ 2 yrs) |

| Automation-ready thin-gauge cross-linked films driving high-speed lines in Asia | +1.0% | Asia-Pacific, particularly China, India, and Japan | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

E-commerce tamper-evidence demand in North America

E-commerce growth has driven demand for tamper-evident polyolefin shrink films to secure products during transit. North American retailers use these films to protect goods and build consumer trust, with 78% of online shoppers valuing visible tamper-evidence. Intertape Polymer Group's ExlfilmPlus PCR, a polyolefin shrink film with 35% recycled content, addresses security and sustainability needs[1]Intertape Polymer Group, “IPG to Showcase Automation, Consumable and Service Solutions at Pack Expo International 2024,” itape.com. The film combines high clarity with post-consumer recycled content, meeting e-commerce packaging challenges.

PVC-to-POF switch in European food-contact films

European food manufacturers pivot towards recyclable polyolefin films after April 2024 packaging legislation targeting a 5% waste reduction by 2030 [2]European Parliament, “New EU Rules to Reduce, Reuse and Recycle Packaging,” europarl.europa.eu. Parallel plastic taxes in the UK, Spain and Italy penalize films with under 30% recycled content. Clysar’s Store-Drop-Off-qualified EV-HPG illustrates how converters combine food safety, clarity and recyclability.

High-definition printing & branding

Beverage producers such as Anadolu Efes launched 77 new SKUs in 2024, each wrapped in vivid 360-degree graphics to maximize shelf impact. Digital presses speed changeovers, letting converters satisfy shorter promotional runs without plate inventories. The result is a virtuous cycle in which converters invest in wider web, high-opacity white inks, and matte-gloss contrasts that boost brand storytelling in the polyolefin shrink film market.

Cost advantage over alternatives

Film optimisation projects saved Heineken EUR 0.6 billion in 2024 as the brewer cut resin usage and simplified secondary packaging. Producers in emerging regions further curb spend by installing wide-width lines, such as UFlex’s 18,000 MTPA CPP unit, which improves economies of scale.

Restraint Impact Analysis*

| Restraint | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PE & PP resin price volatility | -0.8% | Global, acute in North America | Short term (≤ 2 years) |

| Single-use-plastic levies on over-wrap | -1.1% | Europe, potential global echo | Long term (≥ 4 years) |

| Trade-off between downgauging & shrink force limiting adoption in heavy-duty industrial packs | -0.5% | Global, particularly in industrial applications | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

PE & PP resin price volatility

Shale-feedstock disruptions in the United States heighten raw-material swings that already represent up to 70% of finished film cost. The OECD warns that plastic production may hit 736 million tonnes by 2040, intensifying feedstock competition[3]OECD, “Policy Scenarios for Eliminating Plastic Pollution by 2040,” oecd.org. Converters hedge risks via multi-sourcing, shorter resin contracts, and recipes that dilute virgin inputs with PCR pellets.

Single-use-plastic levies on over-wrap

Germany’s January 2024 levy obliges firms to report units sold and finance litter clean-up schemes, raising administrative and monetary burden. EU rules also require 90% separate collection of single-use beverage containers by 2029. These policies accelerate R&D into store-drop-off-ready sleeves and mono-material bundles within the polyolefin shrink film market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cross-linked films redefine performance expectations

General shrink film held the largest 53.20% polyolefin shrink film market share in 2025, underpinned by affordability and wide processing windows. The segment’s clarity and ease of printing keeps it entrenched in food multipacks and promotional bundles across supermarkets. Yet converters increasingly upsell cross-linked grades where puncture resistance, scuff holdout and thinner profiles allow faster line speeds without wrap failure.

Cross-linked output is forecast to grow at a 6.55% CAGR from 2026 to 2031 as pharmaceutical blister bundles, boxed cosmetics and electronics seek lower sealing temperatures that protect heat-sensitive contents. Expanded capacity in Asia and North America narrows the price delta, encouraging switchovers that stretch the polyolefin shrink film market beyond traditional displays.

By Material Type: Polypropylene accelerates premium adoption

Polyethylene maintained a commanding 56.40% stake within the polyolefin shrink film market size in 2025, driven by transparency and cost competitiveness. Multi-layer PE blends permit tight seals even at low oven dwell times, making them a staple in beverage can dernests and produce trays. Processors now incorporate PCR streams to comply with brand circularity pledges without diluting optical properties.

Polypropylene is expected to rise 6.92% annually to 2031, buoyed by higher stiffness, chemical inertness and elevated heat-deflection points desirable for retorted foods and medical kits. New five-layer co-extruders co-blend PP with elastomer tie layers, retaining gloss while boosting tear resistance. This premium mix separates converters from commoditised PE offerings within the polyolefin shrink film market.

By Layer Structure: Multilayer engineering multiplies functionality

Multilayer architectures captured 51.40% of the polyolefin shrink film market size in 2025, supported by 6.62% CAGR prospects through 2031. Tailored barrier layers block oxygen or moisture, while surface skins dial in sealability and high-definition ink anchorage. Brands use proprietary barrier cocktails to extend ambient shelf life for sauces and dairy sticks without secondary cartons.

Monolayer films remain cost-efficient for low-risk parcels but struggle when cross-border shipping demands superior toughness. Advances in co-extrusion allow seven-layer films that still qualify for mechanical recycling streams when kept within the polyolefin family, as demonstrated by Woolworths’ recyclable beverage sleeves. This balance positions multilayer solutions as the go-to choice for next-generation compliance within the polyolefin shrink film market.

By Application: Pharmaceuticals take growth spotlight

Food and beverage preserved 41.30% share of the polyolefin shrink film market size in 2025 by wrapping multipacks, fresh produce punnets and shelf-ready trays. Processors continually down-gauge gauge to cut resin usage while adding anti-fog additives that maintain see-through appeal. Regulatory bans on PVC cling in Europe accelerate substitution toward cleaner-burning polyolefin grades.

Pharmaceutical use will surge at an 8.47% CAGR as blister cards, injectable vials and diagnostic kits mandate tamper evidence and readability of barcodes through clear film. COVID-19 vaccine rollout elevated packaging scrutiny, cementing polyolefin as the secure yet transparent enclosure for unit doses. Brand owners also exploit the expansive printable area to communicate authentication holograms, adding intangible value in the polyolefin shrink film market.

Geography Analysis

Asia Pacific dominated the polyolefin shrink film market with 37.60% revenue contribution in 2025, and its projected 6.82% CAGR remains the fastest globally. China’s entrenched extruder base partners with multinational FMCG packers, while India’s rigid packaging boom responds to urban retail growth. Regional converters foster in-house plateless digital presses, enabling swift private-label promotion campaigns that capture domestic e-commerce surges.

Japan and South Korea focus on high-barrier multilayer technology, supplying niche cross-linked rolls for export pharmaceuticals; domestic demand leans on automation-ready thin gauges that fit compact factory footprints. Association grants channel R&D tax credits toward energy-efficient shrink ovens, reinforcing adoption inside the polyolefin shrink film market.

North America constitutes a mature yet innovation-led arena powered by the United States’ omnichannel retail ecosystem. Canada and Mexico complement regional supply through proximity to resin production and tariff-favoured trade corridors, anchoring resilience against price swings.

Europe balances stringent regulatory oversight with high purchasing power. Circular economy directives push converters to certify recyclability and shift toward PCR blends by 2027. Germany, Italy and the United Kingdom represent core demand clusters owing to strong beverage, confectionery and pharmaceutical output. Southern and Eastern member states gradually catch up as retail chains harmonise packaging briefs across the bloc.

South America and the Middle East & Africa present smaller but increasingly attractive frontiers. Brazil leverages a robust petrochemical base to serve Mercosur neighbours, while Saudi Arabia’s Vision 2030 encourages downstream polymer investments that extend the reach of the polyolefin shrink film market into Gulf Cooperation Council markets.

Competitive Landscape

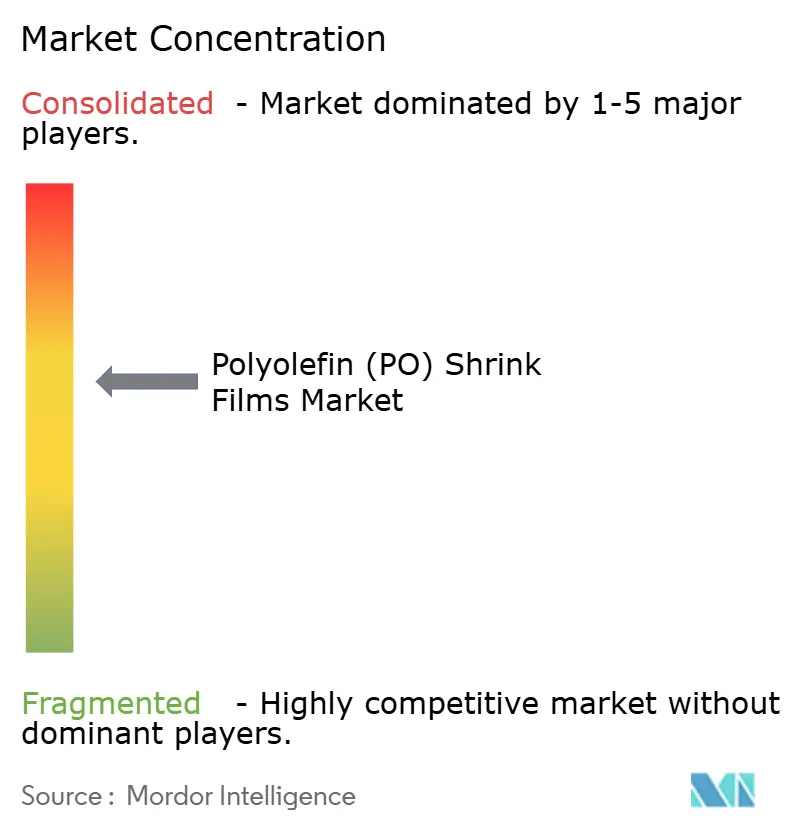

The polyolefin shrink film market is moderately consolidated, with the top five players holding less than 50% market share. Key players like Berry Global, Sealed Air, and Klockner Pentaplast integrate extrusion and in-house printing to offer turnkey solutions, emphasizing sustainability through initiatives like Berry's closed-loop pilot. Intertape Polymer Group focuses on PCR content and service networks, while UFlex expands CPP and biaxially oriented polyolefin capacity. Asian competitors leverage local resin but face certification challenges. Strategic alliances in recycled feedstock, co-extrusion, and digital printing are growing. Converters secure resin supplies to manage volatility, and OEMs innovate oven designs for thinner gauges. Success increasingly depends on balancing cost efficiency with sustainability credentials.

Polyolefin (PO) Shrink Films Industry Leaders

-

Berry Global Inc.

-

Sigma Plastics Group

-

SABIC

-

Bollore Group

-

IPG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Innovia Films has expanded its floatable polyolefin shrink range by introducing a 45 µm grade to improve material efficiency and a high-shrink variant tailored for contoured bottles. This development is expected to enhance product versatility and drive growth in the polyolefin shrink film market.

- February 2024: Intertape Polymer Group (IPG) introduced ExlfilmPlus PCR, featuring 35% recycled content for e-commerce wraps. This innovation is expected to drive sustainability trends and influence the polyolefin shrink film market by increasing the adoption of eco-friendly packaging solutions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the polyolefin shrink film market as the worldwide sales value of new, industrially produced polyethylene and polypropylene-based shrinkable over-wraps supplied on rolls or pre-formed bags that contract under heat to secure or bundle consumer and industrial goods.

Films developed primarily for stretch wrapping, PVC shrink sleeves, barrier liners, and collation stretch hoods lie outside this scope.

Segmentation Overview

-

By Type

- General Shrink Film

- Cross-Linked Shrink Film

-

By Material Type

- Polyethylene (PE)

- Polypropylene (PP)

-

By Layer Structure

- Monolayer

- Multilayer

-

By Application

- Food & Beverage

- Industrial Packaging

- Personal Care & Cosmetics

- Pharmaceutical

- Printing & Stationery

- Other Applications

-

By Geography

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We conduct structured interviews with film converters, resin suppliers, shrink-tunnel OEMs, and packaging line integrators across Asia, Europe, North America, and Latin America. These conversations validate average sold widths, regional gauge mix, pricing spreads, and service life assumptions, filling gaps left by desk research and anchoring key model coefficients.

Desk Research

Our analysts first map the demand pool using freely accessible macro and trade datasets such as UN Comtrade resin export codes, U.S. Census shrink-film import tariffs, Eurostat polymer converter statistics, and national packaging association shipment surveys. Regulatory portals (for instance, the EU Single-Use Plastics Directive repository) and patent analytics from Questel help flag technology shifts that shape film gauges and resin blends. Company 10-Ks, investor decks, and quarterly calls provide real-world price bands and capacity additions. The sources cited illustrate, rather than exhaust, the wider set of references consulted throughout the study.

Market-Sizing & Forecasting

Our model begins with a top-down reconstruction of film demand, translating resin production and cross-border trade into shrink-grade supply volumes, which are then adjusted for converter yields and average selling prices. Results are cross-checked against bottom-up approximations drawn from sampled converter revenues and distributor channel checks before final reconciliation. Critical variables include e-commerce parcel growth, retail multipack penetration, resin price indices, downgauging trends, shrink-oven installation counts, and regional bans on PVC over-wrap. Forecasts employ multivariate regression, where each driver is projected through consensus industry outlooks collected during primary work. Scenario analysis is used when policy outcomes remain uncertain.

Data Validation & Update Cycle

Prior to sign-off, separate analyst pairs rerun the model, compare outputs with independent packaging production benchmarks, and investigate anomalies exceeding preset variance bands. The report is refreshed every twelve months, with interim updates triggered by feedstock price shocks, major capacity additions, or game-changing legislation, ensuring clients always receive a current baseline.

Why Mordor's Polyolefin (PO) Shrink Films Baseline Commands Reliability

Published market estimates seldom align because each provider selects unique scope limits, price points, and refresh cadences.

By restricting coverage to heat-shrinkable PE and PP films, applying live currency conversions, and revisiting inputs annually, Mordor delivers a balanced midpoint that decision-makers can trace to clearly documented variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.16 B (2025) | Mordor Intelligence | - |

| USD 9.20 B (2025) | Regional Consultancy A | Counts non-shrink specialty sleeves and applies uniform 3 % growth without primary validation |

| USD 1.08 B (2023) | Global Consultancy B | Limits thickness to <=25 um and omits informal Asia converter sales; outdated base year |

| USD 6.10 B (2023) | Industry Association C | Uses resin shipment proxy and fixed 2022 exchange rates, introducing conversion bias |

Taken together, the comparison reveals that divergences mainly stem from scope creep, dated baselines, or single-source proxies. By grounding our figures in verified multi-source data and recurring expert feedback, Mordor's baseline stands as the most transparent and repeatable starting point for strategic planning.

Key Questions Answered in the Report

What is driving the fastest growth segment in the polyolefin shrink film market?

The pharmaceutical segment leads with an 8.47% CAGR to 2031 as stricter tamper-evidence rules and demand for barcode visibility boost adoption of high-clarity, security-grade films.

Which region offers the highest expansion opportunity?

Asia Pacific accounted 37.60% share in 2025, and will leads with a 6.82% CAGR from 2026-2031, powered by e-commerce, industrialization and capacity additions in China and India.

How are converters addressing sustainability pressures?

Leading firms integrate PCR resin, develop recyclable mono-material multilayers and partner with retailers on store-drop-off schemes to align with EU waste-reduction targets.

Why are cross-linked polyolefin films gaining popularity?

They deliver puncture resistance and allow faster, lower-temperature sealing, which cuts energy use and supports high-speed automation lines in industries such as electronics and pharmaceuticals.

What impact do European plastic taxes have on film demand?

Levies on single-use over-wrap accelerate the shift from PVC to recyclable polyolefin grades and push converters to certify films that exceed 30% recycled content thresholds.

How are resin price fluctuations mitigated?

Producers diversify feedstock sources, negotiate shorter contracts and redesign formulations to use less virgin material, buffering the -0.8% CAGR impact attributed to volatility.

What is the current market size of polyolefin shrink films market?

The Polyolefin Shrink Films Market size is estimated at USD 8.55 billion in 2026, and is expected to reach USD 10.8 billion by 2031, at a CAGR of 4.79% during the forecast period (2026-2031).

Page last updated on: