Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

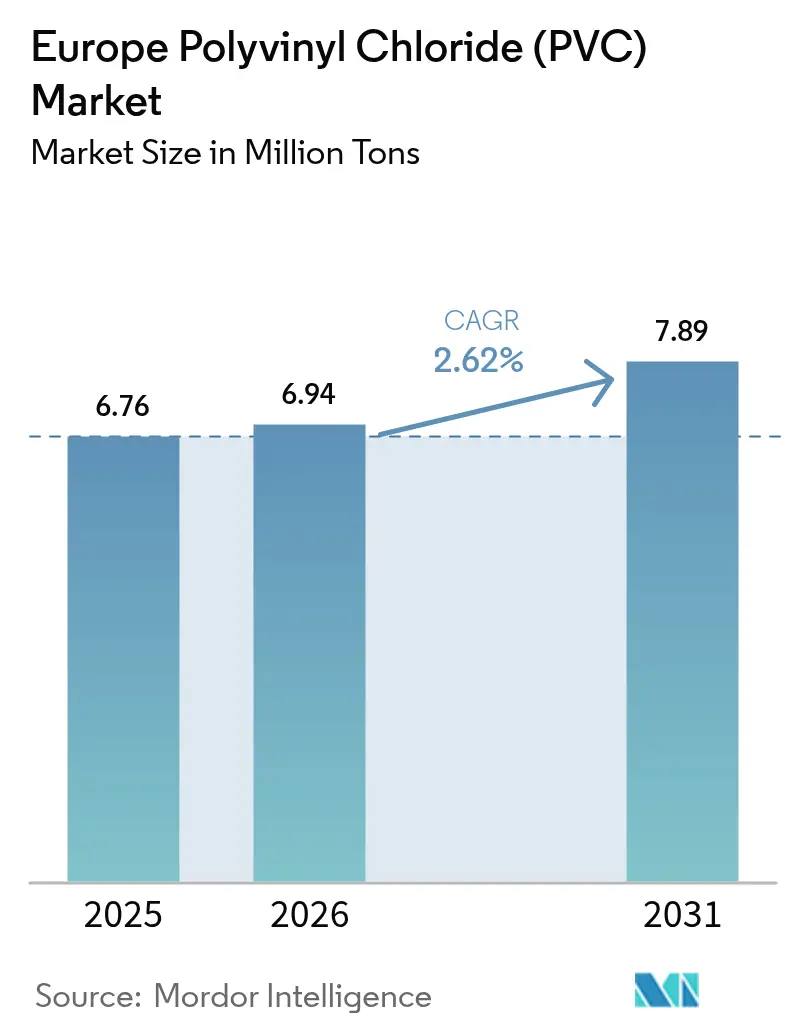

| Base Year Market Size (2025) | 6.76 Million tons |

| Market Volume (2026) | 6.94 Million tons |

| Market Volume (2031) | 7.89 Million tons |

| Growth Rate (2026 - 2031) | 2.62% CAGR |

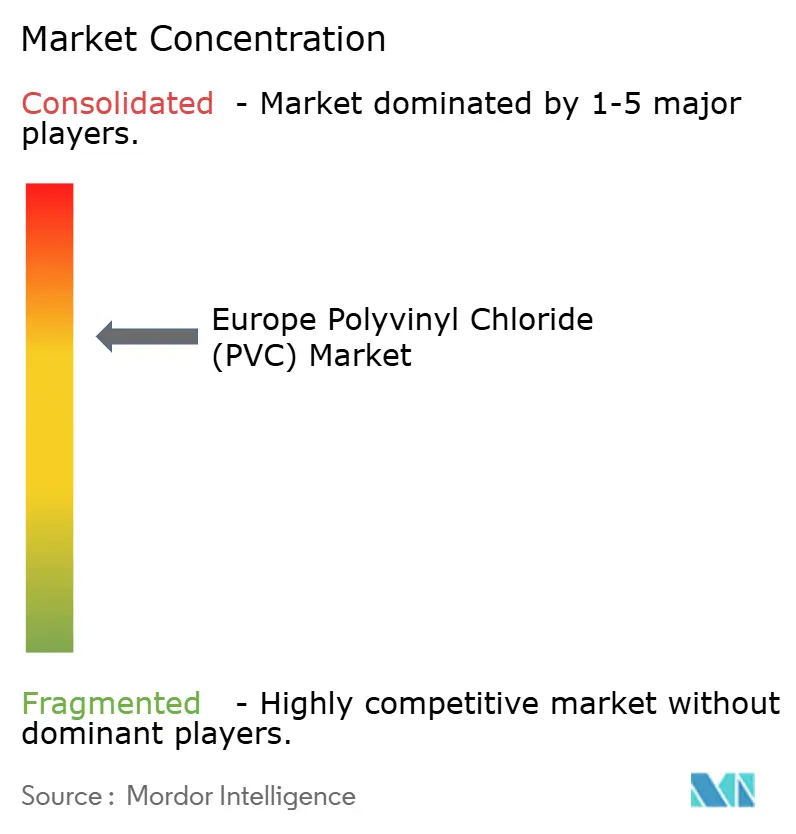

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Polyvinyl Chloride (PVC) Market Analysis by Mordor Intelligence

The Europe Polyvinyl Chloride Market size was valued at 6.76 million tons in 2025 and is estimated to grow from 6.94 million tons in 2026 to reach 7.89 million tons by 2031, at a CAGR of 2.62% during the forecast period (2026-2031). In the Europe Polyvinyl Chloride (PVC) market, steady structural growth is supported by the compliance-driven demands, such as water infrastructure upgrades and circular procurement mandates. These factors are creating premium niches. However, producers face challenges, as high energy costs and pressures from Asian imports are squeezing margins. This strain was evident with the December 2025 insolvency of Vynova’s Wilhelmshaven and Runcorn complexes. While construction commands a dominant share of demand and anchors overall volume, it also increases cyclical risks. The market's shift toward higher-specification, regulation-compliant segments is highlighted by the rapid growth of low-smoke cable compounds and calcium-zinc stabilized grades, where margin recovery is more feasible. Germany stands out as the primary consumption hub, but Turkey is experiencing the fastest growth, albeit with significant pricing fluctuations due to an influx of low-cost imports.

Key Report Takeaways

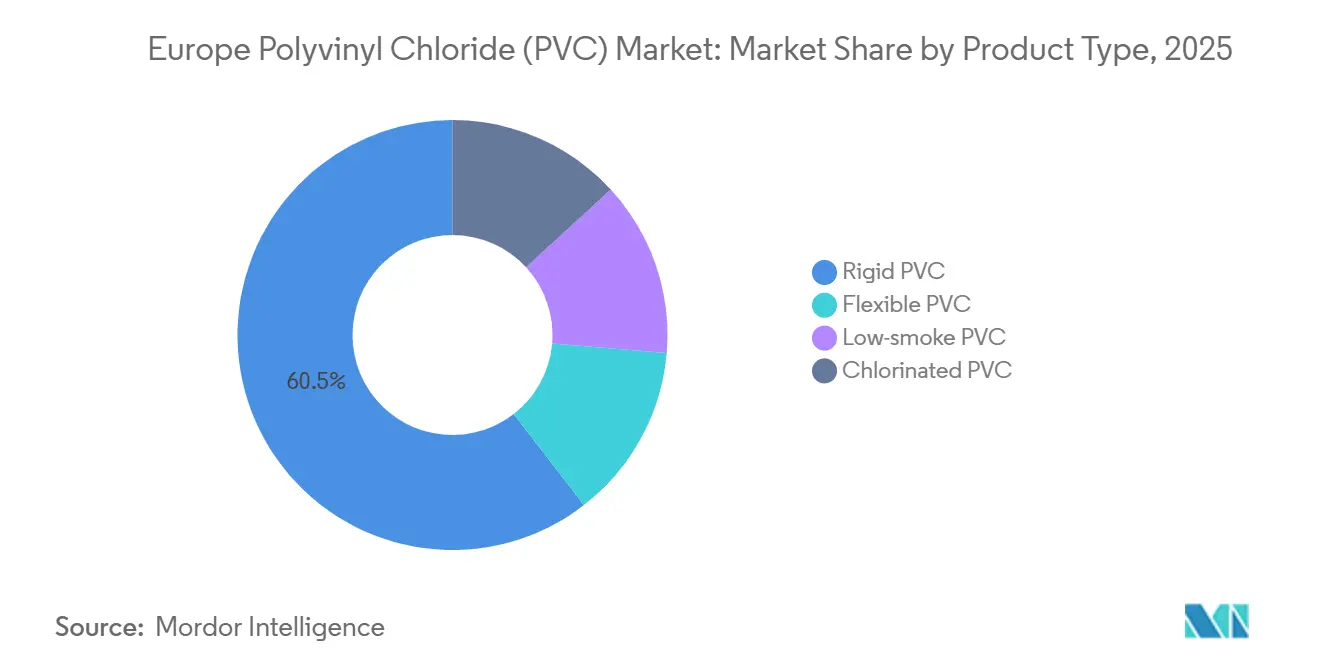

- By product type, rigid PVC led with 60.48% of the Europe Polyvinyl Chloride (PVC) market share in 2025, whereas low-smoke PVC is forecast to expand at a 3.88% CAGR through 2031.

- By stabilizer chemistry, calcium-zinc systems accounted for 43.12% share of the Europe Polyvinyl Chloride (PVC) market size in 2025 and are advancing at a 3.49% CAGR to 2031.

- By application, pipes and fittings held 49.24% of the 2025 volume, while wires and cables record the highest projected CAGR at 3.61% through 2031.

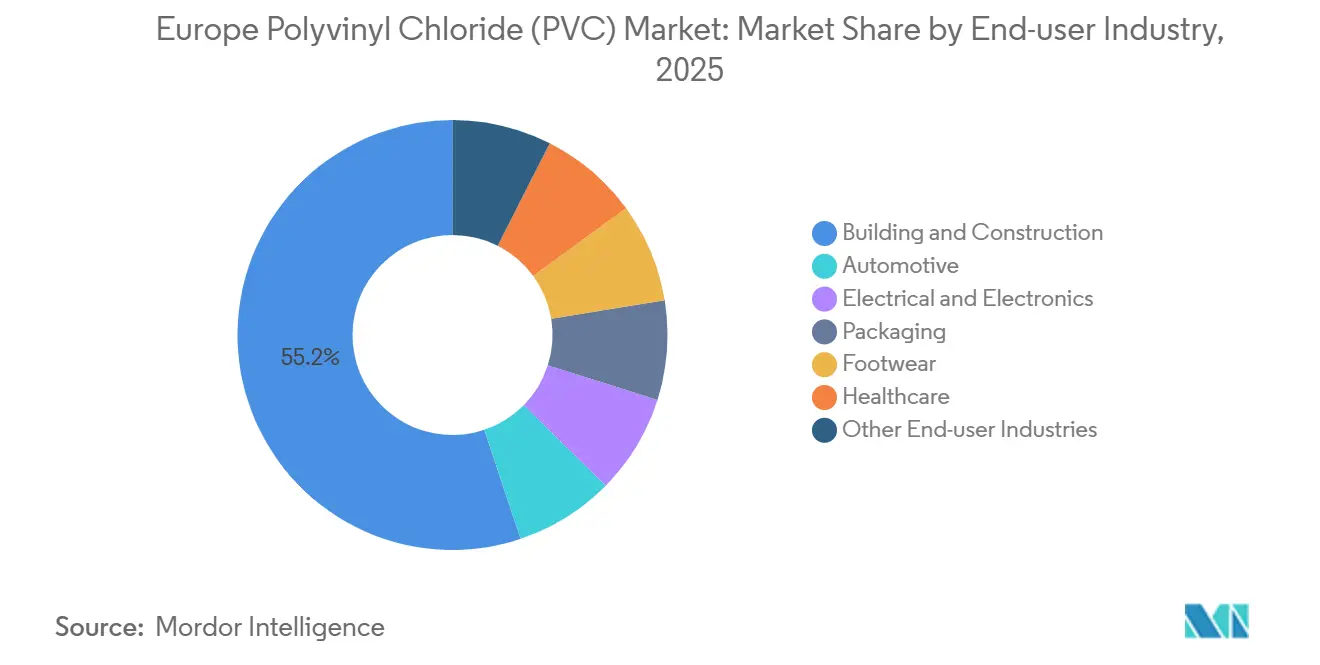

- By End-user Industry, building and construction accounted for a 55.15% share of market size in 2025, whereas electrical and electronics is forecast to expand at a 3.92% CAGR through 2031.

- By geography, Germany led with 21.13% of the 2025 volume; Turkey is projected to grow at 3.33% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Polyvinyl Chloride (PVC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting initiatives | +0.50% | Germany, France, Spain, Italy | Medium term (2-4 years) |

| EU water-infrastructure upgrade funding | +0.70% | Spain, Italy, France, Germany | Medium term (2-4 years) |

| Surge in offshore-wind HV-cable demand | +0.40% | Germany, UK, France, Netherlands | Long term (≥ 4 years) |

| Hydrogen backbone needs PVC-lined pipe | +0.30% | Germany, Netherlands, Belgium | Long term (≥ 4 years) |

| VinylPlus circular-procurement mandates | +0.60% | Germany, France, UK, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automotive Lightweighting Initiatives

European automakers are increasingly incorporating polyvinyl chloride (PVC) in vehicles, particularly in interior trims, door panels, and under-body coatings, due to the polymer's lower density compared to engineering plastics. The push for electrification has driven demand for flame-retardant cable insulation, as weight reductions contribute to extended driving ranges. Additionally, closed-loop compounds that include a certified recyclate are gaining popularity. In recent years, Benvic expanded its recyclate capacity at its Porcieu-Amblagnieu facility. This strategic move positions Benvic to meet Tier-1 procurement programs that mandate a minimum recycled content. Consequently, original equipment manufacturer (OEM) mandates across Germany, France, Spain, and Italy are driving growth in the Europe Polyvinyl Chloride (PVC) market.

EU Water-Infrastructure Upgrade Funding

The EU Recovery and Resilience Facility has allocated funds for the renewal of water networks, with Spain and Italy collectively securing a significant portion[1]European Commission, “Recovery and Resilience Facility,” europa.eu . Outdated asbestos-cement and ductile-iron pipes, which are prone to leaks, are being replaced with PVC lines. These new lines have a service life of 50 years and are resistant to corrosion. Procurement activities are heavily concentrated in 2024-2026, driving up the demand for rigid pipes and contributing to the projected growth. Contractors are increasingly selecting PVC-O and PVC-U for pressure mains, a trend that is significantly boosting the Europe polyvinyl chloride (PVC) market.

Hydrogen Backbone Needs PVC-Lined Pipe

In Europe, a proposed hydrogen network, stretching across thousands of kilometers, is championing the use of PVC-lined steel for its low-pressure distribution. Trials in Germany's Salzgitter cluster have validated the material's impermeability and its resistance to embrittlement. Although the volumes are still modest, this premium specification enhances profit margins and fuels the expansion of Europe Polyvinyl Chloride (PVC) market.

VinylPlus Circular-Procurement Mandates

VinylPlus recycled 724,638 tons of PVC in 2024 and aims to achieve 1 million tons per year by 2030[2]VinylPlus, “Sustainability Report 2024,” vinylplus.eu . Public tenders in Germany, France, and the United Kingdom now mandate recycled-content thresholds ranging from 25% to 75%, significantly redirecting demand toward certified recyclate. ISCC PLUS accreditation, secured by KEM ONE in 2025, allows for mass-balance claims that attract procurement premiums, collectively contributing an additional 0.6 percentage points to market growth during the forecast period of 2026-2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retailer bans on PVC food packaging | -0.40% | EU-wide (early in Germany, France, Netherlands) | Short term (≤ 2 years) |

| Tightening REACH limits on legacy stabilizers | -0.30% | EU27 (uniform), UK derogations | Medium term (2-4 years) |

| Anti-dumping duty volatility on imports | -0.20% | Germany, Italy, France, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Retailer Bans on PVC Food Packaging

By 2027, major supermarket chains plan to phase out PVC from their private-label food packaging. This initiative is expected to impact the demand for flexible films, leading to a significant reduction. Additionally, with the imposition of limits on BPA and PFAS, the policy is projected to decelerate the growth rate of the Polyvinyl Chloride (PVC) market in Europe. This decline is attributed to the increasing adoption of polyethylene and PLA substitutes on retail shelves.

Tightening REACH Limits on Legacy Stabilizers

Effective November 2024, a new lead cap is complicating the mechanical recycling of old window frames, many of which still contain lead additives. The need for costly sorting and the removal of these additives reduces recycler profits. This reduction has negatively impacted the forecasted growth for the 2026-2031 period and has reinforced the compliance premium for clean recyclate in Europe Polyvinyl Chloride (PVC) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rigid Dominance, Low-Smoke Acceleration

Rigid PVC accounted for 60.48% of the Europe Polyvinyl Chloride (PVC) market in 2025. This dominance was driven by the use of pipes, fittings, and window profiles, which benefit from the polymer's long-term durability. Low-smoke PVC is growing at a CAGR of 3.88% through the forecast period of 2026-2031. Demand for rigid PVC has remained strong in Germany, where PVC-U windows hold a significant market share, and in southern Europe, where an ongoing pipe-replacement initiative is underway. Although low-smoke formulations represented a smaller portion of the market in 2025, they have been growing rapidly due to fire-safety stipulations outlined in recent regulations. Consequently, the market size for low-smoke products in the European PVC sector is expected to expand further during the forecast period of 2026-2031. As building-safety regulations have tightened, cable manufacturers have been transitioning from traditional compounds to premium low-chloride, low-acidic-gas grades. This shift, while enhancing safety, incurs higher costs compared to standard flexible PVC. Producers capable of certifying both smoke performance and recycled content have been capturing a larger market share. In contrast, commodity rigid suppliers have faced challenges, struggling with slim margins as they compete with Asian imports, which are priced lower than domestic offerings.

By Stabilizer Type: Calcium-Zinc Ascendancy

Calcium-zinc systems owned 43.12% of the 2025 volume and are growing at a 3.49% CAGR through the forecast period of 2026-2031, driven by the complete phase-out of lead stabilizers and a shift away from costlier tin chemistries. While tin and organotin packages remain pivotal for crystal-clear grades, they are under scrutiny for reproductive toxicity by the ECHA. As a result, the share of tin systems in Europe's Polyvinyl Chloride (PVC) market is projected to decline, with calcium-zinc systems moving closer to dominating stabilized resin during the forecast period of 2026-2031.

Economic factors support these regulatory shifts: calcium-zinc provides comparable heat stability at a lower cost than organotin counterparts. Producers who craft stabilizers in-house enjoy a margin boost, but toll compounders dependent on external additives face steeper compliance costs. The REACH restriction on lead in recycled PVC, implemented in November 2024, has spurred investments in X-ray fluorescence sorting and selective dissolution technologies, giving a competitive edge to vertically integrated recyclers.

By Application: Pipes Anchor, Cables Accelerate

Pipes and fittings absorbed 49.24% of total volume in 2025, buoyed by an EU-funded water-network renewal, set to peak in 2026-2027. Wires and cables are projected to deliver a 3.61% CAGR through 2026-2031, driven by the roll-outs in offshore wind, data centers, and EV charging. Consequently, compounding houses supplying Bca-rated LSA formulations are witnessing strong revenue growth, even with moderate tonnage.

As retailer bans gain momentum, the use of flexible films in food packaging is declining, with the film's market share expected to decrease further by 2031. Similarly, demand for medical tubing and blood bags is shifting. This change is largely due to the impending July 2030 DEHP sunset, leading hospitals to trial TPE and PP alternatives.

By End-User Industry: Construction Anchors, Electronics Accelerates

Building and construction consumed 55.15% of the 2025 volume, solidifying its role as the cornerstone of the European Polyvinyl Chloride (PVC) market. While recycling targets and Germany's established window-profile collection network bolster the sustainability narrative, they do not entirely insulate volumes from fluctuations tied to housing cycles. Electrical and electronics grow fastest at a 3.92% CAGR during the forecast period of 2026-2031, driven by the stringent specifications for fire-safe insulation in offshore wind cabling.

Automotive applications contribute to steady, albeit modest, growth, spurred by the rising demand for lightweight interior components. Meanwhile, the packaging sector contracts due to retailer-imposed bans, and the healthcare industry is gradually but decisively moving away from plasticized PVC. As a result, the market is increasingly leaning toward segments where compliance and performance are paramount, leading to a bifurcated European PVC landscape.

Geography Analysis

Germany accounted for 21.13% of the total 2025 volume, buoyed by a commanding share in PVC-U windows and an impressive recycling rate for post-consumer profiles. Despite facing pressures on producer margins from soaring electricity costs, Germany's PVC market is set to grow steadily over the forecast period of 2026-2031. France, riding the wave of significant spending on pipe replacements and a strong profile-recycling ecosystem, secures the second spot. Meanwhile, the United Kingdom grapples with the complexities of adhering to both the European Union's REACH and separate DEFRA duties, complicating matters for converters operating across the Channel.

In 2023, Italy emerged as Europe's top PVC importer. Competitive tenders and a robust supply from Asia drove down average prices in 2024. While local extruders remain busy due to water infrastructure funding, ongoing price undercutting has stymied any significant margin recovery. Spain, echoing Italy's infrastructure initiatives, has allocated substantial funding for leak-reduction programs favoring PVC-O pipes. However, it is worth noting that new construction projects lag behind pre-pandemic figures.

Turkey delivers the highest forecast CAGR at 3.33% during the 2026-2031 period. In the first ten months of 2025, imports surged significantly, even as Petkim operated at roughly half its capacity. Yet spot prices dropped to levels reminiscent of the pandemic. The nation has positioned itself as a pivotal outlet for surplus cargoes from the United States and Asia, a move that injects volatility into the broader European PVC market.

In the rest of Europe, spanning Central and Eastern Europe, Scandinavia, and the Balkans, construction lags and high energy tariffs have kept operating rates below optimal levels. Without trade protections to bridge the cost gap with importers, further rationalization among non-integrated producers seems likely.

Competitive Landscape

The Europe Polyvinyl Chloride (PVC) market is moderately consolidated. INEOS, Westlake, and KEM ONE, collectively held a notable share of effective capacity in 2025. Rationalization accelerated when INEOS Inovyn shut two lines in July 2024, and Vynova filed for insolvency in December 2025. However, aggregate operating rates remained at approximately 65 percent, reflecting weak demand rather than tight supply.

Cost-focused producers have responded by filing anti-dumping petitions; INEOS alone has multiple chemical cases pending. Differentiation-focused companies are pursuing bio-attributed and recycled-content strategies. For instance, KEM ONE launched ISCC PLUS-certified mass-balance PVC in 2025, and Benvic obtained OCS Europe certification while doubling its recyclate capacity. Meanwhile, suppliers from the Asia-Pacific region, including Shin-Etsu, LG Chem, and Formosa Plastics, are expanding their capacities in the United States and Asia-Pacific regions. These expansions are strategically targeting the Europe Polyvinyl Chloride (PVC) market, leveraging feedstock-cost advantages.

Investments in technology are focusing on X-ray fluorescence sorters for lead-contaminated recyclates and acid-scavenger additive packages. These innovations ensure compliance with EN 50399 smoke thresholds without compromising flame retardancy. As a result, the market's competitive landscape is divided between commodity resins priced on Asian parity and specialty grades priced based on compliance value.

Europe Polyvinyl Chloride (PVC) Industry Leaders

INEOS

KEM ONE

Shin-Etsu Chemical Co. Ltd.

Vynova Group

Westlake Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Vynova, a European company, has announced the launch of a research and development program aimed at advancing PVC recycling. This initiative seeks to drive the PVC value chain toward greater circularity. Vynova focuses on innovating technologies to remove heavy metals from post-consumer PVC waste.

- December 2024: Kem One and Olin have entered into a manufacturing agreement to enhance their positions in the global market. Olin will leverage its expertise in EDC production and its extensive commercial network, while Kem One will apply its industrial proficiency to convert EDC into PVC.

Europe Polyvinyl Chloride (PVC) Market Report Scope

Polyvinyl chloride (PVC) is a high-strength thermoplastic material widely used in applications such as pipes, medical devices, and wire and cable insulation. It is the world's third-largest thermoplastic material in terms of usage.

The Europe Polyvinyl Chloride (PVC) market is segmented by product type, stabilizer type, application, end-user industry, and geography. By product type, the market is segmented into rigid PVC, flexible PVC, low-smoke PVC, and chlorinated PVC. By stabilizer type, the market is segmented into calcium-based, lead-based, tin and organotin-based, barium-based and others. By application, the market is segmented into pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses and tubings, and other applications. By end-user industry, the market is segmented into building and construction, automotive, electrical and electronics, packaging, footwear, healthcare, and other end-user industries. The report also covers the market size and forecasts for the polyvinyl chloride in 6 countries across major European region. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

By Product Type

| Rigid PVC | Clear Rigid PVC |

| Non-clear Rigid PVC | |

| Flexible PVC | Clear Flexible PVC |

| Non-clear Flexible PVC | |

| Low-smoke PVC | |

| Chlorinated PVC |

By Stabilizer Type

| Calcium-based (Ca-Zn) |

| Lead-based (Pb) |

| Tin and Organotin-based (Sn) |

| Barium-based and Others (Liquid Mixed Metals) |

By Application

| Pipes and Fittings |

| Films and Sheets |

| Wires and Cables |

| Bottles |

| Profiles, Hoses and Tubings |

| Other Applications |

By End-user Industry

| Building and Construction |

| Automotive |

| Electrical and Electronics |

| Packaging |

| Footwear |

| Healthcare |

| Other End-user Industries |

By Geography

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Turkey |

| Rest of Europe |

| By Product Type | Rigid PVC | Clear Rigid PVC |

| Non-clear Rigid PVC | ||

| Flexible PVC | Clear Flexible PVC | |

| Non-clear Flexible PVC | ||

| Low-smoke PVC | ||

| Chlorinated PVC | ||

| By Stabilizer Type | Calcium-based (Ca-Zn) | |

| Lead-based (Pb) | ||

| Tin and Organotin-based (Sn) | ||

| Barium-based and Others (Liquid Mixed Metals) | ||

| By Application | Pipes and Fittings | |

| Films and Sheets | ||

| Wires and Cables | ||

| Bottles | ||

| Profiles, Hoses and Tubings | ||

| Other Applications | ||

| By End-user Industry | Building and Construction | |

| Automotive | ||

| Electrical and Electronics | ||

| Packaging | ||

| Footwear | ||

| Healthcare | ||

| Other End-user Industries | ||

| By Geography | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Turkey | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected volume of the Europe Polyvinyl Chloride (PVC) market in 2031?

The Europe polyvinyl chloride (PVC) market size stands at 6.94 million tons in 2026, and it is projected to reach 7.89 million tons by 2031 at a 2.62% CAGR.

Which segment is growing fastest in European PVC applications?

Low-smoke cable compounds are expected to register a 3.88% CAGR through 2031, the highest among product segments.

Why did Vynova file for insolvency in 2025?

Persistently high energy costs and low-priced Asian imports squeezed margins, making operations at Wilhelmshaven and Runcorn unsustainable.

Which stabilizer chemistry dominates European PVC today?

Calcium-zinc systems hold 43.12% market share and are still expanding as lead and tin alternatives are phased out.

What role does recycled content play in procurement decisions?

Public tenders increasingly mandate 25-75% recycled PVC, pushing producers with certified recyclate to the front of the supplier queue.

Page last updated on: