Polyimide Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

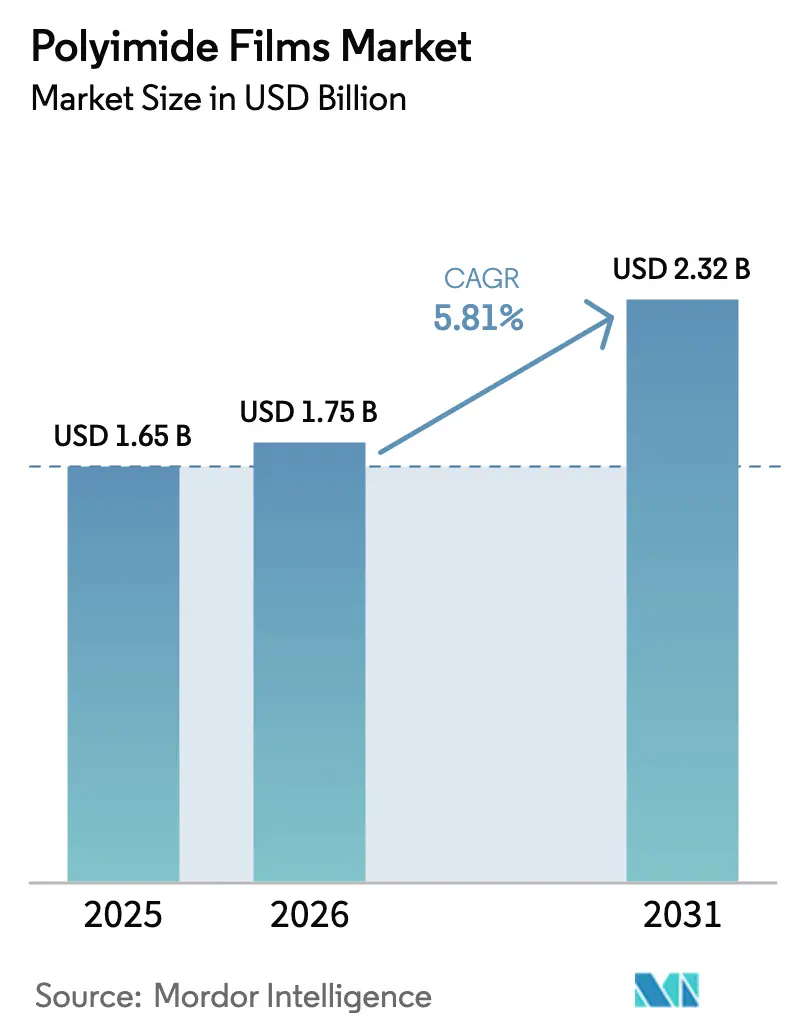

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

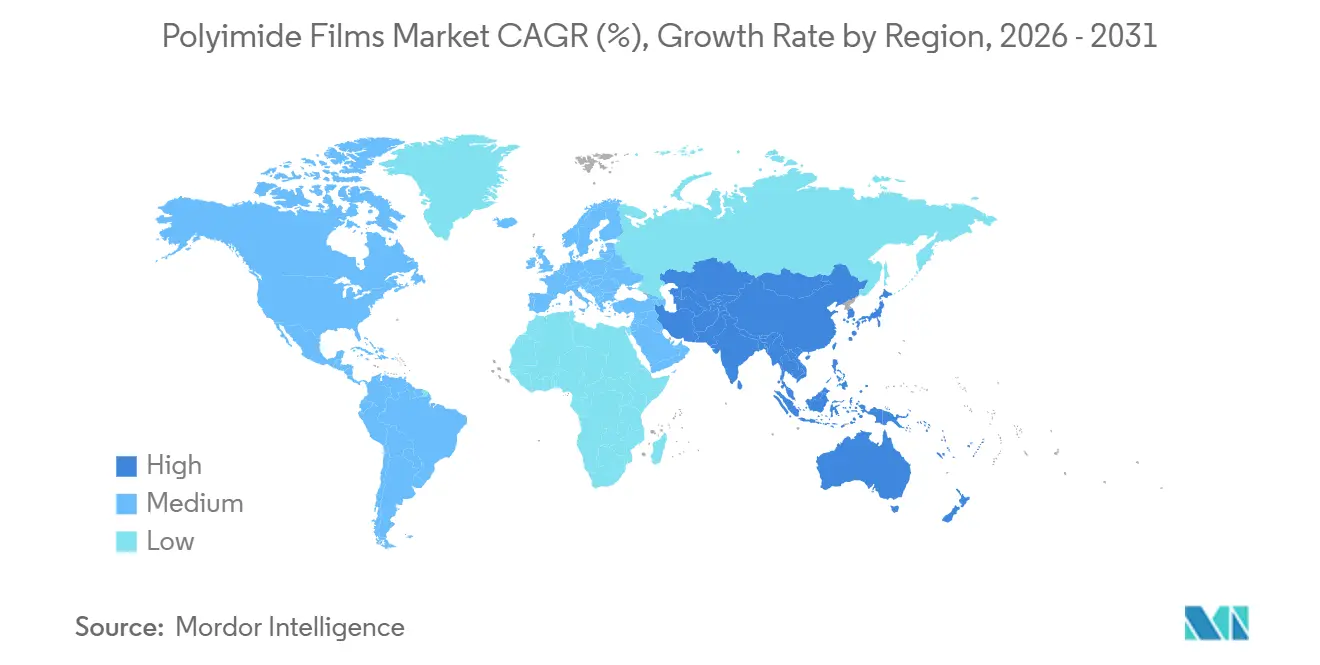

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

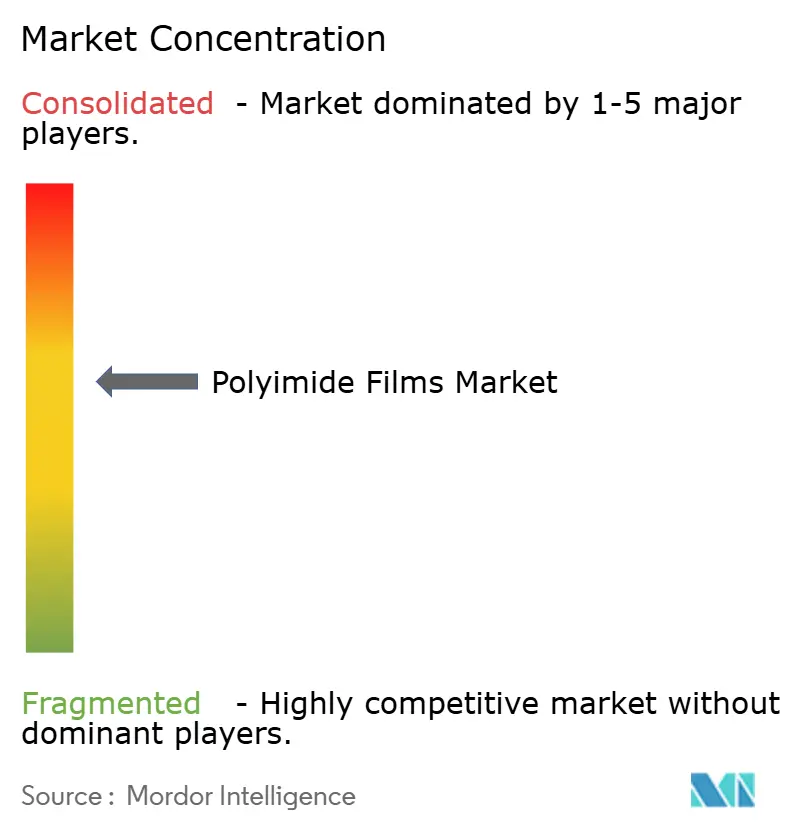

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyimide Films Market Analysis by Mordor Intelligence

The Polyimide Films Market size is projected to expand from USD 1.65 billion in 2025 and USD 1.75 billion in 2026 to USD 2.32 billion by 2031, registering a CAGR of 5.81% between 2026 to 2031. Growing investment in electric-vehicle battery enclosures, satellite thermal blankets, and advanced semiconductor packaging is shifting revenue toward specialty grades that command price premiums over commodity insulation films. Electronics miniaturization is shrinking dielectric layers in flexible printed circuits, while 5G base-station designers require low-loss substrates to handle millimeter-wave frequencies. Foldable displays are scaling commercial volumes and pushing demand for colorless grades that maintain optical clarity under mechanical stress. Concurrently, space-sector procurement emphasizes weight reduction, and automotive OEMs specify high-voltage insulation rated beyond 1,000 V, both of which reinforce structural demand for high-performance polyimides. Competitive dynamics remain moderately consolidated because a handful of suppliers control solvent-recovery infrastructure that new entrants find costly to replicate.

Key Report Takeaways

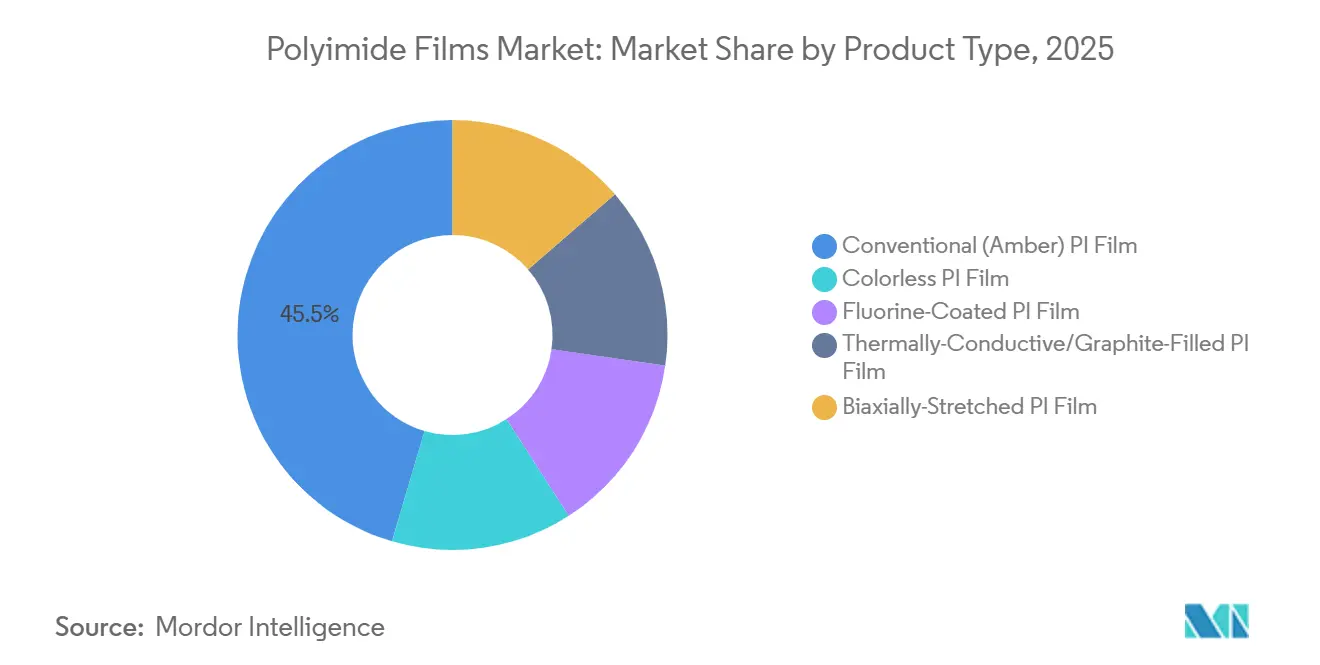

- By product type, Conventional (Amber) PI films led with 45.45% of polyimide films market share in 2025; colorless PI films are projected to expand at a 6.22% CAGR through 2031.

- By application, flexible printed circuit boards accounted for a 43.77% share of the polyimide films market size in 2025, while pressure-sensitive tapes recorded the fastest projected CAGR at 6.02% to 2031.

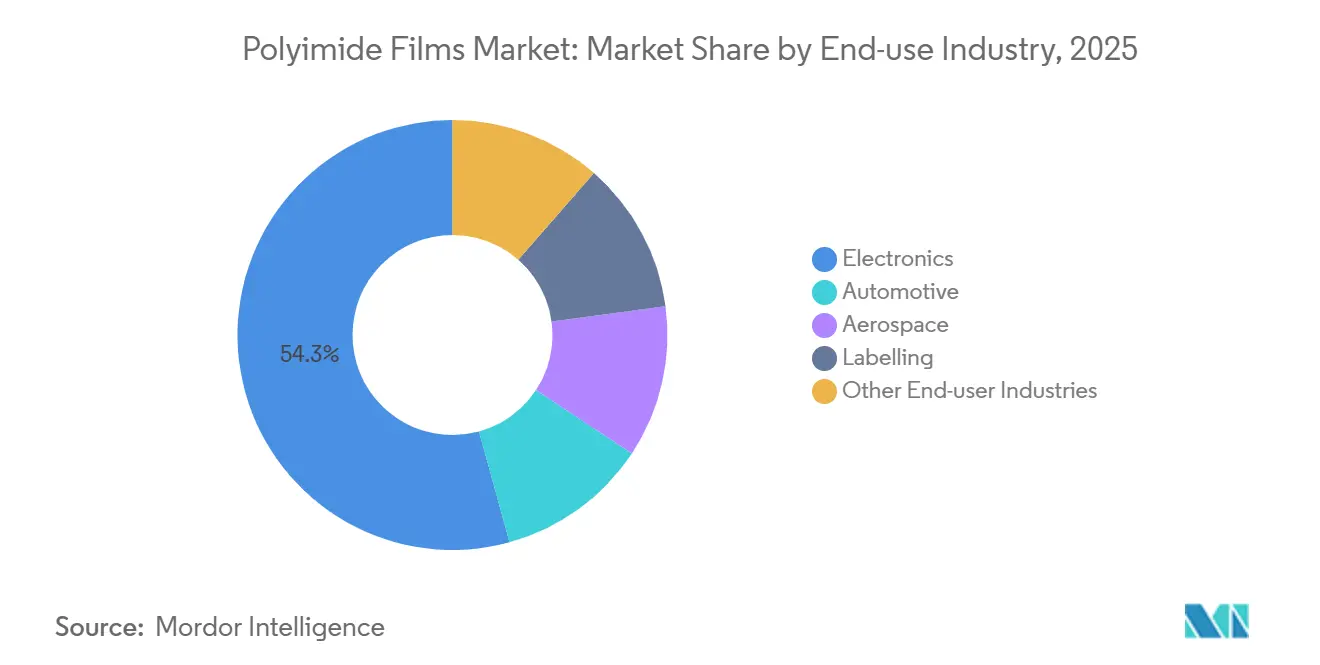

- By end-use industry, electronics commanded 54.28% share of the polyimide films market size in 2025, whereas the labelling segment is set to grow at a 6.09% CAGR to 2031.

- By geography, Asia-Pacific captured 44.91% of the polyimide films market share in 2025 and is advancing at a 6.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyimide Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronics miniaturization and flexible-display boom | +1.2% | APAC core (China, South Korea, Japan), spill-over to North America | Medium term (2-4 years) |

| EV high-voltage insulation demand surge | +1.0% | Global, with early concentration in China, Europe, North America | Medium term (2-4 years) |

| 5G/6G high-frequency PCB adoption | +0.9% | APAC manufacturing hubs, North America telecom infrastructure | Short term (≤ 2 years) |

| Space-sector lightweight thermal shielding expansion | +0.6% | North America, Europe (ESA), emerging in India (ISRO) | Long term (≥ 4 years) |

| Additive-manufactured low-k PI for chiplet packaging | +0.8% | APAC (Taiwan, South Korea foundries), North America (Intel, AMD) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electronics Miniaturization and Flexible-Display Boom

Colorless polyimide film enables foldable smartphones and rollable televisions because amber grades absorb blue wavelengths and depress OLED luminance by 8% to 12%[1]Samsung Display Newsroom, “Foldable OLED Advances,” Samsung Electronics, samsung.com. Samsung Display and LG Display migrated to colorless substrates in 2024, allowing screen radii below 1.5 mm without cracking. Kolon Industries expanded its Gumi line in 2025 to meet rising panel demand, signaling that colorless materials have shifted from niche prototypes to mass production. BOE is now qualifying the film for under-display cameras that require more than 88% light transmission. As a result, the polyimide film market is fragmenting into optically transparent and thermally robust subsegments, each demanding distinct polymer architectures.

EV High-Voltage Insulation Demand Surge

Battery architectures are moving from 400 V to 800 V platforms, pushing insulation specifications toward dielectric strengths above 200 kV /mm and continuous-use temperatures above 250°C. DuPont Kapton meets these thresholds and is already wrapped around busbars and separators in lithium-ion modules[2]DuPont, “Kapton Technical Data Sheet,” DuPont, dupont.com. Oerlikon introduced a plasma-enhanced coating in 2024 that trimmed thermal-runaway propagation by 18%, while Avery Dennison released a UL 94 V-0 compliant tape in 2025 for European automakers. Chinese battery producers are adopting graphite-filled grades to dissipate heat in cell-to-pack designs. Together, these developments draw the polyimide film market further into the EV battery value chain.

5G/6G High-Frequency PCB Adoption

Millimeter-wave base stations above 24 GHz need substrates with dielectric constants below 3.5 and loss factors under 0.005. DuPont’s Pyralux laminate posted a 0.0025 dissipation factor at 28 GHz in 2024, satisfying antenna-array designers. Telecom rollouts in India and Southeast Asia are replacing rigid FR-4 boards with flexible polyimide, shedding 30% weight from rooftop antennas. Nokia and Ericsson locked multi-year supply agreements with Asian laminators in 2025, ensuring demand continuity into early 6G trials. The polyimide film market, therefore, benefits from both the speed and density imperatives of next-generation wireless infrastructure.

Space-Sector Lightweight Thermal Shielding Expansion

Satellite operators prize polyimide blankets for their radiation resistance and low mass. NASA’s Parker Solar Probe survived 1,370°C perihelion temperatures using Kapton-based shielding. ESA specified similar films for its JUICE mission to Jupiter. SpaceX and OneWeb integrate polyimide flexible circuits in power distribution, trimming harness mass by 20%. ISRO is developing an indigenous supply for its Gaganyaan crewed mission, seeking to reduce import reliance. As launch economics hinge on kilograms delivered to orbit, the polyimide film market stands to gain sustainable aerospace pull.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile dianhydride and diamine feedstock pricing | -0.7% | Global, acute in regions dependent on Chinese intermediates | Short term (≤ 2 years) |

| VOC-emission compliance cost for solvent casting | -0.5% | Europe, North America, China (post-2025 enforcement) | Medium term (2-4 years) |

| PFAS-linked supply-chain traceability mandates | -0.3% | North America, Europe (REACH), emerging in Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Dianhydride and Diamine Feedstock Pricing

Pyromellitic dianhydride and oxydianiline prices swung 22% through 2024 as Chinese environmental inspections curtailed benzene-derivative output. Film producers exposed to 60-day contract cycles saw margins compress when raw-material spikes outpaced customer repricing. Vertically integrated suppliers such as DuPont and Toray hedge through long-term purchase agreements, but mid-tier players in Taiwan and India endured utilization dips below 70%. This volatility steers R&D toward solvent-free extrusion and aqueous dispersions, yet pilot lines have not matched the mechanical integrity of solvent-cast grades. Consequently, raw-material risk remains a drag on polyimide film market expansion.

VOC-Emission Compliance Cost for Solvent Casting

Solvent casting emits N-methyl-2-pyrrolidone and dimethylacetamide, now capped below 20 mg / m³ in many jurisdictions. Retrofitting thermal oxidizers adds USD 5 million to USD 15 million per line, discouraging capacity additions in Europe and North America. China tightened national standards in 2025, prompting domestic lines to upgrade abatement systems or suspend production during pollution alerts. Although water-based dispersions alleviate VOC exposure, tensile modulus lags by 10% to 15%. The resulting two-tier supply structure squeezes small converters and slows wider adoption, tempering the polyimide film market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Grades Drive Revenue Diversification

Conventional amber film retained 45.45% share of the polyimide film market size in 2025, buoyed by cost-sensitive motor insulation and tape backings. Colorless grades are forecast to climb at a 6.22% CAGR as display makers demand more than 88% light transmission. Fluorine-coated films appeal to aerospace hydraulics, and graphite-filled variants move into EV battery thermal interfaces where heat flux tops 5 W / m-K. Biaxially stretched grades deliver higher tear resistance, though their 15% price premium restricts uptake to automotive electronics.

Specialty formulations now draw higher margins and insulate producers from commodity price swings. Kolon, Kaneka, and Asahi Kasei are expanding colorless and photosensitive capacity, with the latter investing to double PIMEL PSPI output by 2030. These multiyear bets indicate that premium segments will anchor revenue growth within the polyimide film market.

By Application: Tape Growth Outpaces FPCB Dominance

Flexible printed circuit boards delivered 43.77% of the polyimide film market share in 2025, reflecting entrenched use in smartphones, wearables, and ADAS sensors. Pressure-sensitive tapes, however, are tracking a 6.02% CAGR as RFID tags spread across retail logistics and pharmaceutical packaging. Specialty fabricated products such as die-cut gaskets serve mature motor markets, and wire-and-cable demand grows with renewable-energy installations.

Tape suppliers introduce flame-retardant and thermally conductive variants to penetrate EV battery assembly, where manual application and reworkability are crucial. FPCB technology is migrating toward finer pitch, yet price pressure persists because smartphone OEMs benchmark costs quarterly. These offsetting dynamics keep the polyimide film industry balanced between volume from circuits and premium growth from engineered adhesive systems.

By End-use Industry: Labelling Emerges as a High-Growth Adopter

Electronics retained 54.28% of demand in 2025, encompassing smartphones, laptops, and base-station hardware. Labelling applications are projected to expand at a 6.09% CAGR through 2031 as consumer-brand owners embed NFC chips in tamper-evident flexible labels for supply-chain visibility. Automotive electrification channels polyimide into battery modules, motor slots, and sensor circuits. Aerospace depends on the material for satellite blankets and harness insulation tied to constellation launches.

The polyimide film market now sees a diversified pipeline where non-traditional users, such as luxury goods and pharmaceuticals, rely on high-temperature labels to combat counterfeiting. Automotive growth is structural, given safety requirements in high-voltage packs, while aerospace orders remain episodic but sticky once qualified. This combination broadens the total addressable market and cushions revenue cycles.

Geography Analysis

Asia-Pacific accounted for 44.91% of revenue in 2025 and is set to grow at a 6.14% CAGR through 2031, underpinned by electronics assembly, automotive production, and vertically integrated dianhydride supply in China. Japan maintains leadership in colorless and photosensitive grades, supplying Samsung Display, LG Display, and TSMC. South Korea leverages proximity to panel makers for rapid prototyping, while India’s production-linked incentive scheme spurs local FPCB demand, although film imports still dominate.

North America held a mid-teens slice of the polyimide film market. DuPont’s USD 250 million Circleville expansion in Ohio reinforces domestic supply for aerospace and defense customers who prioritize reliability over cost. The US CHIPS Act funds new packaging fabs in Arizona and New Mexico, pulling photosensitive grades into regional supply chains. Canada and Mexico absorb wire-and-cable volumes linked to wind and EV investments.

Europe contributed a high-teens share, concentrated in Germany, France, and Italy, for automotive and satellite uses. REACH emission limits curb fresh capacity, so many converters import Asian film while focusing on downstream tapes and laminates. South America and the Middle East remain nascent, but Brazil’s EV programs and Saudi Arabia’s petrochemical diversification hint at future incremental demand for the polyimide film market.

Competitive Landscape

The Polyimide Films market is moderately consolidated. PI Advanced Materials, Taimide, and Wuhan Imide compete regionally and customize niche grades, while 3M, AGC, and Saint-Gobain leverage downstream laminates and tapes to capture value beyond raw film. Innovation continues in water-based dispersions and dry-phase processing aimed at eliminating VOCs, yet mechanical parity with solvent-cast grades remains elusive. Patent filings for graphite-filled thermal interface films and low-k photosensitive formulations underscore R&D rivalry.

Polyimide Films Industry Leaders

DuPont

KANEKA CORPORATION

PI Advanced Materials Co., Ltd.

TORAY INDUSTRIES, INC.

Kolon Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: FUJIFILM Corporation unveiled ZEMATES, its latest brand of photosensitive insulating materials tailored for semiconductor back-end processes, with a primary focus on polyimide. The ZEMATES range features liquid polyimide designed for redistribution layers (RDL) and protective films.

- July 2025: Arkema, alongside its affiliate PI Advanced Materials, unveiled a new brand name for its flagship high-performance polyimide product, Zenimid. This rebranding underscores PI Advanced Materials' dedication to broadening the global footprint of its product range, targeting diverse markets including aerospace, automotive, electronics, and industrial sectors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the polyimide films market as the sale of new, fully-imidized aromatic or colorless polyimide sheets and rolls supplied for flexible printed circuits, electrical insulation, aerospace wiring, photovoltaic modules, and other high-temperature uses where continuous service above 240 °C is demanded.

Scope exclusion: Pre-laminated tapes that already include pressure-sensitive adhesive are kept out to avoid double counting downstream adhesive value.

Segmentation Overview

- By Product Type

- Conventional (Amber) PI Film

- Colorless PI Film

- Fluorine-Coated PI Film

- Thermally-Conductive/Graphite-Filled PI Film

- Biaxially-Stretched PI Film

- By Application

- Flexible Printed Circuit Boards (FPCB)

- Specialty Fabricated Products

- Pressure Sensitive Tapes

- Wire and Cable

- Motor/Generator

- By End-use Industry

- Electronics

- Automotive

- Aerospace

- Labelling

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Analysts conducted structured interviews with film makers in Japan, China, and the United States, flexible PCB fabricators in South Korea and Germany, and aerospace harness integrators in Texas. These conversations confirmed real selling prices, yield ramps for colorless grades, and qualification timelines, strengthening our confidence in each assumption.

Desk Research

We began with public datasets from UN Comtrade, the United States International Trade Commission, OECD STAN, and the IPC electronics association, which map export tonnage, device output, and prevailing prices. Standards and chemical guidance from the European Chemicals Agency and ASTM clarified regulatory ceilings that shape demand. Company 10-Ks, patent families gathered through Questel, and news streams from Dow Jones Factiva helped our team follow capacity additions and technology migration. D&B Hoovers supported producer revenue cross-checks. The sources listed are indicative; many other documents were consulted for validation and clarification.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model framed the market. Global supply was rebuilt from nameplate film capacity, typical utilization, and net trade, then allocated to end uses with penetration metrics such as film area per OLED panel and meters per aircraft wire bundle. Average selling prices gathered during interviews converted volume to value and were reconciled with sampled producer revenues. Multivariate regression on smartphone OLED shipments, commercial aircraft deliveries, EV battery pack production, and industrial PMI trends produced the 2025-2030 outlook, with scenario adjustments where data were sparse.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent indicators before senior review. Reports refresh annually, and interim updates are triggered when events like plant outages or sharp resin price shifts would materially change the baseline.

Why Mordor's Polyimide Films Market Baseline Commands Reliability

Published estimates often diverge because firms apply different scopes, price ladders, or refresh cadences. One 2024 study valued the market at USD 2.61 billion, while another placed it at USD 1.38 billion. Our disciplined variable selection and yearly reconfirmation keep numbers anchored to real-world transactions.

Key gaps arise when adhesive-coated tapes are folded into core film revenue, when specialty colorless grades are excluded, or when headline capacity is treated as fully utilized; such choices can swing 2025 values by hundreds of millions of dollars.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.65 B (2025) | Mordor Intelligence | - |

| USD 2.61 B (2024) | Global Consultancy A | Includes tapes and assumes full capacity use |

| USD 1.38 B (2024) | Industry Research B | Excludes colorless grades and most aerospace demand |

The comparison shows that by clarifying scope choices, sampling real prices, and refreshing inputs every twelve months, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to verifiable volumes and prices.

Key Questions Answered in the Report

How large is the polyimide film market in 2026?

How large is the polyimide film market in 2026?

Which application segment leads demand?

Which application segment leads demand?

What region records the fastest revenue growth?

What region records the fastest revenue growth?

Why are colorless polyimide films important?

Why are colorless polyimide films important?

What is the main restraint facing producers?

What is the main restraint facing producers?

Page last updated on: