Polytrimethylene Terephthalate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

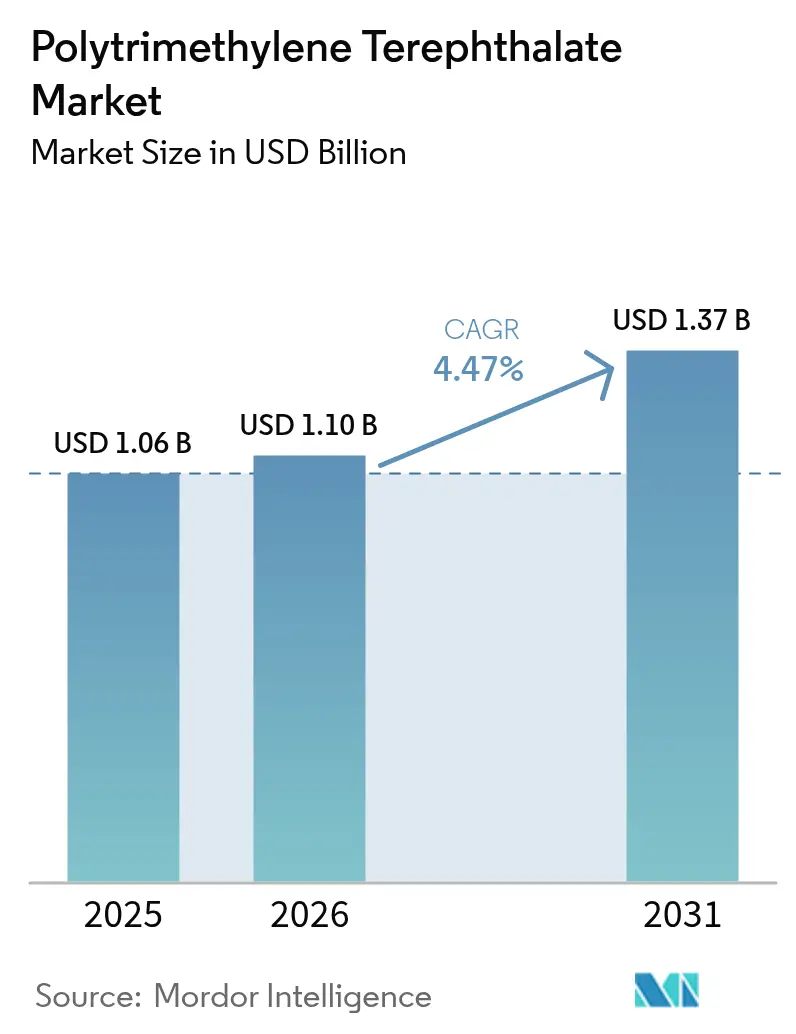

| Market Size (2026) | USD 1.10 Billion |

| Market Size (2031) | USD 1.37 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polytrimethylene Terephthalate Market Analysis by Mordor Intelligence

The Polytrimethylene Terephthalate Market size is expected to grow from USD 1.06 billion in 2025 to USD 1.10 billion in 2026 and is forecast to reach USD 1.37 billion by 2031 at 4.47% CAGR over 2026-2031. Brands are increasingly adopting PTT for applications like stretch-comfortable apparel, residential flooring, and additive manufacturing due to its helical molecular backbone, which eliminates the need for elastane. Producers are also using bio-based methods to reduce life-cycle emissions, helping brands showcase Scope 3 progress. China's launch of the world's largest integrated PDO-PTT complex by 2025 highlights its aim to lead the regional supply chain and cut costs. Meanwhile, DuPont's bio-PDO fermentation in North America has secured a premium niche, benefiting from renewable content certifications.

Three factors are driving demand. The global athleisure apparel market is outpacing the broader apparel sector, boosting the need for durable, stretchable fibers. Regulatory changes in Europe and North America now allow mass-balance recognition of bio-based and chemically recycled PTT. Additionally, lightweight materials for EVs and miniaturized consumer electronics are increasing interest in specialty polymers for resilient, soft-touch components. These trends reduce reliance on traditional PET and PBT grades while sustaining premium pricing, despite China's new commodity capacities saturating the market.

Key Report Takeaways

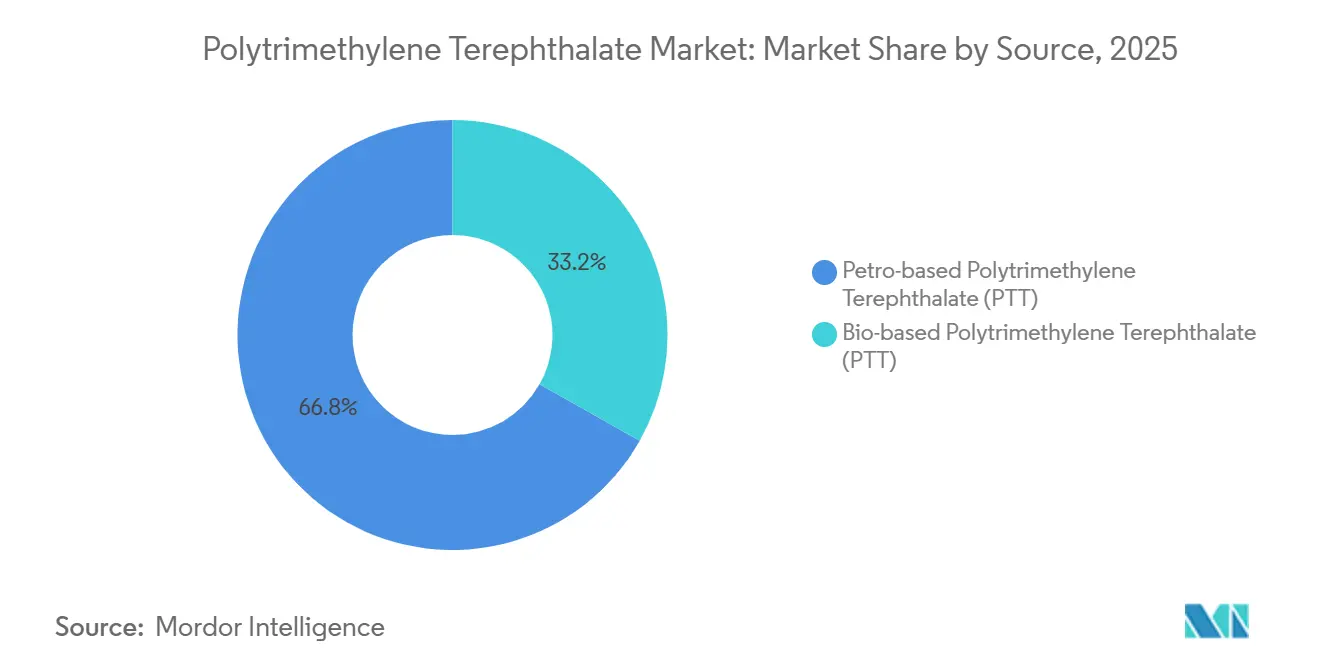

- By source, petro-based grades commanded 66.81% of the Polytrimethylene Terephthalate market share in 2025, while bio-based grades are forecast to register a 5.41% CAGR in the forecast period (2026-2031).

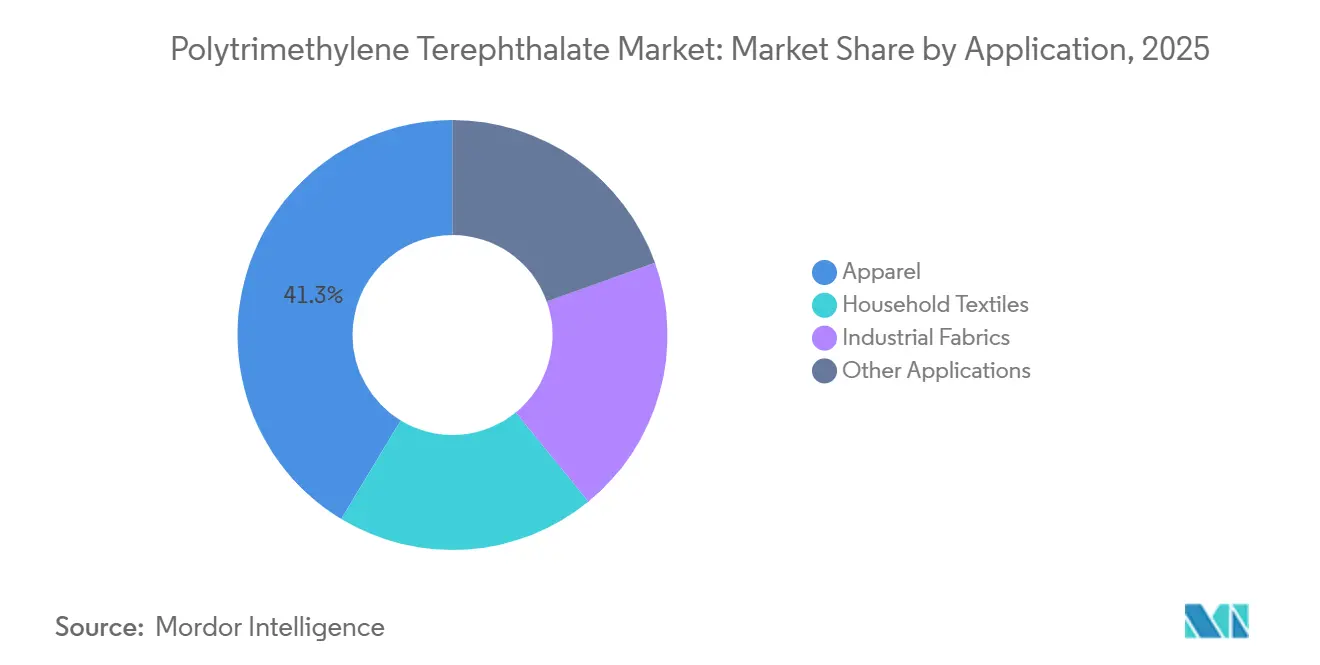

- By application, apparel held 41.34% of the Polytrimethylene Terephthalate market size in 2025, whereas the “other applications” cluster is poised for the fastest 4.99% CAGR in the forecast period (2026-2031).

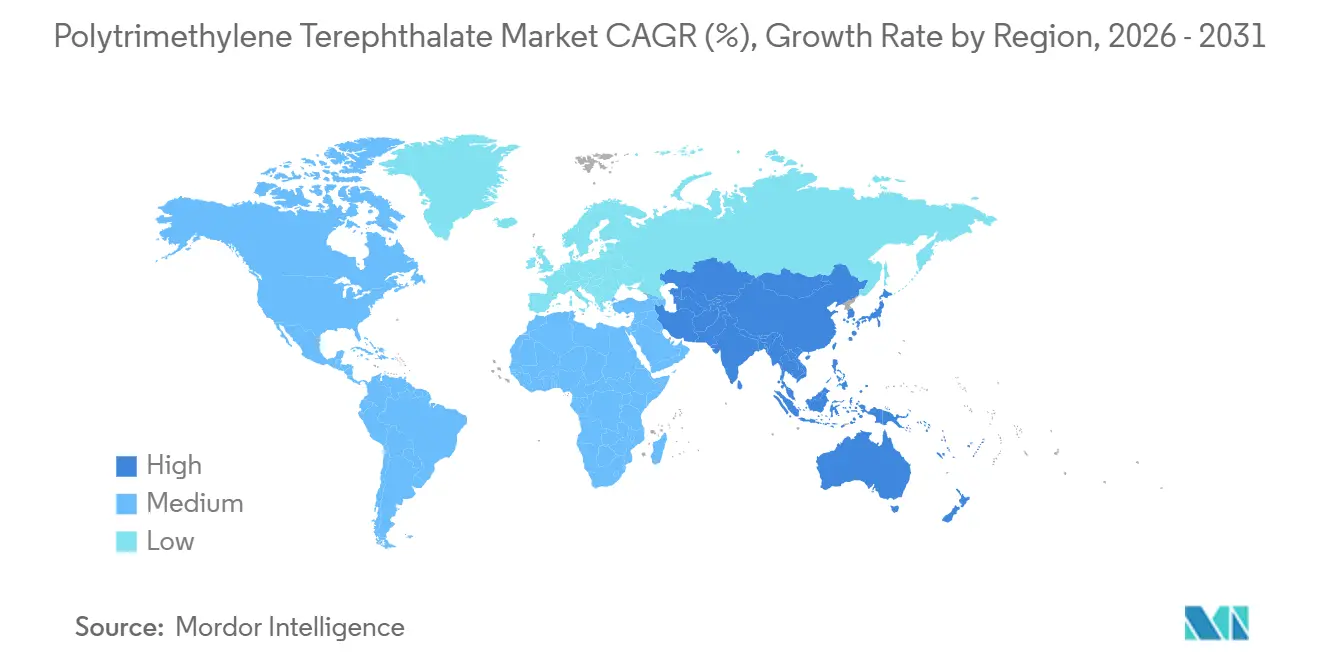

- By geography, Asia-Pacific led with 60.89% revenue share of the Polytrimethylene Terephthalate market in 2025 and is advancing at a 5.36% CAGR in the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polytrimethylene Terephthalate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising textile demand for stretch-comfort fibres | +1.2% | Global, with APAC core and North America athleisure segment | Medium term (2-4 years) |

| Sustainability push toward bio-based and recyclable polyester | +1.0% | North America and EU, spill-over to APAC brand supply chains | Long term (≥ 4 years) |

| Expansion of carpet/flooring applications (Triexta) | +0.9% | North America residential, emerging in Europe and Middle-East | Medium term (2-4 years) |

| PTT adoption in 3-D-printing filaments for prototyping | +0.5% | North America and EU industrial hubs, Japan research and development centers | Long term (≥ 4 years) |

| Use in EV lightweight composite components | +0.6% | APAC (China EV production), North America and EU OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Textile Demand for Stretch-Comfort Fibres

PTT, with its distinctive three-carbon diol bridge forming a spring-like helix that returns to shape after deformation, is gaining traction over standard polyester in athleisure, performance menswear, and fitted bottoms. Indian mills, motivated by fiscal incentives, are transitioning from traditional PET lines to PTT, targeting a balanced mix of man-made and natural fibers and aiming for premium orders. Teijin Frontier, a prominent player in Japan, has introduced bicomponent yarns featuring engineered crimp patterns for added stretch, eliminating the need for polyurethane and simplifying end-of-life processing. In North America, brand programs are assessing Sorona blends against nylon and elastane for wearer comfort, setting the stage for retail adoption at mid-tier price points.

Sustainability Push Toward Bio-Based and Recyclable Polyester

DuPont's fermentation-derived 1,3-propanediol (PDO), which reduces non-renewable energy consumption compared to nylon 6, has earned the USDA BioPreferred certification. In January 2026, Europe finalized rules granting mass-balance accreditation for chemically recycled polymers[1]European Commission, “EU Circular Plastics Package,” ec.europa.eu. This regulation permits PTT producers to count depolymerized monomers toward their recycled-content targets. In the agriculture sector, regenerative corn-growing practices, overseen by Truterra's platform, now evaluate nitrogen efficiency, soil health, and erosion metrics. This process ensures that brand buyers have a transparent chain of custody from feedstock to the final yarn. Lab research from CovationBio indicates that recycled PTT flakes can integrate seamlessly into PET streams without losing mechanical integrity. This advancement opens opportunities for PTT's incorporation into existing PET recycling facilities.

Expansion of Carpet/Flooring Applications (Triexta)

The U.S. Federal Trade Commission's endorsement of "Triexta" as a carpet fiber has effectively shielded it from the fate of commoditized polyester, cementing its reputation for stain resistance and durability. Mohawk's SmartStrand brand, which boasts renewable content, comes with a long-term wear warranty. Installers point to quicker drying times and resistance to chlorine as reasons for fewer call-backs, extending replacement cycles in both residential and hospitality flooring. With mortgage rates leveling off and renovation spending projected to rebound during the forecast period of 2026–2031, Triexta is steadily gaining ground in the mid-priced carpet segment. Retailers are spotlighting Triexta's softer texture and vibrant color clarity as standout attributes.

PTT Adoption in 3-D-Printing Filaments for Prototyping

Research and development centers in Detroit, Nagoya, and Munich are testing PTT filaments for various applications, including dashboards, consumer electronics housings, and prototypes for athletic equipment. PTT, a polymer that extrudes at lower temperatures than PET, offers advantages such as reduced warping and improved inter-layer bonding. Early adopters emphasize that PTT filaments provide an optimal balance between the rigidity of polylactic acid and the flexibility of thermoplastic polyurethane. However, challenges persist, as only a limited number of specialty compounders can ensure precise diameter control. On a positive note, the recent increase in resin capacity in China indicates potential for wider availability and price parity with premium PLA grades during the forecast period of 2026–2031.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs | -0.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Competition from PET and PBT incumbents | -0.6% | Global, with APAC price-sensitive segments | Medium term (2-4 years) |

| Feed-stock (PDO/PTA) supply volatility | -0.5% | Global, concentrated PDO supply in North America and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs

Bio-based PDO fermentation depends on the use of specialized bioreactors and efficient glucose logistics. As a result, the raw material costs for PTT are significantly higher than those for ethylene glycol-based PET. Although petrochemical methods utilizing propylene oxide or acrolein can help reduce feed costs, they do so at the expense of the renewable-content claims that brands with a focus on chemistry increasingly pursue. The capital demands in polymerization are also rising, as the need for twin-screw extruders with precise temperature zones arises from the higher melt viscosity, and slower crystallization requires extended cooling paths. In China, Ningbo Juhua has introduced its inaugural single-train design, improving unit economics; however, it still falls short of the benchmarks set by major PET complexes.

Competition from PET and PBT Incumbents

Decades of plant depreciation strengthen PET, which adheres to global recycling codes and benefits from commodity pricing that is more favorable than PTT. While PBT is the preferred material for high-heat electrical connectors, PTT's lower glass-transition temperature does not meet the necessary long-term creep standards. Thread manufacturers are advocating for a widespread shift to chemically recycled PET blends, putting pressure on the price-to-value balance of virgin PTT. Although laboratory findings suggest PTT's compatibility with PET recycling loops, the absence of dedicated sorting infrastructure for PTT hampers its commercial adoption. This delay not only reinforces PET's leading role but also hinders PTT's integration into the bottle-to-fiber recycling process.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Bio-Based PTT Captures Sustainability Premium

Forecasts predict that bio-based PTT, primarily sourced from fermentation-derived PDO, will experience a 5.41% CAGR growth rate during the forecast period of 2026–2031, outpacing its petrochemical counterpart. Brands across the European Union and North America are investing in certifications, reinforcing their commitment to net-zero goals. The market for bio-based polytrimethylene terephthalate (PTT) is poised for expansion, as the traceability from regenerative farming helps fashion labels sidestep reputational pitfalls. While the Asia-Pacific region leans toward petro-based PTT, benefiting from proximity to PTA supplies and cost-efficient integrated propylene oxide-PDO routes, tightening carbon taxes and shifting mass-balance regulations are nudging Chinese exporters. They are now marketing petro-PTT with claims of partial recycled content to retain their competitive edge. In 2025, petro-based PTT commanded a dominant 66.81% share of the polytrimethylene terephthalate market.

Policy initiatives further underscore this trend. The European Union's Circular Plastics Package, ratified earlier this year, endorses chemically recycled terephthalate monomers. This endorsement is catalyzing investments in depolymerization units adjacent to PET recyclers. On another front, India's February 2026 budget introduced the National Fibre Scheme. This scheme provides subsidies to man-made fiber plants that prioritize renewable or recycled inputs, subtly guiding investments toward bio-PTT production. Such policy moves not only accelerate the return on investment for fermentation facilities but also enhance the availability of certified materials favored by brands. This bolsters the case for bio-based dominance in the polytrimethylene terephthalate market.

By Application: Apparel Dominates, Other Uses Accelerate

In 2025, the apparel sector seized a 41.34% share of the polytrimethylene terephthalate (PTT) market, leveraging PTT's natural bulk, softness, and stretch, thus negating the need for spandex. Luxury outerwear brands are now opting for Sorona-based faux furs, branding them as a more sustainable and lower-shedding choice compared to traditional acrylics. Technical fashion brands are capitalizing on PTT's distinctive heat-settable crimp, ensuring pleated skirts and performance knitwear maintain their patterns even after multiple washes.

Other applications, identified as the fastest-growing segment, are set to expand at a 4.99% compound annual growth rate (CAGR) during the 2026-2031 period. The automotive interior segment of the polytrimethylene terephthalate market is expected to see steady growth, as electric vehicle manufacturers turn to low-VOC PTT foams and fabrics, moving away from heavier PVC and nylon. Prototype shops are adopting PTT-based 3-D printing filaments, praising their tactile comfort and recyclability. Concurrently, technical textile producers are incorporating PTT into filter bags and industrial ropes, utilizing its elastic recovery to extend service life.

Geography Analysis

In 2025, the Asia-Pacific region held a commanding 60.89% share of the polytrimethylene terephthalate market, a trend projected to persist through the forecast period of 2026–2031 with a steady CAGR of 5.36%. China's integrated PDO-PTT complex in Ningbo not only strengthens the regional resin supply but also strategically prices its export volumes below their North American bio-based counterparts. In India, the government's Textile Park stimulus and production-linked incentives are driving investments into synthetic-fiber modernization. This initiative positions converters in Surat and Tirupur to adopt PTT for warp-knitted athleticwear. Meanwhile, Japan's Teijin Frontier is capitalizing on the domestic demand for functional fashion by scaling up specialty bicomponent yarns. South Korean spinners are promoting hybrid PTT/PET hollow fibers, specifically designed for bedding.

North America, led by DuPont's integrated PDO fermentation in Loudon, Tennessee, and polymerization assets in North Carolina, is firmly anchored in premium bio-based grades. Mohawk's SmartStrand carpet franchise experiences consistent demand, supported by federal procurement guidelines that favor renewable-content flooring, increasing public-sector interest. United States athleticwear brands emphasize Sorona's significant reduction in greenhouse-gas emissions compared to nylon 6, reinforcing their sustainability commitments. Simultaneously, Canadian outerwear brands are experimenting with PTT blends, drawn by their flexibility in colder climates.

Circular economy mandates are increasingly shaping Europe. The End-of-Life Vehicle Regulation, now in effect, requires recycled plastic content by 2030[2]European Commission, “EU End-of-Life Vehicle Regulation,” ec.europa.eu. This regulation has spurred trials with PTT for instrument-panel skins, aiming to integrate them into PET's chemical-recycling processes. German automotive leaders are collaborating with tier-one suppliers to evaluate PTT's odor characteristics in heated cabin environments. Scandinavian outdoor brands, striving to meet the rigorous Bluesign standards, are incorporating bio-based PTT insulation, highlighting its rapid-drying capabilities, especially after extensive alpine testing.

Competitive Landscape

The Polytrimethylene Terephthalate market is moderately consolidated. Japanese firms are establishing premium niches with proprietary yarn architectures. Chinese players threaten to compress prices. Their integrated PDO-PTT flows cut down on freight and internal transfer margins. In retaliation, South Korean converters are diversifying their offerings. They are simultaneously developing PTT/PET side-by-side and hollow fibers, aiming at bulk home textiles and padding for colder continental markets. There is a promising avenue in chemical recycling consortia, which are exploring co-processing PTT with PET, and in elastomeric PTT copolymers. These copolymers, derived from bioPTMEG soft segments, are making inroads into medical devices and soft robotics.

Polytrimethylene Terephthalate Industry Leaders

DuPont

Huvis

TORAY INDUSTRIES, INC

Teijin Limited

Asahi Kasei Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Teijin Limited developed a lightweight, stretchable fabric from polytrimethylene terephthalate (PTT). The fabric, named "Solotex Liberte," combines stretchability and lightness with a premium texture, targeting the sportswear and casual wear segments.

- April 2023: Technip Energies received a contract from Ningbo Juhua Chemical & Science Co., Ltd. to construct a 150 KTA polytrimethylene terephthalate (PTT) facility in Ningbo, Zhejiang, China. The project will implement Technip Energies' proprietary Zimmer PTT technologies.

Global Polytrimethylene Terephthalate Market Report Scope

Polytrimethylene Terephthalate (PTT) is defined as a thermoplastic aromatic polyester produced through the condensation polymerization of 1,3-propanediol and terephthalic acid. Known for its combination of polyester's stain resistance and nylon's stretch and resilience, PTT is primarily utilized in carpets, textiles, and engineering plastics.

The Polytrimethylene Terephthalate (PTT) market is segmented by source, application, and geography. By source, the market is segmented into petro-based polytrimethylene terephthalate (PTT) and bio-based polytrimethylene terephthalate (PTT). By application, the market is segmented into apparel, household textiles, industrial fabrics, and other applications (e.g., automotive interior parts). The report also covers the market size and forecasts for the market in 17 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Petro-based Polytrimethylene Terephthalate (PTT) |

| Bio-based Polytrimethylene Terephthalate (PTT) |

| Apparel |

| Household Textiles |

| Industrial Fabrics |

| Other Applications (Automotive Interior Parts, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Petro-based Polytrimethylene Terephthalate (PTT) | |

| Bio-based Polytrimethylene Terephthalate (PTT) | ||

| By Application | Apparel | |

| Household Textiles | ||

| Industrial Fabrics | ||

| Other Applications (Automotive Interior Parts, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the polytrimethylene terephthalate market by 2031?

The Polytrimethylene Terephthalate Market size is expected to grow from USD 1.06 billion in 2025 to USD 1.10 billion in 2026 and is forecast to reach USD 1.37 billion by 2031 at 4.47% CAGR over 2026-2031.

Which application currently dominates demand?

Apparel leads with a 41.34% share of 2025 consumption, thanks to athleisure and performance menswear uptake.

How fast is bio-based PTT growing compared with petro-based grades?

Bio-based PTT is expanding at a 5.41% CAGR over 2026-2031, outpacing petro-based growth.

Why is PTT favored for residential carpet?

Its spring-like molecular structure yields built-in stain resistance and resilience without topical treatments, lowering maintenance costs.

What regulatory change in 2026 may boost PTT in automotive interiors?

The EU End-of-Life Vehicle Regulation mandates recycled plastic content by 2030, encouraging OEMs to trial recyclable PTT trims.

Which region holds the largest share of PTT demand?

Asia-Pacific commands 60.89% of global consumption in 2025, and is growing at a 5.36% CAGR (2026-2031).

Page last updated on: