Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

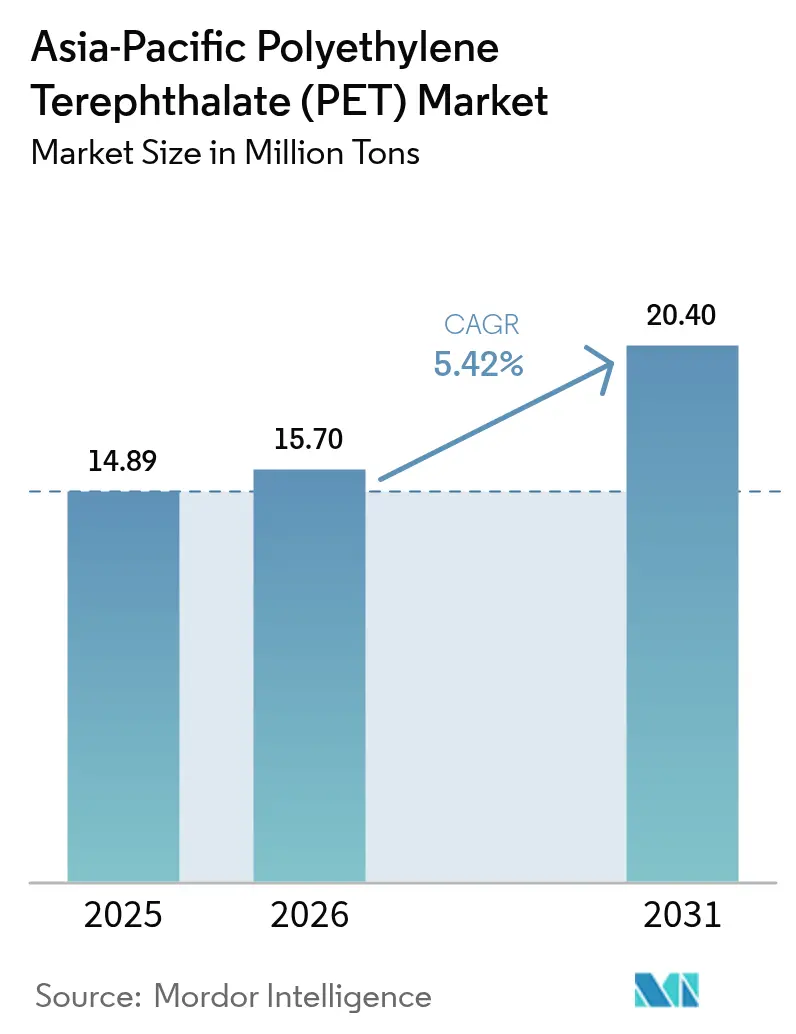

| Base Year Market Size (2025) | 14.89 Million tons |

| Market Volume (2026) | 15.7 Million tons |

| Market Volume (2031) | 20.4 Million tons |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

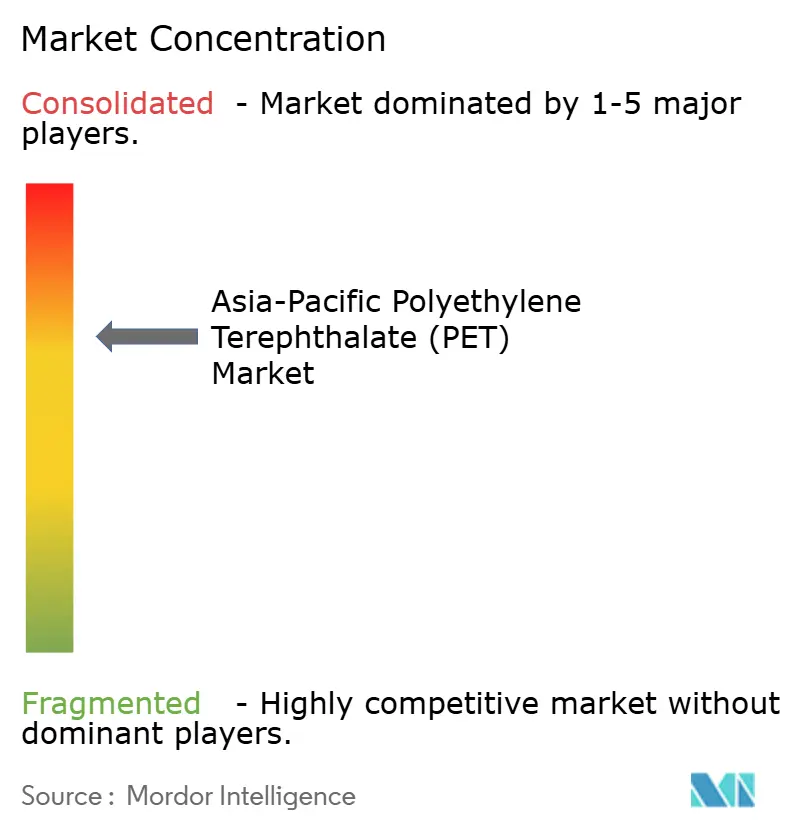

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Polyethylene Terephthalate (PET) Market Analysis by Mordor Intelligence

The Asia-Pacific Polyethylene Terephthalate Market size was valued at 14.89 Million tons in 2025 and estimated to grow from 15.7 Million tons in 2026 to reach 20.4 Million tons by 2031, at a CAGR of 5.42% during the forecast period (2026-2031). Current expansion is anchored in beverage premiumization, e-commerce logistics needs, and textile sector sustainability targets that collectively deepen PET penetration across consumer and industrial supply chains. Robust downstream integration keeps production costs competitive, while chemical recycling breakthroughs unlock bottle-to-bottle loops that appeal to regulators and multinational brand owners seeking verifiable carbon reductions. Demand diversification into automotive, electronics, and building applications stabilizes revenue streams against packaging seasonality, and localized capacity additions mitigate trade-policy friction by shortening lead times and lowering freight emissions. These converging factors reinforce the Asia-Pacific Polyethylene Terephthalate (PET) market leadership position and sustain investor confidence despite raw-material volatility.

Key Report Takeaways

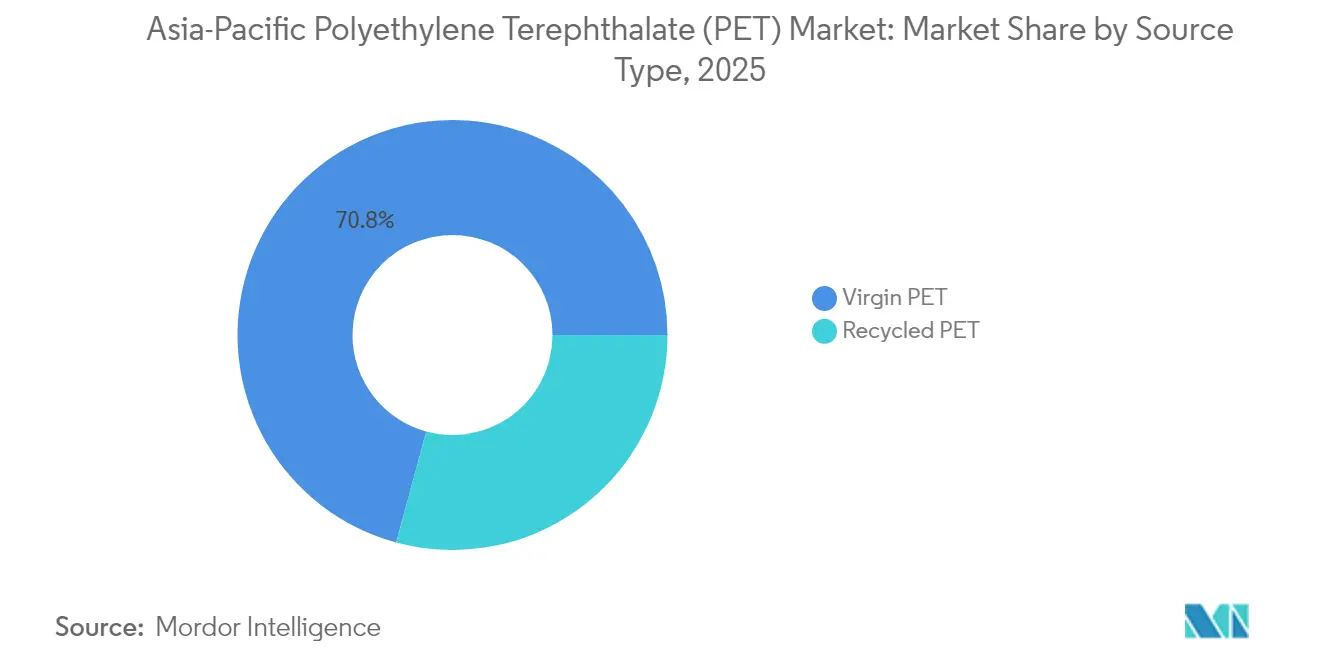

- By source type, virgin PET held 70.78% of the Asia-Pacific Polyethylene Terephthalate (PET) market size in 2025; recycled PET is poised to expand at a 6.62% CAGR between 2026 and 2031.

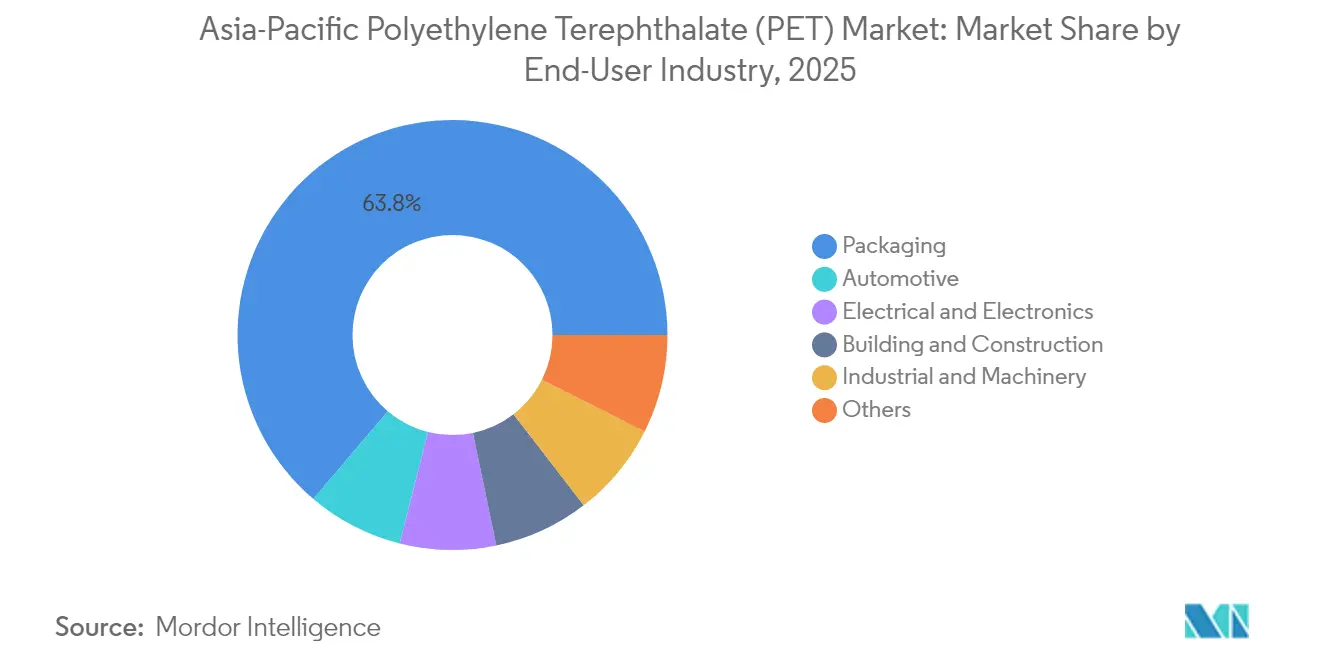

- By end-user industry, packaging captured 63.80% revenue share in 2025, while automotive applications are expected to grow fastest at a 5.65% CAGR through 2031.

- By geography, China led with 56.90% share in 2025; India is forecast to log the highest 5.99% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Polyethylene Terephthalate (PET) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in packaged beverage consumption | +1.40% | China, India, ASEAN core markets | Medium term (2-4 years) |

| Shift from glass/metal to PET packaging | +1.20% | Global, with concentration in India, Vietnam, Indonesia | Long term (≥ 4 years) |

| Growth of e-commerce protective packaging | +0.80% | China, South Korea, Japan, expanding to ASEAN | Short term (≤ 2 years) |

| Expansion of PET fiber use in fast-fashion | +1.10% | China, India, Bangladesh textile hubs | Medium term (2-4 years) |

| Chemical‐recycling scale-up in China and Japan | +1.30% | China, Japan, with technology transfer to India and ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Packaged Beverage Consumption

Asia-Pacific beverage producers increasingly favor lightweight PET over heavier legacy materials because the switch cuts logistics costs and widens rural distribution reach without compromising shelf stability. Brand owners moving into functional drinks and single-serve packs demand multilayer PET bottles with oxygen scavengers that keep nutrients intact across long supply chains. Regulatory permissions for recycled PET food-contact use, such as India’s 2025 FSSAI approval, remove compliance barriers and amplify circular-content messaging. Domestic converters respond by raising bottle-grade resin purity, thereby minimizing downstream reheat energy and shortening mold cycle times at high-volume fillers. These process gains reinforce the Asia-Pacific Polyethylene Terephthalate (PET) market trajectory because beverage demand climbs even during macroeconomic slowdowns when staple hydration products remain resilient.

Shift from Glass/Metal to PET Packaging

Value-chain participants trace material substitution momentum to the broader need for resilient packaging that withstands fragmented retail channels and erratic import duties on glass. In Vietnam, CPC’s 30,000 t y recycling plant generates locally sourced rPET pellets that feed bottle converters, establishing a closed-loop ecosystem which offsets virgin import costs and lowers carbon taxes. Early movers lock in collection networks by underwriting deposit-return schemes, ensuring steady feedstock while enhancing brand differentiation through traceable PCR logos. As smaller beverage companies confront capital constraints, turnkey hot-fill PET lines offer faster commissioning compared with glass furnaces, enabling agile product launches in flavored tea and dairy-based drinks. Consequently, substitution accelerates and reinforces demand visibility for the Asia-Pacific Polyethylene Terephthalate (PET) market.

Growth of E-commerce Protective Packaging

Online retail growth shifts packaging design from bulk palletization to individual parcel protection, prompting converters to supply co-extruded PET films that resist puncture yet remain curbside recyclable. Leading Chinese marketplaces stipulate 100% recyclability for private-label fulfillment packaging by 2027, embedding PET laminates with water-based adhesives that delaminate in alkaline wash lines. Regional film extruders invest in tandem orientation lines to deliver thinner gauges without sacrificing stiffness, lowering material intensity per shipment while maintaining consumer unboxing aesthetics. Seasonality peaks around shopping festivals create volatile demand spikes; PET film producers hedge by using real-time forecasting algorithms tied to e-commerce order books. This data-driven flexibility underpins steady consumption growth in the Asia-Pacific Polyethylene Terephthalate (PET) market and diversifies revenue beyond beverages.

Expansion of PET Fiber Use in Fast-Fashion

Global apparel brands committed to 25% recycled fiber content by 2030 pressure Asian spinners to secure rPET yarn supply at commercial scale. Melt-direct spinning, pioneered by Jiangsu Peipu, eliminates pelletizing and rewashing steps, cutting energy usage 30% while producing colored yarns that bypass aqueous dyeing. Brands leverage blockchain tags embedded in fiber masterbatches to certify bottle origin, satisfying transparency audits and widening marketing appeal. Textile mills blend rPET with bio-based PTA modifiers, achieving softer hand-feel and moisture management comparable to premium nylon, thereby unlocking higher price points. These advancements anchor double-digit volume gains for fiber-grade PET and extend the Asia-Pacific Polyethylene Terephthalate (PET) market reach into sustainable fashion segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Feedstock (PX/PTA) price volatility | -0.90% | Global, with acute impact on import-dependent markets | Short term (≤ 2 years) | |

| Competition from bio-degradable polymers | -0.70% | Developed APAC markets (Japan, South Korea, Australia) | Long term (≥ 4 years) | |

| Export tariffs on PX/PTA disrupting supply | -0.80% | China, South Korea, Japan export-dependent supply chains | Medium term (2-4 years) | |

| Source: Mordor Intelligence | ||||

Feedstock (PX/PTA) Price Volatility

Spot paraxylene prices surged in Q1 2025 after Middle-East maintenance outages, pushing PTA cash costs above contract PET selling prices for independent Chinese resin makers. Integrated majors weather the squeeze through internal hedging that blends term crude contracts with arbitrage cargoes from the U.S. Gulf. Smaller Southeast Asian producers lacking hedging sophistication confront negative spreads, triggering production cuts that tighten regional supply and lift delivered prices in India. Policymakers respond by reducing PTA import duties, yet currency depreciation offsets relief, keeping margins uncertain and delaying expansion capex. Such turbulence tempers near-term growth for the Asia-Pacific Polyethylene Terephthalate (PET) market until supply-demand balance stabilizes.

Competition from Bio-degradable Polymers

Multilayer coffee capsules and single-use cutlery markets in Japan and South Korea are increasingly adopting poly-lactic acid or polyethylene furanoate blends to comply with landfill-diversion targets effective 2028. Brand owners highlight compostability claims, capitalizing on consumer sentiment despite price premiums exceeding 40% over PET. However, scale-up hurdles persist because bio-feedstock cultivation competes with food crops, and bioreactor yields remain volatile. PET converters counter by integrating enzymatic depolymerization units that achieve circularity without abandoning established infrastructure, thereby diluting biodegradable materials’ appeal. Consequently, displacement risk for the Asia-Pacific Polyethylene Terephthalate (PET) market remains application-specific and gradual.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Virgin Leadership Encounters rPET Surge

Virgin resin remains the dominant feedstock, accounting for 70.78% of the Asia-Pacific Polyethylene Terephthalate (PET) market size in 2025, supported by long-term crude contracts and a depreciated Chinese yuan that keeps export pricing attractive. Nonetheless, recycled PET registers the fastest advance, projected at 6.62% CAGR, catalyzed by bottle-to-bottle mandates in India, Indonesia, and South Korea. Bhilwara Energy’s 100,000 t y Rajasthan facility showcases scaled depolymerization that processes 20 million post-consumer bottles daily while employing 700 workers. Government subsidies covering 15% capital expenditure shorten payback periods and lure additional investors, signaling robust policy alignment. Virgin producers hedge relevance by co-locating polymerization lines with mechanical wash-flake operations, securing blended resin supply that meets global food-contact protocols.

Supply-chain localization intensifies, with collection centers outfitted with AI-enabled optical sorters that raise flake purity above 98%, minimizing downstream filtration and extrusion energy. Export-oriented Indian rPET pelletizers tap European demand, where extended producer responsibility fees climb each year, making high-quality imported feedstock attractive despite shipping costs. In parallel, chemical recycling innovation converts colored textile scraps into clear polymers eligible for beverage applications, broadening feedstock pools and easing collection constraints. Consequently, feedstock diversification stabilizes resin availability and buffers the Asia-Pacific Polyethylene Terephthalate (PET) market from crude price shocks.

By End-user Industry: Packaging Strength Meets Automotive Acceleration

Packaging dominated revenue streams, capturing 63.80% Asia-Pacific Polyethylene Terephthalate (PET) market share in 2025 amid sustained beverage, personal-care, and household-chemical consumption. Lightweighting drives average bottle weight reductions of 12% over three years, yet absolute resin volumes rise because unit sales expand across rural regions adopting bottled water. Conversely, automotive uptake surges, advancing at a 5.65% CAGR as electric-vehicle OEMs substitute metal housings with PET-based composite enclosures that assure electromagnetic shielding and flame resistance. High-gloss interior trims molded from PET/ASA blends replace painted ABS, trimming volatile-organic-compound emissions during assembly.

Electronics manufacturers escalate PET film demand for flexible printed circuits and insulation barriers in 5G smartphones, leveraging the polymer’s dielectric stability and dimensional control. Construction contractors adopt UV-stabilized PET sheets as transparent roofing in tropical climates, where resistance to yellowing surpasses PVC alternatives. Industrial machinery integrators specify PET gears and housings that withstand lubricants and deliver quieter operation than metal, opening fresh specialty niches. This multi-sector adoption deepens market resilience, extends the Asia-Pacific Polyethylene Terephthalate (PET) market reach, and minimizes exposure to regulatory shocks in any single downstream segment.

Geography Analysis

China anchored 56.90% Asia-Pacific Polyethylene Terephthalate (PET) market share in 2025, leveraging vertically integrated complexes that co-locate PX, PTA, and polymerization units to trim logistics overhead. Strategic stockpiling of refinery-grade mixed xylenes insulates producers from geopolitically driven crude swings, sustaining competitive FOB pricing. Environmental policies enforce stricter wastewater recycling, prompting capex in membrane bioreactors that simultaneously elevate ESG credentials and unlock export opportunities to eco-label-driven Western brands. Meanwhile, India outpaces regional peers with a projected 5.99% CAGR, propelled by production-linked incentives and emerging middle-class consumption upgrading to packaged drinks and synthetic garments. Partnership agreements such as LNJ GreenPET-Sumitomo advance rPET ecosystem maturity, combining global marketing networks with domestic collection know-how. Further, in India, the PET recycling rate stands at 90%, surpassing Japan's 72%, Europe's 48%, and the United States' 31%. This underscores India's significant potential for advancing a circular economy.

Japan pursues premium-grade flakes for high-barrier films, capturing elevated margins despite stagnant population growth by emphasizing technology licensing and design services. Malaysia leverages strategic shipping lanes and free-trade agreements to attract converter relocation from tariff-exposed China, boosting domestic pellet demand while launching anti-dumping probes that curtail low-priced imports. South Korea supplies advanced melt-filter and solid-state polycondensation equipment, exporting turnkey lines to ASEAN refurbishing clusters. Collectively, these geographic dynamics sustain supply-chain resilience and nurture balanced growth across the Asia-Pacific Polyethylene Terephthalate (PET) market.

Competitive Landscape

The Asia-Pacific Polyethylene Terephthalate (PET) market comprises integrated petrochemical conglomerates, mid-tier regional specialists, and fast-growing recyclers vying for share amid tightening sustainability mandates. Top-tier players leverage captive PX and PTA streams, automated polymer lines, and multi-country distribution networks to maintain low unit costs and secure multiyear offtake agreements with global beverage and apparel brands. Mid-tier firms differentiate through niche grades, responsive customer service, and tactical geographic positioning close to end-markets, enabling shorter lead times and customized resin properties.

Recycling specialists attract private-equity funding by demonstrating scalable bottle-to-bottle flows and by securing FDA and EFSA food-contact letters that broaden export opportunities. These entrants often partner with city governments to guarantee feedstock volumes via deposit-return schemes, thereby reducing input-price volatility and ensuring predictable margins. Large incumbents hedge competitive threats by acquiring minority stakes in recyclers and by integrating enzymatic depolymerization units that complement mechanical recycling, positioning themselves as full-spectrum circular-polymer suppliers.

Strategic moves include Indorama Ventures’ decision to establish advanced greenfield PET recycling facilities across India[2]Indorama Ventures Public Company Limited, “Indorama Ventures, Dhunseri and Varun Beverages Joint Venture plans multiple cutting-edge recycling facilities in India,” indoramaventures.com. Wankai New Materials invests in Indonesian flake production to bypass tariffs and capture emerging Southeast Asian growth, while CPC scales Vietnam’s wash-line infrastructure to supply high-grade pellets to Japanese converters. Collectively, these maneuvers elevate technology entry barriers, consolidate feedstock control, and intensify rivalry across the Asia-Pacific Polyethylene Terephthalate (PET) market.

Asia-Pacific Polyethylene Terephthalate (PET) Industry Leaders

China Petroleum & Chemical Corporation

Far Eastern New Century Corporation

Indorama Ventures Public Company Limited

Reliance Industries Ltd.

Zhejiang Hengyi Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Indorama Ventures Public Company Limited announced the recycling of more than 150 billion post-consumer PET bottles since 2011. This milestone reflects the company's unwavering commitment to circular economy practices and its ongoing investments in global recycling infrastructure.

- September 2024: Indorama Ventures Public Company Limited has entered into a joint venture with Varun Beverages Limited, PepsiCo's second-largest global bottler outside the US, through its direct subsidiary, IVL Dhunseri Petrochem Industries Limited, and Dhunseri Ventures Limited. The partnership aims to establish advanced greenfield PET recycling facilities across India.

Asia-Pacific Polyethylene Terephthalate (PET) Market Report Scope

Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Australia, China, India, Japan, Malaysia, South Korea are covered as segments by Country.By Source Type

| Virgin PET |

| Recycled PET (rPET) |

By End-user Industry

| Packaging |

| Automotive |

| Electrical and Electronics |

| Building and Construction |

| Industrial and Machinery |

| Others |

By Geography

| China |

| India |

| Japan |

| Malaysia |

| South Korea |

| ASEAN Countries |

| Rest of Asia-Pacific |

| By Source Type | Virgin PET |

| Recycled PET (rPET) | |

| By End-user Industry | Packaging |

| Automotive | |

| Electrical and Electronics | |

| Building and Construction | |

| Industrial and Machinery | |

| Others | |

| By Geography | China |

| India | |

| Japan | |

| Malaysia | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyethylene terephthalate market.

- Resin - Under the scope of the study, virgin polyethylene terephthalate resin in primary forms such as liquid, powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms