Middle East Polyethylene Terephthalate (PET) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

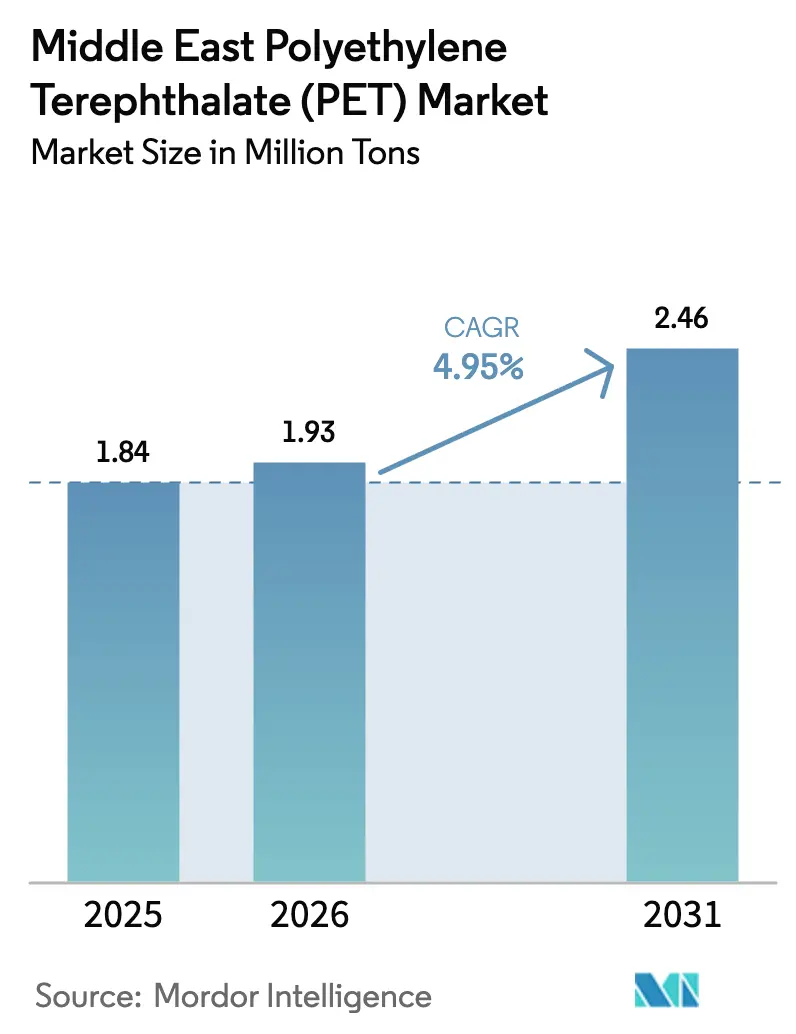

| Base Year Market Size (2025) | 1.84 Million tons |

| Market Volume (2026) | 1.93 Million tons |

| Market Volume (2031) | 2.46 Million tons |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

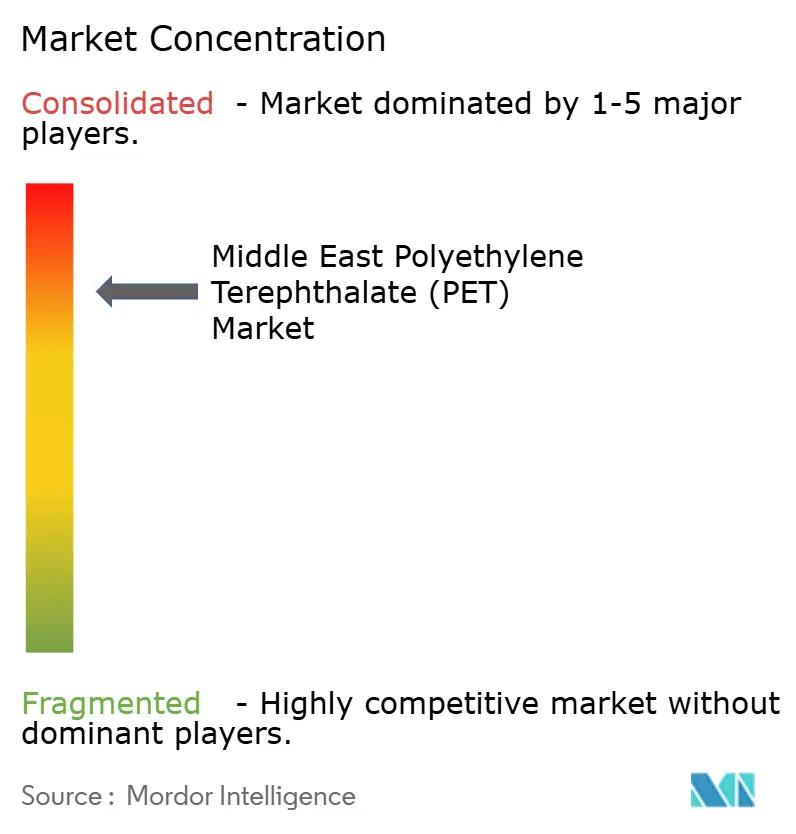

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Polyethylene Terephthalate (PET) Market Analysis by Mordor Intelligence

The Middle East Polyethylene Terephthalate Market size was valued at 1.84 million tons in 2025 and estimated to grow from 1.93 million tons in 2026 to reach 2.46 million tons by 2031, at a CAGR of 4.95% during the forecast period (2026-2031). Strong tourism flows, urban lifestyle shifts, and clear sustainability mandates keep demand on an upward path even as price volatility and regulatory complexity challenge producers. Saudi Arabia and the UAE remain the largest volume centers, yet smaller GCC members contribute a rising share of incremental growth as they scale hospitality and retail infrastructure. Integrated producers benefit from a USD 200–300 per-ton feedstock cost edge that preserves margins when crude prices rise. At the same time, mandatory recycled content rules accelerate investment in chemical recycling and rPET capacity, gradually tilting the competitive field toward players that can secure post-consumer feedstock. A widening application base in electronics and renewable-energy hardware adds another layer of structural growth that lifts volumes beyond traditional beverage packaging.

Key Report Takeaways

- By source type, virgin PET commanded 72.64% share of the Middle East PET market size in 2025, while recycled PET is forecast to increase at a 5.62% CAGR through 2031.

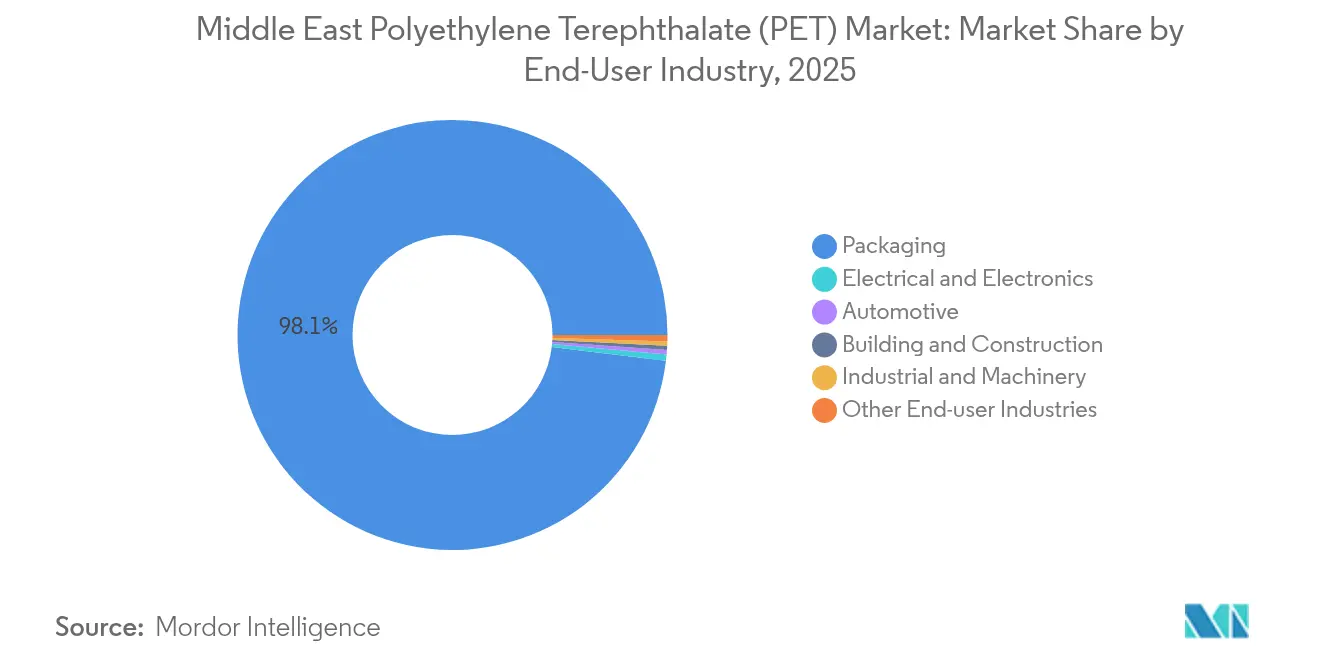

- By end-user industry, packaging accounted for 98.08% of the Middle East PET market size in 2025, and electrical and electronics is advancing at a 7.25% CAGR through 2031.

- By geography, Saudi Arabia accounted for 44.80% revenue share of the Middle East PET market size in 2025 and is progressing at a 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Polyethylene Terephthalate (PET) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding bottled-water consumption in GCC | +1.20% | Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Booming packaged and convenience food sector | +1.00% | UAE, Saudi Arabia, Kuwait | Medium term (2–4 years) |

| GCC tourism spike driving on-the-go PET demand | +0.80% | UAE, Saudi Arabia, Bahrain | Short term (≤ 2 years) |

| Petrochemical feedstock cost advantage | +0.60% | Saudi Arabia, Kuwait, UAE | Long term (≥ 4 years) |

| Mandatory rPET content targets from 2027 | +0.50% | UAE, Saudi Arabia, regional spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exploding Bottled-Water Consumption in GCC

Per-capita bottled-water intake in Saudi Arabia stands at 120 liters per year, roughly double the global average, a figure that underscores climate-driven hydration needs and premium brand preferences. Dubai’s 17.15 million visitors in 2024 added 130 million liters of bottled water demand, with summer months accounting for 40% of that volume surge. Qatar’s expanding hospitality pipeline and Saudi Arabia’s NEOM development are poised to lift tourist water consumption even higher through 2030. This relentless thirst sustains bottle-grade resin offtake, supports high-speed preform lines, and incentivizes lightweighting to reduce material intensity. The result is persistent growth in the Middle East PET market despite gradual shifts toward refillable systems.

Booming Packaged and Convenience Food Sector

UAE hypermarkets and e-commerce channels report double-digit growth in ready-to-eat meals, snacks, and multi-cuisine frozen products that require PET-based barrier films for extended shelf life. Expat communities representing more than 80% of the UAE population seek global food brands formatted in portion-controlled packs, magnifying demand for thermoformed trays and lidding film. Saudi Arabia’s Vision 2030 food-processing drive encourages local conversion of imported staples, opening avenues for domestic packaging lines built around PET clarity and strength. As dual-income households proliferate across GCC capitals, the convenience gap widens, further cementing PET as the material of choice for portable, microwavable, and high-oxygen-barrier food solutions within the Middle East PET market.

GCC Tourism Spike Driving On-the-Go PET Demand

More than USD 100 billion in hospitality and entertainment projects are underway, from Dubai’s Expo-legacy districts to Saudi Arabia’s Red Sea resorts. These assets attract short-stay travelers who favor portable beverage, snack, and personal-care packs capable of tolerating temperature swings. Airline catering, duty-free retail, and stadium concessions consume large quantities of single-serve PET bottles that must meet lightweight, shatter-resistant standards. Seasonal visitor peaks trigger supply chain strains that favor local resin production over imports and secure additional off-take contracts for regional converters. The tourism flywheel therefore feeds back into the Middle East PET market, lifting baseline demand through 2030.

Petrochemical Feedstock Cost Advantage

Ethane-based steam crackers and paraxylene units in Jubail, Yanbu, and Shuaiba deliver a USD 200–300 per-ton cost cushion versus naphtha-based plants in Asia. Long-term supply pacts with Saudi Aramco and Kuwait Petroleum anchor price stability, enabling competitive export offers even when Brent exceeds USD 85 per barrel. Clustering reduces logistics costs by up to 20%, and government incentives on utilities lower variable costs further. This structural edge allows producers to invest in chemical recycling, specialty copolymers, and multilayer technologies without eroding margins, a dynamic that keeps the Middle East PET market attractive to both incumbents and new entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil & PX price volatility | -0.70% | Regional, with Kuwait most exposed | Short term (≤ 2 years) |

| Single-use-plastic bans in UAE & KSA | -0.40% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Limited food-grade rPET capacity less than 30 ktpa | -0.30% | Regional, affecting all GCC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil and PX Price Volatility

Paraxylene prices track crude swings, compressing spreads for PET producers during high-priced cycles even after feedstock discounts. Kuwait’s EQUATE plant, reliant on naphtha cracking, sees margin dips of 15% when Brent rallies, prompting occasional load reductions. Saudi-based integrated complexes hedge better but still struggle to maintain export competitiveness when oil tops USD 90. Regional governments have begun rationalizing energy subsidies that once cushioned these shocks, pushing producers to lock in shorter contracts or adopt cost-plus formulas. Such volatility injects planning uncertainty into the Middle East PET market and may deter brownfield expansions until pricing visibility improves.

Single-Use-Plastic Bans in UAE & KSA

The UAE banned single-use plastic bags in 2024 and is rolling out 30% recycled-content rules for beverage bottles by 2027. Saudi Arabia follows with phased restrictions that vary by province, complicating compliance. Beverage bottles remain temporarily exempt, yet converters must prepare for future scope expansion into cups, lids, and specialty film. Smaller import-reliant processors face capital hurdles in transitioning to rPET or alternative materials, and enforcement inconsistencies delay investment decisions. While policy clarity improves over time, the interim uncertainty restrains capacity additions in the Middle East PET market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Virgin PET Leadership Faces rPET Acceleration

Virgin resin accounted for 72.64% of 2025 volume, but recycled grades aim for 5.62% CAGR through 2031 as policy and brand pledges realign purchasing. UAE law mandates 30% rPET in bottles by 2027, pushing beverage fillers to secure food-grade pellets months ahead of compliance deadlines. SABIC’s tie-up with Chinese depolymerization specialists and Nile Plastic Recycling’s USD 15 million expansion will lift local rPET supply by 20,000 tons once operational in 2026.

Still, regional collection systems capture less than 10% of post-consumer PET, forcing importers to backhaul baled bottles from African and European ports. Producers with pyrolysis and solvent-based technologies can tap mixed-plastic streams, although cost parity with virgin resin remains elusive when crude prices are low. As feedstock aggregation improves, the Middle East PET market expects rPET penetration to rise while maintaining virgin dominance in niche optical and high-stress uses.

By End-User Industry: Packaging Supremacy Challenged by Electronics Growth

Packaging accounted for 98.08% of the 2025 PET volume, reflecting the region’s consumption tilt and reliance on bottled water. Electrical and electronics demand posts the fastest pace at a 7.25% CAGR, driven by data center corridors in Dubai South and Saudi Arabia’s NEOM tech zone. Infrastructure projects upgrade to PET-based insulating films due to dielectric stability and dimensional accuracy at elevated temperatures.

Retail digitization and rapid grocery delivery models require tamper-evident clear packaging that supports QR-code track-and-trace, further cementing PET’s packaging stranglehold. Yet smartphone assembly and solar-panel back-sheet makers are beginning to specify flame-retardant PET substrates, signaling a gradual broadening. As diversified industries mature, the Middle East PET market will still lean on packaging for scale but pivot toward electronics for margin lift.

Geography Analysis

Saudi Arabia’s 44.80% share anchors the Middle East PET market, and its 5.52% CAGR outlook keeps it in the lead through 2031. Population growth to 38 million, Vision 2030 tourism corridors, and feedstock abundance overlap to support both domestic conversion and export shipments. SABIC’s incremental debottlenecking and JBF RAK’s expansion secure inward resin flows for bottled-water, dairy, and industrial clients while positioning the Kingdom as a supply hub to Africa.

The UAE’s cosmopolitan retail landscape is distinguished by its regulatory innovation. The nation mandates the use of recycled content and has enacted bans on single-use items, steering the market towards high-performance and sustainable products. Duty-free channels at Dubai and Abu Dhabi airports add transit-driven demand that often peaks in the winter months when tourist arrivals crest. Local recyclers accelerate post-consumer collection schemes in partnership with municipal authorities to meet looming 2027 requirements.

Kuwait, Qatar, and Oman collectively account for a modest share today but exhibit bright prospects given tourism investment and omnichannel retail adoption. Kuwait’s EQUATE complex offers regional supply redundancy, while Qatar’s airport expansion funnels beverage and catering volumes into PET. Oman’s Duqm special economic zone attracts logistics operators who prefer PET for bulk edible-oil and chemical drums. Though fragmented, these markets expand faster on a percentage basis, bringing incremental tonnage that enriches the overall Middle East PET market.

Competitive Landscape

The Middle East PET market exhibits consolidated concentration. SABIC exercises portfolio breadth, blending commodity grades with emerging rPET streams via alliances with Chinese technology partners. Indorama Ventures and JBF RAK leverage process know-how to bolt on 210,000 tons of fresh capacity aimed at lightweight bottles and high-gloss films.

Competition pivots on access to post-consumer feedstock and the ability to certify food-grade rPET. Smaller recyclers focus on flake exports but risk feedstock scarcity once beverage fillers internalize collection. Asian integrated groups eye joint ventures near UAE ports to circumvent logistics costs and capitalize on tourism-driven demand. Meanwhile, specialty film converters explore antistatic and UV-stabilized PET for electronics, diversifying revenue beyond beverage packaging.

Strategic responses coalesce around vertical integration, technology upgrades, and supply-chain localization. Producers deepen alliances with waste-management firms to lock in bottle bales, while converters invest in rapid-tooling and digital printing to serve short-run SKUs. Regulatory compliance complexity favors scale operators with in-house legal and sustainability teams, reinforcing existing leadership yet leaving room for niche challengers that deliver differentiated performance or circularity credentials within the Middle East PET market.

Middle East Polyethylene Terephthalate (PET) Industry Leaders

Alpek S.A.B. de C.V.

Indorama Ventures Public Company Limited

JBF RAK LLC

Reliance Industries Limited

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: JBF RAK LLC, a Gulf-based producer of polyethylene terephthalate (PET) polymer resin, has unveiled a comprehensive restructuring initiative. With the restructuring now in effect, JBF RAK is positioned to strengthen its role in the polyethylene terephthalate market, potentially enhancing the supply chain and driving growth in the Middle East market.

- July 2025: Nile Plastic Recycling announced plans to invest an additional USD 15 million to expand its polyethylene terephthalate (PET) recycling facility in Egypt's Sokhna Industrial Zone. This expansion aims to increase the company's recycling capacity by 20,000 tons annually. The upgraded plant is scheduled to begin operations in the first half of 2026.

Middle East Polyethylene Terephthalate (PET) Market Report Scope

Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Saudi Arabia, United Arab Emirates are covered as segments by Country.| Virgin PET |

| Recycled PET (rPET) |

| Packaging |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Other End-user Industries |

| Saudi Arabia |

| United Arab Emirates |

| Rest of Middle East |

| By Source Type | Virgin PET |

| Recycled PET (rPET) | |

| By End-User Industry | Packaging |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Other End-user Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyethylene terephthalate market.

- Resin - Under the scope of the study, virgin polyethylene terephthalate resin in primary forms such as liquid, powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms