Polyisobutylene (PIB) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

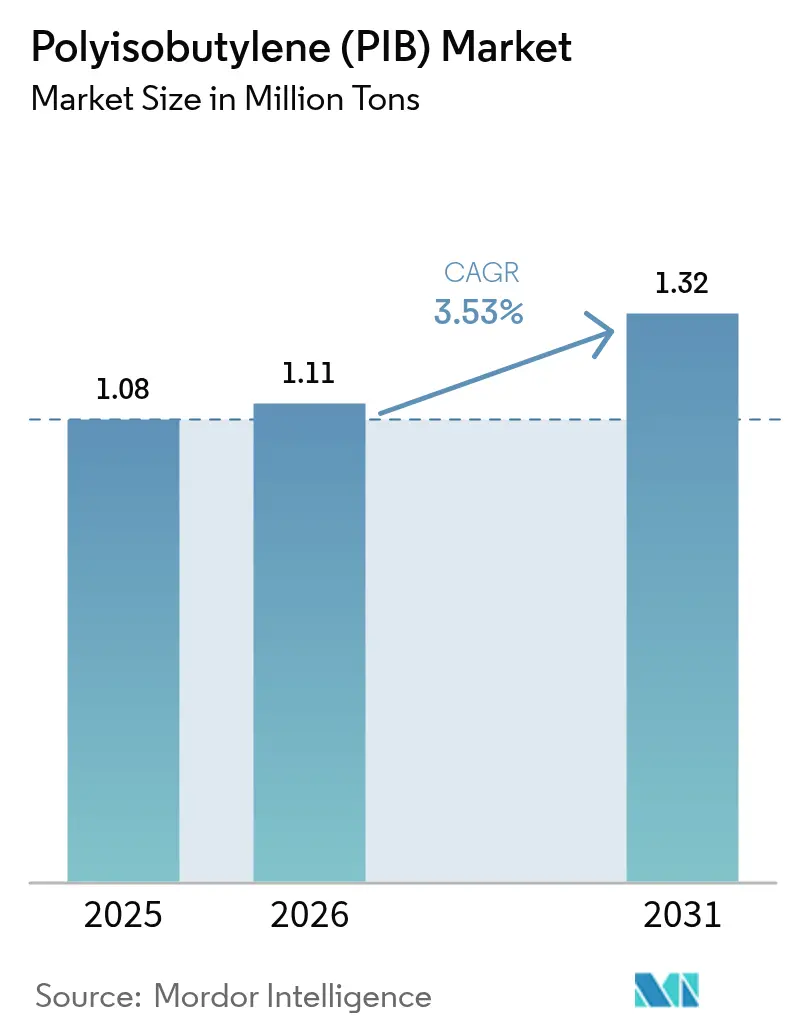

| Market Volume (2026) | 1.11 Million tons |

| Market Volume (2031) | 1.32 Million tons |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyisobutylene (PIB) Market Analysis by Mordor Intelligence

The Polyisobutylene Market size was valued at 1.08 Million tons in 2025 and is estimated to grow from 1.11 Million tons in 2026 to reach 1.32 Million tons by 2031, at a CAGR of 3.53% during the forecast period (2026-2031). Regulatory pressure for low-viscosity engine oils, the transition to tubeless radial tires, and an upswing in construction adhesives jointly reinforce demand momentum. Producers are directing capital toward highly reactive and medium-molecular-weight grades that meet stringent fuel-economy, emissions, and durability targets. While Asia-Pacific spearheads capacity additions, the Middle-East leverages inexpensive ethane and butane feedstocks to position itself as an export hub. Competitive emphasis therefore tilts toward differentiation—through oxidation-stable chemistries, battery-binder functionality, and water-borne dispersions—rather than pure volume expansion, buffering margins against feedstock volatility and price-based competition.

Key Report Takeaways

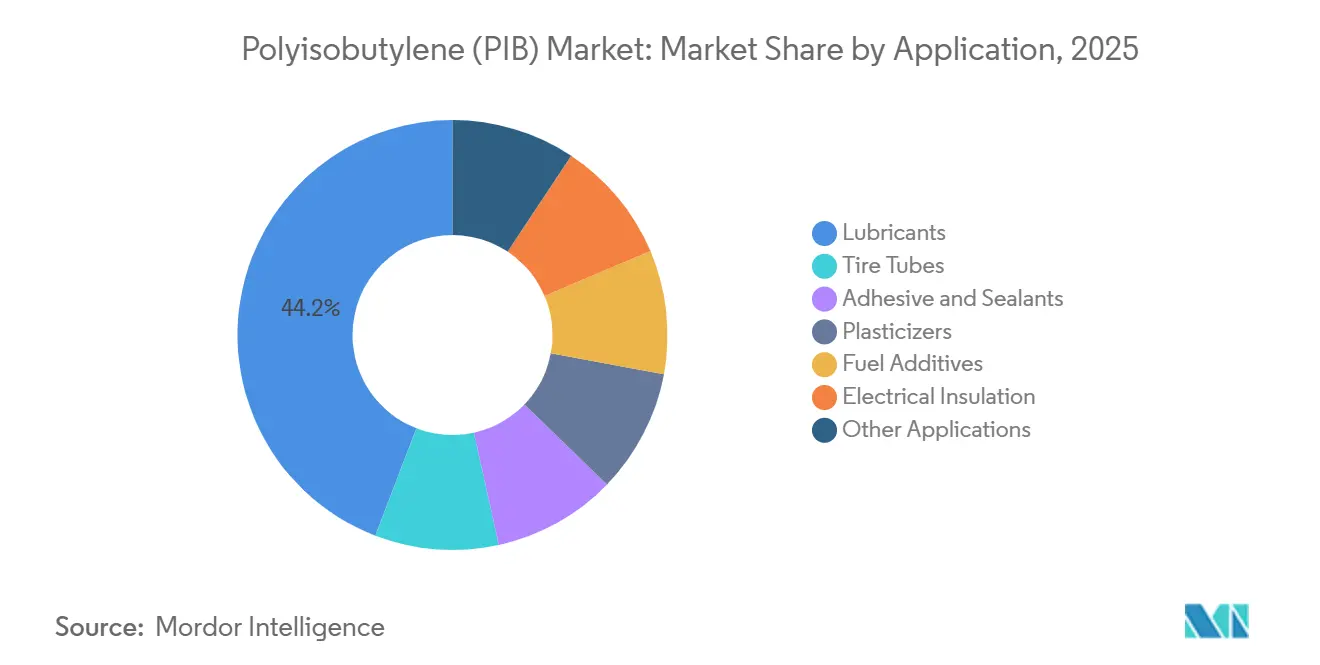

- By application, lubricants led with 44.16% of polyisobutylene market share in 2025 and are forecast to expand at a 3.78% CAGR through 2031.

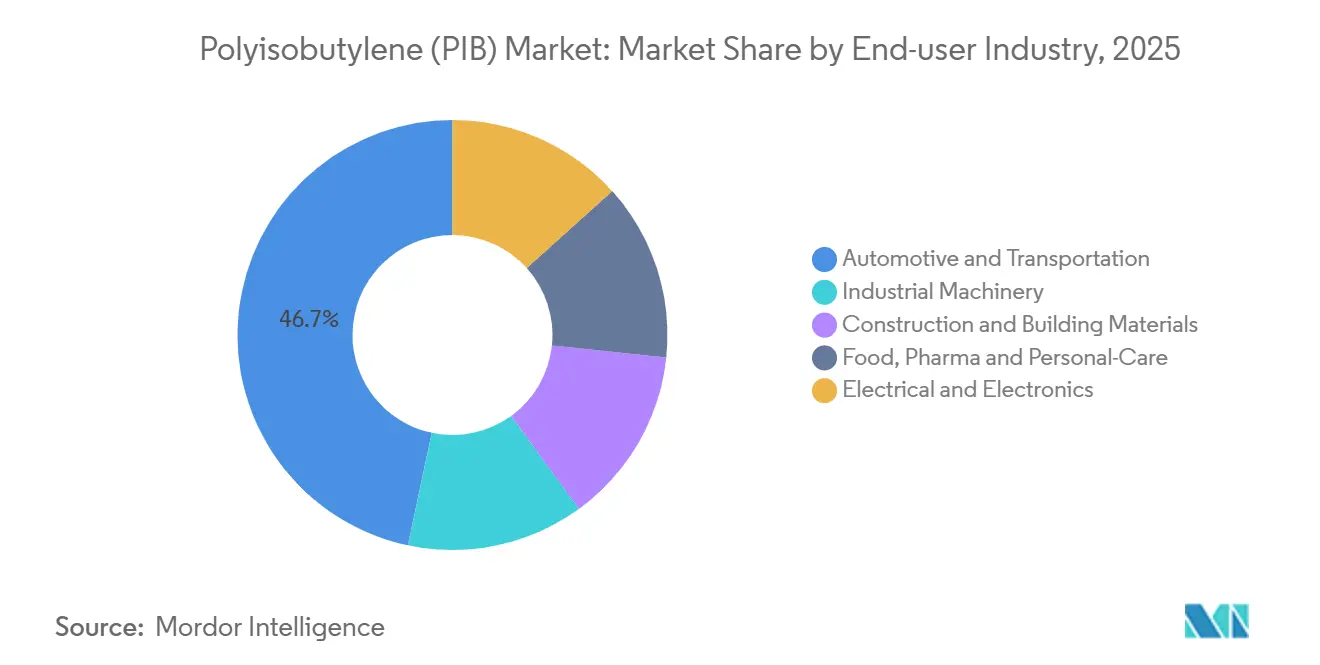

- By end-use industry, automotive and transportation held 46.67% of the polyisobutylene market size in 2025 and is projected to grow at a 3.89% CAGR through 2031.

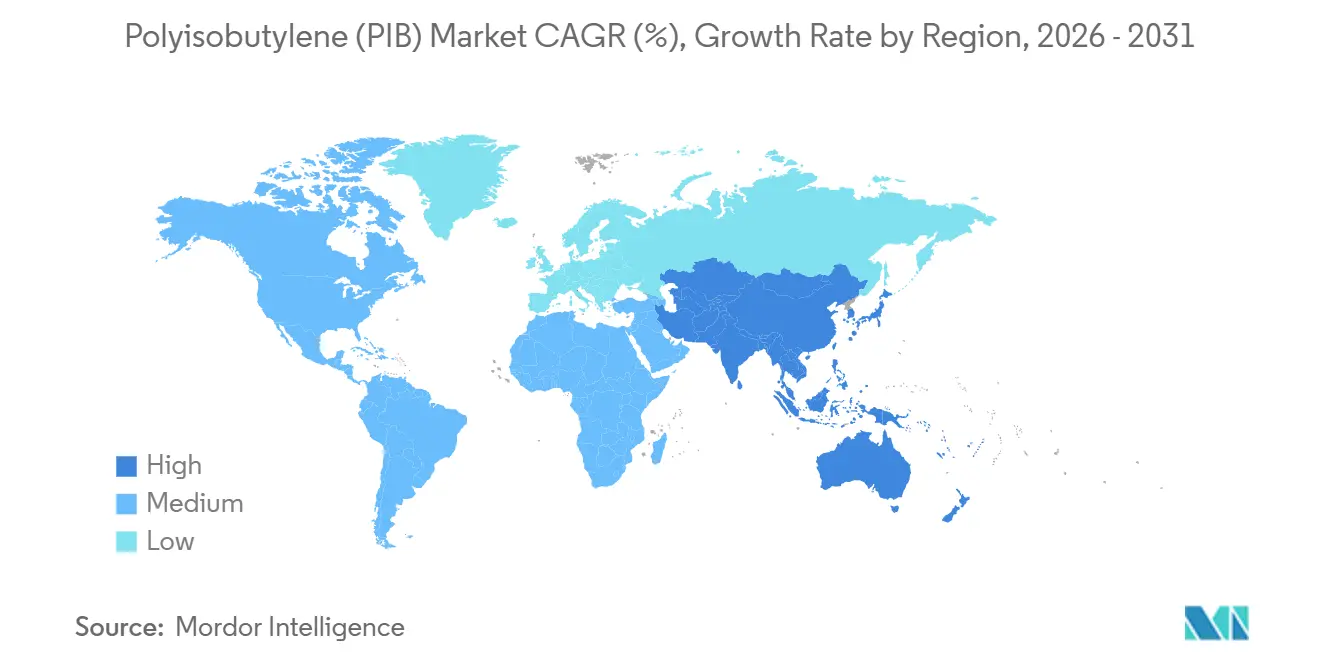

- By geography, Asia-Pacific held 39.42% of the polyisobutylene market size in 2025 and is projected to grow at a 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyisobutylene (PIB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from adhesives and sealants | +0.8% | Global, with concentration in Asia-Pacific construction and North America automotive aftermarket | Medium term (2–4 years) |

| Rising use in tire inner-liners and tubeless compounds | +1.0% | Asia-Pacific (China, India tire production), North America OEM fleets | Medium term (2–4 years) |

| Expanding role as viscosity modifier in next-generation lubricants | +0.9% | Global, led by North America and Europe regulatory-driven reformulation | Long term (≥4 years) |

| Shift toward highly reactive PIB for fuel/lubricant additives | +0.6% | North America, Europe, Japan (stringent emissions standards) | Long term (≥4 years) |

| Hydrogen infrastructure gaskets and seals requiring PIB barrier films | +0.2% | Europe (hydrogen corridors), Japan, South Korea (national hydrogen strategies) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Adhesives and Sealants

Construction and aftermarket adhesives increasingly specify polyisobutylene because moisture- and gas-barrier performance surpasses polyurethane and acrylic alternatives. H.B. Fuller’s insulated-glass sealants, based on medium-Mn grades, exceed 25-year edge-seal durability under EN 1279 thermal cycling, which aligns with tighter European building-energy codes. Pressure-sensitive-tape makers blend low-Mn PIB with tackifiers to secure ≥20 N/25 mm peel strength, satisfying packaging and automotive-trim requirements across humid Asian climates. ISO 11600 and ISO 9047 compliance opens international procurement channels for Chinese and Indian converters, allowing them to move beyond domestic sales without compromising performance. The polyisobutylene market therefore benefits doubly—from higher unit volumes in new construction and from premium pricing for long-life sealants. Capacity investments across Zhejiang and Guangdong are timed to catch this demand crest, amplifying Asia-Pacific’s share in global shipments.

Rising Use in Tire Inner-Liners and Tubeless Compounds

Tire makers substitute conventional butyl inner-liners with halobutyl-PIB blends that lower air permeability by 30-40%, lengthening pressure-retention intervals and cutting rolling resistance to satisfy fuel-economy rules. ExxonMobil’s Exxpro™ elastomer family achieves permeability coefficients below 20 × 10⁻¹² cm³ cm/(cm² s cmHg), now a baseline for electric-vehicle tires. Goodyear’s 2024 filings add cold-flexibility enhancements, preserving liner integrity below −40 °C. China’s GB/T 29042 labeling and India’s 22% tire-export surge underpin Asia-Pacific volume growth, while Southeast Asian new entrants license technology from Daelim and ENEOS to supply OEM fleets. As a result, tire formulations inject fresh momentum into the polyisobutylene market, ensuring that volume growth keeps pace with vehicle electrification trends.

Expanding Role as Viscosity Modifier in Next-Generation Lubricants

Engine-oil formulators shift toward high-Mn PIB (10,000–50,000) for viscosity modification that resists mechanical shear in turbocharged gasoline direct-injection engines. Lubrizol’s PIBSI dispersants maintain viscosity index ≥150 across API SP and ILSAC GF-6 oils, curbing sludge and varnish deposition. Chevron Oronite’s chlorine-free OLOA 15500 line meets California Safer Consumer Products rules, signaling tighter additive stewardship. The 0W-16 and 0W-20 viscosity grades mandated by U.S. CAFE standards and Japan’s JASO GLV-1 protocol amplify PIB consumption as formulators balance fuel-economy with engine durability. Industrial uses follow a similar arc: wind-turbine-gearbox lubes incorporating PIB stretch oil-change intervals beyond five years, supporting offshore wind maintenance economics. This driver secures a long-term pillar for the polyisobutylene market.

Shift Toward Highly Reactive PIB for Fuel and Lubricant Additives

High-reactive PIB (HR-PIB) with ≥75% vinylidene content enables detergents that achieve injector-cleanliness ratings above 9.5 in IKA tests—well ahead of conventional PIBA benchmarks. Daelim’s scale-up from 65 kt to 100 kt in Yeosu and its 80 kt joint venture in Jubail cement Middle-Eastern cost leadership. BASF’s Ludwigshafen debottlenecking prioritized 2,500–10,000 Mn material targeting battery binders and medium-viscosity dispersants. TPC Group’s epoxidized PIBplus variant enhances oxidation stability, challenging PAO in premium motor-oil formulations. Together, these offerings widen performance bandwidth and secure premium pricing, inflating the value pool within the broader polyisobutylene market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock isobutylene price volatility | -0.7% | Global, acute in regions dependent on naphtha crackers (Europe, Northeast Asia) | Short term (≤2 years) |

| Intrinsic UV instability demanding costly stabilizers | -0.3% | North America and Europe (outdoor construction, automotive aftermarket) | Medium term (2–4 years) |

| Tightening VOC and REACH limits on solvent-borne PIB systems | -0.4% | Europe (REACH enforcement), California (CARB regulations) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Feedstock Isobutylene Price Volatility

Isobutylene originates mainly from C4 refinery cuts and on-purpose isobutane dehydrogenation, exposing PIB producers to 75% spot-price swings between USD 800 and USD 1,400 per tonne during 2024-2025[1]U.S. Energy Information Administration, “Petroleum Supply Monthly,” eia.gov . EU carbon permits at EUR 80–100 per tonne of CO₂ further tax European naphtha crackers, tilting the cost curve toward ethane-rich Middle-Eastern plants. On-purpose routes stabilize supply but entail catalyst and hydrogen-management costs that only large integrated sites can absorb. Bio-routes from Global Bioenergies and LanzaTech remain pilot-scale, with costs at 2–3× petrochemical pathways, constraining near-term relief. This volatility compresses margins and dampens capital planning across the polyisobutylene industry.

Intrinsic UV Instability Demanding Costly Stabilizers

Outdoor sealants require 1–3% hindered-amine or benzotriazole packages to meet 10-year durability under ASTM G154, adding up to USD 1.50 kg-¹ to finished costs. These additives face potential REACH re-registration due to endocrine-disruption flags, risking further cost escalation. Alternatives such as co-extruded UV-opaque layers increase process complexity, while fully UV-stable chemistries like silicone challenge PIB on price. The margin squeeze is especially acute in Europe and North America, where warranty expectations extend past 20 years for insulating-glass sealants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Lubricants Anchor Growth

Lubricants held 44.16% of 2025 volume, accounting for the largest slice of the polyisobutylene market. This segment will outpace the broader market at a 3.78% CAGR as automakers adopt 0W-16 and 0W-20 oils to reach U.S. 49 mpg fleet targets. HR-PIB-based dispersants maintain sludge control and shear stability, ensuring compliance with API SP and ILSAC GF-6. Additive suppliers leverage PIB’s saturated backbone to resist oxidation, giving energy producers longer gear-oil drain intervals in offshore wind assets.

Conversely, fuel additives, consuming HR-PIB for PIBA detergents, remain a smaller but technologically intensive segment. Demand growth hinges on increased gasoline direct-injection penetration, especially in North America and Europe where over 50% of new cars employ GDI systems. Adhesives and sealants represent about one-fifth of volume, propelled by Asia-Pacific construction but tempered by VOC mandates in Europe. In chewing-gum and pharmaceutical closures, FDA-cleared low-Mn PIB remains irreplaceable for sensory neutrality. Electrical-insulation uses—cable compounds and potting materials—contribute a modest share yet realize steady growth as renewable-energy grids expand. Collectively, these niches stabilize baseline volume and diversify profit streams within the polyisobutylene market.

By End-use Industry: Automotive Dominance Continues

Automotive and transportation captured 46.67% of 2025 demand and will grow at 3.89% CAGR, fueled by halobutyl-PIB inner-liners, low-viscosity lubricants, and high-tack weatherstrip adhesives. Asia-Pacific, with 900 million tires produced in 2024, remains the center of gravity for this surge.

Industrial machinery follows with roughly one-quarter of consumption. Wind-turbine gearboxes in Europe and China specify PIB-enhanced lubes to push oil-change cycles beyond five years, slashing offshore maintenance costs. Construction gains incremental share through long-life sealants needed for energy-efficient glazing in dense urban centers. Food, pharma, and personal-care preserve a safety-critical but smaller demand pocket, leveraging PIB’s biocompatibility under FDA 21 CFR 175.105. Electrical and electronics applications rise in tandem with high-voltage cable and charging-station rollouts, ensuring steady volume absorption across the forecast horizon.

Geography Analysis

Asia-Pacific dominated with 39.42% of 2025 volume and is the fastest-growing at 4.12% CAGR. China’s 18% H1 2024 spike in tire output and India’s cost-advantaged specialty-grade exports cement regional leadership. Japan and South Korea add technology heft via HR-PIB plants that feed global additive chains. Southeast Asian newcomers in Malaysia and Vietnam license halobutyl compounding lines to win OEM contracts, broadening intra-regional competition and expanding the polyisobutylene market footprint.

North America is expanding on shale-gas feedstock advantages. TPC Group’s 27% Houston di-isobutylene augmentation and Lubrizol’s Deer Park HR-PIB line cater to domestic and export customers. Canada and Mexico add incremental pulls through automotive-component factories tied to U.S. OEMs, while California’s VOC rules drive early adoption of water-borne emulsions, nudging product-mix evolution.

In Europe, BASF’s 25% Ludwigshafen expansion targets automotive and battery niches, while INEOS’ Project ONE cracker promises lower-carbon feedstocks by 2027, potentially lifting regional cost competitiveness[2]INEOS, “Project ONE Progress Update,” ineos.com . However, REACH and Decopaint VOC caps prompt adhesive formulators to re-engineer toward hybrid or aqueous systems, a shift that restrains near-term growth but may unlock value for high-performance, compliant grades.

In South America, Brazil’s vehicle production and Argentina’s agricultural-equipment needs underpin adhesive and lubricant purchases. Middle-East and Africa demand is led by Saudi Aramco/Total and Daelim’s 80 kt HR-PIB venture in Jubail, positioning the region as a low-cost export springboard. Emerging hydrogen corridors in the UAE and Saudi Arabia also create niche demand for PIB-based gasket materials, signaling future-ready diversification in the polyisobutylene market.

Value Chain Analysis

The PIB value chain starts with C4 feedstocks (isobutylene and mixed butenes from refinery FCC streams and steam crackers) or from on-purpose isobutane dehydrogenation, then uses cationic polymerization to produce low-, medium-, and highly reactive PIB grades. Integration can reduce exposure to feedstock swings for some large producers, including BASF, INEOS, and Daelim, while stand-alone and smaller regional players typically see more variability in supply continuity and delivered costs.

Midstream value creation focuses on purification, molecular-weight control, and functionalized intermediates such as PIBSA for lubricant and fuel-additive packages. The material then feeds compounding and formulation for tires (inner-liners and tubeless compounds), lubricants (viscosity modifiers and dispersants), and adhesives and sealants (insulated glass, construction membranes, and tapes). Distribution is commonly direct to additive majors and tire makers, with chemical distributors also supporting sealants and industrial uses. Logistics and European energy and feedstock shocks are repeatedly cited as bottlenecks; meanwhile, China added around 30,000 tpa of high-reactivity capacity during 2024-2025, aimed at PIBSA-linked demand in India and Vietnam, which supports more regionalized flow from Asian production hubs into downstream additive and compounding corridors.

Competitive Landscape

The polyisobutylene market demonstrates moderate concentration: the top five producers—BASF, INEOS, TPC Group, Daelim, and Lubrizol—control roughly 62% of global capacity. Operating rates hover near 70%, limiting spot-market liquidity and channeling rivalry into product differentiation and service depth. BASF’s 25% Ludwigshafen debottlenecking targets battery-binder and medium-Mn dispersant grades, signaling a pivot toward e-mobility adjacencies. TPC Group’s PIBplus introduces epoxidation to raise oxidation resilience, carving space in premium lubricant blends, while INEOS fields Indopol and PANALANE series spanning 3 cSt to 45,000 cSt to match diverse customer needs.

Daelim exports HR-PIB technology to Lubrizol and Middle-Eastern partners, reinforcing its stature as a license-led growth architect. ENEOS, through a Japanese seal-maker partnership, develops PIB-FKM hybrids for hydrogen infrastructures, seeking early-mover advantage in that nascent segment. Chinese mid-tier firms like Zhejiang Shunda push commodity grades priced 15–20% below Western offers but struggle to meet HR-PIB purity required for fuel-additive markets, leaving an opening for incumbents to preserve premium margins.

Innovation moves beyond chemistry into logistics and digital service. INEOS modernizes French infrastructure to streamline C4 feedstock flows, while TPC upgrades Houston isocontainer loading for agile exports. Lubrizol extends technical-support labs to help blenders navigate API and ILSAC test regimes, embedding stickiness in its customer relationships. With rising sustainability scrutiny, producers also invest in life-cycle analyses and low-carbon certifications, aligning portfolios with customer ESG mandates and reinforcing differentiation within the polyisobutylene market.

Polyisobutylene (PIB) Industry Leaders

BASF

TPC Group

INEOS

Daelim Co., Ltd.

Lubrizol

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Higher-value PIB opportunities stand out where performance and compliance pressures overlap: low-VOC adhesive and sealant systems (including insulated-glass edge seals and specialty construction membranes), high-reactivity PIB for detergent and dispersant chemistries in low-viscosity engine oils, and emerging barrier and binder roles connected to electrification. BASF has already indicated this shift through actions at Ludwigshafen, combining medium-molecular-weight capacity expansion with product work oriented around battery-related assembly needs. This supports a move away from commodity PIB toward grades that face tighter specifications for purity, reactivity (including vinylidene content), and oxidation stability.

A second opportunity is localization and supply assurance across Asia-Pacific as tire and additive ecosystems scale. The 2024-2025 buildout of high-reactivity capacity in China targeted PIBSA-oriented downstream chains in India and Vietnam, while producers and additive formulators continue to re-engineer formulation packages to meet API SP and ILSAC GF-6 performance requirements without relying on legacy chemistries. In addition, non-traditional end uses within the scope, such as PIB as a substitute for wool-fat in leather stuffing agents and PIB-based binder technologies for next-generation battery anodes, point to premium niches where qualification cycles and application engineering, rather than nameplate capacity alone, shape share gains.

Recent Industry Developments

- June 2026: BASF completed capacity expansion at Ludwigshafen for medium-molecular-weight PIB grades to support higher-purity PIB for downstream battery-related assembly and sealant applications. The project improves BASF's ability to supply specialty PIB grades to automotive and construction customers and expands the role of PIB in e-mobility platforms.

- December 2025: TPC Group reported completing its first ISCC system transaction, extending its ability to document certified sustainability attributes through its supply chain. This step improves credentials for customers in lubricants and other formulated products as procurement requirements around traceability tighten. It also complements the company's feedstock and site-infrastructure strategy by pairing operational capability with certification readiness.

- December 2024: TPC Group completed a capital program at its Houston operations that lifted crude C4 processing capacity to a maximum sustained daily rate 25% higher than any prior year peak. Greater C4 flexibility supports availability of key PIB-related streams, including isobutylene and di-isobutylene routes, during tight or volatile periods. The upgrade improves responsiveness to downstream demand swings across additives, elastomers, and specialty hydrocarbon chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers polyisobutylene (PIB) sold as a polymer material and consumed across industrial uses where PIB is selected for tack, sealing, and viscosity control.

Scope exclusions: We exclude downstream finished goods revenue (such as tires, sealants, and lubricant packs) and count only the PIB material value or volume traded and consumed.

Segmentation Overview

- By Application

- Lubricants

- Tire Tubes

- Adhesive and Sealants

- Plasticizers

- Fuel Additives

- Electrical Insulation

- Other Applications

- By End-use Industry

- Automotive and Transportation

- Industrial Machinery

- Construction and Building Materials

- Food, Pharma and Personal-Care

- Electrical and Electronics

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Russia

- Spain

- Turkey

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- Nigeria

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to structure the demand pool and make sure the key PIB consuming industries were not missed. We referenced public sources such as USGS chemical and materials data, US International Trade Commission trade statistics, UN Comtrade, OECD industry indicators, and the European Chemicals Agency database for regulatory and substance-level context.

Along with this, we reviewed producer and downstream disclosures like annual reports, investor presentations, product brochures, and reputable press coverage to track capacity changes, grade positioning, and shifts in end-use demand. Patent databases and an import-export shipment-level database were used selectively to cross-check trade direction and to spot where cross-border supply meaningfully influences availability. These desk sources are illustrative, and other public references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on validating how PIB demand forms inside important customer chains, including lubricant additive blending, tire and rubber compounding, and adhesive and sealant formulation. We spoke with producers, distributors, compounders, and large end users across APAC, EMEA, and the Americas, and then rechecked key assumptions when responses showed a wide spread.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 45% |

| Mid tier: 42% | Functional/Unit leaders: 29% | EMEA: 34% |

| Smaller Players: 20% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where PIB consumption is reconstructed from end-use output and trade signals, and then translated into polymer demand using application intensity factors. To keep totals grounded, we corroborated the result with selective bottom-up approximations like sampling typical price ranges by grade, reviewing announced capacity and utilization signals where visible, and using channel checks on order patterns and substitution behavior.

Key inputs that shaped the model included lubricant additive treat rates linked to the automotive parc and engine oil demand, tire and rubber production trends, adhesives and sealants output tied to construction activity, PIB grade mix shifts (low versus medium and high molecular weight), and feedstock-driven pricing movements that affect buying behavior. Forecasts were developed using scenario analysis, where macro indicators and end-use output were varied and then aligned to what industry experts expect for adoption and substitution. When visibility was limited in smaller countries, gaps were handled by using regional normalization factors and then filtering the result through import reliance and local manufacturing presence checks.

Data Validation & Update Cycle

Model outputs are triangulated against independent signals, including regional trade balances, known capacity change timelines, and whether implied demand growth matches end-use production patterns. Outliers are reviewed in a second pass where unit conversions, price assumptions, and application shares are stress-tested, and we re-contact sources when variance stays high.

Before publication, the work goes through multi-step analyst reviews so calculations, assumptions, and written conclusions remain consistent. Reports refresh annually, and interim updates are made when material events occur such as outages, major expansions, or sharp feedstock price moves. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Polyisobutylene Pib Market Size Measured Against Other Published Estimates

Published market sizes for PIB often do not line up because the same material can be counted using different units, different grade mixes, and different pricing assumptions. Base-year selection, currency timing, and whether recycling or reprocessing loops are treated as new demand can also create visible differences.

The main gap comes from unit choice and conversion assumptions, where Mordor Intelligence keeps the headline sizing anchored to reported metric-ton demand and uses price mainly as a cross-check by grade and region, instead of applying a single global ASP curve. Some other sources present only a revenue number and may blend in stronger price uplift, or they may extend the counted market by implicitly including downstream product economics rather than the PIB material itself.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.00 B (2026) | |

| Industry Publisher A | USD 2.25 B (2024) | Revenue-first sizing can diverge when a single average price is applied across PIB grades and regions, and when price changes are assumed to compound faster than physical demand growth. |

| Global Publisher B | USD 2.16 B (2024) | Uses a revenue model with its own base-year pricing and type and application mix assumptions, which can shift the implied ASP and the total market size even if volumes are similar. |

The table shows that most of the spread is explained by whether PIB is sized in tons or converted into dollars, and by how grade mix and regional pricing are handled over time. By keeping the demand pool definition tied to material consumption indicators and then validating pricing with interviews and desk checks, our output stays easier to reproduce and audit.

Key Questions Answered in the Report

What is the size of the polyisobutylene market?

The polyisobutylene market size stands at 1.11 million tons in 2026 and is forecast to hit 1.32 million tons by 2031, supported by a 3.53% CAGR from 2026-2031.

Which application segment leads in consumption?

Lubricants command 44.16% of 2025 volume and will remain the largest consumer through 2031 as low-viscosity engine oils proliferate.

Why is Asia-Pacific the fastest-growing region?

Robust tire production in China and India, coupled with regional capacity additions for highly reactive grades, propels Asia-Pacific at a 4.12% CAGR.

How are VOC regulations affecting PIB adhesives?

EU and California VOC caps push formulators toward water-borne or hot-melt PIB systems, spurring adoption of patented aqueous emulsions despite higher formulation complexity.

Page last updated on: