Polyetheramine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

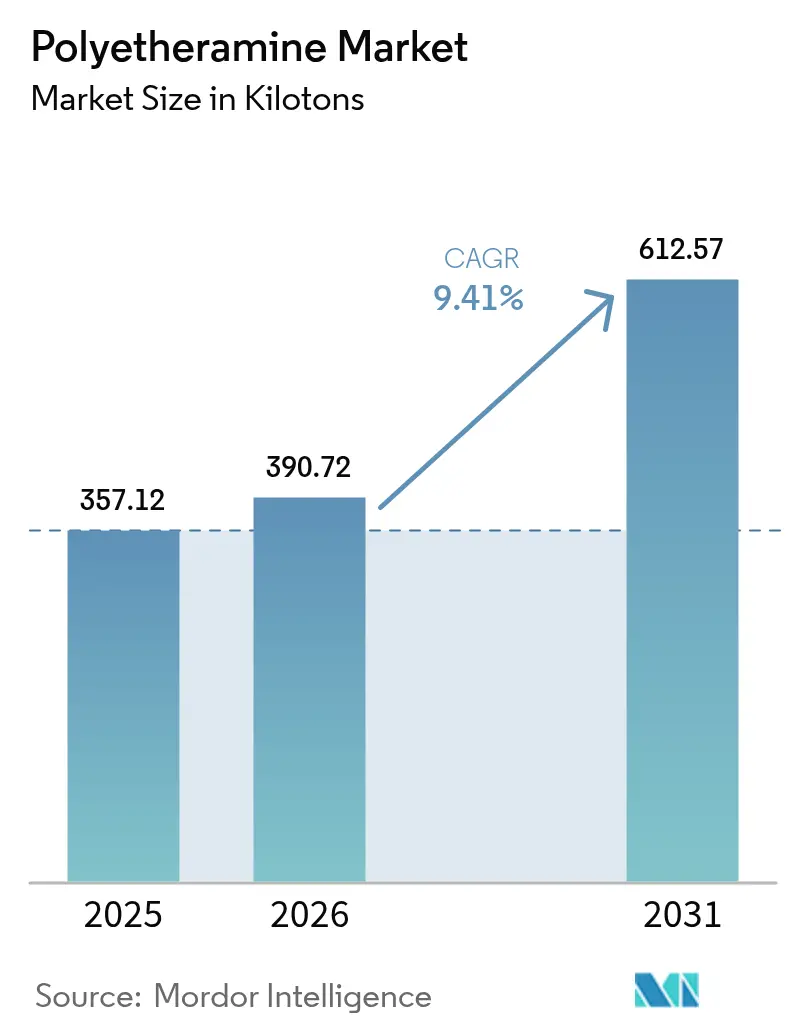

| Market Volume (2026) | 390.72 kilotons |

| Market Volume (2031) | 612.57 kilotons |

| Growth Rate (2026 - 2031) | 9.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyetheramine Market Analysis by Mordor Intelligence

The Polyetheramine Market size was valued at 357.12 kilotons in 2025 and is estimated to grow from 390.72 kilotons in 2026 to reach 612.57 kilotons by 2031, at a CAGR of 9.41% during the forecast period (2026-2031). Consistent demand from wind-energy composites, greater use in rapid-cure polyurea coatings, and aggressive upstream integration in Asia keep the polyetheramine market on a strong upward trajectory. Capacity additions by BASF and Wanhua Chemical, both backed by renewable-power transitions or captive ethylene-oxide feedstocks, lower variable costs and reinforce global supply security. Turbine-blade OEMs are qualifying recyclable amine chemistries, which extend service life while meeting emerging extended-producer-responsibility laws. At the same time, tightened ethylene-oxide emission caps in the United States and Europe are nudging producers toward closed-loop operations that further decarbonize the overall polyetheramine market value chain.

Key Report Takeaways

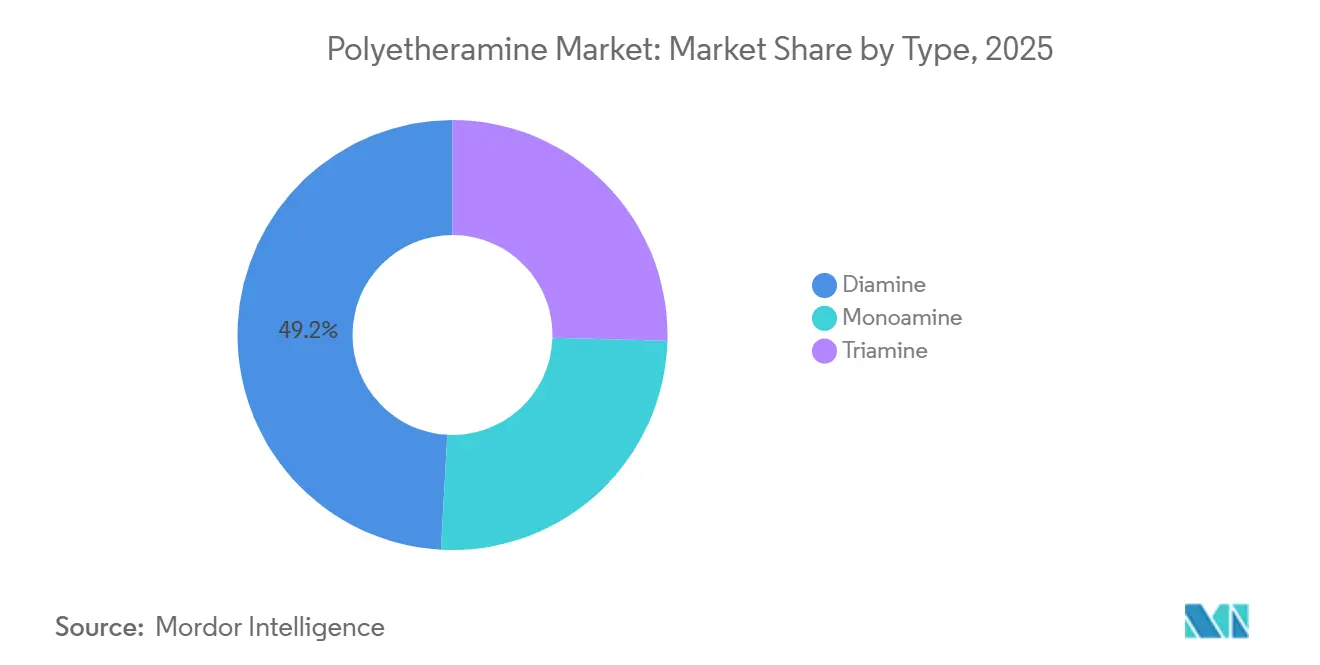

- By type, diamine held 49.15% of polyetheramine market share in 2025 and is forecast to grow at a 9.91% CAGR through 2031.

- By application, composites commanded 45.72% of the polyetheramine market size in 2025 and are advancing at a 10.95% CAGR to 2031.

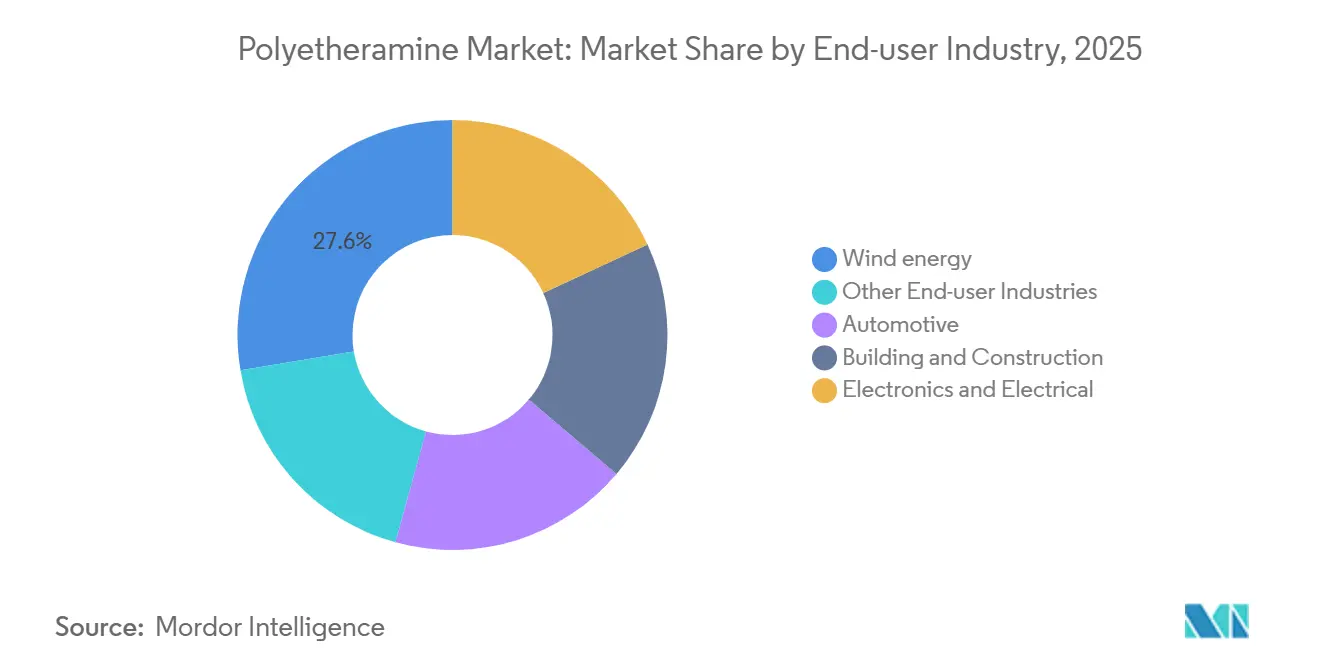

- By end-user industry, wind-energy industry accounted for 27.63% of the polyetheramine market share in 2025 and will post a 10.56% CAGR through 2031.

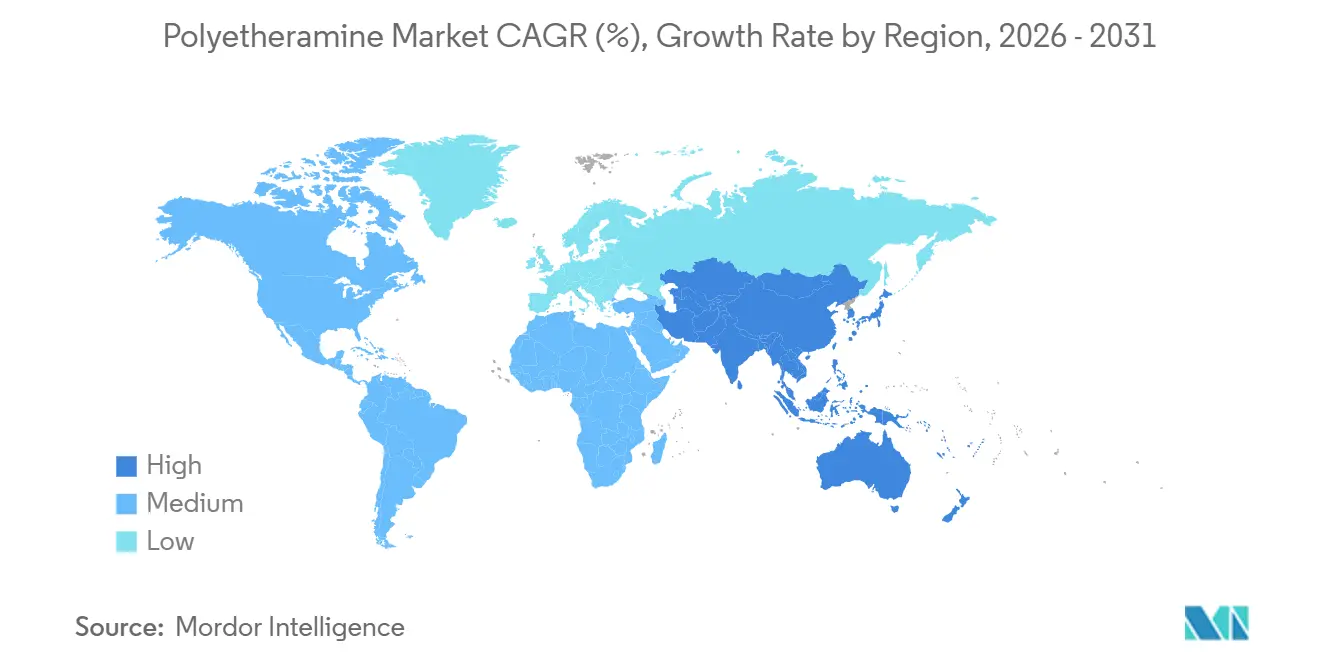

- By geography, Asia-Pacific contributed 53.55% of the polyetheramine market share in 2025 and is expanding at a 10.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyetheramine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing investments in adhesives and sealants industry | +1.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2–4 years) |

| Growing demand from composites manufacturing | +2.5% | Global, led by Asia-Pacific and Europe (offshore wind hubs) | Long term (≥4 years) |

| Expansion of wind-turbine blade production | +2.3% | Asia-Pacific, Europe, North America (offshore installations) | Long term (≥4 years) |

| Surge in high-performance polyurea protective coatings | +1.4% | North America, Middle-East and Africa (infrastructure projects) | Medium term (2–4 years) |

| Adoption in 3D-printing–grade epoxy systems | +1.1% | North America, Europe (aerospace and tooling applications) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing Investments in Adhesives and Sealants Industry

Automotive electrification is redirecting bonding technologies toward flexible, peel-resistant two-component epoxies cured with diamine modifiers. BASF reported that over half of its Materials-segment revenue now ties to polyurethane and related amine chains, with a target USD 800 million EBITDA uplift by 2028 via specialty polyols and polyetheramine upgrades. Chinese output of polyether polyol, the primary feedstock for diamines, rose 15.91% year-over-year in 1H 2024 as Wanhua and Longhua completed debottlenecks. Automated battery-pack lines prefer low-viscosity diamines that dispense in less than 60 seconds, trimming total vehicle weight by 5–8%. Consequently, the polyetheramine market is receiving a double boost from both lightweighting and throughput efficiency.

Growing Demand from Composites Manufacturing

Offshore-wind blades must endure more than10,000 cyclic loads, and lab work by the National Renewable Energy Laboratory confirmed epoxy-foam joints cured with polyetheramine exceeded 13 MPa, triple the strength of thermoplastic rivals. Recyclamine technology from Aditya Birla embeds cleavable bonds enabling acetic-acid solvolysis at 70–100 °C, aligning blade manufacturers with EU circular-economy requirements without re-tooling molds. Siemens Gamesa already commercialized these blades at Kaskasi, Sofia, and Dogger Bank wind farms. Such successes are expected to keep the polyetheramine market firmly embedded in composite value chains even as alternative matrices emerge.

Expansion of Wind-Turbine Blade Production

Rotor diameters topping 240 m necessitate more than 100 m spars; vacuum infusion over that span requires gel times more than 90 minutes, a property readily tuned with difunctional polyetheramines. Wanhua Chemical’s 40 ktpa unit, integrated into its 1.2 Mtpa ethylene complex, supplies Chinese OEMs that build 60% of global blades. Competitive pricing from such captive integration ensures the polyetheramine market keeps pace with record turbine order books destined for Asia-Pacific coastal arrays.

Surge in High-Performance Polyurea Protective Coatings

Rapid-set polyurea elastomers applied to bridges, pipelines, and armored vehicles now rely on diamine extenders that permit sub-5-second gel while delivering 3,000 psi tensile strength. The U.S. Department of Defense procures amine-extended liners to mitigate blast-wave energy in concrete structures. Middle-Eastern infrastructure adopts UV-stable polyurea topcoats, and formulators tout 20% spray-temperature energy savings versus classic polyurethane routes. These production realities support lasting growth of the polyetheramine market across civil-engineering segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns over amine emissions | −1.2% | Global, with stringent enforcement in Europe and North America | Medium term (2–4 years) |

| Slow approval for food-contact adhesive grades | −0.8% | Europe, North America (FDA and EFSA jurisdictions) | Long term (≥4 years) |

| Emerging substitution threat from bio-based amine alternatives | −0.6% | Europe, North America (renewable-carbon mandates) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns Over Amine Emissions

New U.S. EPA rules force ethylene-oxide vents at polyether-polyol plants to hit 99.9% destruction or ≤1 ppm v/v outlet levels, with weekly heat-exchanger checks and swift repairs[1]U.S. Environmental Protection Agency, “Proposed Rule for Polyether Polyols Production,” epa.gov . Compliance is estimated at USD 18.7 million a year across 21 sites, prompting some operators to pause expansion plans. Europe pursues similar zero-discharge goals, and worker-safety dossiers at ECHA flag corrosivity that necessitates closed transfer systems. BASF pre-emptively shifted its Nanjing complex to 100% renewable power, slicing 9,800 tons CO₂ per year. These requirements tighten margins yet also favor incumbents able to invest, thereby consolidating the polyetheramine market around larger, greener operators.

Slow Approval for Food-Contact Adhesive Grades

EFSA now permits 2,2′-oxydiethylamine at ≤14 wt% in thin polyamide films but caps monomer migration at 0.05 mg kg−1 and oligomers at 5 mg kg−1, forcing retesting under water up to 60 °C instead of ethanol simulants[2]European Food Safety Authority, “Safety Assessment of 2,2′-Oxydiethylamine,” efsa.europa.eu . FDA retains narrow clearances restricted to reverse-osmosis membranes alone. Lengthy dossiers and renewed toxicology setbacks delay broader adhesive rollouts and shave an estimated 5–10% from prospective demand, tempering the polyetheramine market outlook in food-contact packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Diamine Grades Drive Controlled Reactivity

The diamine captured 49.15% of the polyetheramine market share in 2025 and is tracking a 9.91% CAGR to 2031. This branch of the polyetheramine industry satisfies epoxy, polyurea, and recyclable-blade formulations thanks to balanced molecular-weight options from 400 g/mol rigids to 4,000 g/mol flexibles. Monoamines lag as surfactant players pivot to bio-based alternatives, while triamines find niche favor in thick root-joint lay-ups for 100 m blades.

The diamine cohort benefits from integrated feedstock economics. Wanhua connects its new 40 ktpa unit directly to propylene-oxide streams, undercutting Western FOB prices by 15–20%. BASF’s Lupragen catalysts address regulatory VOC drives, offering drop-in substitutions at identical curing windows. With epoxy formulators standardizing on recycled-ready systems, diamines featuring cleavable backbones may soon outpace total polyetheramine market averages.

By Application: Composites Uptake Outruns Every Peer

Composites consumed 45.72% of the polyetheramine market share in 2025 and will accelerate at a 10.95% CAGR through 2031 on offshore-wind builds longer than a soccer field. Polyetheramine curing balances 90-minute gel times with ambient-temperature post-cure, ideal for vacuum infusion of giant spars. Polyurea follows, vaulted by infrastructure rehab tasks requiring sub-5-second set times and 3,000 psi strength. Fuel-additive volumes stagnate as diesel sales fade, shrinking that portion of the polyetheramine market size even while adhesives gain from EV battery adhesive requirements. Recyclamine breakthroughs keep epoxy composites squarely dependent on diamines, ensuring the polyetheramine market remains central to circular-blade strategies.

Polyurea’s climb mirrors GCC and U.S. bridge rehabilitation programs. Its 100%-solids recipe using diamines eliminates volatile solvents, aligning with stricter VOC caps. Meanwhile, 3D-printing epoxy resins adopt triamines that slash cure cycles, thereby pushing triamine channel growth.

By End-user Industry: Wind Energy Sets the Pace

Wind energy held 27.63% of of the polyetheramine market share in 2025 and will post a 10.56% CAGR to 2031 as gigawatt-scale offshore projects lock in recyclable blade contracts. Automotive electrification buffs adhesive demand, though legacy fuel-additive use wanes. Construction specifies polyurea membranes for rapid waterproofing, and electronics OEMs prefer low-viscosity diamines for automated under-fill dispense. The polyetheramine market thus enjoys portfolio insulation, with wind and EV batteries offsetting any attrition elsewhere.

Asia supplies ≥60% of global blades; China’s ISO 14001 cleared producers like Sinoma adopt Wanhua’s integrated diamines, confirming regional feedstock sovereignty. Automotive OEMs in Mexico and the U.S. introduce battery-bonding diamines, further diversifying the polyetheramine industry revenue mix. These cross-sector cushions temper cyclic risk and sustain long-run polyetheramine market stability.

Geography Analysis

Asia-Pacific dominated the polyetheramine market with 53.55% of 2025 volume and is locked into a 10.12% CAGR through 2031. Chinese capacity expansions Wanhua’s 40 ktpa and Longhua’s parallel 40 ktpa lines grant captive ethylene-oxide economics, while India qualifies aerospace prepregs running amine-cured out-of-autoclave cycles. Japan supports high-purity electrolyte potting compounds, and South Korea’s yards use polyurea cargo-tank coatings. Collectively, these national programs anchor near-term growth trajectories for the polyetheramine market across the region.

North America follows as infrastructure spending under the Inflation Reduction Act boosts epoxy-based wind-tower fabrication. BASF’s Geismar output now services U.S. offshore projects from Maine to Texas, with added low-VOC Baxxodur capacity delivering premium blends. Yet stricter EPA ethylene-oxide rules could squeeze upstream availability and nudge the polyetheramine industry toward more import reliance.

Europe retains a sizable post-Brexit share built on North Sea wind hubs and stringent circular-economy directives. Siemens Gamesa’s recyclamine blades prove viable at Kaskasi and Dogger Bank, locking in long-term diamine demand. EFSA’s narrow migration limits slow food-contact upgrades, yet Europe’s decarbonization arc prompts broader substitution of solvent-borne resins with amine-cured systems, preserving momentum in the polyetheramine market.

South America and the Middle-East and Africa collectively contribute a smaller slice, but Brazil’s turbine OEMs and Saudi Arabia’s mega-construction pipeline spur robust local uptake of polyurea and epoxy-composite solutions. Both regions represent future-option territories for producers looking to widen the polyetheramine market footprint during the next planning cycle.

Competitive Landscape

The top five suppliers, including BASF, Huntsman, Evonik, Yangzhou Chenhua New Material Co., Ltd., and Clariant, held roughly 85% of installed nameplate capacity in 2025, signaling high concentration. Chinese entrants like Longhua seize price points by integrating propylene-oxide streams and tapping low-cost renewable power. Western majors focus on Scope 3 reduction, VOC-free formulations, and cleavable chemistries to defend margins. BASF transitioned its Nanjing plant to 100% renewable electricity, trimming 9,800 tCO₂ each year, while Wanhua undercuts delivered costs by 15–20% via its captive 1.2 Mtpa ethylene cracker.

Strategic moves include BASF’s USD 780 million Geismar expansion finishing in 2026 to reach 600 ktpa MDI plus aligned diamine catalysts, and Wanhua’s roll-out of integrated amine-polyol packages. Aditya Birla’s recyclamine patents create substitution risk for legacy hardeners, but they also open high-margin niches where incumbents can license or co-develop. Digital twins and AI-enabled process control emerge as competitive levers; BASF’s intelligent factory modules reduce off-spec batches, while Wanhua’s real-time EO monitoring lowers emissions and compliance costs. Collectively, these tactics underscore an increasingly technology-driven polyetheramine market.

Polyetheramine Industry Leaders

BASF

Evonik Industries AG

Huntsman International LLC

Yangzhou Chenhua New Material Co., Ltd.

CLARIANT

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BASF expanded its plants, increasing polyetheramine production capacity by approximately 25%. This reinforced BASF's position in high-performance amine solutions.

- February 2025: Huntsman International LLC showcased JEFFAMINE EDR-148, a newly developed polyetheramine designed for epoxy resin curing, at the European Coatings Show. This polyetheramine enhanced crosslinking speed while improving flexibility and toughness.

Global Polyetheramine Market Report Scope

Polyetheramines, a class of aliphatic organic compounds, are characterized by the presence of both ether and amine groups. Primarily, polyetheramines serve as curing agents. These amines play a crucial role in augmenting the properties of end products, imparting qualities like flexibility, hydrophobicity, hydrophilicity, and toughness.

The polyetheramine market is segmented by type, application, end-user industry, and geography. By type, the market is segmented into diamine, monoamine, and triamine. By application, the market is segmented into composites, polyurea, fuel additives, epoxy coatings, adhesives and sealants, and other applications. By end-user industry, the market is segmented into wind energy, automotive, building and construction, electronics and electrical, and other end-user industries. The report also covers the market size and forecasts for polyetheramine in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Diamine |

| Monoamine |

| Triamine |

| Composites |

| Polyurea |

| Fuel Additives |

| Epoxy Coatings |

| Adhesives and Sealants |

| Other Applications |

| Wind energy |

| Automotive |

| Building and Construction |

| Electronics and Electrical |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Diamine | |

| Monoamine | ||

| Triamine | ||

| By Application | Composites | |

| Polyurea | ||

| Fuel Additives | ||

| Epoxy Coatings | ||

| Adhesives and Sealants | ||

| Other Applications | ||

| By End-user Industry | Wind energy | |

| Automotive | ||

| Building and Construction | ||

| Electronics and Electrical | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the polyetheramine market?

The polyetheramine market stands at 390.72 kilotons in 2026 and is projected to reach 612.57 kilotons by 2031, reflecting a 9.41% CAGR from 2026 to 2031.

Which application will add the most incremental demand from 2026 to 2031?

Composites are expanding at the fastest 10.95% CAGR from 2026 to 2031.

What makes diamine dominant in 2025?

The bifunctional reactivity of diamine offers balanced crosslink density, resulting in 49.15% of polyetheramine market share in 2025.

How will new U.S. EPA rules influence the market?

Mandatory 99.9% ethylene-oxide destruction may elevate compliance costs, favoring capital-rich producers and slightly tightening near-term supply.

Page last updated on: