Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Polyolefin Powder Report is Segmented by Polymer Type (Polyethylene Powder, Polypropylene Powder, and Ethyl Vinyl Acetate Powder), Particle Size (less Than 100 Μm, 100 To 500 Μm, Greater Than 500 Μm), Application (Rotational Molding, Masterbatch, and Other Applications), End-User Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

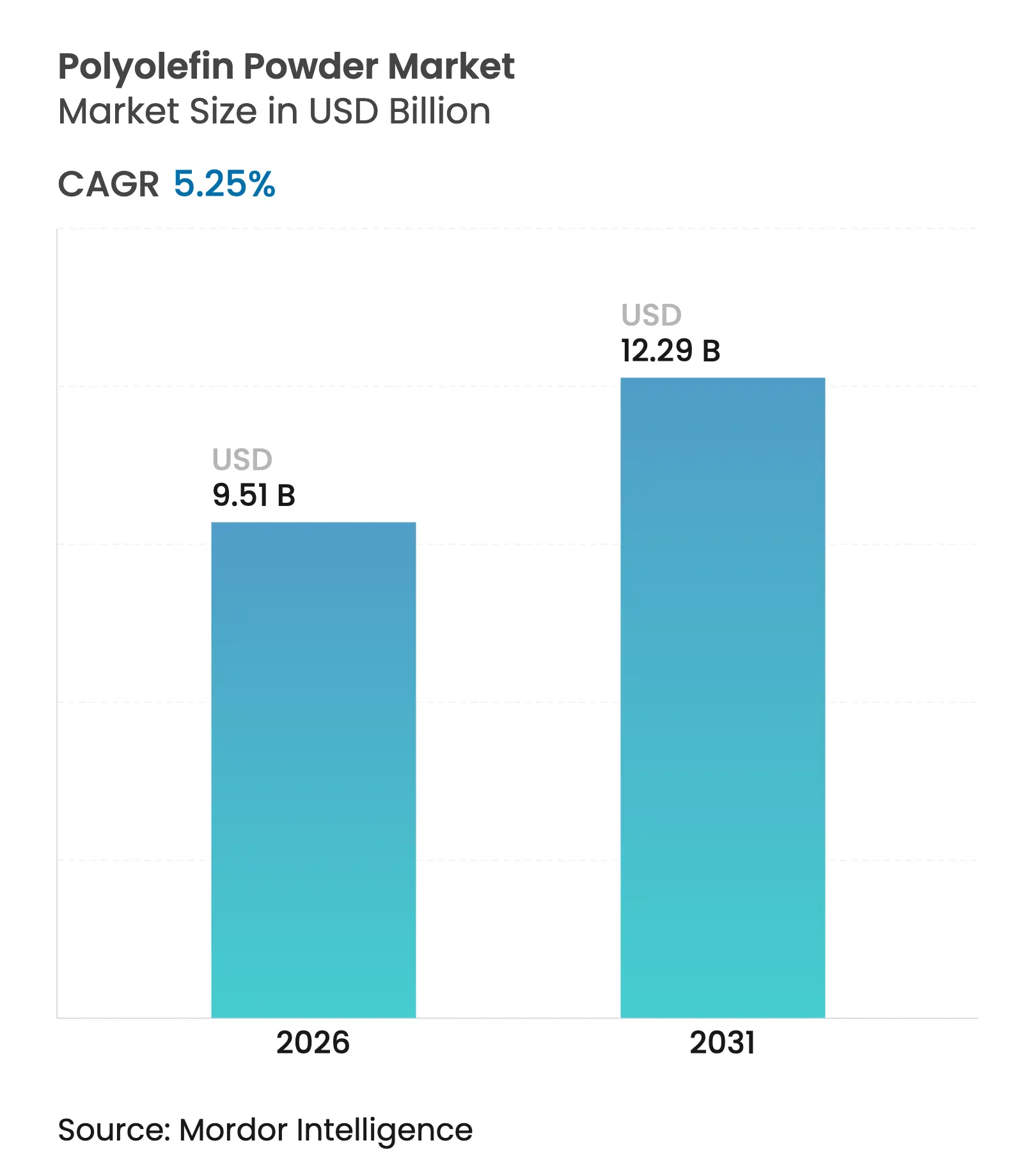

| Market Size (2026) | USD 9.51 Billion |

| Market Size (2031) | USD 12.29 Billion |

| Growth Rate (2026 - 2031) | 5.25 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Polyolefin Powder market size in 2026 is estimated at USD 9.51 billion, growing from 2025 value of USD 9.04 billion with 2031 projections showing USD 12.29 billion, growing at 5.25% CAGR over 2026-2031. This growth profile demonstrates the material’s continued relevance to lightweighting strategies, cost-sensitive production runs, and sustainability-driven innovations across multiple industrial value chains. Polyethylene and polypropylene powders combine easy melt processing, broad chemical resistance, and reliable supply, enabling efficient rotational molding, masterbatch compounding, and functional coating operations. Strong capital inflows into Asia-Pacific petrochemical complexes, widening adoption of electric vehicles that favor lightweight plastics, and rapid scaling of solar module encapsulation lines sustain demand momentum. Meanwhile, additive manufacturing laboratories in North America and Europe validate polyolefin powders as cost-effective feedstocks for prototyping and short-run production, complementing established tank, container, and pipe markets. Heightened regulatory scrutiny of single-use plastics and feedstock price swings complicate planning cycles, but new battery separator, 3D-printing, and bio-based resin opportunities expand the polyolefin powder market’s addressable scope.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising rotomolding demand from tanks and large containers

Rising rotomolding demand from tanks and large containers

| +1.2% | Global, concentrated in APAC and North America | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, concentrated in APAC and North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Expanding masterbatch consumption in flexible packaging

Expanding masterbatch consumption in flexible packaging

| +0.8% | Global, led by APAC packaging hubs | Short term (≤ 2 years) | |||

Lightweighting push in automotive parts

Lightweighting push in automotive parts

| +0.9% | North America and EU, expanding to APAC | Medium term (2-4 years) | |||

Growth of 3D-printing powders for prototyping

Growth of 3D-printing powders for prototyping

| +1.1% | North America and EU innovation centers | Long term (≥ 4 years) | |||

Niche adoption in Li-ion battery separator coatings

Niche adoption in Li-ion battery separator coatings

| +0.3% | APAC battery hubs, spreading worldwide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Rotomolding Demand from Tanks and Large Containers

Industrial water, chemical storage, and agricultural infrastructure projects increasingly specify seamless, uniform-wall containers. Rotational molding provides stress-free geometries impossible to achieve economically with welded metal or multi-piece plastic assemblies. Recent advances in downer-reactor thermal rounding technology yield more spheroidal polyethylene particles, improving flow inside the mold and enhancing final surface aesthetics. Faster heat-transfer cycles reduce energy consumption and shorten takt times, lowering total cost of ownership for producers. As many emerging economies invest in rural sanitation and irrigation, regional compounders scale bespoke polyolefin grades engineered for rotomolding so that buyers can access corrosion-resistant, long-life tanks without expensive imports. Collectively, these dynamics boost mid-term volume growth in the polyolefin powder market.

Expanding Masterbatch Consumption in Flexible Packaging

Brand owners target precise shade repeatability, down-gauge film thickness, and barrier upgrades in personal care, snack, and liquid pouch formats. Uniform polyolefin powder particles act as carrier resins in high-speed masterbatch lines, giving consistent pigment dispersion and tight melt-flow control. Mitsui Chemicals’ HI-WAX micro-powders enhance color strength while maintaining food-contact compliance, enabling converters to trim resin usage yet still meet visual targets. As retailers elevate sustainability commitments, masterbatch formulations with recycled or bio-based content allow packaging lines to switch grades without altering processing windows. The resulting flexibility anchors near-term demand additions to the polyolefin powder market.

Lightweighting Push in Automotive Interior and Exterior Parts

Automakers target 150-200 kg weight cuts per vehicle, catalyzing substitution of metals and engineering plastics with advanced polyolefin blends. Electrostatic powder-coated polypropylene trim delivers Class A gloss while staying cost-competitive. ExxonMobil’s Vistamaxx modifiers deliver impact strength and low-temperature ductility so designers can specify thinner wall sections without safety trade-offs. As electric vehicle pack weights rise, every kilogram saved in cabin and exterior panels translates into extended driving range, reinforcing OEM procurement of lightweight polyolefin powder grades.

Niche Adoption in Li-ion Battery Binder/Separator Coatings

Battery makers apply ceramic-coated polypropylene separators that withstand spiking temperatures during runaway events, enhancing cell safety. Academic programs reveal three-layer PP/PP-R + SiO₂ separators outperform baseline polyolefin films by suppressing shrinkage above 130 °C[1]Journal of Power Sources, “Multi-Layer PP/SiO₂ Separator for High-Energy Lithium-Ion Batteries,” sciencedirect.com . While high-temperature chemistries explore polyphenylene sulfide alternatives, large-format energy-storage projects still specify upgraded polyolefin solutions for cost and supply reasons. Although a niche today, each gigawatt-hour of capacity adds specialized powder demand over the long term.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent single-use plastics and micro-plastics

regulations

Stringent single-use plastics and micro-plastics

regulations

| −0.7% | EU leading, expanding to North America and selective APAC markets | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

−0.7%

|

Geographic Relevance

:

EU leading, expanding to North America and selective APAC

markets

|

Impact Timeline

:

Short term (≤ 2 years)

|

Volatile ethylene/propylene feedstock prices

Volatile ethylene/propylene feedstock prices

| −0.5% | Global, pronounced where feedstock is imported | Short term (≤ 2 years) | |||

Emerging recycled polyolefin powders disrupting virgin demand Emerging recycled polyolefin powders disrupting virgin demand | -0.4% | North America and EU circular economy initiatives, expanding to APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Single-Use Plastics and Micro-Plastics Regulations

The European Union’s Single-Use Plastics Directive restricts numerous disposables, while its REACH initiative targets synthetic polymer microparticles under 5 mm. From 2025, microbead bans in cosmetics shift formulators away from polyethylene spheres, curbing short-cycle powder volumes[2]European Chemicals Agency, “Microplastics,” echa.europa.eu . In parallel, fourteen US states implement Extended Producer Responsibility fees that could reach USD 4.7 billion by 2026, effectively taxing virgin resin packaging. Regulatory momentum propels brand owners to explore compostable films or mechanically recycled grades, pressuring traditional polyolefin powder market volumes in fast-moving consumer goods.

Volatile Ethylene/Propylene Feedstock Prices

Swings in prices of propylene and ethylene squeeze in Korea and Southeast Asia integrated cracker-to-powder margins, prompting Southeast Asian operators to idle lines during troughs. In the United States, propylene glycol surpassed 40 cents/lb by mid-2025 on energy-driven cost inflation, reinforcing caution around capacity investments. Volatility complicates long-term planning in the polyolefin powder market and may delay innovation outlays.

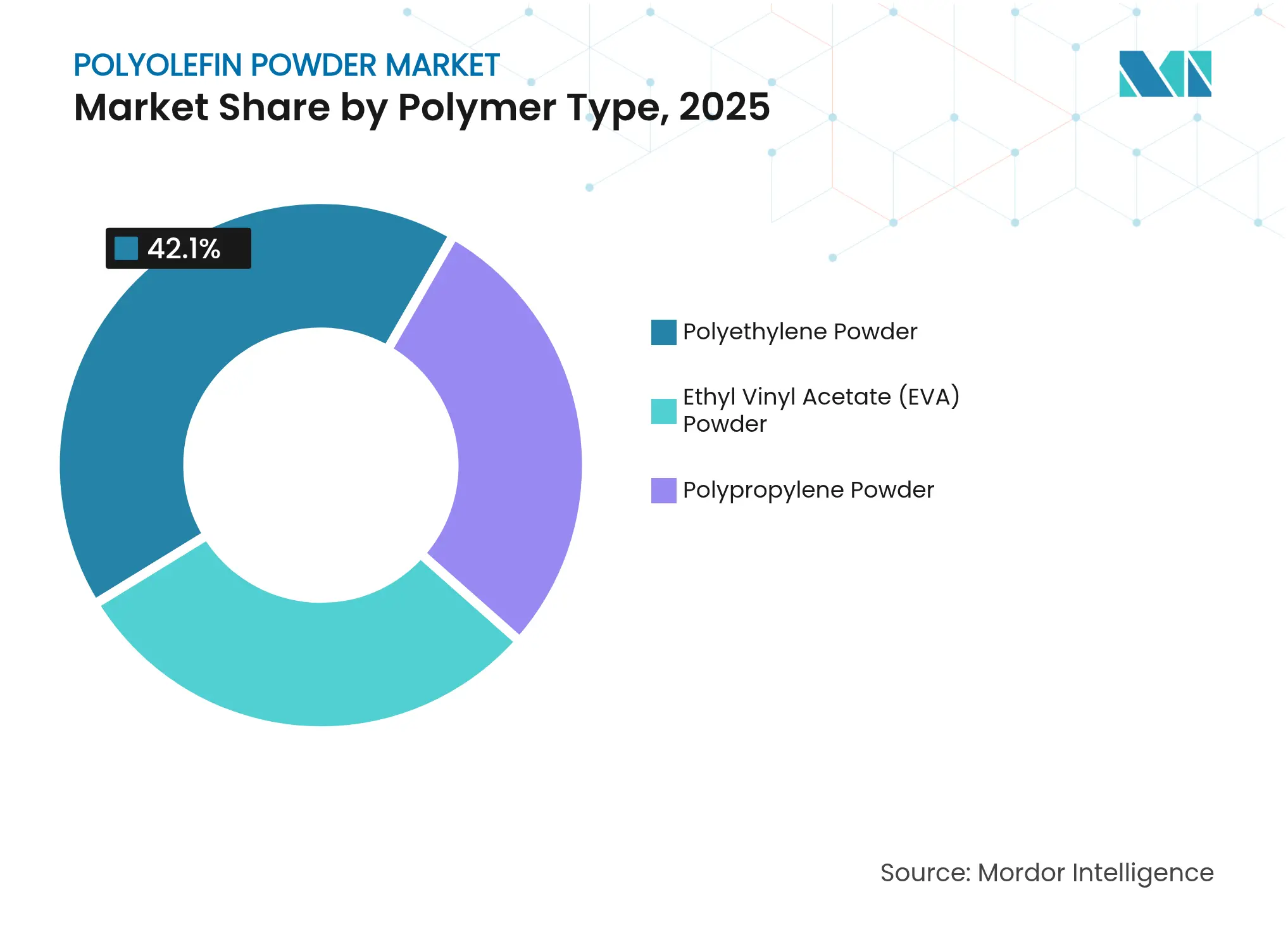

By Polymer Type: Polyethylene Leadership Faces EVA Momentum

Polyethylene powders represented 42.10% of the polyolefin powder market share in 2025, underpinned by proven performance in rotationally molded tanks, masterbatch carriers, and corrosion-resistant pipe coatings. The polyolefin powder market size for polyethylene grades is projected to expand steadily as infrastructure programs in Asia-Pacific and Africa specify lightweight, chemical-inert containers. Nevertheless, EVA powders post the fastest 5.85% CAGR through 2031, driven by encapsulant consumption in photovoltaic modules, where 18-33% vinyl acetate content delivers superior UV transparency.

EVA’s rising share does not erase polyethylene’s advantages in cost, global supply base, and recyclability pathways. Continuous-loop mechanical recycling keeps high-density polyethylene grades in tank applications competitive against steel, while low-density polyethylene remains the carrier of choice for color master-batches in retail films. In parallel, polypropylene’s high-melting-point derivatives address battery pack covers and under-hood parts that require dimensional stability. Future uptake of bio-based variants and chemically recycled feedstocks is expected to reshape polymer preferences in the polyolefin powder market.

Note: Segment shares of all individual segments available upon report purchase

By Particle Size: Fine Powders Unlock Premium Functions

Particles sized 100-500 µm captured 55.60% of 2025 revenue, balancing flowability and bulk density to suit rotational molding and electrostatic coating conveyors. This band remains the workhorse of the polyolefin powder market because it eliminates bridging in hoppers, ensures complete mold coverage, and offers predictable sintering rates.

Meanwhile, market demand for powders below 100 µm posts a 6.08% CAGR, anchored in automotive clear-top coatings and emerging laser-sintering printers that require narrow spreads for consistent layer thickness. Comparative lab work showed 15 µm polyethylene particles generate smoother automotive finishes than traditional 100 µm grades, enabling thinner protective skins that cut paint stack costs.

By Application: Rotational Molding Retains Core, Coatings Rise

Rotational molding held 26.70% of global revenue in 2025 thanks to its ability to produce seamless, thick-walled tanks, playground equipment, and marine buoys without expensive tooling. Developers of agricultural water storage in sub-Saharan regions routinely specify rotationally molded high-density polyethylene tanks for their 20-year service life and UV stabilizer packages.

However, electrostatic spray and fluidized bed coating use records the highest 5.95% CAGR as automakers, appliance makers, and pipeline contractors transition from solvent-borne paints to zero-VOC powder alternatives. ChemPoint reports transfer efficiencies approaching 100%, minimizing waste, and the ability to build 250-500 µm protective films in minutes.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

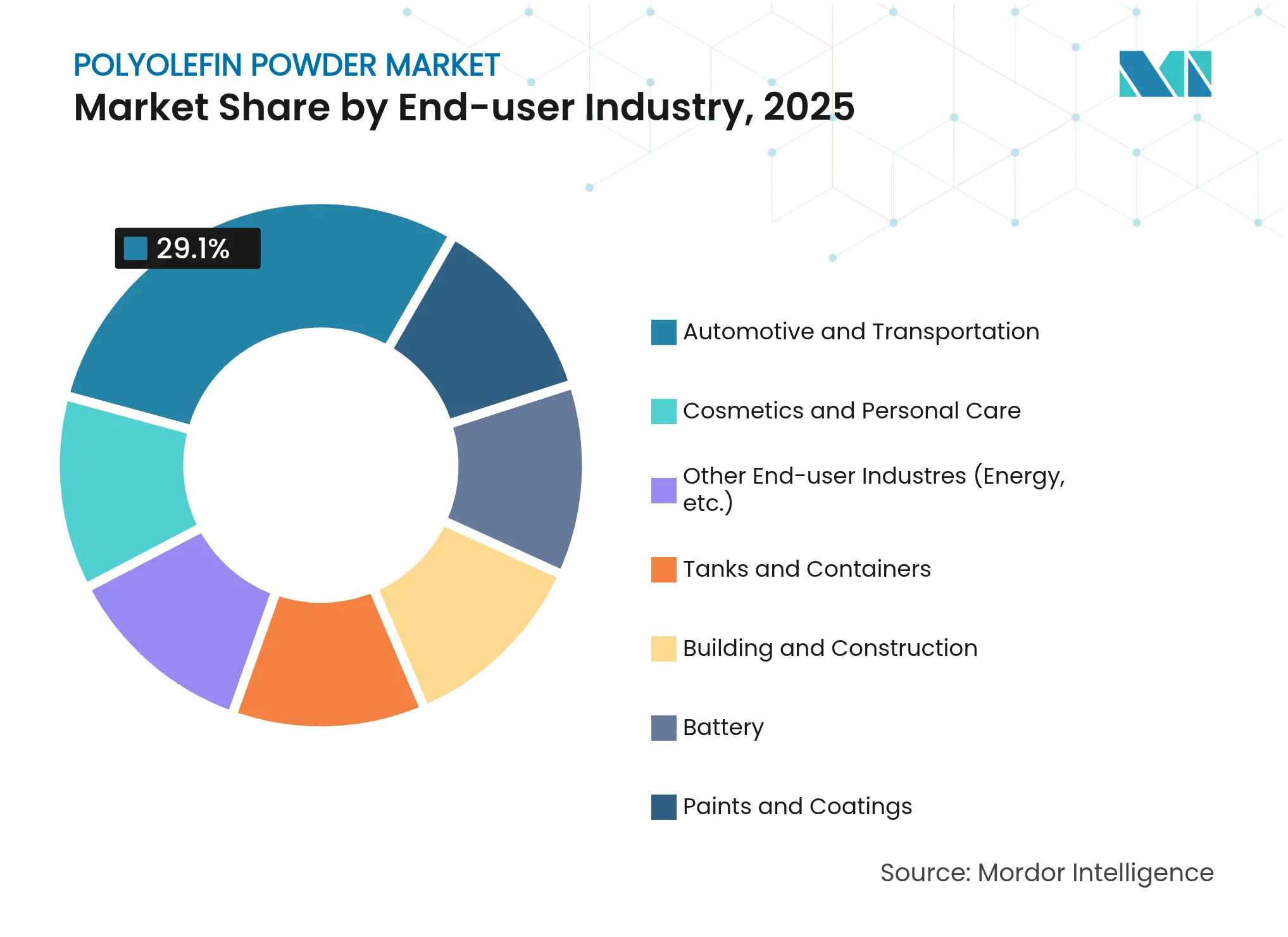

By End-User Industry: Automotive Dominates but Diversification Accelerates

Automotive commanded 29.10% of 2025 sales, propelled by interior panels, bumper skins, and underbody shields that exploit powder-coated polypropylene for corrosion protection and design flexibility. Each lightweight component contributes to fleetwide fuel-economy targets, while EV platforms appreciate mass savings that offset battery weight. The polyolefin powder market size aligned to automotive is forecast to keep pace as electrification expands and range anxiety keeps pressure on curb weights. Building and construction follow, leveraging weather-resistant coatings on guard rails, cladding, and pipeline insulation.

Battery manufacturing emerges as a notable new arena. Ceramic-coated polypropylene separators and binder blends enhance safety and energy density, moving specialized powders into gigafactory supply chains. Tanks and containers, paintings and coatings, and cosmetics together make up the “other industries” basket that records the fastest 5.98% CAGR, owing to 3D-printing prototypes, sports gear shells, and exfoliating microspheres in personal care creams. This diversification strategy shields producers from cyclicality in any single sector, underscoring the resilience of the polyolefin powder market.

Note: Segment shares of all individual segments available upon report purchase

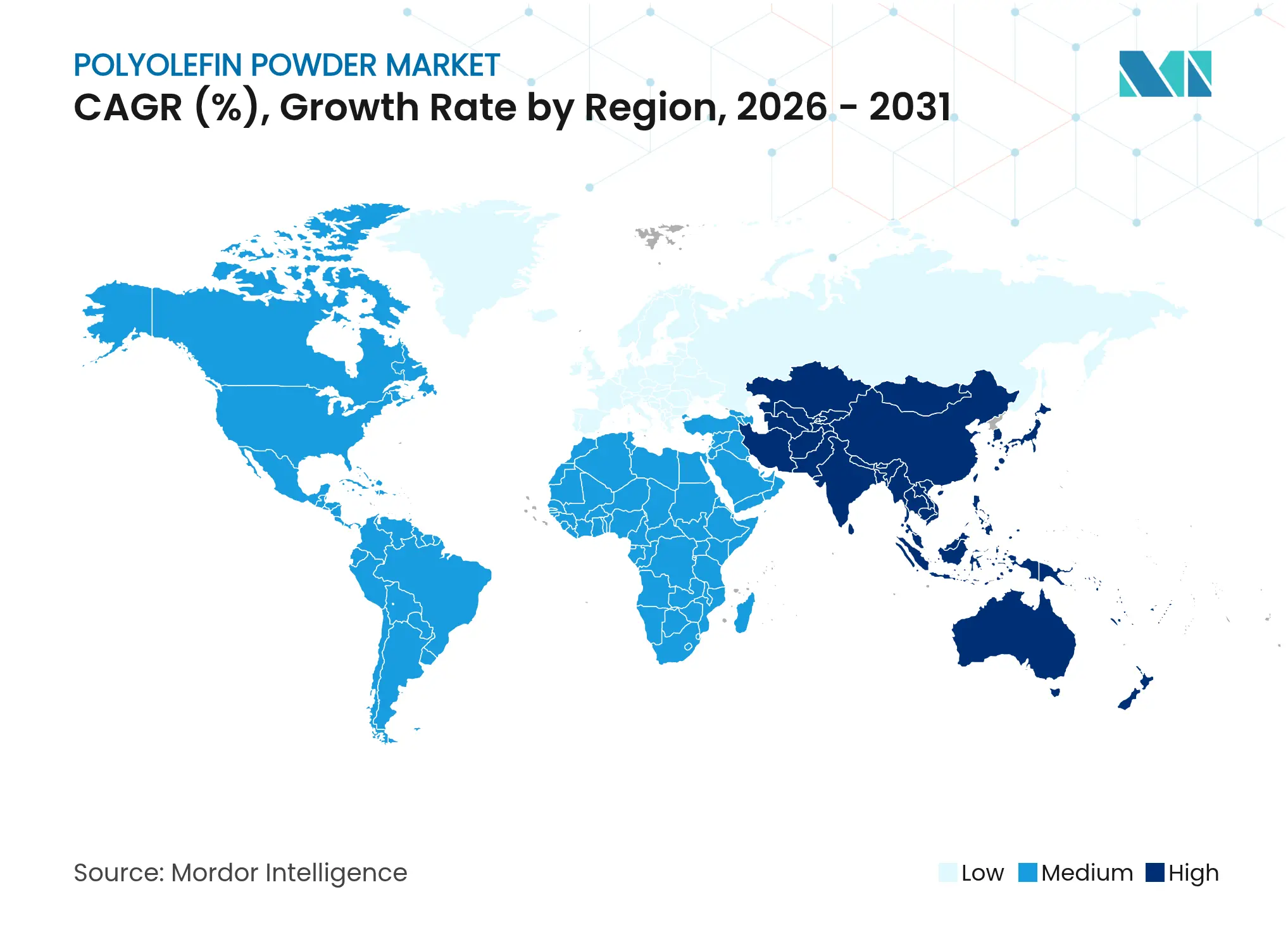

Asia-Pacific safeguarded 39.00% of global revenue in 2025 and is on track for 5.78% CAGR through 2031. National oil companies extend cracker networks that back-integrate into powder lines, ensuring secure feedstock and export readiness. China’s multi-billion-dollar petchem hubs, including SABIC’s Fujian complex, position domestic converters near raw materials and port logistics.

North America maintains steady growth as research and development centers refine additive manufacturing, automotive lightweighting, and high-value coatings. Europe advances a sustainability-centric agenda, with chemical recyclate incorporation and bio-feedstock adoption differentiating local suppliers. Regulatory constraints such as the EU plastics levy accelerate substitution toward recycled grades, adding complexity but also premium opportunities in the polyolefin powder market. South America and the Middle East, and Africa together contribute a smaller base yet exhibit above-average growth as infrastructure developments stimulate tank and pipe demand.

Market Concentration

The polyolefin powder market demonstrates moderate fragmentation, with integrated majors retaining cost advantages through feedstock ownership, global plant footprints, and technical support networks. Technology differentiation centers on particle size tuning, custom additive packages, and proprietary coating processes. Patent activity surrounding electrostatic fluidized bed deposition indicates continuing barriers to entry; Google Patents lists formulations that optimize powder charge density to increase deposition rates. Start-ups targeting chemically recycled or mass-balanced portfolio offerings challenge incumbents to match sustainability credentials. Overall, buyers balance security of supply, technical service, and carbon-intensity credentials when selecting partners, reinforcing a competitive yet innovation-driven environment within the polyolefin powder market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The report on the polyolefin powder market includes:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.