North America Polyamide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

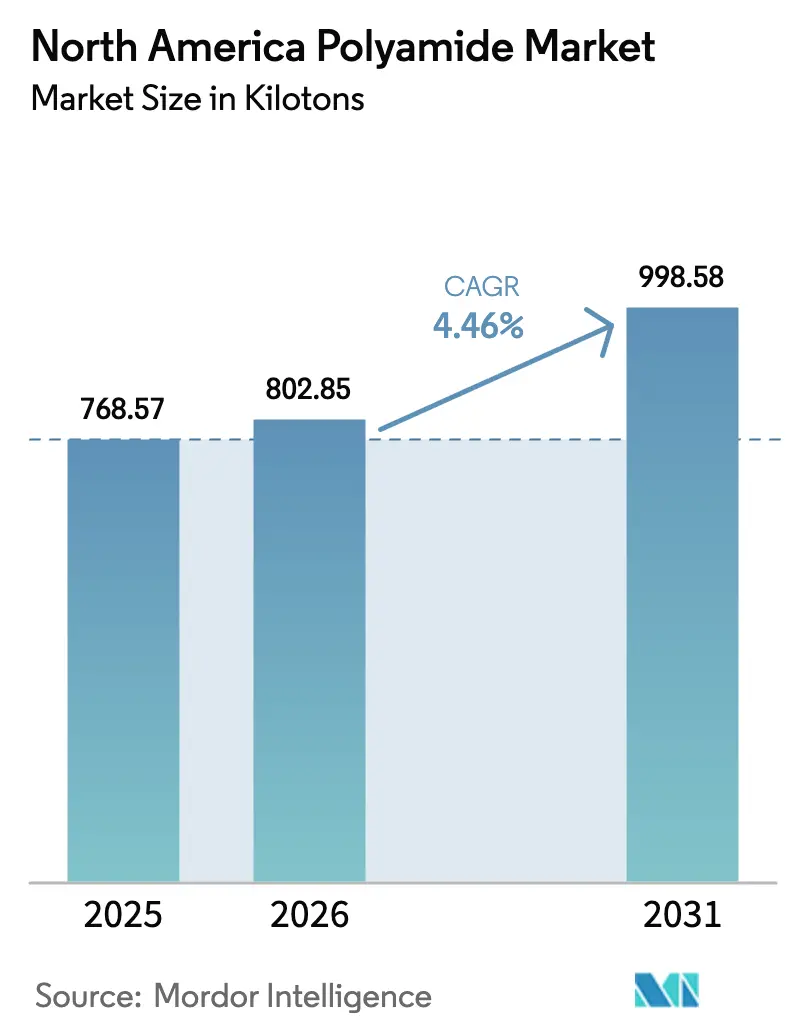

| Base Year Market Size (2025) | 768.57 kilotons |

| Market Volume (2026) | 802.85 kilotons |

| Market Volume (2031) | 998.58 kilotons |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

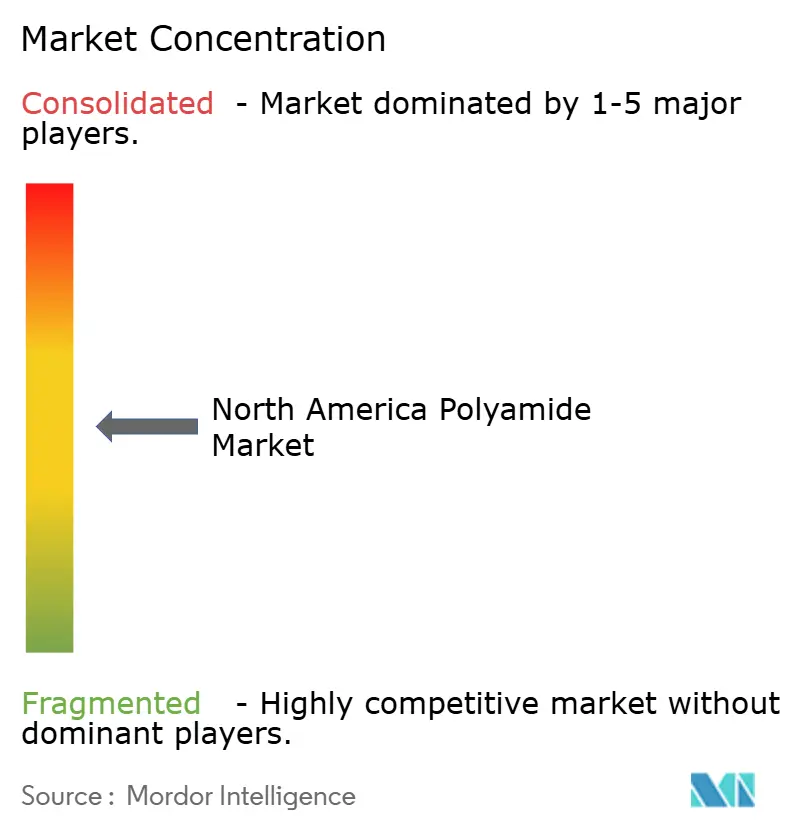

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Polyamide Market Analysis by Mordor Intelligence

The North America Polyamide Market size is expected to grow from 768.57 kilotons in 2025 to 802.85 kilotons in 2026 and is forecast to reach 998.58 kilotons by 2031 at 4.46% CAGR over 2026-2031. Growth reflects a mature yet adaptive industrial base that is absorbing demand shifts tied to electric-vehicle production, aerospace recovery, and supply-chain regionalization. Structural weight-reduction targets are amplifying polymer substitution in vehicles, while data-center expansion and 5G roll-outs are boosting high-temperature grades for connectors and circuit components. At the same time, recycled-content mandates are nudging compounders toward circular feedstocks, and localized feedstock investments are easing logistics bottlenecks. Volatile prices for caprolactam and hexamethylenediamine still pose margin risk, but greater vertical integration and multi-year offtake contracts are tempering cost swings.

Key Report Takeaways

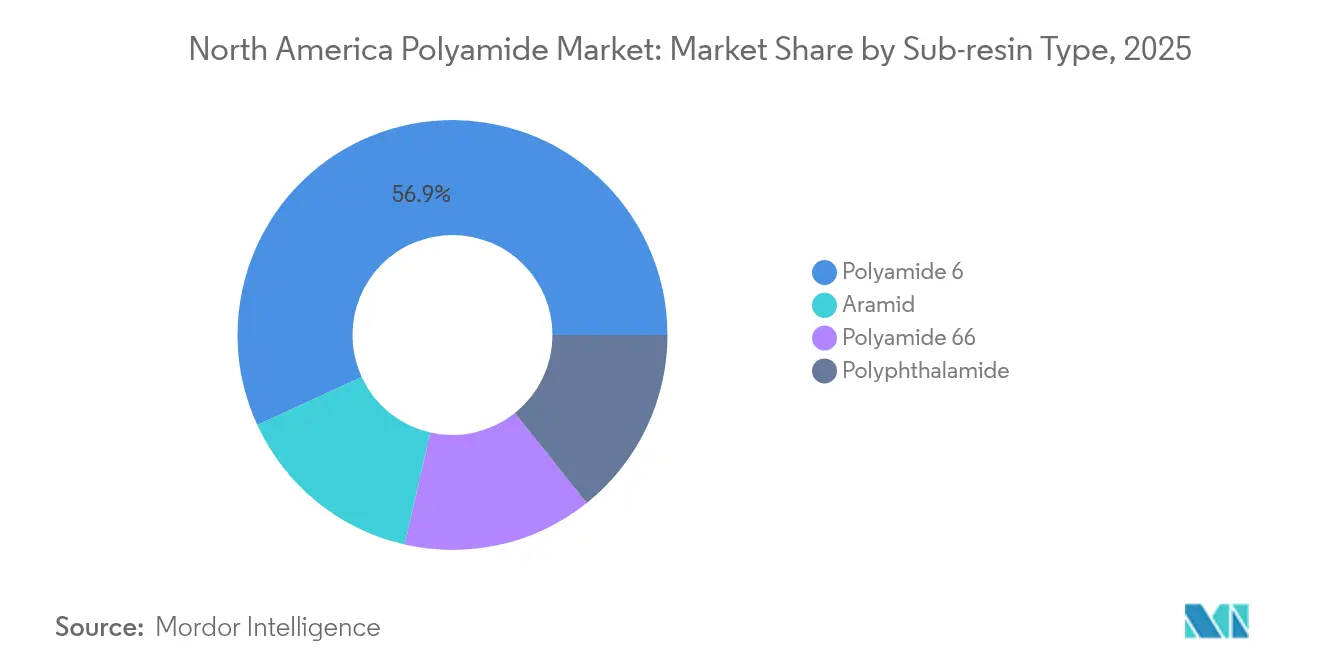

- By sub-resin type, polyamide 6 led with 56.88% of the North America polyamide market share in 2025, whereas aramid fibers are forecast to expand at a 5.44% CAGR through 2031.

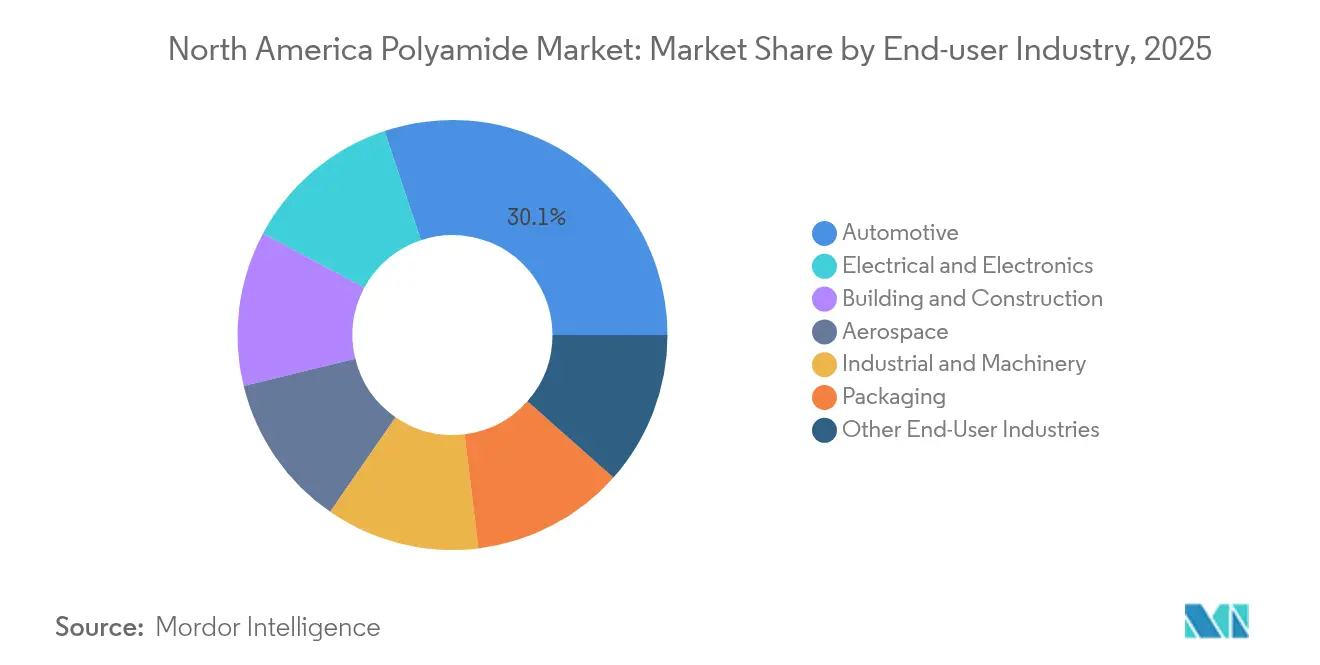

- By end-user industry, automotive held 30.12% of the North America polyamide market size in 2025, while electrical and electronics is projected to advance at a 6.93% CAGR to 2031.

- By geography, the United States contributed a dominant 77.85% share of the North America polyamide market in 2025 and Mexico is poised for the quickest 6.02% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Polyamide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting push | +1.0% | United States and Mexico automotive corridors | Medium term (2-4 years) |

| High-temperature e-mobility connectors | +0.8% | Michigan, Ontario, Northern Mexico | Short term (≤ 2 years) |

| On-shoring of performance-polymer supply | +0.9% | U.S. Gulf Coast, Midwest, Mexican Bajío | Long term (≥ 4 years) |

| OEM recycled-content mandates | +0.7% | Continental North America with EU spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Automotive Lightweighting Push

OEM weight-reduction programs are accelerating polyamide uptake because lighter vehicles translate directly into fuel-economy gains and longer electric-vehicle range. The American Chemistry Council recorded nylon usage of 45 lb per light vehicle in 2024 and signaled rising adoption for engine covers, battery housings, and structural brackets[1]American Chemistry Council, “Chemistry and Light-Vehicle Outlook 2024,” americanchemistry.com. LANXESS commercialized new PA6 grades for electric-vehicle thermal-management modules that displace PA66 where processing latitude and cost advantages offset marginal heat resistance. Automakers also value the design freedom that injection-molded polyamides provide relative to stamped metals, enabling part consolidation and lower tooling costs. With major platforms now engineered for battery integration, compounders that supply flame-retardant and thermally conductive PA grades are securing multi-year nominations. These dynamics establish a resilient demand floor for the North America polyamide market even if cyclical vehicle production softens.

Surging Demand for High-Temperature E-Mobility Connectors

Rapid charger rollout, on-board 800-V architectures, and tighter under-hood packaging are driving demand for materials that retain dimensional stability above 200 °C while insulating high-voltage circuits. BASF’s polyphthalamide launch targets molded connector housings that must endure thermal shock, dielectric stress, and exposure to glycol-based coolants. INVISTA redirected its Camden, South Carolina line from staple fiber to polymer chips specifically aimed at e-mobility connectors, reflecting the higher value capture in specialty grades. Similar specifications surface in data-center cooling manifolds and wind-turbine inverters, broadening the addressable market. As OEM design cycles compress, compounders offering simulation support and UL yellow-card certifications are winning design-in positions, fueling the near-term lift to the North America polyamide market.

On-shoring of Performance-Polymer Supply Chains

Supply-chain shocks in 2022-2023 motivated resin users to shorten logistics lanes and insure against Asia-centric sourcing. Mexico secured USD 43.9 billion of foreign direct investment in 2023, including USD 8.5 billion tied directly to integrated automotive supply chains that rely on regional polyamide compounders. U.S. Gulf Coast expansions dovetail with abundant shale-derived benzene and propylene feedstocks, anchoring competitive monomer positions. These projects collectively raise self-sufficiency, lower lead-times, and reinforce the long-run competitiveness of the North America polyamide market.

OEM Recycled-Content Mandates

Automakers now mandate minimum recycled content in specified resin families, spurring investment in chemical depolymerization and mechanical reclaim. DOMO Chemicals is committed to 20% circular or bio-based polyamide volumes by 2030 and is scaling ISCC+-certified operations across North American assets. Asahi Kasei’s partnership with Aquafil to trial recycled PA6 filament for 3-D printing prototypes demonstrates early convergence of additive manufacturing and circular materials. Heightened audit requirements push compounders to trace bale-to-pellet certifications, driving digital ledger adoption. While post-industrial regrind remains the primary recycled feed, pilot plant success in depolymerizing end-of-life carpets and airbags could provide incremental tonnage by 2027. These developments enlarge the potential pool of sustainable offerings within the North America polyamide market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile HMDA and caprolactam pricing | −0.6% | Continental North America with global linkage | Short term (≤ 2 years) |

| Automotive resin re-qualification delays | −0.4% | U.S. and Mexico OEM supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile HMDA and Caprolactam Feedstock Pricing

Caprolactam prices swung in 2024 after unplanned outages combined with elevated freight cost, squeezing PA6 compounder margins. BASF’s decision to take full control of Alsachimie and its 1.22 million t capacity shows how producers hedge volatility through upstream integration. However, resin buyers locked into quarterly price grids encountered immediate pass-throughs, distorting budgeting and contract negotiations. Petrochemical feedstocks remain tethered to crude-oil price swings and geopolitically driven shipping disruptions, creating a drag on the North America polyamide market. Inventory risk management and index-based formulas partially mitigate exposure but cannot eliminate rapid cost spikes.

Automotive Model-Year Resin Re-Qualification Delays

Stringent PPAP and IMDS documentation protocols mean new polyamide grades can wait 18-24 months for OEM approval, even when alternate materials offer pronounced performance gains. This latency slows market penetration of flame-retardant, conductive, or bio-based PA chemistries vital for next-generation electric-vehicle designs. Smaller resin innovators without legacy platform approvals encounter particular headwinds, often relying on tier-one cockpit or battery suppliers to champion the material upstream. The delay factor tempers the growth upside for specialty blends, trimming the aggregate expansion rate of the North America polyamide market during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Resin Type: Versatile PA6 Faces Specialty Growth Pressures

Polyamide 6 captured 56.88% of the North America polyamide market in 2025 by leveraging broad processing windows, competitive cost, and entrenched supply contracts with compounders across automotive, flexible-packaging, and furniture applications. Its dominance is reinforced by ample caprolactam capacity on the U.S. Gulf Coast, facilitating localized compound inventories and rapid color-match cycles. While continuing to gain share in EV battery shields where heat loads remain moderate, PA6 encounters increasing competition from PA66 and polyphthalamide when peak service temperatures exceed 150 °C.

Specialty sub-resins record faster tempo. Aramid fiber demand is accelerating at a 5.44% CAGR on tailwinds from commercial-aircraft ramp-ups, defense armor programs, and telecom-cable reinforcement. Polyphthalamide volumes remain niche yet rise in double digits, underpinned by superior creep resistance in miniaturized connectors. Producers are also commercializing long-glass PA grades that approach magnesium strength at 25% of the density, nudging metal-replacement share. Collectively, these specialty families capture incremental value pools that diversify the revenue base of the North America polyamide market.

By End-user Industry: Automotive Anchors While Electronics Accelerates

Automotive retained 30.12% share of the North America polyamide market in 2025, buoyed by 13.6 million North American vehicle assemblies and aggressive electrification roadmaps. Lightweight structural brackets, thermal-runaway barriers, and coolant connectors dominate the bill of materials.

Electrical and electronics emerges as the fastest-growing segment at 6.93% CAGR, riding data-center server count expansion, 5G-enabled base-station deployments, and consumer-device final assembly shifting into Mexico. High-temperature grades protect soldered joints and maintain dielectric properties under elevated power densities. Building and construction maintains mid-single-digit growth, supported by infrastructure bills and insulation upgrades, whereas industrial machinery sees moderate upticks linked to factory automation. Collectively, the demand mosaic sustains an overall balanced trajectory for the North America polyamide market.

Geography Analysis

The United States retained a commanding 77.85% share of the North America polyamide market in 2025 on the strength of integrated monomer crackers, established compounding clusters, and proximate automotive and aerospace OEMs. Evonik booked EUR 3,667 million in North American sales in 2024, underpinned by PA12 and PA610 expansions in Alabama and Michigan.

Mexico delivered the sharpest expansion path at a projected 6.02% CAGR to 2031. Nearshoring momentum saw USD 43.9 billion in FDI during 2023, funneling new molding, painting, and wiring-harness capacity into Bajío and northern states. Imports of 140 million kg of polyamides in 2023 filled immediate resin gaps, and local compounders are racing to commission lines compatible with automaker traceability standards.

INVISTA’s CAD 23 million hexamethylenediamine restart at Maitland secures a domestic PA66 intermediate, shortening supply chains for Canadian Tier-1s. Energy-sector projects, such as blue-hydrogen pipelines in Alberta, require high-performance polyamide pipe liners and insulation. Although absolute tonnage is modest, Canadian demand provides a diversified customer base that cushions against U.S. automotive cyclicality, reinforcing stability in the overall North America polyamide market.

Competitive Landscape

The North America polyamide market exhibits moderate fragmentation. BASF’s acquisition of Alsachimie streamlines internal PA66 precursor supply, reflecting a wider trend toward feedstock self-reliance. Evonik’s open publication of life-cycle metrics for over 100 grades underscores the new competitive currency of ESG transparency. Mid-tier specialists such as EMS-Chemie and Ensinger differentiate by focusing on metal-replacement compounds and carbon-fiber-reinforced PA grades, capturing niche margins. Distributors like PolySource broaden smaller producers’ reach, while custom compounders co-locate within OEM industrial parks to supply just-in-sequence pellets. Competitive intensity rises in recycled-content formulations, where emerging players leverage proprietary depolymerization to undercut virgin resin. Overall, technical agility and supply-chain proximity, rather than sheer scale, increasingly dictate share shifts within the North America polyamide market.

North America Polyamide Industry Leaders

Arkema

Ascend Performance Materials

BASF

Domo Chemicals

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Lone Star Funds agreed to acquire RadiciGroup’s Specialty Chemicals and High Performance Polymers divisions, restructuring competitive dynamics in European PA supply.

- July 2024: RadiciGroup won an industry award for a 100% recycled-polyamide automotive air-intake manifold supplied to a German OEM, demonstrating full circular feasibility at Tier-1 scale.

North America Polyamide Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Aramid, Polyamide (PA) 6, Polyamide (PA) 66, Polyphthalamide are covered as segments by Sub Resin Type. Canada, Mexico, United States are covered as segments by Country.| Aramid |

| Polyamide 6 |

| Polyamide 66 |

| Polyphthalamide |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-User Industries |

| Canada |

| Mexico |

| United States |

| By Sub-Resin Type | Aramid |

| Polyamide 6 | |

| Polyamide 66 | |

| Polyphthalamide | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-User Industries | |

| By Geography | Canada |

| Mexico | |

| United States |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyamide market.

- Resin - Under the scope of the study, virgin polyamide resins like Polyamide 6, Polyamide 66, Polyphthalamide, and Aramid in the primary forms are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms