Polydextrose Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

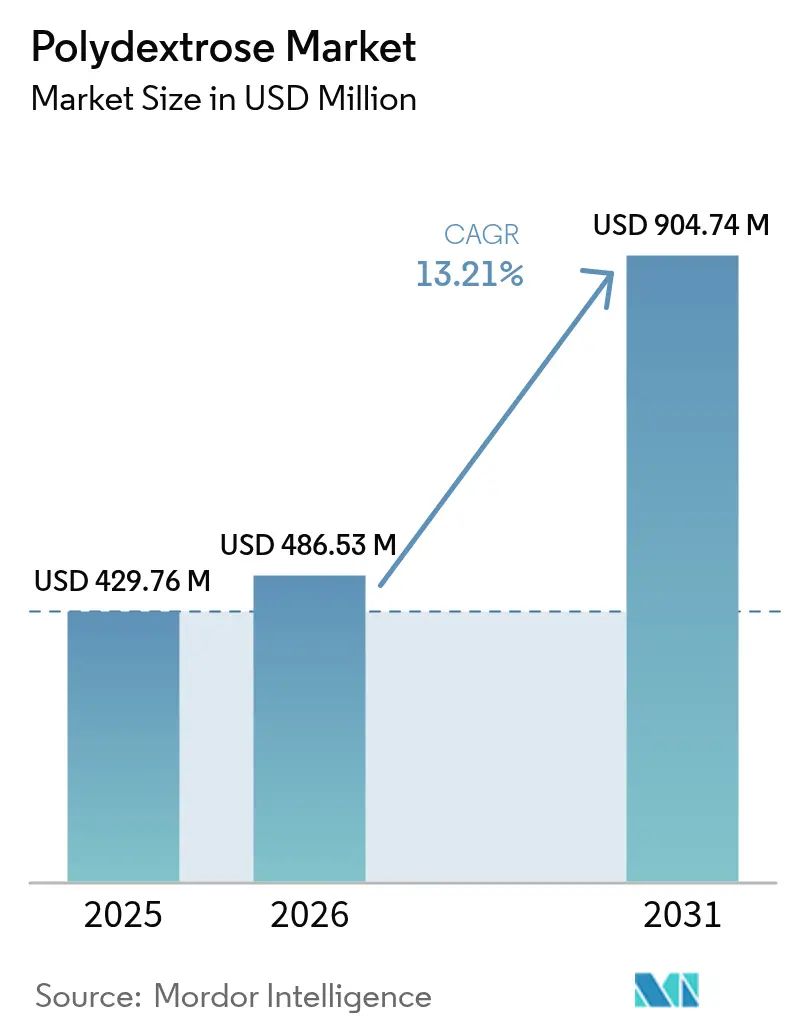

| Market Size (2026) | USD 486.53 Million |

| Market Size (2031) | USD 904.74 Million |

| Growth Rate (2026 - 2031) | 13.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polydextrose Market Analysis by Mordor Intelligence

The polydextrose market size is expected to grow from USD 429.76 million in 2025 to USD 486.53 million in 2026 and is forecast to reach USD 904.74 million by 2031 at 13.21% CAGR over 2026-2031. The market growth is driven by polydextrose's dual functionality as a low-calorie bulking agent and prebiotic fiber, enabling food and beverage manufacturers to reduce sugar content while providing scientifically proven digestive health benefits. Regulatory approvals from organizations like the U.S. Food and Drug Administration have enhanced the ingredient's market acceptance, reduced reformulation risks, and increased manufacturer confidence in product development. The market expansion is further supported by increased functional beverage production across multiple categories, growing demand in pharmaceutical applications as excipients, and stringent sugar reduction regulations in European countries. The polydextrose market continues to benefit from increasing health-conscious consumer preferences, clean label demands, and extensive product reformulation trends across the food and beverage industry, supporting its projected strong growth trajectory through 2030.

Key Report Takeaways

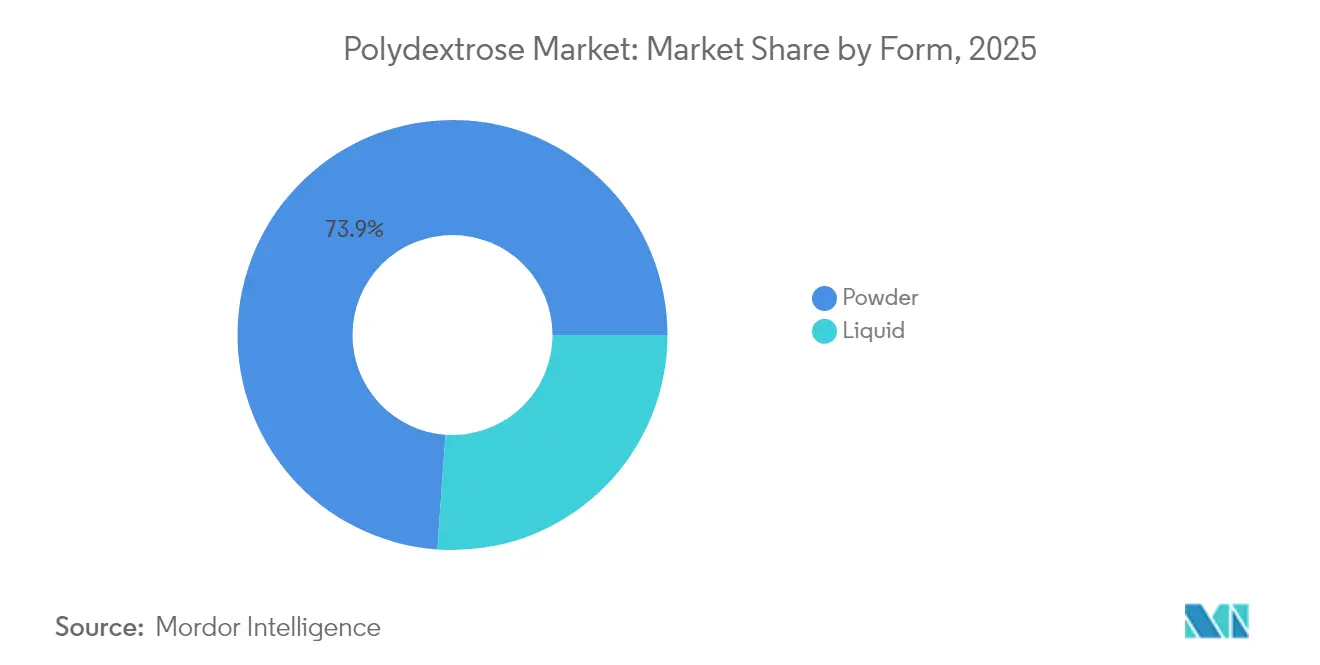

- By form, powder led with 73.88% of polydextrose market share in 2025, while liquid is poised for the quickest expansion at 14.12% CAGR over the same horizon.

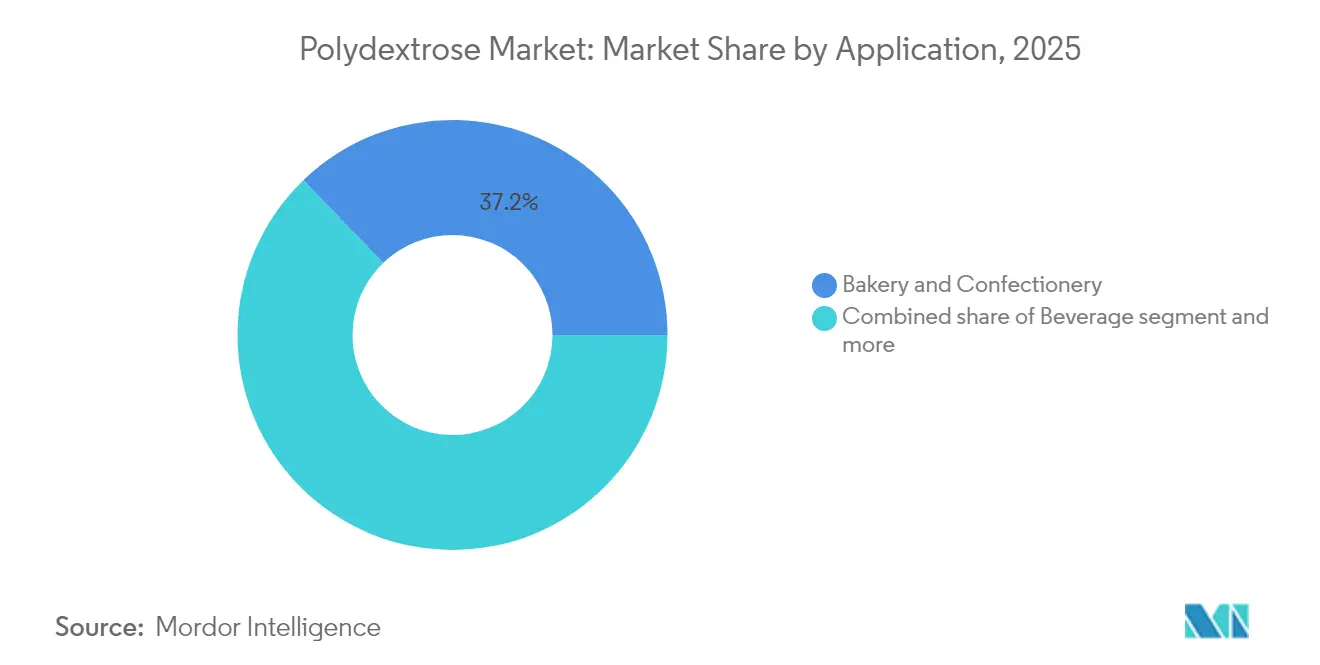

- By application, bakery and confectionery captured 37.20% revenue share of the polydextrose market in 2025; beverages are projected to record the highest 14.05% CAGR between 2026-2031.

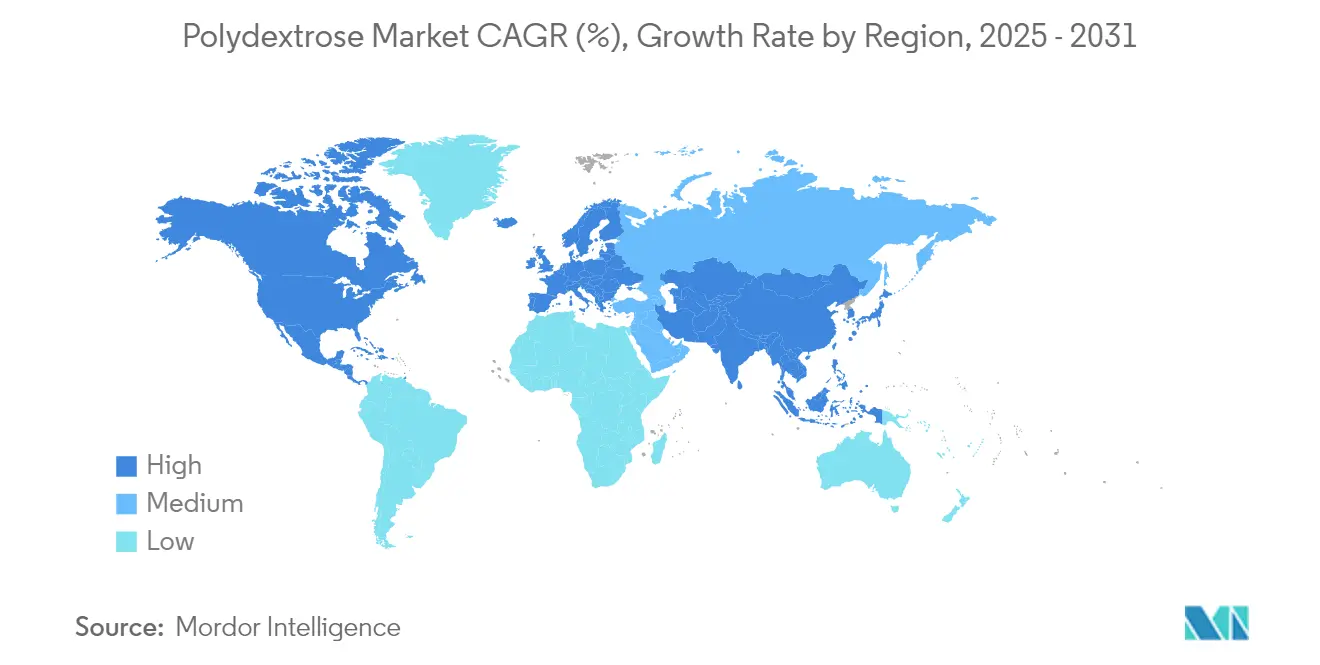

- By geography, Europe commanded 35.10% of the polydextrose market share in 2025, whereas Asia-Pacific is expected to post the fastest 14.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polydextrose Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health consciousness raises demand for low-calorie, high-fiber foods | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Expansion of pharmaceutical manufacturing boosts excipient demand | +1.8% | United States, Europe, India manufacturing hubs | Long term (≥ 4 years) |

| Rising focus on digestive wellness energizes prebiotic fiber uptake | +1.5% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Wider use in low-calorie bakery products | +1.2% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Food-processing technology advancements widen application scope | +0.9% | Global, led by developed markets | Long term (≥ 4 years) |

| Lifestyle-related disease prevalence supports healthier diets | +0.8% | Global, acute in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Health Consciousness Fuels Demand for Low-Calorie, High-Fiber Foods

Consumers are increasingly conscious of their dietary choices, seeking products that help manage weight, support digestive health, and reduce the risk of chronic diseases. Polydextrose, a low-calorie soluble fiber used to replace sugar and fat while increasing fiber content, meets these consumer requirements while delivering essential functional benefits. The International Food Information Council's 2024 Food and Health Survey reveals that 24% of U.S. consumers consider "good source of fiber" and 17% consider "low calorie" as primary indicators of healthy food [1]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY," foodinsight.org. This trend has prompted food and beverage manufacturers to develop products that meet these requirements while maintaining taste and texture. Polydextrose enables companies to achieve both fiber enrichment and calorie reduction, making it a key ingredient in snacks, bakery products, beverages, and confectioneries targeting health-conscious consumer segments. The Centers for Disease Control and Prevention (CDC) reports that approximately 1 in 10 Americans has diabetes, predominantly type 2 [2]Source: Centers for Disease Control and Prevention (CDC), "Type 2 Diabetes," cdc.gov.

Expanding Pharmaceutical Manufacturing Drives Demand for Excipients and Fillers

Global pharmaceutical manufacturing expansion fuels the growth of the polydextrose market. As pharmaceutical formulations diversify, spanning tablets, capsules, and functional health supplements, the demand surges for excipients and fillers vital for ensuring product stability, uniformity, and health benefits. In pharmaceuticals, polydextrose boasts several key physicochemical attributes: it provides bulk without adding significant calories, enhances texture, and ensures consistent tablet formation. Its high solubility and neutral taste allow for seamless integration into various oral dosage forms, preserving the product's sensory appeal. Moreover, polydextrose's classification as a dietary fiber enhances formulations aimed at promoting digestive health and glycemic control. Global pharmaceutical production is on the rise, spurred by an aging population, a surge in chronic diseases, and better healthcare access in emerging markets. Bolstered by a robust safety profile, stability characteristics, and broad regulatory acceptance, polydextrose solidifies its stance, especially amidst stringent pharmaceutical excipient regulations.

Increasing Consumer Interest in Digestive Health Drives Prebiotic Fiber Market

As consumers increasingly prioritize digestive wellness, the demand for prebiotic fibers, especially polydextrose, surges. Heightened awareness of gut microbiota's role in immunity, nutrient absorption, and overall health has spurred a demand for dietary solutions that bolster digestive function. Manufacturers are infusing polydextrose into functional foods, beverages, and dietary supplements. With a shift towards preventive health, consumers are gravitating towards long-term digestive care solutions, propelling the growth of the polydextrose market. Notably, Japan and South Korea exhibit a pronounced demand for polydextrose, driven by aging populations keen on preserving digestive health for active lifestyles. The World Economic Forum projects that the global population aged 65 and older will reach 1.6 billion by 2050, doubling current numbers, with Asia experiencing the most significant demographic shift. South Korea, Hong Kong, and Japan are expected to have nearly 40% of their populations aged 65 or older by 2050 [3]Source: World Economic Forum, "The world's oldest populations," weforum.org . This demographic trend creates substantial market opportunities for prebiotic fibers like polydextrose, as older adults seek solutions for age-related digestive issues and overall health maintenance.

Amplifying Use in Low Calorie Bakery Products

Polydextrose is increasingly being incorporated into low-calorie bakery products, driving its market growth. As consumers focus on calorie intake and carbohydrate quality, manufacturers are reformulating items like breads, muffins, and pastries with low-calorie, high-fiber ingredients that promote weight management and digestive health. Polydextrose provides bulk and texture similar to sugar but with significantly fewer calories, making it a key functional ingredient for healthier, yet tasty, alternatives. Further, the Snack Food and Wholesale Bakery report indicates that center store breads ranked as the second highest-selling bakery category in the U.S. in 2024, with unit sales reaching 3.3 billion. As consumers continue to purchase bakery staples in large volumes, there is a growing opportunity and necessity for brands to differentiate through low-calorie, fiber-enhanced formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of raw materials | -1.4% | Global, particularly acute in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Limited consumer awareness in developing economies | -0.9% | Asia-Pacific emerging markets, Latin America, Africa | Medium term (2-4 years) |

| Potential digestive side effects at high consumption levels | -0.7% | Global, regulatory concern in all markets | Long term (≥ 4 years) |

| Lack of standardization in global quality specifications | -0.5% | Global, cross-border trade impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Raw Materials

Raw material price volatility significantly hampers the growth of the polydextrose market. Polydextrose production relies heavily on glucose syrups, starches, and sorbitol, with their prices tethered to agricultural commodity markets and global supply-demand dynamics. Unpredictable weather, geopolitical tensions, supply chain disruptions, and shifts in agricultural policies can lead to substantial increases in production costs for manufacturers. This impact is especially pronounced in regions that are both raw material-scarce and heavily reliant on imports. Such price instabilities challenge manufacturers in setting consistent prices for polydextrose, squeezing profit margins, and undermining operational efficiency. Faced with rising costs, manufacturers must either absorb the costs, curtailing investments and market expansion, or pass them onto consumers, risking reduced demand in price-sensitive markets.

Limited Consumer Awareness in Developing Economies

Limited consumer awareness in developing economies constrains the polydextrose market growth. While polydextrose offers benefits as a low-calorie, high-fiber ingredient that supports digestive health and weight management, consumers in emerging regions remain largely unfamiliar with the ingredient. The lack of understanding about its functional properties, health benefits, and food applications results in low demand and slower market penetration. Traditional dietary preferences in developing markets reduce consumer interest in functional ingredients like polydextrose. The limited marketing initiatives and restricted availability of polydextrose-enriched products further impede its adoption. Manufacturers and suppliers struggle to generate product trials and repeat purchases due to insufficient consumer awareness and education, which impacts the market growth in developing economies. Expanding consumer education and awareness programs remains essential for market development in these regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Meets Liquid Innovation

Powder polydextrose holds 73.88% market share in 2025, maintaining its dominant position in dry-mix applications due to its stability and handling advantages. The powder format offers extended shelf life and reduced transportation costs, making it cost-effective for industrial food production. Liquid polydextrose is projected to grow at 14.12% CAGR through 2031, primarily due to its operational benefits in beverage manufacturing by eliminating dissolution processes. The liquid format enables accurate dosing and direct integration into production processes, minimizing processing time and workforce requirements.

The beverage industry's increasing focus on digestive health-oriented functional drinks has increased the demand for liquid polydextrose, which readily incorporates into water-based systems. The sports nutrition segment particularly benefits from liquid formats in protein powder production, where proper dissolution is crucial for product quality. Glanbia reports that by 2025, approximately one-third of sports nutrition consumers globally will increase their product consumption compared to the previous year, motivated by health benefits (46%) and increased exercise (43%). Manufacturing innovations in spray-drying and fluid-bed granulation continue to enhance powder properties, while developments in liquid concentration methods improve stability and reduce shipping expenses.

By Application: Bakery Leadership Faces Beverage Disruption

Bakery and confectionery applications hold a 37.20% market share in 2025, as polydextrose serves as a sugar replacement while improving texture and moisture retention. This segment's strength stems from well-established formulation practices and consumer acceptance of fiber-enriched baked products. Dairy products represent the second-largest application segment, with polydextrose enabling reduced-calorie yogurt and ice cream without affecting texture. Ready-to-eat products incorporate polydextrose for extended shelf life.

The beverages segment is growing at a 14.05% CAGR through 2031, driven by increased demand for functional drinks targeting digestive health and weight management. This growth is supported by polydextrose's high solubility and neutral taste, enabling high-fiber claims while maintaining product taste. Meat products remain a smaller application segment but show growth potential in processed meat formulations requiring fiber enrichment. Additional applications in supplements and pharmaceuticals contribute to market expansion and value-added opportunities.

Geography Analysis

Europe holds the largest market share at 35.10% in 2025, driven by strict regulatory frameworks supporting scientifically validated ingredients like polydextrose. The region's health-conscious consumers and advanced food processing infrastructure enable widespread adoption across food applications. The European Food Safety Authority's (EFSA) 2021 safety re-evaluation reinforces manufacturer confidence, while sugar reduction initiatives and clean-label preferences maintain consistent demand. North America holds the second-largest market position, supported by long-standing Food and Drug Administration (FDA) approval and well-defined food additive regulations. The region shows strong demand growth, particularly in premium and organic food segments, driven by consumer understanding of digestive health benefits.

Asia-Pacific demonstrates the highest growth rate at 14.18% CAGR through 2031, fueled by increasing disposable incomes and health awareness in urban areas. China's expanding food processing sector and regulatory acceptance create market opportunities, while India's pharmaceutical industry growth increases excipient demand. Japan's aging population and functional food focus support high-value polydextrose applications. Despite varying regulations across countries, successful market entry provides access to large consumer bases with increasing purchasing power.

South America, and Middle East and Africa (MEA) show promising growth potential. South American demand increases through urbanization, health awareness, and government nutrition initiatives. Brazil expanding bakery and beverage industries incorporate polydextrose to meet health-conscious consumer demands.Both regions face challenges in consumer awareness and regulatory compliance, requiring targeted education and strategic partnerships for market development.

Competitive Landscape

The polydextrose market demonstrates moderate consolidation, characterized by competition between multinational companies and regional manufacturers. Market leaders maintain competitive advantages through vertical integration, encompassing raw material sourcing, production, and application expertise. The major players in the market include Tate & Lyle, International Flavors & Fragrances Inc., Cargill, Incorporated, Ingredion Incorporated, and Roquette Frères. Companies differentiate themselves through technology adoption, with major players investing in automated laboratories and advanced processing capabilities to enhance product development efficiency.

Regional manufacturers compete by focusing on niche applications and leveraging their market proximity and operational flexibility. The competitive landscape continues to evolve through strategic collaborations and acquisitions. Companies form partnerships with ingredient distributors, food manufacturers, and research institutions to enhance their product offerings and market reach. Environmental sustainability has become a competitive factor, with manufacturers implementing eco-friendly production processes and using renewable raw materials to meet regulatory requirements and consumer preferences.

Competition intensifies through innovation in customized polydextrose solutions that address specific dietary requirements, including sugar reduction, digestive health, and calorie control. Companies that combine technological capabilities, regulatory compliance, and strong customer relationships are positioned to capture market growth opportunities in this competitive environment.

Polydextrose Industry Leaders

-

Tate & Lyle PLC

-

Ingredion Incorporated

-

International Flavors & Fragrances Inc. (IFF)

-

Shandong Saigao Group Corporation

-

Foodchem International Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: IFF announced the renovation and expansion of its Shanghai Creative Center, the company's largest research and development facility in Asia. The 16,000-square-meter site will integrate the company's capabilities in flavors, functional ingredients, biotechnology, and perfumery operations. The expanded facility is scheduled to begin full operations in August 2024.

- May 2024: Tate & Lyle completed a EUR 25 million expansion of its Boleráz facility in Slovakia to increase production of its non-GMO PROMITOR® soluble fibres. The initial phase improves the facility's capacity to serve European and global customers while enhancing energy efficiency and supply chain operations.

- March 2023: Azelis acquired Gillco Ingredients, a specialty ingredient distributor located in San Marcos, California. Gillco serves approximately 1,000 customers across bakery, beverage, dairy, culinary, and nutraceutical markets with its portfolio of clean-label and specialty ingredients. The acquisition, scheduled for completion in Q2 2023,

Global Polydextrose Market Report Scope

The global polydextrose market is segmented on the basis of application and form. By application, the polydextrose market is segmented as bakery and confectionery, beverages, yogurts and dairy products, and others. By form, the market is segmented as powder and liquid.

| Powder |

| Liquid |

| Bakery and Confectionery |

| Dairy and Dairy Products |

| Ready-To-Eat Products |

| Meat and Meat Products |

| Beverage |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| By Application | Bakery and Confectionery | |

| Dairy and Dairy Products | ||

| Ready-To-Eat Products | ||

| Meat and Meat Products | ||

| Beverage | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the polydextrose market by 2031?

The market is forecast to reach USD 904.74 million by 2031, advancing at a 13.21% CAGR from 2026 levels.

Which form leads the polydextrose market and why?

Powder holds the dominant 73.88% share in 2025 because of stability, longer shelf life, and easier handling in dry-mix applications.

Why are beverages the fastest-growing application?

Digestive-health drinks and sugar-free carbonates favor polydextrose for its neutral flavor and high solubility, pushing the segment at a 14.05% CAGR through 2031.

Which region offers the quickest growth prospects?

Asia-Pacific is set to grow at 14.18% CAGR to 2031, driven by rising disposable incomes, regulatory approvals, and expanding functional food awareness.

Page last updated on: