Dimethyl Ether Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

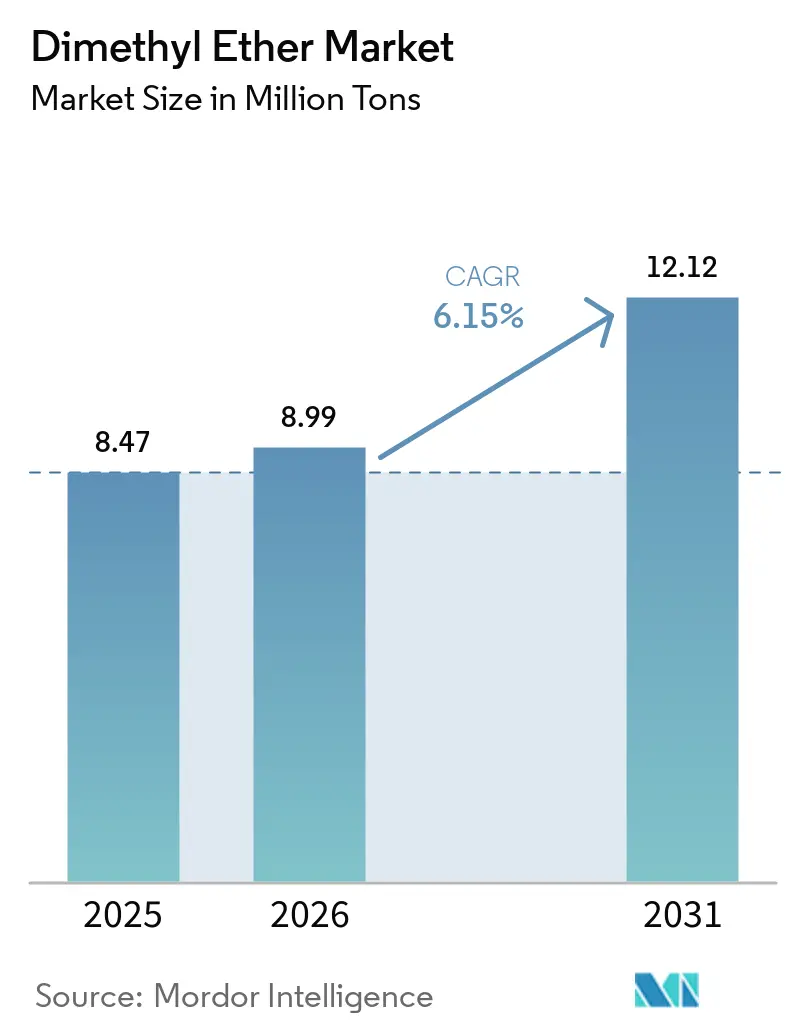

| Market Volume (2026) | 8.99 Million tons |

| Market Volume (2031) | 12.12 Million tons |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dimethyl Ether Market Analysis by Mordor Intelligence

The Dimethyl Ether Market size is projected to expand from 8.47 million tons in 2025 and 8.99 million tons in 2026 to 12.12 million tons by 2031, registering a CAGR of 6.15% between 2026 to 2031. Demand stems from household LPG blending mandates, emerging fuel-substitution programs for heavy-duty fleets, and the shift toward low-global-warming aerosol propellants, with Asia-Pacific retaining 86.22% of global volume in 2025. Natural-gas pathways still dominate output, yet modular bio-DME projects that pair green hydrogen with captured CO₂ are expanding at an 8.45% annual pace, helped by carbon-credit incentives and declining electrolyzer costs. Direct gas-to-DME processes under development in Japan, South Korea, and Malaysia promise to trim capital expenditure versus two-step methanol dehydration, although large-scale validation is pending. Competition across these routes is fragmenting the market, creating room for hybrid configurations that balance feedstock flexibility with decarbonization credentials.

Key Report Takeaways

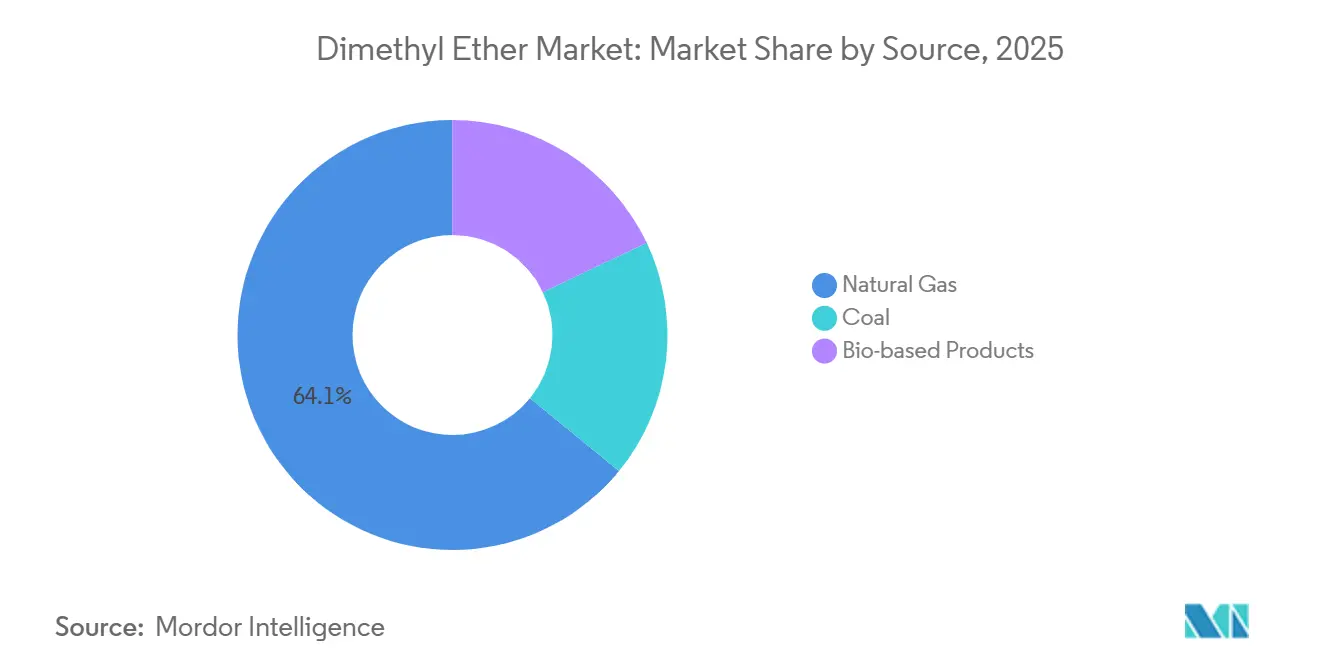

- By source, natural-gas DME held 64.11% of the dimethyl ether market share in 2025, whereas bio-based output is projected to advance at an 8.45% CAGR to 2031.

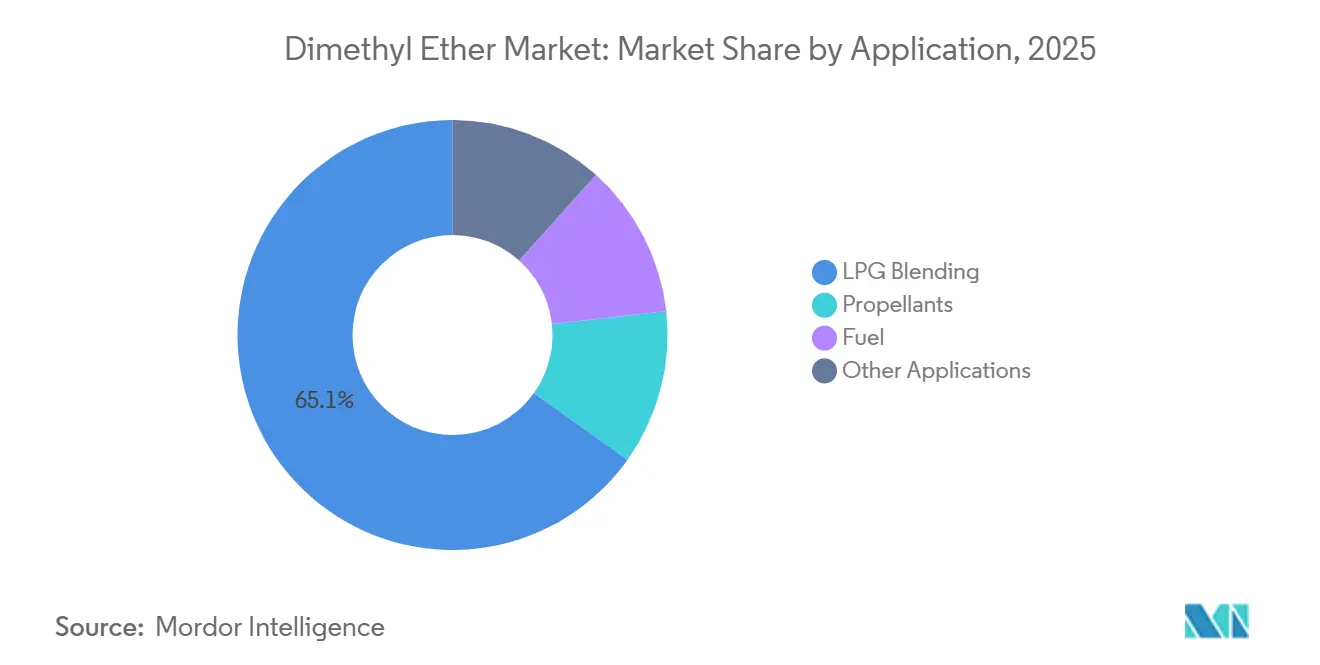

- By application, LPG blending commanded a 65.15% share of the dimethyl ether market size in 2025, while fuel is set to post a 6.48% CAGR through 2031.

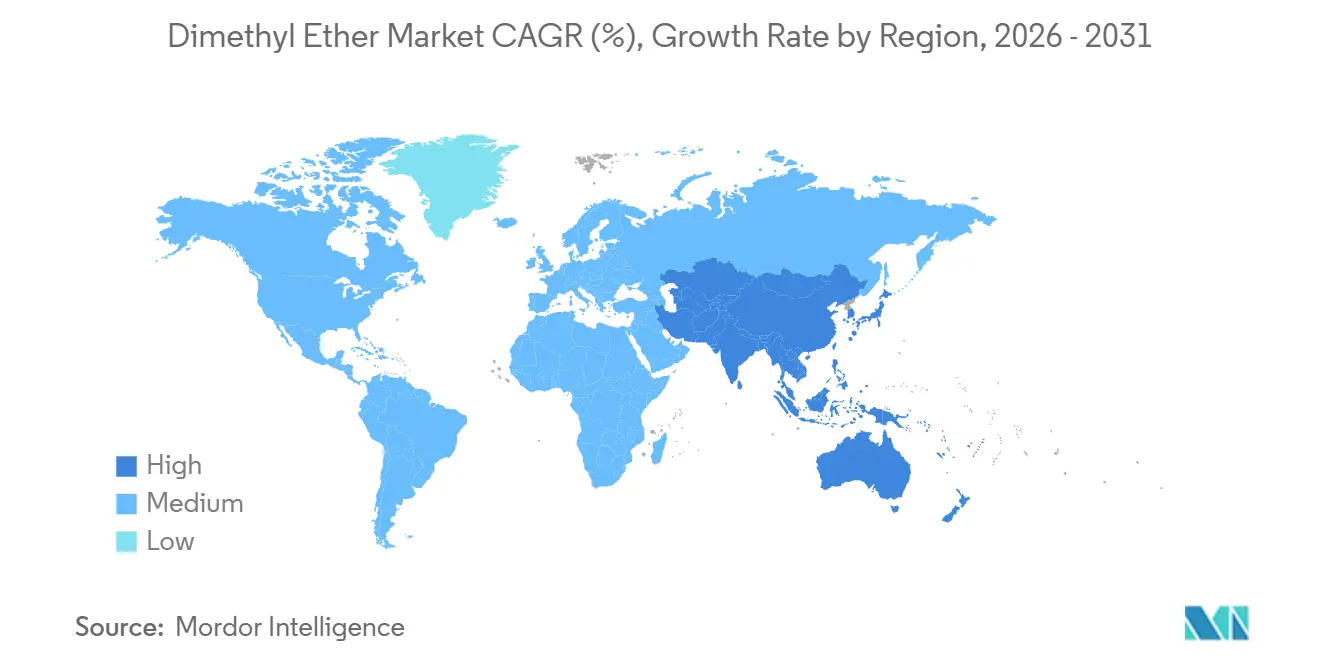

- By geography, Asia-Pacific captured 86.22% of the dimethyl ether market share in 2025 and is expanding at a 6.14% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dimethyl Ether Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand from LPG Blending Applications | +1.8% | Asia-Pacific core, spill-over to Middle-East and Africa | Medium term (2-4 years) |

| Increasing Fuel Demand from Transportation and Industrial Boilers | +1.2% | Global, with early adoption in China, India, Japan | Medium term (2-4 years) |

| Government Incentives for Ultra-Low-Sulfur Household Fuels | +1.0% | India, Indonesia, Thailand, Vietnam | Short term (≤ 2 years) |

| Modular Bio-DME Plants Leveraging Green H₂ and Captured CO₂ | +0.9% | North America, Europe, with pilot projects in South Korea | Long term (≥ 4 years) |

| DME as a Hydrogen Carrier for Long-Haul Fuel-Cell Logistics | +0.6% | Japan, South Korea, select EU corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from LPG Blending Applications

Asian countries, often densely populated, are prioritizing the reduction of sulfur emissions. One method to achieve this is by blending Dimethyl Ether (DME) into Liquefied Petroleum Gas (LPG) cylinders. This not only stretches the volumes of imported propane and butane but also addresses environmental concerns. In India, where LPG cylinders are distributed daily to households, the oil ministry has proposed a nationwide DME blend. This initiative aims to reduce the country's dependence on LPG imports from the Middle-East. Meanwhile, in Indonesia, studies reveal that DME substitution can lower household fuel costs without necessitating any modifications to stoves. Further validating these moves, Korea Gas Corporation has confirmed that a DME blend is compatible with the existing LPG infrastructure, appliances, and distribution networks[1]Korea Gas Corporation, “12% DME Blend Demonstration Project,” kogas.or.kr. Additionally, utilities are leaning towards multi-year supply contracts, linking them to cylinder-fill ratios. This strategy helps shield producers from the volatility of the spot market. Consequently, LPG blending has emerged as the dominant volume anchor for the Dimethyl Ether market.

Increasing Fuel Demand from Transportation and Industrial Boilers

Heavy-duty trucks and industrial boilers are turning to DME to meet Euro VI particulate standards, sidestepping the need for selective catalytic reduction systems. China's LNG-powered truck fleet is projected to grow significantly by 2030. This surge paves the way for a parallel demand for DME, celebrated for its lower sulfur content and simplified after-treatment. Japan's trade ministry is eyeing DME for power generation on remote islands, where diesel logistics come at a premium. In India and Thailand, pilot boiler projects are experimenting with DME to reduce coal consumption. However, there's a pressing need for investment in bulk storage and vaporization infrastructure. For widespread adoption, standardized fuel-quality specifications and retail networks on par with diesel are essential. Despite these challenges, the early growth signals a promising mid-term expansion for the Dimethyl Ether market.

Government Incentives for Ultra-Low-Sulfur Household Fuels

Governments in South and Southeast Asia are subsidizing ultra-low-sulfur cooking fuels to align with the WHO's indoor-air guidelines supporting growth in the dimethyl ether market. While India's Methanol Economy Program champions methanol and DME as cleaner alternatives to kerosene and biomass, domestic methanol production remains insufficient, leading to a dependence on imports. In peri-urban areas with unreliable grid power, Thailand and Vietnam are testing pilot DME–LPG blends. These countries offer incentives such as tax exemptions on DME imports, capital grants for cylinder filling, and public-awareness campaigns promoting DME as “green LPG.” Although the immediate effects are felt regionally, the policy framework could be adopted by Middle Eastern and African nations grappling with similar indoor-air challenges and import costs.

Modular Bio-DME Plants Leveraging Green H₂ and Captured CO₂

In a groundbreaking approach, modular bio-DME facilities harness electrolytic hydrogen and point-source CO₂ to produce methanol, which is subsequently dehydrated into DME, all without relying on fossil feedstock creating new opportunities for the dimethyl ether market. Oberon Fuels, based in California, operates a plant that utilizes waste methanol and solar steam, setting its sights on a significant production target by 2030[2]Oberon Fuels, “Renewable DME Production Fact Sheet,” oberonfuels.com. Meanwhile, Biofriends Inc. is in the process of commissioning a unit in South Korea, adept at capturing CO₂ from cement kilns and converting it to DME. Research indicates that when powered by renewable electricity, these facilities can achieve lifecycle greenhouse gas reductions exceeding diesel. While capital costs are currently higher than traditional natural gas routes, the modular design of these facilities offers the advantage of incremental capacity increases and proximity to emitters, significantly cutting down on pipeline expenses. The key to their competitiveness lies in achieving hydrogen price parity, a milestone anticipated in the early part of the next decade.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex/OPEX For Large-Scale Synthesis and Dehydration | -1.3% | Global, acute in regions lacking natural-gas pipelines | Medium term (2-4 years) |

| Competition from LNG, LPG, and Green Methanol | -0.8% | Asia-Pacific, Europe, Middle East | Short term (≤ 2 years) |

| Methanol Feedstock Price Volatility Amid E-Methanol Boom | -0.7% | Global, most pronounced in Asia and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex/OPEX For Large-Scale Synthesis and Dehydration

Building a DME plant requires significant investment. Operating margins for these plants are notably influenced by fluctuations in natural gas prices and the cycles of catalysts. A reference plant in Japan underscores the maturity of the technology but also its capital-intensive nature, posing challenges for the DME market. Meanwhile, a unit in Germany grapples with the volatility of European gas prices, which significantly impact its profitability. In Malaysia, a feasibility study is exploring an approach that aims to sidestep methanol dehydration, potentially saving on capital expenditures, but it remains untested on a large scale. Additionally, regions lacking access to affordable pipeline gas incur extra transport costs. This financial burden not only concentrates production in areas rich in feedstock but also hampers efforts for geographic diversification.

Methanol Feedstock Price Volatility Amid E-Methanol Boom

Between Q4 2024 and Q1 2025, methanol prices dipped. Yet, major marine bunker projects are securing multi-year offtakes, tightening spot availability. Methanex reported Q1 2025 contract prices in North America, Europe, and Asia. While these figures represent a decline from the previous quarter, they remain volatile for uncontracted producers creating cost pressures for the dimethyl ether market. Ørsted and Maersk are eyeing an e-methanol plant in Louisiana, set to launch by 2027. Meanwhile, in 2024, CNOOC–Shell inaugurated a unit in Huizhou, diverting supply from DME. The shipping industry's enthusiasm for e-methanol is evident as Maersk placed orders for methanol-ready vessels and Mitsui OSK Lines added to their fleet. DME producers, lacking captive feedstock, face a choice: either backward-integrate or contend with squeezed margins, especially in Asia, which is heavily reliant on imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Bio-Based Routes Gain Despite Natural-Gas Dominance

Natural-gas pathways held 64.11% of the Dimethyl Ether market share in 2025, reflecting abundant gas reserves and mature methanol-to-DME technology. Coal-to-DME remains a niche in China, yet rising carbon costs challenge its economics. Bio-based output, though small, is expanding at an 8.45% CAGR through 2031. Oberon Fuels leverages waste methanol in California, while Biofriends Inc. captures cement-kiln CO₂ in South Korea. Lifecycle studies confirm emissions reductions, but capex stays above conventional plants.

Cost divergence is sharpening. Gas-based facilities enjoy scale and low variable cost yet face exposure to gas-price swings and looming carbon-border adjustments. Bio-based operators secure premium offtakes under California’s Low Carbon Fuel Standard and Europe’s Renewable Energy Directive II, but must manage green-hydrogen supply chains. Coal-to-DME is likely to contract as China’s national carbon market expands, diverting investment to gas and bio routes that align with net-zero commitments. The Dimethyl Ether market size for bio-based output is therefore expected to climb steadily despite today’s higher costs.

By Application: Fuel Segment Accelerates as LPG Blending Plateaus

LPG blending accounted for 65.15% of the Dimethyl Ether market size in 2025, bolstered by India's daily filling of cylinders and Indonesia's endorsement of DME blends. Additionally, Korea Gas Corporation showcased compatibility with traditional LPG appliances. Aerosol propellants form a stable niche as firms replace hydrofluorocarbons under the Kigali Amendment. The fuel segment, covering heavy-duty trucks and boilers, is projected to increase at a 6.48% CAGR.

China’s LNG truck fleet expansion creates a ready corridor for DME, while Japan studies DME for remote-island power where diesel is costly. Industrial boilers in India and Thailand test DME blends to curb coal use, pending bulk-storage investments. As fuel applications scale, the Dimethyl Ether market share for LPG blending will gradually plateau, yet it remains the dominant anchor through the forecast period. Future growth hinges on harmonized fuel standards and widespread refueling infrastructure.

Geography Analysis

Asia-Pacific held 86.22% volume share in 2025 and is forecast to grow at a 6.14% CAGR through 2031. This surge is largely attributed to China's expanding LNG truck fleet, India's initiative to blend LPG, and South Korea's experimental pilots in direct synthesis. This uptick bolsters the demand for DME, touted as a sulfur-free alternative. India's ambition to blend DME with LPG for its households could significantly reduce its LPG imports from the Middle East. Meanwhile, Korea Gas Corporation is eyeing a target from its Malaysian project, leveraging direct gas-to-DME synthesis to optimize operational costs.

North America and Europe are emerging as pivotal tech hubs for renewable DME, supporting growth in the US dimethyl ether market. Oberon Fuels has secured ISCC PLUS certification for its California plant, underscoring its credibility. Additionally, Suburban Propane's notable equity stake signals LPG distributors' strategic move to hedge against the looming wave of electrification. Across the Atlantic, Grillo-Werke's facility in Germany is a key supplier of aerosol propellants. However, the company grapples with margin pressures due to the volatility of European gas prices. In a strategic maneuver, Ørsted and Maersk's e-methanol initiative in Louisiana is poised to reroute methanol feedstock towards the shipping sector, potentially constraining the supply for North American DME producers.

While South America, the Middle-East, and Africa are still in the early stages, they hold promise. Brazil and Argentina boast rich biomass resources, yet they face hurdles in financing synthesis units. In the Gulf, Saudi Arabia and the UAE are positioning DME as a premium product, eyeing exports to Asia. Closer to home, Nigeria and South Africa grapple with increasing LPG demand and air quality concerns. However, they require solid offtakes and international funding to establish domestic DME plants. Given the current landscape, these regions are likely to depend on imports until 2031, solidifying Asia-Pacific's status as the DME market's nucleus.

Competitive Landscape

The dimethyl ether market is moderately fragmented. White-space opportunities cluster around modular plants co-located with cement or steel sites where point-source CO₂ capture feeds bio-DME synthesis. Patent activity in direct gas-to-DME catalysts is rising as JGC Holdings and Mitsubishi disclose formulations that curb deactivation. ISO committees are drafting DME blend standards, which will ease cross-border trade once finalized. Competitive intensity is set to rise as e-methanol projects absorb incremental methanol for shipping, forcing DME makers to secure captive feedstock or backward-integrate. Companies lacking access to low-cost gas or renewable power risk being confined to niche regional markets, whereas vertically integrated players can defend margins across the value chain.

Dimethyl Ether Industry Leaders

Nouryon

Dongguan Jovo Warehousing Services Co., Ltd.

Korea Gas Corporation

Mitsubishi Gas Chemical Company, Inc.

Shell PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nouryon attained ISCC PLUS certification for DME output at Rotterdam, enabling customers to verify scope-3 emission cuts.

- June 2024: Mitsubishi Gas Chemical produced Japan’s first bio-methanol from digester gas, establishing a feedstock base for bio-DME.

Global Dimethyl Ether Market Report Scope

Dimethyl ether (DME) or methoxy methane is a transparent, scentless gas with a low boiling point. It is produced from diverse sources like natural gas, methanol, coal, and biomass. DME is mainly used in LPG blending and as an alternative energy fuel without sulfur content. Also, it is used as an aerosol propellant across different industries, such as cosmetics, pharmaceuticals, etc., and as a refrigerant.

The dimethyl ether market is segmented by source, application, and geography. By source, the market is segmented into natural gas, coal, and bio-based products. By application, the market is segmented into propellants, LPG blending, fuel, and other applications. The report also covers the market size and forecasts for the dimethyl ether market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Natural Gas |

| Coal |

| Bio-based Products |

| Propellants |

| LPG Blending |

| Fuel |

| Other Applications |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Natural Gas | |

| Coal | ||

| Bio-based Products | ||

| By Application | Propellants | |

| LPG Blending | ||

| Fuel | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is Asia-Pacific demand for DME growing?

Asia-Pacific’s Dimethyl Ether market is forecast to expand at a 6.14% CAGR between 2026 and 2031, led by LPG blending and fuel applications.

Which application currently uses the most DME?

LPG blending dominates with 65.15% of the 2025 volume, driven by cylinder programs in India, Indonesia, and South Korea.

What share does bio-based production hold today?

Bio-based is rising rapidly at an 8.45% CAGR as modular plants scale in North America, Europe, and South Korea.

Why are methanol prices a risk for DME producers?

Marine e-methanol projects are locking long-term offtakes, reducing spot availability, and creating feedstock price volatility for DME plants without captive methanol.

What is the current global demand for the dimethyl ether market and its expected growth by 2031?

Global consumption is 8.99 million tons in 2026 and is projected to reach 12.12 million tons by 2031, reflecting a 6.15% CAGR.

Page last updated on: