Point-of-Care Data Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

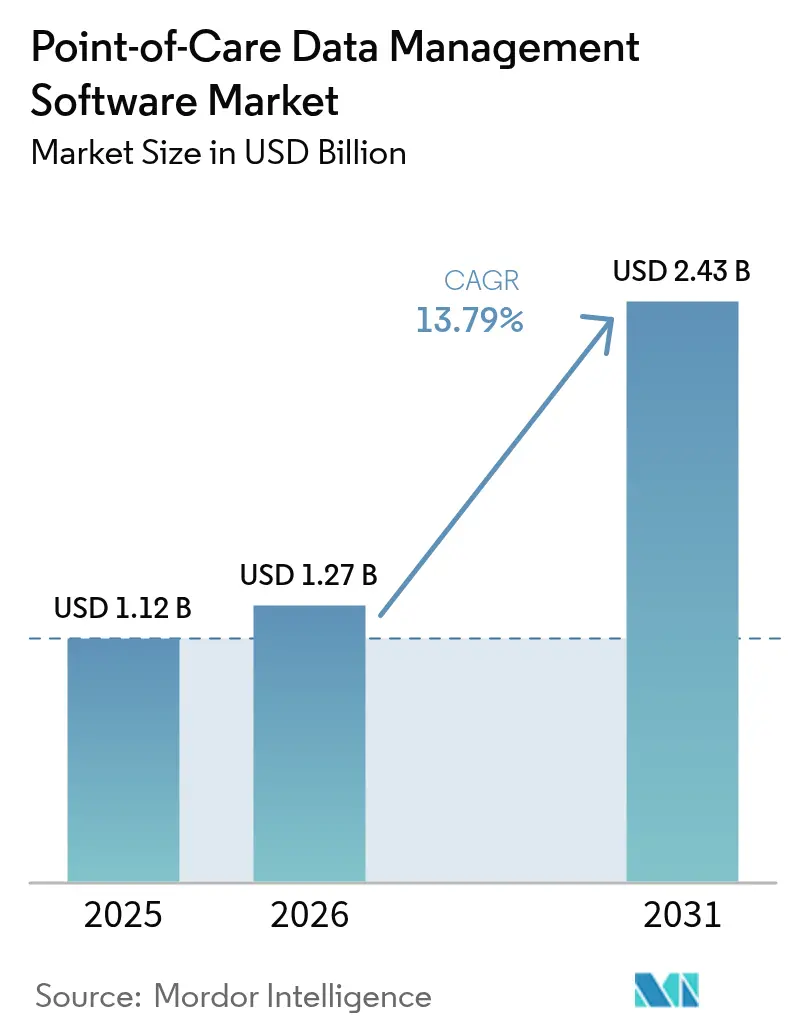

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 13.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Point-of-Care Data Management Software Market Analysis by Mordor Intelligence

The point-of-care data management software market size is expected to grow from USD 1.12 billion in 2025 to USD 1.27 billion in 2026 and is forecast to reach USD 2.43 billion by 2031 at 13.79% CAGR over 2026-2031. This brisk expansion springs from health systems’ pivot toward real-time diagnostics, wider government funding for flexible connectivity, and a rising preference for outcome-based reimbursement. Cloud migration, AI-driven analytics, and middleware that links hundreds of device types are now central buying criteria. Vendors able to bundle software, services, and cybersecurity safeguards stand to capture share as hospitals standardize data workflows and home-care programs scale. Consolidation among large incumbents coexists with niche innovators, creating a moderate-concentration landscape poised for steady deal activity.[1]National Institutes of Health, “Point-of-Care Technologies Research Network,” nih.gov

Key Report Takeaways

- By deployment mode, on-premises solutions held 51.62% of the point-of-care data management software market share in 2025, whereas cloud platforms are projected to post the fastest 15.88% CAGR through 2031.

- By end user, hospitals and critical-care units led with 46.15% revenue share in 2025, while home healthcare is tracking the highest 14.71% CAGR to 2031.

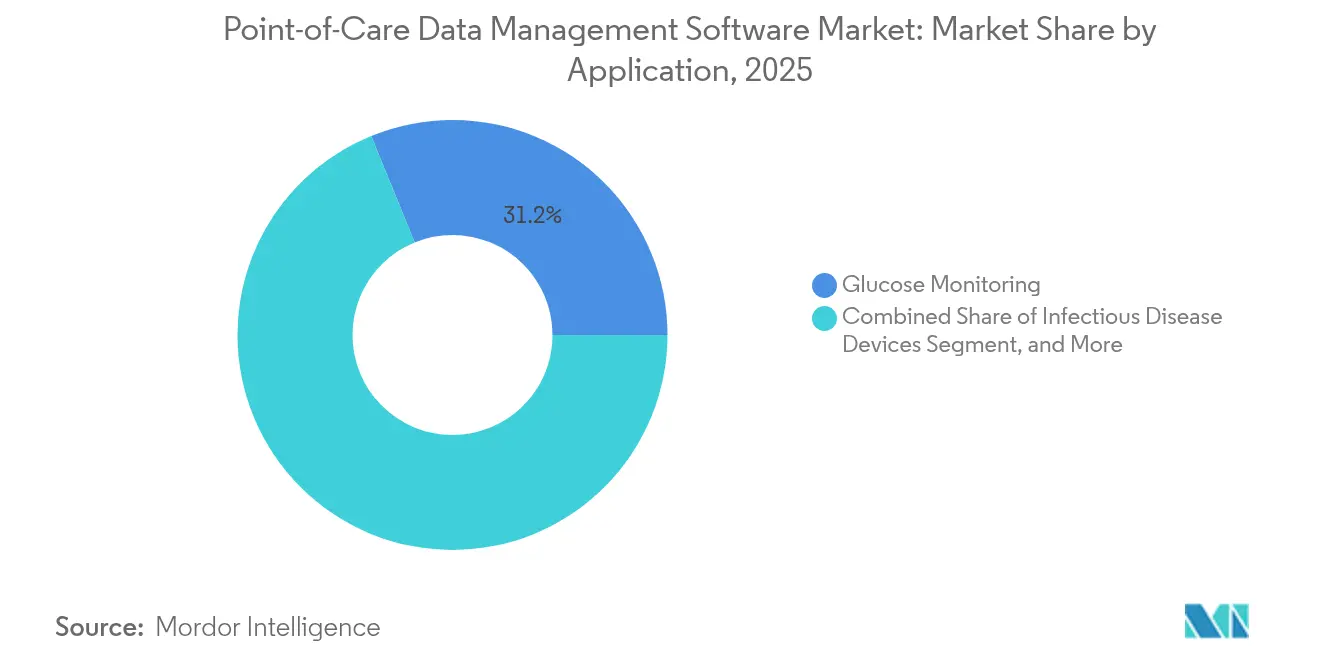

- By application, glucose monitoring accounted for 31.17% of the point-of-care data management software market size in 2025; infectious-disease testing devices are accelerating at a 15.46% CAGR over the same horizon.

- By component, middleware captured 39.61% share in 2025, yet services are projected to expand at a 16.07% CAGR as buyers seek turnkey support.

- By geography, North America remained dominant with 38.21% share in 2025, but Asia Pacific is forecast to grow the quickest at 16.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Point-of-Care Data Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in Flexible Connectivity and Interface Solutions | +2.30% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Expansion of Healthcare Infrastructure Budgets | +2.10% | Asia Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Government Funding Initiatives for POC Testing | +1.80% | North America and Europe, emerging in Asia Pacific | Short term (≤ 2 years) |

| Payor Shift Toward Outcome-Based Reimbursement | +1.60% | North America and Europe primary, limited Asia Pacific | Medium term (2-4 years) |

| AI-Driven Analytics Modules for Antimicrobial Stewardship | +1.40% | Global, with regulatory leadership in North America | Medium term (2-4 years) |

| Growing Cybersecurity Compliance Requirements | +1.20% | Global, with stringent requirements in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Innovation in Flexible Connectivity and Interface Solutions

Health systems are demanding interoperable middleware that links more than 200 distinct point-of-care devices through standardized FHIR R4 APIs, a capability spurred by CMS’s Interoperability and Patient Access Rule.[2]Centers for Medicare and Medicaid Services, “Interoperability and Patient Access Final Rule,” cms.gov Vendors now treat connectivity as core infrastructure, not add-on code, to avoid data silos and accelerate clinical decision-making. The arrival of 5G and edge-computing nodes cuts latency for cloud-native deployments, letting multi-site operators harmonize workflows across dispersed facilities. FDA’s Digital Health Software Precertification Program further elevates connectivity by embedding it in regulatory review, creating an incentive for continuous performance monitoring. As a result, buyers prioritize middleware depth and future-proof interface roadmaps when awarding contracts.

Expansion of Healthcare Infrastructure Budgets

Governments spent USD 200 billion on health-infrastructure projects in 2024, earmarking sizable funds for digital platforms that include point-of-care data management software.[4]World Health Organization, “Global Health Observatory Data Repository,” who.int Programs like India’s National Digital Health Mission and China’s Healthy China 2030 channel budget toward IT modernization, opening doors for vendors able to meet country-specific data-localization rules. Private-public partnerships often bundle software clauses into construction tenders, effectively converting optional tech into mandatory kit. As new hospitals and diagnostic centers go live, they specify analytics suites that feed value-based care dashboards, ensuring software procurement aligns with bricks-and-mortar schedules. This spends surge enlarges the addressable base in mid-income economies and smooths revenue visibility for suppliers through long-term maintenance deals.

Government Funding Initiatives for POC Testing

Federal bodies such as NIH and BARDA injected USD 3.2 billion into rapid-diagnostics programs, each grant mandating data-management compatibility from day one. The RADx portfolio alone backed 19 platforms in 2024, all of which require real-time data capture for regulatory dossiers and clinical-workflow integration. Funding calls explicitly reward AI-enhanced analytics that shorten diagnostic turnarounds, steering software roadmaps toward predictive insights. International donors, including the Global Fund, now embed digital-health criteria in grants, so vendors aligned to grant templates gain early-mover status in lower-income markets. Streamlined review pathways for government-funded prototypes also lower time-to-market, padding CAGR gains in the forecast window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Deployment and Integration Costs | -2.80% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Data Privacy and Cybersecurity Threats | -1.90% | Global, with regulatory complexity in Europe and North America | Medium term (2-4 years) |

| Fragmented Legacy Device Firmware Ecosystem | -1.50% | Global, with concentration in established healthcare markets | Medium term (2-4 years) |

| Shortage of Skilled IT Staff in Rural Facilities | -1.30% | North America and Europe rural areas, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Deployment and Integration Costs

Comprehensive rollouts cost USD 500,000-USD 2 million per facility, a hurdle that stalls adoption in smaller or rural hospitals where 40% of IT posts sit vacant. Legacy-system heterogeneity inflates interface coding and workflow redesign, often stretching timelines past budget cycles. Total cost of ownership widens when annual maintenance, staff training, and upgrade subscriptions enter the calculus. For facilities with thin patient volumes, payback models remain weak, nudging them toward grant funding or SaaS options with phased billing. Vendors able to package modular, cloud-hosted offerings at lower entry prices can unlock pent-up demand and counter this drag on CAGR.

Data Privacy and Cybersecurity Threats

Healthcare cyberattacks rose 93% in 2024, costing an average USD 4.88 million per breach, a figure that includes HIPAA fines and legal restitution. Point-of-care systems multiply network touchpoints, creating a wider attack surface that often outstrips in-house monitoring capacity. Compliance frameworks such as ISO 27001 and updated HIPAA Security rules compel continuous vulnerability scanning, encryption, and audit logging, adding recurring expense and lengthening procurement cycles. Providers risk reputational damage and payer penalties when breaches compromise outcome-based contracts, so they vet vendors for mature security postures and incident-response playbooks, factors that can elongate buying decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Migration Gains Ground Amid Legacy Strongholds

On-premises deployments still commanded 51.62% revenue in 2025, showing the historical sway of in-house servers for direct data custody. Yet cloud solutions are sprinting at a 15.88% CAGR, fuelled by robust disaster-recovery, auto-patching, and elastic storage benefits. A hybrid approach acts as a transition bridge: many systems keep latency-sensitive modules on-site while pushing analytics to HIPAA-compliant clouds. Multi-site chains prize cloud-centric dashboards that synchronize performance metrics across campuses, trimming duplicated infrastructure. FDA’s recent guidance equating validated cloud configurations with local installations further eases CIO concerns, nudging purchase orders toward SaaS models. Savings from hardware refresh deferral often finance cybersecurity upgrades, accelerating the migration curve.

Cloud vendors tout FedRAMP and HITRUST credentials to win federal and academic accounts, denting the head-start enjoyed by legacy on-premises incumbents. Rising ransomware threats also make off-site backups imperative, a default feature in many cloud contracts. Conversely, research institutes handling genomic data still lean on local clusters to maximize compute throughput. Even here, containerized workloads permit burst capacity in the cloud during peak demand, showcasing a future where line-blurring hybrid architectures dominate. Over time, service-based pricing shifts vendor focus from perpetual licenses to retention-driven roadmaps rich in AI modules and API marketplaces that monetize ecosystem participation.

By End User: Home Healthcare Rapidly Reshapes Demand Patterns

Hospitals and critical-care units retained the lion’s 46.15% share in 2025, supported by emergency-department throughput targets and lab turnaround mandates. Nevertheless, home-health programs are clocking a 14.71% CAGR, buoyed by Medicare’s Hospital-at-Home expansion and aging-population dynamics. Portable analyzers and telehealth kits feed a need for lightweight, browser-based dashboards that caregiver’s access from patient residences. Diagnostic centers integrate auto-verification rules to handle ballooning specimen loads while clinics lean on point-of-care data to shorten visit cycles under capitated payment plans.

Home-care operators grapple with variable broadband quality, propelling interest in store-and-forward architecture that syncs when connectivity resumes. Hospitals continue to invest in enterprise-wide middleware that flags quality-control drifts and consolidates reagent inventory data, improving supply chain efficiency. Outpatient clinics adopt shared-service models, licensing centralized analytics but maintaining autonomy over local device pools. The growing “other” category spanning long-term care and occupational-health sites creates opportunities for modular UI skins tailored to non-hospital workflows, widening addressable revenue.

By Application: Infectious Disease Testing Surges on Stewardship Mandates

Glucose monitoring held 31.17% share in 2025, propelled by continuous-glucose sensors and population-health programs targeting diabetes. Infectious-disease devices, however, are scaling fastest at 15.46% CAGR as antimicrobial-resistance stewardship moves from policy to practice. Labs now rely on software that auto-pushes susceptibility data into hospital formularies, enabling real-time prescribing alerts. Coagulation monitoring occupies a stable niche in cardiac and anticoagulation clinics, while urinalysis remains a high-volume staple for routine screening.

Cardiometabolic panels gain from corporate-wellness contracts that reimburse on biomarker targets, requiring near-instant scorecards. Cancer markers, though smaller, ride precision-medicine funding that mandates longitudinal data capture tied to treatment regimens. Emerging respiratory and molecular assays nest in the “other” bucket, each bringing unique QC flags and regulatory filing prerequisites. Vendors able to pre-configure application-specific report templates cut adoption friction and differentiate in RFP scoring.

By Component: Services Uptick Signals Market Maturation

Middleware led with a 39.61% slice in 2025, underscoring its role as the synaptic layer binding disparate analyzers to EHRs. Yet the services line item is pacing a 16.07% CAGR, mirroring buyers’ desire for hands-on workflow mapping, training, and 24-7 support. Software platforms now compete on AI-embedded decision support, natural-language result explanations, and mobile-first UI.

Hospitals outsourcing integration gain predictable budgets but expect continual KPI optimization, pushing vendors toward managed-service agreements. Consulting add-ons include cybersecurity audits and ISO 13485 documentation assistance, illustrating rising compliance complexity. Middleware itself grows more contextual, triggering alerts when QC coefficients deviate or reagent lots near expiry, thereby shifting value upstream from simple connectivity to actionable intelligence. Subscription bundles that pair software and services hence secure stickier revenue and deepen client lock-in.

Geography Analysis

North America maintained a 38.21% share in 2025, anchored by NIH grants, BARDA’s DRIVe program, and mature EHR penetration. U.S. hospitals deploy analytics to satisfy Medicare Advantage quality metrics, whereas Canada’s provincial systems fund rural-access upgrades that hinge on middleware interoperability. Venture capital flows and predictable FDA pathways make the region a test bed for AI-rich modules, giving suppliers early feedback loops.

Asia Pacific is set to compound at 16.52% CAGR, the fastest worldwide. China’s USD 15 billion health-digitization budget funnels into county-level hospitals eager for cloud-hosted dashboards. India’s Ayushman Bharat Digital Mission enforces interoperability, nudging buyers toward standards-compliant software. Japan leverages Society 5.0 to back aging-care pilots that marry home-monitoring kits with centralized analytics. Singapore acts as the regional deployment hub, exporting expertise across Southeast Asia. The mosaic of regulations rewards platforms sporting flexible data-sovereignty toggles and multilingual interfaces.

Europe exhibits steady, regulation-driven uptake. Germany’s Digital Healthcare Act finances hospital IT overhauls, while the United Kingdom’s NHS Digital campaign pushes all acute trusts onto a shared interoperability standard. France and Spain tap EU Recovery funds for telemedicine and lab IT modernization. Strict GDPR rules require baked-in consent management and encryption, extending deployment cycles but enhancing trust. Suppliers that pre-validate compliance templates gain bidding advantages. South America, the Middle East, and Africa trail in share but post mid-teens growth as public-private buildouts stipulates digital kits from the outset.

Competitive Landscape

The point-of-care data management software market shows moderate concentration: top multinationals carry sizable reach, yet local specialists still thrive. Siemens Healthineers, Abbott, and Danaher engineer end-to-end ecosystems, often buying niche firms to plug feature gaps, as seen in Siemens’ USD 16.4 billion Varian deal. Their scale yields bundled pricing across devices, middleware, and support.

Emerging challengers harness cloud-native microservices, AI-driven antimicrobial alerts, and zero-trust security frameworks to woo greenfield deployments. They exploit incumbent technical debt, especially among legacy on-premises suites slow to adopt open APIs. Cybersecurity posture now doubles as a sales lever; platforms boasting ISO 27001 and SOC 2 Type II audits shorten procurement cycles in North America and Europe.

Outcome-based reimbursement pressures favour vendors that correlate device data with length-of-stay or readmission reductions, which can be validated in payer negotiations. Strategic alliances with EHR giants or 5G telcos also surface as differentiators, supplying embedded distribution channels. As consolidation continues, bolt-on valuations trend upward, pushing innovators either toward premium exits or specialized niches like home-care analytics.

Point-of-Care Data Management Software Industry Leaders

Siemens Healthineers AG + (Conworx)

Abbott Point of Care Inc. + (Alere)

Danaher Company (HemoCue and Radiometer Medical ApS)

Roche Diagnostics Corporation

TELCOR Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2022: Roche Diagnostics added an AI audit-trail module to its digital pathology suite, enabling automated QC checks before result sign-off.

- December 2025: Masimo began U.S. rollout of its cloud-linked vital-signs hub that streams data directly into clinician dashboards.

- September 2025: Siemens Healthineers closed the USD 16.4 billion Varian Medical Systems acquisition, creating an integrated oncology workflow.

- October 2025: Abbott debuted a next-gen continuous-glucose monitor featuring predictive alerts that sync with major EHRs.

Global Point-of-Care Data Management Software Market Report Scope

The study tracks the point-of-care data management integration software that would allow remote access of the POCT devices by acting as an interface between LIS and EMR solutions. The tool primarily aids the stakeholders in making quick clinical and diagnostic decisions, resulting in an analytics interface across multiple platforms while ensuring patient satisfaction.

The Point-of-Care Data Management Software Market is segmented by End User (Hospitals/Critical Care Units, Diagnostic Centers, Clinics/Outpatient), Application (Infectious Disease Devices, Glucose Monitoring, Coagulation Monitoring, Urinalysis, Cardiometabolic Monitoring, Cancer Markers, Hematology), and Geography.

| Cloud-Based |

| On-Premise |

| Hybrid |

| Hospitals / Critical Care Units |

| Diagnostic Centers |

| Clinics / Outpatient |

| Home Healthcare |

| Other End Users |

| Infectious Disease Devices |

| Glucose Monitoring |

| Coagulation Monitoring |

| Urinalysis |

| Cardiometabolic Monitoring |

| Cancer Markers |

| Hematology |

| Other POC Applications |

| Software Platform |

| Middleware |

| Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Hospitals / Critical Care Units | |

| Diagnostic Centers | ||

| Clinics / Outpatient | ||

| Home Healthcare | ||

| Other End Users | ||

| By Application | Infectious Disease Devices | |

| Glucose Monitoring | ||

| Coagulation Monitoring | ||

| Urinalysis | ||

| Cardiometabolic Monitoring | ||

| Cancer Markers | ||

| Hematology | ||

| Other POC Applications | ||

| By Component | Software Platform | |

| Middleware | ||

| Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the point-of-care data management software market in 2026?

The market stands at USD 1.27 billion in 2026 and is on track to reach USD 2.43 billion by 2031.

What is the expected CAGR for point-of-care data platforms through 2031?

Industry revenue is projected to climb at a 13.79% compound annual growth rate through 2031.

Which deployment model is growing the fastest?

Cloud-based deployments show the quickest rise, advancing at a 15.88% CAGR as hospitals shift workloads off-premise.

Why is Asia Pacific considered the most attractive growth region?

Government digitization drives, including India's Ayushman Bharat and China's Healthy China 2030, fuel a 16.52% CAGR for the region.

Which application segment is expanding most rapidly?

Infectious-disease testing devices lead growth, rising at a 15.46% CAGR on the back of antimicrobial stewardship policies.

What are the key barriers to adoption?

High integration costs and cybersecurity compliance requirements remain the foremost hurdles for prospective buyers.

Page last updated on: