Software As A Medical Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.24 Billion |

| Market Size (2031) | USD 25.87 Billion |

| Growth Rate (2026 - 2031) | 37.62% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software As A Medical Device Market Analysis by Mordor Intelligence

The Software as a Medical Device market size is expected to grow from USD 3.81 billion in 2025 to USD 5.24 billion in 2026 and is forecast to reach USD 25.87 billion by 2031 at 37.62% CAGR over 2026-2031. Sharply rising clinical validation of artificial-intelligence algorithms, the maturation of cloud-native architectures, and payer adoption of new reimbursement codes collectively anchor the Software as a Medical Device market on an accelerated growth path. Smartphone and tablet proliferation supplies a ready platform for clinically cleared apps, while edge AI chips in consumer wearables move real-time inference out of the cloud and deeper into patients’ daily routines. Regulators have responded with streamlined change-control pathways, allowing continuous-learning software to iterate without lengthy re-filings. At the same time, cross-border data-privacy laws are forcing regional deployment strategies that temper the otherwise global reach of SaMD solutions.

Key Report Takeaways

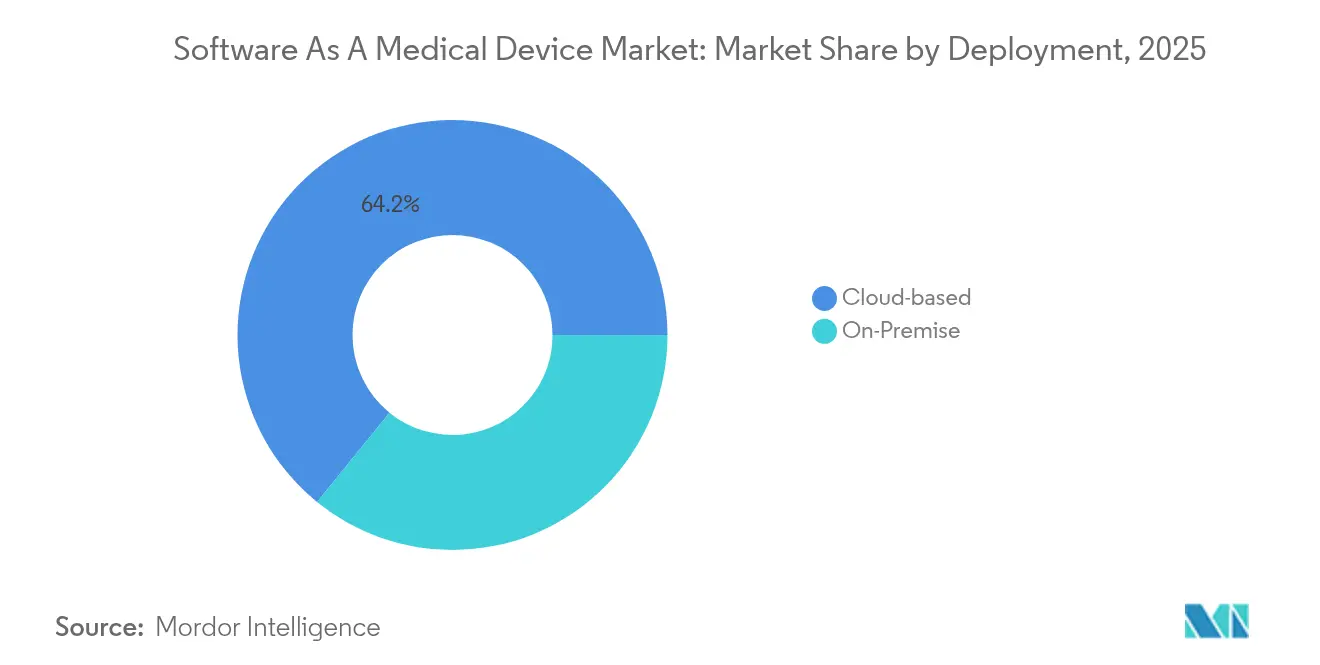

- By deployment, cloud-hosted solutions held 64.15% revenue share in 2025; hybrid and pure-cloud models together are forecast to expand at a 44.9% CAGR through 2031.

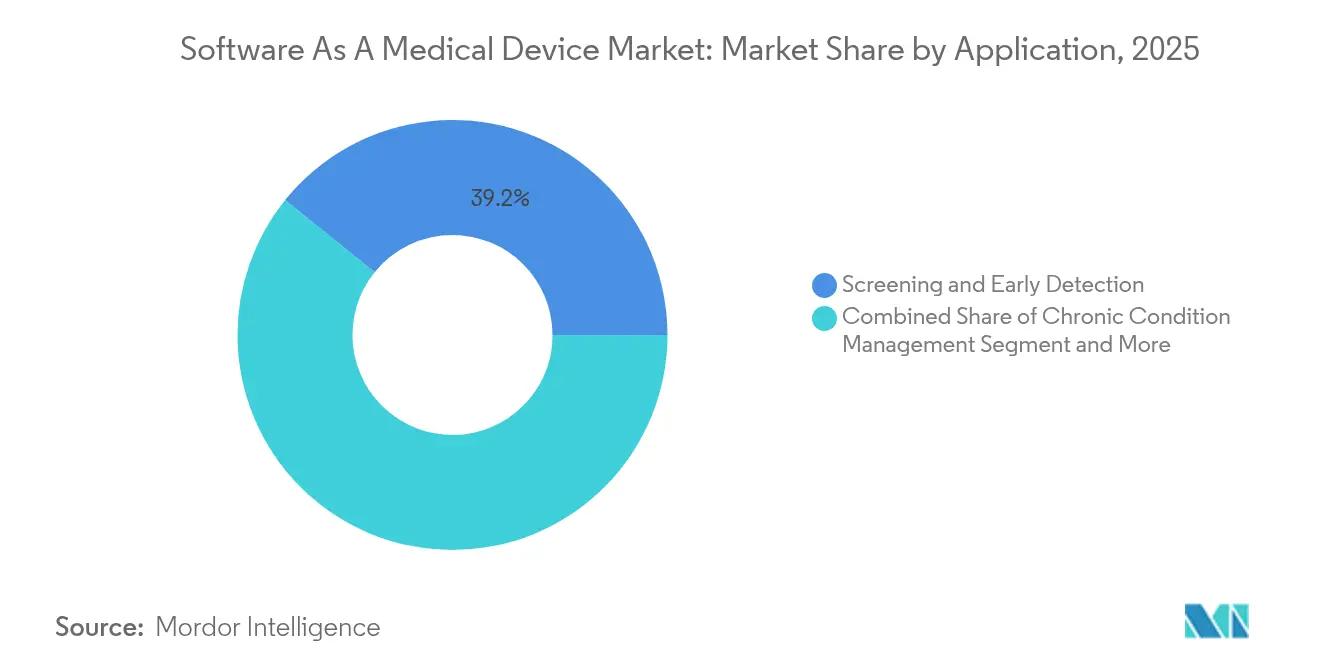

- By application, screening and early detection accounted for 39.20% of the Software as a Medical Device market size in 2025, while chronic-condition management is advancing at a 39.9% CAGR to 2031.

- By end-user, hospitals and clinics contributed 41.05% revenue in 2025, yet home-care settings are poised for the highest 42.2% CAGR over the next five years.

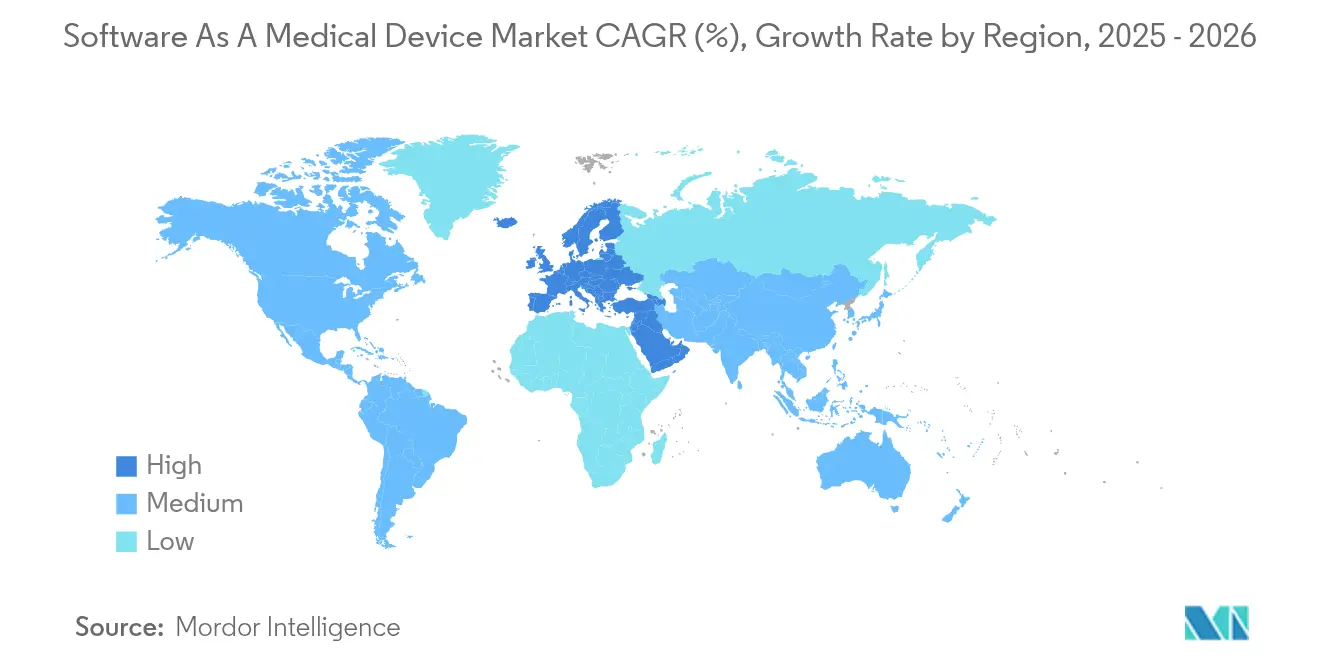

- By region, North America commanded 41.30% share in 2025; Europe is projected to post the quickest 43.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Software As A Medical Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid AI/ML algorithm validation tool-chains | +8.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Growth of chronic-disease remote monitoring programs | +7.2% | Global, particularly strong in North America and Asia-Pacific | Long term (≥ 4 years) |

| Smartphone sensor accuracy now matching Class II hardware | +6.8% | Global, led by consumer electronics adoption | Short term (≤ 2 years) |

| Reimbursement codes for digital therapeutics (DTx) | +5.9% | North America primarily, expanding to EU | Medium term (2-4 years) |

| Under-the-radar – FDA "streamlined real-world-data" pilots for SaMD updates | +4.3% | North America, with regulatory spillover globally | Long term (≥ 4 years) |

| Under-the-radar – Edge-inference chips inside wearables enabling offline SaMD | +3.8% | Global, with manufacturing concentration in Asia-Pacific | Medium term (2-4 years) |

| Rapid AI/ML algorithm validation tool-chains | +8.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid AI/ML Algorithm Validation Tool-chains

The United States Food and Drug Administration has cleared more than 520 AI-enabled medical devices to date, a milestone made possible by predetermined change-control plans that let developers update models without full re-submission.[1]U.S. Food and Drug Administration, “Artificial Intelligence and Machine Learning (AI/ML) Enabled Medical Devices List,” fda.gov Continuous-learning releases transform six-month update cycles into sub-one-month deployments, giving first movers durable competitive speed. Venture capital mirrored that confidence, sending USD 11 billion toward healthcare AI startups in 2024, a quarter of all digital-health funding. Scaled real-world-evidence frameworks further tighten the post-market feedback loop, boosting both safety monitoring and marketing claims.

Growth of Chronic-Disease Remote-Monitoring Programs

At NYU Langone Health, an ambulatory program enrolling 8,000 patients lifted data-submission adherence to 58.7% and lowered acute-care utilization.[2]NEJM Catalyst, “Ambulatory Remote Patient Monitoring at Scale,” catalyst.nejm.org Similar successes across cardiology and endocrinology have nudged payers toward permanent RPM benefit design; the 2025 Medicare Physician Fee Schedule creates bundled codes that reimburse care-team time spent managing SaMD-sourced vitals. Asia-Pacific pilots echo those gains: a diabetes-management platform in Tianjin cut fasting glucose 1.68% and HbA1c 0.45% across thousands of users. These outcomes justify large-scale rollouts and lock in long-term demand.

Smartphone Sensor Accuracy Now Matching Class II Hardware

Clinical studies report smartwatch photoplethysmography detecting atrial fibrillation with 94.8% sensitivity and 95% specificity.[3]A. Vaidya et al., “Smartwatch Photoplethysmography for Atrial Fibrillation Detection,” JACC: Advances, academic.oup.com Separate trials find smartphone-based pulse-oximetry meeting the FDA/ISO 80601 accuracy limit of ±3 SpO₂ points, achieving RMS deviations of 2.6%. These validations—plus Samsung’s FDA-cleared sleep-apnea algorithm—expand the addressable Software as a Medical Device market beyond clinical walls into everyday life.

Reimbursement Codes for Digital Therapeutics (DTx)

New HCPCS Level II code A9291 and three 2025 G-codes now compensate physicians for prescribing FDA-authorized digital therapeutics and managing patient-generated data. Commercial insurers are following suit, creating a predictable revenue path that dismantles a core adoption barrier. Massachusetts Medicaid, for example, already reimburses covered DTx statewide, accelerating patient access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented global cyber-security/ISO 81001-5-1 compliance costs | -4.7% | Global, with varying regional requirements | Medium term (2-4 years) |

| Data-privacy legislation limiting cross-border health-clouds | -3.9% | EU-US primarily, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Under-the-radar – Smartphone OS API deprecations that break legacy SaMD apps | -2.8% | Global, affecting iOS and Android ecosystems | Short term (≤ 2 years) |

| Under-the-radar – Limited actuarial evidence for DTx long-term cost savings | -2.1% | North America and EU insurance markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Global Cyber-security / IEC 81001-5-1 Compliance Costs

SaMD vendors must now align with the new IEC 81001-5-1 secure-development lifecycle while also updating technical files for EU MDR and, soon, the European AI Act. Non-compliance carries fines up to EUR 35 million or 7% of global turnover. Similar guidance from the FDA demands threat-model documentation and vulnerability patching. The multi-layered rules increase certification timelines and favor enterprises with in-house regulatory teams, slowing smaller entrants.

Data-privacy Legislation Limiting Cross-border Health Clouds

Florida’s Electronic Health Records Exchange Act obliges US-based storage for covered entities, while the US Department of Justice will restrict transfers of sensitive health data to designated countries effective April 2025. Parallel GDPR stipulations remain unresolved despite successive EU-US frameworks, compelling SaMD providers to spin up region-specific data stacks. The duplication erodes scale economies and complicates algorithm training that depends on large, heterogeneous datasets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Despite Privacy Pressures

Cloud platforms captured 64.15% revenue in 2025 and will compound at a 44.9% CAGR, outpacing on-premise deployments. Interoperability APIs, containerised micro-services, and auto-scaling databases collectively reduce hospital IT overhead and speed new-feature rollouts. These benefits keep the Software as a Medical Device market biased toward public-cloud elasticity, even as data-sovereignty rules necessitate in-country availability-zones.

On-premise and hybrid architectures survive where institutional risk tolerance demands physical control of protected health information. Hospitals often meter image uploads to the cloud while retaining raw DICOM files in local archives, a split design that balances latency with privacy. Edge computing further blurs boundaries by preprocessing ECG or glucose streams locally, then pushing anonymised insights to central servers. Thus, the market’s future will likely see co-existing models that trade pure-cloud convenience for jurisdiction-level compliance.

By End-user: Home-care Transformation Accelerates

Hospitals and clinics held 41.05% of 2025 revenue, leveraging mature electronic health record interfaces that pull SaMD outputs directly into clinical workflows. Decision-support modules flag deteriorating vitals, letting nurses intervene before escalation. However, home-care environments are positioned for a 42.2% CAGR, the swiftest end-user rise in the Software as a Medical Device market. Medicare’s expanded RPM codes finance remote blood-pressure and glucose telemetry, while user-friendly mobile UI designs reduce technical friction for seniors.

Ambulatory and specialty centers adopt SaMD for episodic but high-acuity use cases such as post-stroke perfusion analysis, where time-to-treatment is pivotal. Greater data continuity from home-based sensors feeds AI risk-scoring engines that schedule earlier specialist follow-ups. Over time, hospitals may act more as data-integration hubs than as primary data generators, closing the feedback loop between clinicians and patients in their living rooms.

By Application: Chronic-care Management Gains Momentum

Screening and early detection retained 39.20% of the Software as a Medical Device market size in 2025, supported by autonomous fundoscopy and dermoscopy algorithms that triage large populations within minutes. These high-volume cases deliver rapid ROI by preventing costly late-stage interventions. Chronic-condition management, meanwhile, is projected to deliver a 39.9% CAGR, fueled by aging demographics and value-based-care contracts that reward controlled HbA1c and blood-pressure metrics.

Digital therapeutics layer evidence-based behavior modification atop monitoring streams, forming closed-loop care pathways. Real-time alerts encourage medication titration before acute episodes occur, cutting readmissions. Clinical-decision-support engines, often embedded in EHR side-panels, synthesize multi-parameter data into succinct recommendations, aiding time-pressed physicians.

By IMDRF Risk Class: Category III Complexity Drives Innovation

Category I solutions—ranging from wellness coaching to basic heart-rate tracking—accounted for 47.25% revenue in 2025 thanks to minimal regulatory overhead and mass-market reach. Their dominance illustrates how consumer channels remain an entry point into the Software as a Medical Device market. Category III products, however, will expand at a 39.1% CAGR as developers progress toward autonomous diagnosis and treatment recommendations. Regulatory pathways now clarify the evidence threshold, encouraging higher-risk innovations.

Category II applications such as glucose-trend prediction gain from real-world-data extensions that lower trial costs. Category IV devices remain niche but strategic; they incorporate advanced radiomics and multi-omics decision engines that demand both algorithmic transparency and longitudinal surveillance. Collectively these tiers showcase a maturation from lifestyle guidance to software that informs or even directs clinical care.

Geography Analysis

North America contributed 41.30% of global revenue in 2025, underpinned by Medicare reimbursement codes and an FDA pipeline that already lists more than 520 cleared AI/ML devices. Providers benefit from long-standing EHR penetration, which makes integration and order-set updates relatively straightforward. Nonetheless, statutes such as Florida’s Electronic Health Records Exchange Act complicate multi-region deployments and increase compliance staffing burdens.

Europe is forecast to post the quickest regional CAGR at 43.2% to 2031. Full enforcement of the EU Medical Device Regulation and the incoming AI Act provide harmonised guardrails that balance patient safety with innovation. Germany’s DiGA process offers a clear reimbursement path for app-based therapeutics, while France’s PECAN scheme reimburses remote-monitoring bundles. Yet Germany’s strict cloud-processing restrictions can raise operating costs for vendors reliant on centralised data-lakes.

Asia-Pacific represents the next frontier. China’s digital-health pilots in Tianjin achieved measurable metabolic improvements, validating large-scale SaMD adoption. Japan fast-tracked algorithmic diagnosis of cerebral infarction, reflecting governmental intent to offset clinical-staff shortages. In parallel, a Saudi Arabian heart-health program developed by Bayer and Huma aligns with Vision 2030 ambitions to digitise preventive care. Market fragmentation persists, but local manufacturing of sensors and phones supplies cost-efficient hardware platforms that facilitate rapid scaling.

Competitive Landscape

The Software as a Medical Device market is moderately fragmented. Medtronic, which reported USD 33.5 billion in FY 2025 sales, continues to embed smart-algorithms into legacy hardware portfolios, edging closer to full software-hardware convergence. Big-tech players Apple and Google exploit mobile-OS dominance to seed health APIs that third-party developers convert into reimbursable modules. Their cloud, AI, and device ecosystems shorten development cycles for partners, amplifying network effects.

Specialist vendors such as Digital Diagnostics focus narrowly on autonomous ophthalmology, securing breakthrough-device designations that deter direct competitors. Biofourmis and Closed Loop Medicine concentrate on adaptive therapeutics, pairing drug regimens with real-time phenotypic feedback. Strategic moves illustrate converging playbooks: NVIDIA and Medtronic formed a joint platform to speed model deployment inside the OR, while Viz.ai inked a multi-year pact with Bristol Myers Squibb to identify hypertrophic cardiomyopathy earlier. Each alliance aims to pull recurring SaaS revenue from clinical pathways that once generated only episodic device sales.

Regulatory mastery now serves as a gating competitive advantage. Enterprises that operationalise IEC-81001 secure-development cycles and maintain living technical dossiers can push software updates weekly, versus quarterly for less-prepared rivals. Meanwhile, localisation of cloud stacks in Europe and certain US states adds overhead that smaller firms must absorb or pass along in pricing.

Software As A Medical Device Industry Leaders

Siemens Healthcare

Medtronic plc

Philips

GE Healthcare

Roche

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Median Technologies obtained up to €47.5 million to file and commercialise its AI lung-cancer diagnostic SaMD, eyonis, in the United States.

- March 2025: XUND raised €6 million in pre-Series A funding to scale its MDR-certified SaMD across Europe.

- March 2024: NVIDIA partnered with Medtronic to accelerate AI-based SaMD development in diagnostics and treatment.

- March 2024: Viz.ai entered a multi-year agreement with Bristol Myers Squibb to deploy its Viz HCM algorithm for hypertrophic cardiomyopathy detection.

Global Software As A Medical Device Market Report Scope

Software as a Medical Device (SaMD) refers to software intended for medical purposes, either independently or in conjunction with other medical devices, yet not integrated into a hardware device. SaMD is crafted to execute distinct medical functions like diagnosing, monitoring, preventing, or treating diseases and is specifically designed for the healthcare environment.

The study tracks the revenue accrued through the sale of software as a medical device by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The software as a medical device market is segmented by device type (laptops/PCs, smartphones/tablets, and wearable devices), deployment (cloud-based and on-premise), and geography (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Cloud-based |

| On-Premise |

| Hospitals and Clinics |

| Ambulatory / Specialist Centers |

| Home Care Settings |

| Screening and Early Detection |

| Chronic Condition Management |

| Digital Therapeutics |

| Clinical Decision Support |

| Category I |

| Category II |

| Category III |

| Category IV |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment | Cloud-based | ||

| On-Premise | |||

| By End-user | Hospitals and Clinics | ||

| Ambulatory / Specialist Centers | |||

| Home Care Settings | |||

| By Application | Screening and Early Detection | ||

| Chronic Condition Management | |||

| Digital Therapeutics | |||

| Clinical Decision Support | |||

| By IMDRF Risk Class | Category I | ||

| Category II | |||

| Category III | |||

| Category IV | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the exceptional CAGR of the Software as a Medical Device market?

Continuous-learning AI pathways at the FDA, new reimbursement codes for digital therapeutics, and clinical-grade sensors in consumer wearables combine to propel a 37.62% CAGR toward 2031.

How do new Medicare codes affect market adoption?

HCPCS A9291 and three 2025 G-codes reimburse clinicians for prescribing and managing SaMD, providing a sustainable revenue channel that accelerates uptake in the United States.

Why is Europe expected to outpace North America in growth?

Clarified rules under the EU Medical Device Regulation and forthcoming AI Act create regulatory certainty, while reimbursement pathways like Germany’s DiGA expedite commercialisation.

What are the main obstacles vendors face when scaling globally?

Fragmented cyber-security standards and data-localisation laws force region-specific deployments, raising compliance costs and elongating launch timelines.

Which risk class will see the greatest innovation?

Category III applications—those offering diagnostic or treatment recommendations—will expand fastest as real-world-evidence frameworks lower the barrier to higher-risk software approvals.

Page last updated on: