Big Data Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

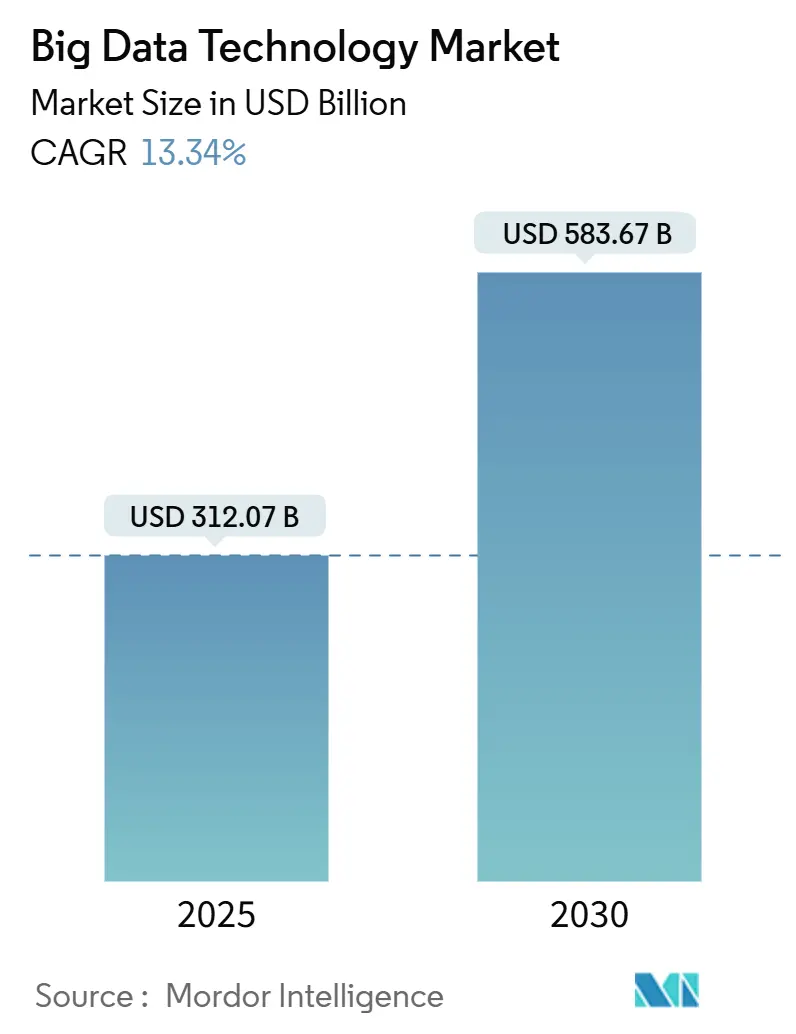

| Market Size (2025) | USD 312.07 Billion |

| Market Size (2030) | USD 583.67 Billion |

| Growth Rate (2025 - 2030) | 13.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Big Data Technology Market Analysis by Mordor Intelligence

The big data technology market size is projected to reach USD 583.67 billion by 2030, advancing at a 13.34% CAGR from USD 312.07 billion in 2025. Organizations are transitioning from passive storage to intelligent platforms that incorporate real-time analytics, machine learning inference, and distributed processing across hybrid environments. Services currently command the largest revenue slice, yet software is adding the most incremental value as enterprises standardize on cloud-agnostic toolchains. The growing reliance on public cloud regions, combined with sovereignty obligations, encourages hybrid deployment, while consumption-based pricing draws small and medium-sized enterprises into advanced analytics. Industry demand is especially strong in banking and healthcare, where low-latency fraud prevention and genomics workloads require specialized infrastructure. Competitive dynamics reflect moderate concentration, with the top five vendors capturing approximately 35% of the 2024 software revenue, leaving room for specialists in edge analytics and privacy-preserving computation.

Key Report Takeaways

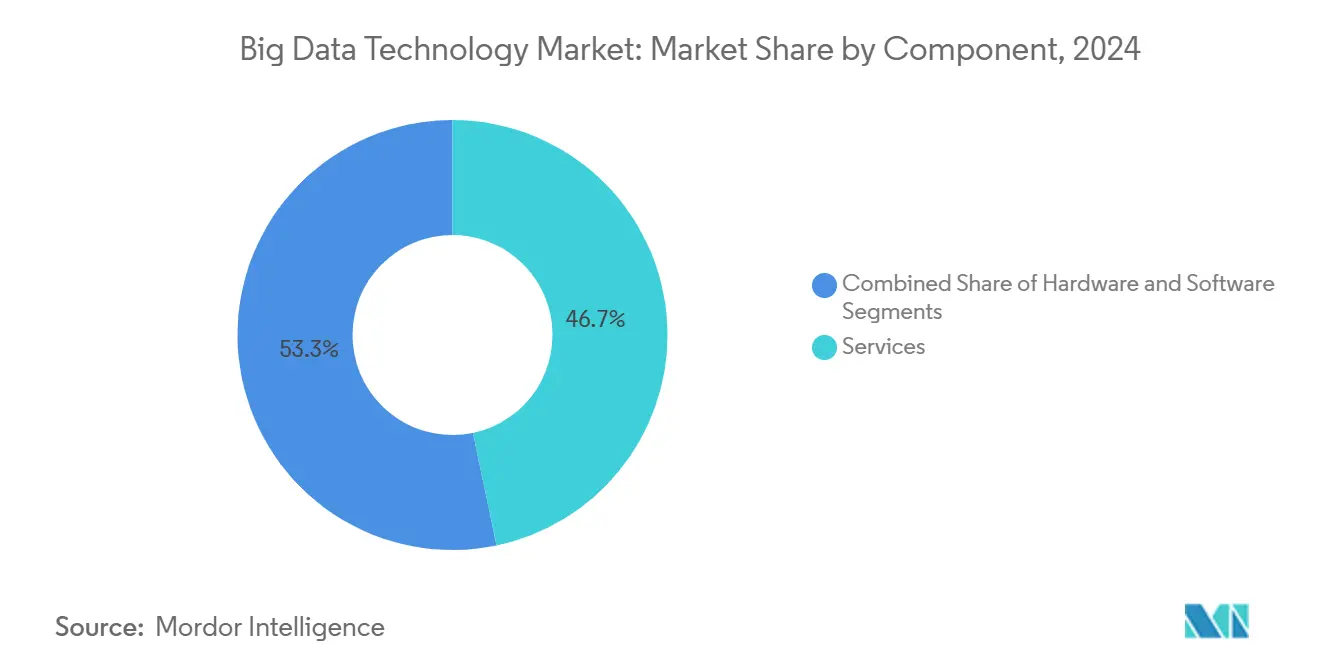

- By component, services led with 46.72% of the big data technology market share in 2024, while software is forecast to post a 13.89% CAGR to 2030.

- By deployment model, cloud held 61.22% of the big data technology market share in 2024; hybrid configurations are set to expand at a 13.94% CAGR through 2030.

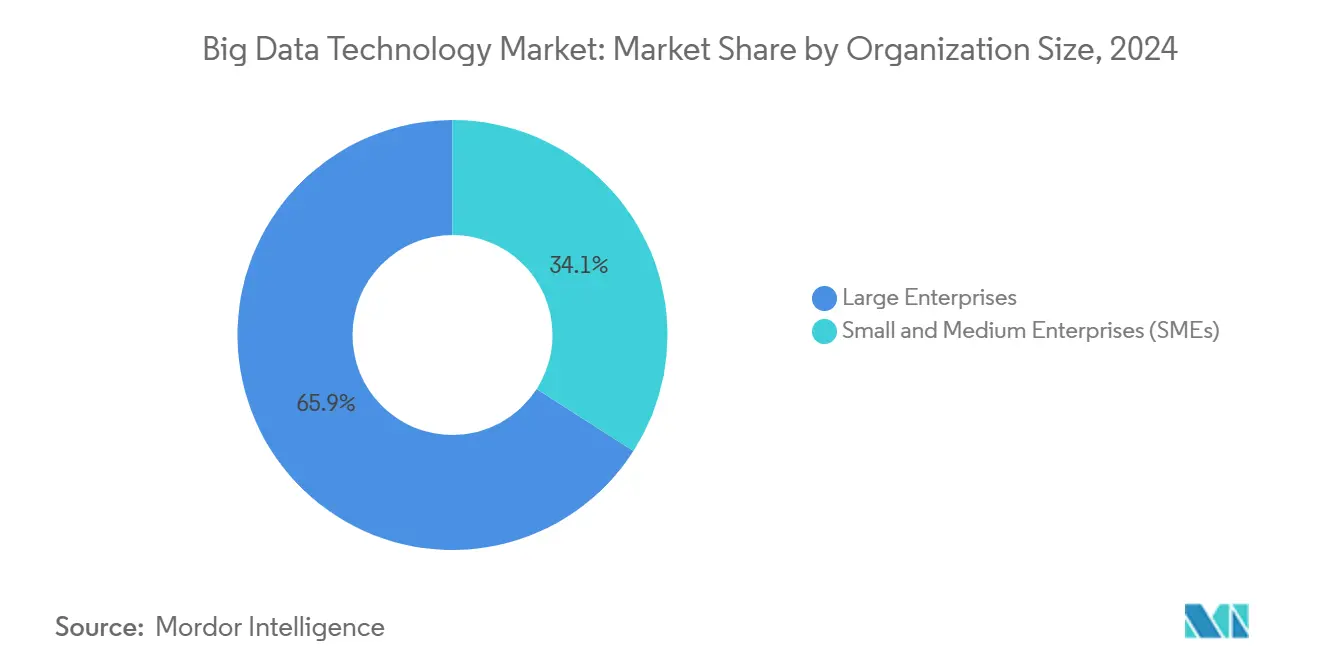

- By organization size, large enterprises accounted for 65.93% of the big data technology market share in 2024, whereas small and medium enterprises are growing at the fastest rate, with a 13.66% CAGR.

- By industry vertical, banking, financial services, and insurance are projected to deliver 25.67% of the big data technology market share in 2024; healthcare and life sciences are expected to rise at a 15.13% CAGR.

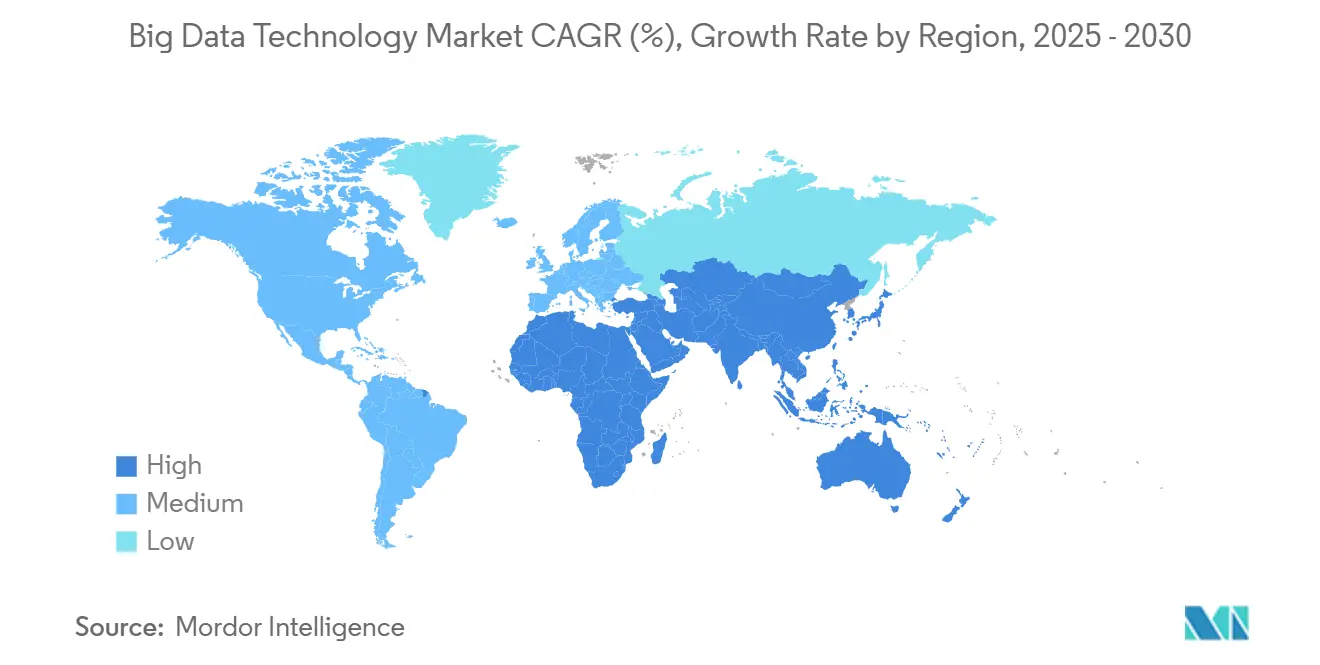

- By geography, North America retained a 37.19% of the big data technology market share in 2024; however, the Asia-Pacific region is on track for a 14.41% CAGR to 2030.

Global Big Data Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Cloud Adoption | +3.2% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Exponential Growth in Data Volume | +2.8% | Global, with emphasis on Asia-Pacific | Long term (≥ 4 years) |

| Advancements in AI and Machine Learning | +2.5% | North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Real-Time Analytics | +2.1% | Global, early uptake in BFSI and telecommunications | Short term (≤ 2 years) |

| Emergence of Data Fabric Architecture | +1.6% | North America and Europe | Long term (≥ 4 years) |

| Proliferation of Data Exchanges and Marketplaces | +1.1% | North America and Europe, early stage elsewhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Cloud Adoption

Cloud services captured 61.22% of 2024 revenue, and capital spending by hyperscalers exceeded USD 200 billion that year. Microsoft dedicated close to 40% of its 2024 infrastructure budget to AI-optimized instances that speed model training tenfold.[1]Microsoft, “Azure Capital Expenditure 2024,” Microsoft.com Amazon plans USD 75 billion of additional capacity through 2025 to support data-local workloads in India and Saudi Arabia. These investments lower entry barriers for analytics, shorten hardware refresh cycles, and motivate enterprises to consolidate platforms to curb egress costs. As a result, cloud adoption is forecast to lift overall demand while redirecting spending from on-premise hardware to subscription software.

Exponential Growth in Data Volume

Global data creation hit 181 zettabytes in 2025 and is on pace for 1 yottabyte by 2030.[2]Ericsson, “Mobility Report 2025,” Ericsson.com Mobile traffic is climbing 25% a year, with augmented-reality video driving three-quarters of bandwidth. Huawei projects that 40% of enterprise data will be processed at the edge by 2028, fragmenting analytics across devices. Volume pressure forces tiered storage strategies that automate data migration from hot to cold tiers, trimming costs by up to 60%. Vendors that streamline lifecycle management gain an advantage as organizations struggle to balance cost, compliance, and performance.

Advancements in AI and Machine Learning Integration

Confluent found that 84% of data leaders gained at least twice their investment from real-time streaming platforms that feed machine-learning models.[3]Confluent, “Real-Time Data Streaming ROI Survey 2024,” Confluent.io Google Cloud reported 79% of customers now run AI workloads through managed services, with natural-language and vision tasks rising 45% year on year. Databricks added automated lakehouse monitoring in 2024 to retrain models when data drift appears. Together these advances blur lines between business intelligence and data science, embedding predictive functions directly into operational applications and accelerating time-to-value.

Rising Demand for Real-Time Analytics

Confluent noted that 86% of enterprises prioritized real-time stream processing in 2024, particularly for fraud detection and dynamic pricing. Snowflake’s dynamic tables keep dashboards current via incremental refresh, lowering compute outlay by 70% for high-frequency aggregates. Telecommunications operators now adjust routing paths in milliseconds, cutting congestion by up to 30%. The need for immediacy is reshaping architectures around change-data-capture and event streaming, sidelining batch-oriented warehousing models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Infrastructure | -2.4% | Global, highest impact in emerging markets | Medium term (2-4 years) |

| Shortage of Skilled Big Data Professionals | -1.9% | Global, severe in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Growing Data Sovereignty Regulations | -1.5% | European Union, China, India | Medium term (2-4 years) |

| Energy Consumption Concerns in Data Processing | -0.8% | Global, regulatory scrutiny in European Union and California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Infrastructure

Meta invested USD 38-40 billion in 2024 to secure advanced data centers, including liquid-cooled hardware with power-usage effectiveness below 1.1. Oracle spent USD 6.9 billion during the same period to broaden its global cloud footprint. Enterprises lacking such budgets find on-premises clusters expensive, with a minimal Hadoop setup still demanding USD 500,000 before software and staffing. Although pay-as-you-go cloud services cut capital outlays, intensive data movement can make total cost of ownership higher in the long run. Cost hurdles therefore slow adoption among mid-market firms and in regions where financing options are scarce.

Shortage of Skilled Big Data Professionals

McKinsey estimated 3.5 million data roles remained unfilled in 2024, driving salaries for experienced engineers to USD 120,000-150,000 in major U.S. hubs. PwC found 60% of enterprises launched reskilling programs, yet most courses last six months or more before participants become productive. Talent scarcity forces organizations to use managed services that hide infrastructure complexity, but reliance on outside providers raises lock-in risk and can inflate long-term costs. The skills gap is particularly acute in Asia-Pacific and Middle East and Africa, limiting regional project velocity despite rising demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Anchor Revenue While Software Captures Innovation Premium

Services contributed 46.72% of 2024 revenue, underscoring the reliance on integrators and managed providers when stitching together multi-cloud analytics ecosystems. A typical professional-services engagement ranges from USD 500,000 to USD 5 million and includes architecture design, migration, and change-management training. Managed contracts then supply ongoing monitoring, patching, and optimization. Meanwhile, software is forecast to grow at a 13.89% CAGR as vendors supply consumption-based licenses and embed generative AI that converts natural-language prompts into code.

Adoption of data-management software accelerates in response to the EU Data Act and California Consumer Privacy Act, which mandate documented data lineage. Analytics packages layer visualization, modeling, and collaboration features atop governed data stores, allowing line-of-business users to explore information without SQL expertise. Hardware demand lags as cloud infrastructure absorbs compute growth. Yet specialized appliances with GPUs or tensor accelerators—retain a niche for latency-sensitive tasks such as fraud scoring.

By Deployment Model: Hybrid Configurations Balance Sovereignty and Elasticity

Cloud offerings made up 61.22% of 2024 sales, reflecting the draw of elastic capacity, but sovereign-data rules compel organizations to keep certain workloads on-premise. Hybrid setups are set to expand 13.94% a year through 2030, blending local data retention with remote analytics services. Financial institutions process card transactions within domestic data centers for compliance, while training anonymized risk models in the cloud. Healthcare providers likewise maintain electronic health records on site under HIPAA, exporting genomics workloads to high-memory cloud nodes.

Hybrid frameworks raise governance complexity, demanding unified identity and security policies across environments. Kubernetes orchestration, container images, and infrastructure-as-code help standardize deployment pipelines, letting teams move jobs between clusters as prices or capacity shift. On-premise installations remain essential for ultra-low-latency control systems, yet their share of total spending continues to fall.

By Organization Size: SMEs Leverage Cloud Economics to Close Capability Gaps

Large enterprises absorbed 65.93% of 2024 spending, driven by petabyte-scale datasets and stringent latency targets. However, small and medium enterprises are projected to advance at a 13.66% CAGR as consumption-based cloud services lower entry hurdles. Roughly 60% of SMEs now run SaaS analytics, up from 45% two years earlier. Providers court this cohort with free tiers, such as BigQuery’s 1 terabyte monthly allowance and template dashboards for customer churn, marketing attribution, and inventory optimization.

Larger corporations, by contrast, explore federated architectures that decentralize query rights while centralizing governance. This structure empowers business units yet preserves enterprise-wide standards. As SMEs mature, many adopt similar federated patterns to avoid data silos, underscoring convergence in architectural best practice across organization sizes.

By Industry Vertical: BFSI Leads Spending While Healthcare Accelerates Fastest

The BFSI sector delivered 25.67% of 2024 demand, anchored by real-time payment processing and regulatory reporting. JPMorgan Chase alone invested USD 17 billion in technology that year, allocating roughly 30% to data infrastructure upgrades. Banks worldwide deploy AI fraud models that cut false positives up to 60% compared with rule-based systems. Healthcare and life sciences, growing at a 15.13% CAGR, use genomics analytics and continuous patient monitoring to tailor interventions. Mayo Clinic’s precision-medicine pipelines process petabytes of sequence data, demonstrating the depth of data growth in this vertical.

Retail, manufacturing, telecommunications, and energy also intensify analytics adoption, but at more moderate rates. Amazon attributes about 35% of revenue to recommendation engines tuned by big data, while Siemens deploys predictive maintenance software that trims unplanned downtime up to 50%. Such cross-sector traction highlights the broad relevance of the big data technology market.

Geography Analysis

North America accounted for 37.19% of 2024 revenue, benefiting from sustained hyperscaler capital outlays and a U.S. federal cloud-first policy that mandates machine-readable public data sets. The CHIPS and Science Act’s USD 52 billion incentive pool is expected to strengthen domestic chip supply, easing server procurement risks. Canada’s Digital Charter Implementation Act stresses data portability and algorithmic transparency, stimulating demand for lineage and governance tools. Mexico emerges as a near-shore data-center hub for continental firms seeking lower latency to Latin American users.

Asia-Pacific is projected to log the fastest regional growth at 14.41% CAGR through 2030. China’s 14th Five-Year Plan classifies big data infrastructure as a strategic priority, and India’s Unified Payments Interface now handles over 13 billion monthly transactions that require sub-second fraud analytics. Japan’s Society 5.0 initiative embeds sensors in manufacturing lines to feed AI quality control, while South Korea’s K-Digital Platform expands 5G and edge computing to support autonomous mobility. Australia mandates domestic data residency for critical-infrastructure entities, reinforcing hybrid deployments that keep sensitive datasets local.

Europe faces slower expansion because the Data Act forces parallel processing environments for cross-border data flows, driving cost without commensurate revenue gains. GDPR fines total EUR 4.5 billion to date, sustaining demand for compliance solutions. Sovereign cloud projects such as Gaia-X seek independence from U.S. providers but still lack parity on price and feature depth. In the Middle East, Saudi Arabia’s Vision 2030 allocates more than USD 500 billion to digital infrastructure, while the United Arab Emirates aims for 10% of GDP from artificial intelligence by 2031. South America shows steady but restrained progress as Brazil enforces LGPD compliance amid macroeconomic pressures.

Competitive Landscape

The big data technology market supports a moderately concentrated vendor field. Cloud hyperscalers vertically integrate analytics features, squeezing margins for pure-play software providers. Databricks and Snowflake compete on lakehouse architecture: Databricks highlights Apache Spark lineage, whereas Snowflake stresses zero-copy data sharing. MongoDB and Couchbase battle for operational-database share, with MongoDB adding vector search for generative-AI workloads. Confluent commercializes Apache Kafka for real-time streaming, and Elastic focuses on log analytics and observability.

Strategic moves center on vertical solutions, geographic reach, and ecosystem alliances. Palantir secures defense contracts that create high switching costs. Teradata shifts legacy customers to cloud subscriptions through joint offerings with Microsoft and Google. Startups such as Starburst and Dremio exploit data-mesh demand by enabling queries without centralized storage, while vendors in data observability and privacy-enhancing technologies address quality and compliance gaps. Compliance frameworks, ISO 27001, SOC 2, HIPAA, remain a baseline requirement that shapes procurement choices.

Big Data Technology Industry Leaders

Cloudera Inc.

Snowflake Inc.

Databricks Inc.

MongoDB Inc.

Splunk Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Confluent released a managed Apache Pulsar service with cross-stream replication, positioning the firm as a one-stop event streaming provider alongside its existing Kafka offerings and simplifying multi-cloud data-in-motion architectures.

- June 2025: Google Cloud introduced BigQuery Omni Edge, extending federated SQL queries to on-premise Kubernetes clusters and rival clouds, cutting data egress charges by executing transformations where data resides.

- April 2025: Snowflake launched a native vector database engine inside Snowpark, allowing billion-scale embeddings and retrieval-augmented generation without external services, and announced immediate general availability across all commercial regions.

- February 2025: Databricks acquired StreamForge, a real-time Apache Flink specialist, for USD 1.2 billion to deepen low-latency processing within its lakehouse platform and accelerate event-driven AI features.

Global Big Data Technology Market Report Scope

The Big Data Technology Market Report is Segmented by Component (Software, Hardware, Services), Deployment Model (On-Premise, Cloud, Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Banking, Financial Services and Insurance (BFSI), Healthcare and Life Sciences, Retail and Consumer Goods, Manufacturing, Government and Public Sector, Telecommunications and IT, Media and Entertainment, Energy and Utilities, Other Industry Vertical), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Software | Data Management Software |

| Analytics Software | |

| Hardware | Servers |

| Storage | |

| Services | Professional Services |

| Managed Services |

| On-Premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and Consumer Goods |

| Manufacturing |

| Government and Public Sector |

| Telecommunications and IT |

| Media and Entertainment |

| Energy and Utilities |

| Other Industry Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | Data Management Software | |

| Analytics Software | |||

| Hardware | Servers | ||

| Storage | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Retail and Consumer Goods | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Telecommunications and IT | |||

| Media and Entertainment | |||

| Energy and Utilities | |||

| Other Industry Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the big data technology market in 2025?

The big data technology market size is USD 312.07 billion in 2025.

What is the expected growth rate through 2030?

The market is projected to record a 13.34% CAGR between 2025 and 2030.

Which component segment is growing fastest?

Software is forecast to expand at a 13.89% CAGR as organizations favor platform-agnostic analytics tools.

Why are hybrid deployments gaining traction?

Hybrid architecture lets firms meet data-sovereignty rules while accessing elastic cloud services, driving a 13.94% CAGR.

Which region will expand most rapidly?

Asia-Pacific is expected to grow at a 14.41% CAGR through 2030, led by China, India, and Japan.

What is the market concentration level?

The top five vendors hold around 35% of software revenue, indicating moderate concentration.

Page last updated on: