Data Processing And Hosting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

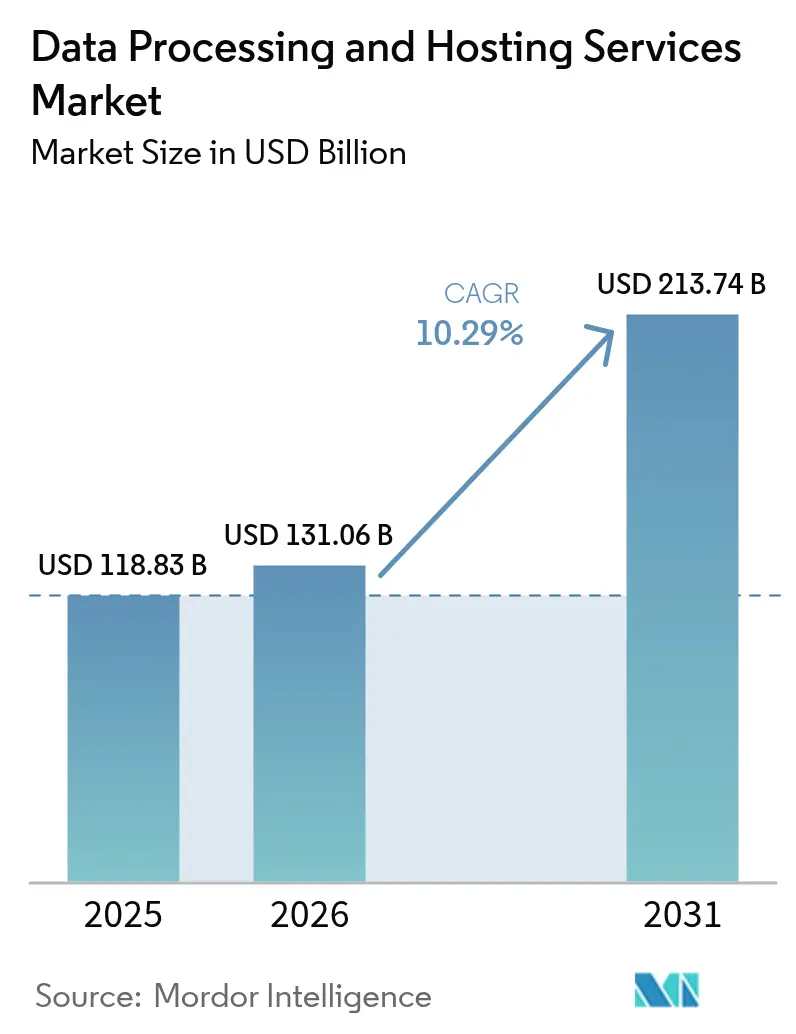

| Market Size (2026) | USD 131.06 Billion |

| Market Size (2031) | USD 213.74 Billion |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

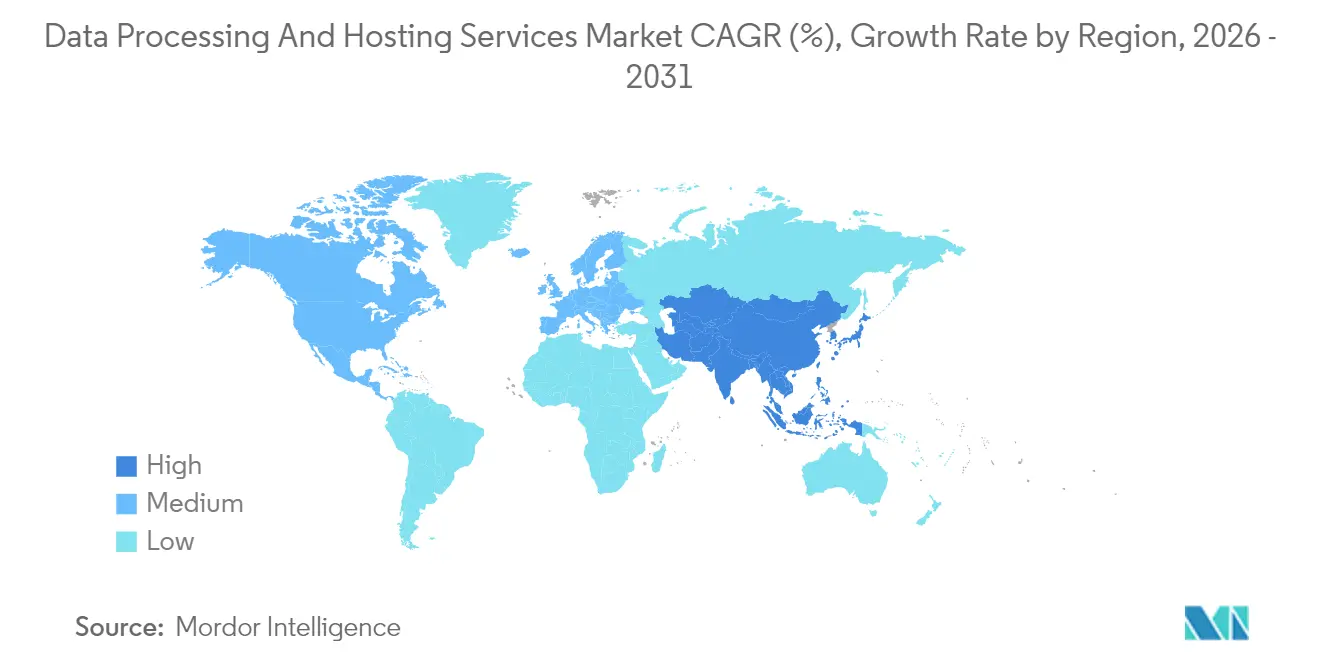

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Processing And Hosting Services Market Analysis by Mordor Intelligence

The Data Processing And Hosting Services market size is expected to grow from USD 118.83 billion in 2025 to USD 131.06 billion in 2026 and is forecast to reach USD 213.74 billion by 2031 at 10.29% CAGR over 2026-2031.

Expansion is propelled by large-scale enterprise migrations to managed compute, an accelerating shift toward AI-ready infrastructure, and unrelenting hyperscale capital expenditure. Enterprises are diverting budgets from refreshed on-prem racks to GPU-dense cloud instances, turnkey colocation suites, and regional edge nodes that compress data-to-insight cycles. Parallel policy shifts in Europe and the Middle East mandate sovereign-cloud deployments, prompting global corporations to localize workloads and create fresh pools of in-country capacity. Meanwhile, the removal of egress fees by the three largest public clouds has lowered switching costs, opening opportunities for specialist challengers that differentiate on stacked silicon, proximity, or sector-specific compliance.

Key technology and regulatory catalysts have reshaped the competitive balance. North America currently commands a 39% revenue share, underpinned by deep fiber networks, reliable power, and dense hyperscale clusters. Asia, in contrast, is expanding the fastest at a 13.4% CAGR as 5G penetration, AI start-up activity, and government tax incentives converge to boost new datacenter builds. Hosting services continue to dominate the data processing and hosting services market with a 64% share, yet cloud-native offerings within that category, especially IaaS, PaaS, and SaaS, post the strongest 14.1% CAGR as customers prioritize elasticity. Hybrid and multi-cloud strategies are surging at 12.5% CAGR, signaling that enterprises now view cloud as a portfolio rather than a monolith.

Key Report Takeaways

- By offering, hosting services led with 63.40% revenue share in 2025, cloud hosting (IaaS/PaaS/SaaS) is advancing at a 13.85% CAGR through 2031

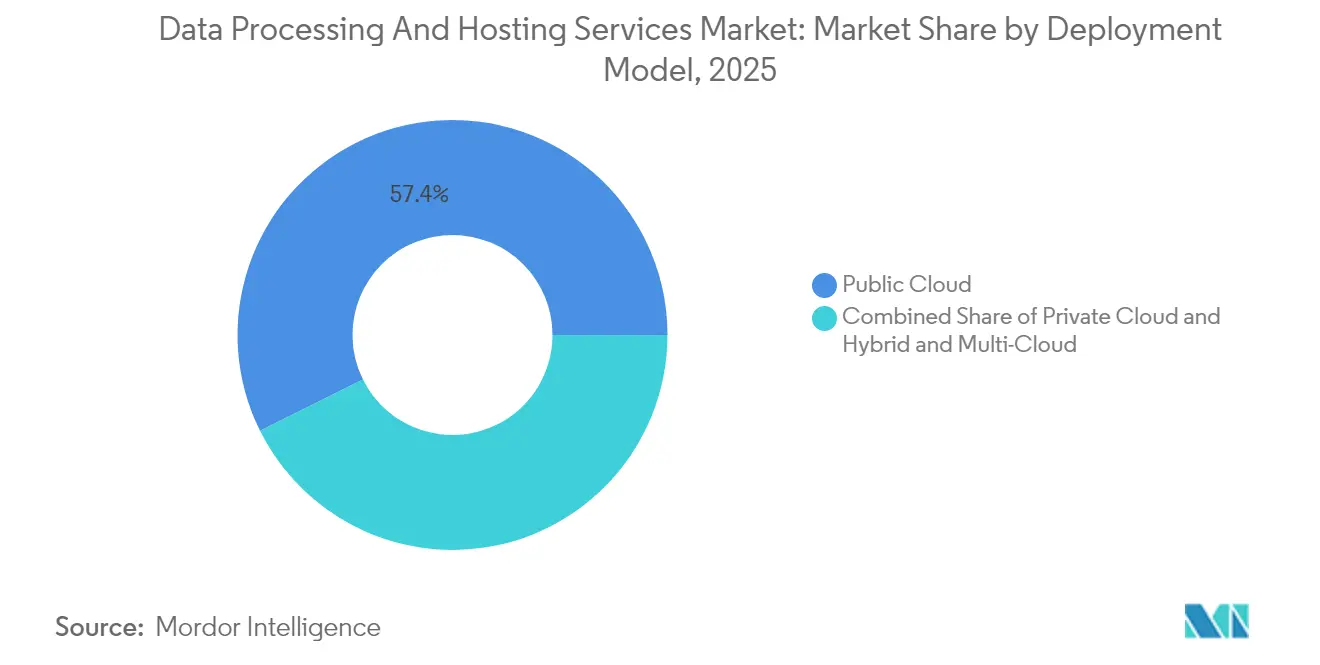

- By deployment model, the hybrid & multi-cloud segment posted a 12.22% CAGR, outpacing the overall data processing and hosting services market size in 2025

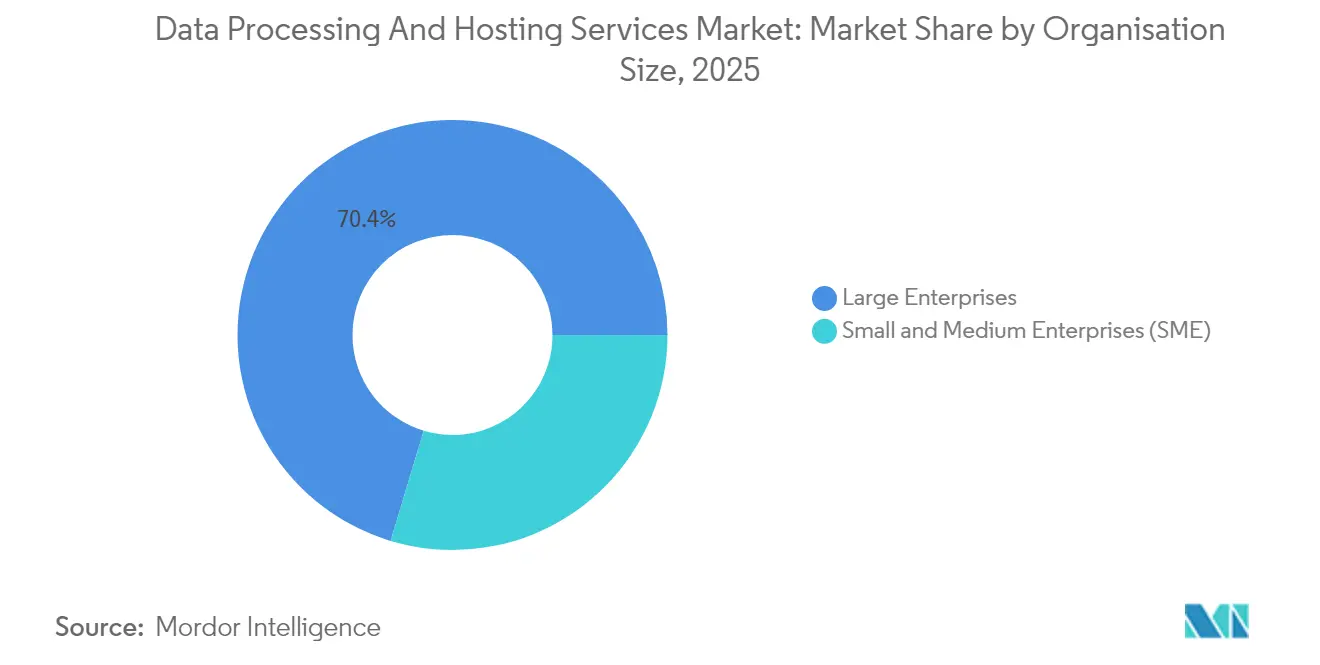

- By organisation size, large enterprises captured 70.35% of the data processing and hosting services market share in 2025, while SMEs recorded the strongest 11.55% CAGR to 2031

- By end-user industry, retail & e-commerce accelerates at a 12.64% CAGR, eclipsing IT & telecom incumbency.

- By region, North America held 38.62% of 2025 revenue; Asia is projected to grow at 13.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Processing And Hosting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing migration of enterprise workloads to hyperscale cloud data centers | +3.20% | North America & Europe | Medium term (2-4 years) |

| Proliferation of edge-native applications requiring distributed micro-hosting | +2.10% | Asia & Oceania | Medium term (2-4 years) |

| Emergence of sovereign-cloud mandates boosts in-country hosting | +1.80% | EU & Middle East | Short term (≤2 years) |

| Zero-Trust and Data-Residency Compliance Driving Managed Processing Contracts (BFSI and Healthcare) | +1.5% | Global (early BFSI & healthcare adoption) | Short term (≤2 years) |

| AI/ML workload explosion elevating demand for high-density GPU hosting | +2.70% | Global, focus on North America & Asia | Medium term (2-4 years) |

| SME Digital-First Strategies Fueling Bundled Processing?Hosting Packages (South America and Africa) | +1.4% | South America & Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Migration of Enterprise Workloads to Hyperscale Cloud Data-Centers

Enterprises continue to de-risk capital budgets by shifting mission-critical systems to hyperscale regions, with U.S. datacenter power demand expected to double to 35 GW by 2030. The move is increasingly capability-driven, anchored in access to AI accelerators and managed security services that remain prohibitively expensive on-prem. Pre-lease agreements now secure capacity years ahead of physical handover, particularly in Ashburn, Phoenix, Dublin, and Frankfurt, where power allotments are constrained.

AI/ML Workload Explosion Elevating Demand for High-Density GPU Hosting

By 2025, over 40,000 companies will run production AI on discrete GPUs, raising computational density and cooling requirements. Dedicated GPU clouds such as Lambda and CoreWeave post triple-digit growth as they guarantee H100 and MI300 inventory for training, fine-tuning, and inference workloads.

Proliferation of Edge-Native Applications Requiring Distributed Micro-Hosting

Edge use cases such as autonomous factory control and in-store analytics demand sub-20 ms latency, propelling micro-datacenter installations at telecom towers, metro rooftops, and retail parks. Global edge spending is projected to reach USD 380 billion by 2028, growing at a 13.8% CAGR. Vendors like Vapor IO layer K-8s orchestration atop container-ready pods, delivering low-touch deployments that minimize backhaul.

Emergence of Sovereign-Cloud Mandates Boosting In-Country Hosting

Regulators in the EU, GCC, and India now enforce data-location mandates that require workloads and encryption keys to stay within national borders. The EU Data Act, effective September 2025, compels clouds to offer seamless switching and cost-based egress, pushing hyperscalers toward joint ventures that confer local operational control. Enterprises accept a 15-25% cost premium for regulatory certainty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-grid instability & rising energy tariffs are limiting data-center expansion | −1.2% | Africa & South Asia | Medium term (2-4 years) |

| Escalating Cloud Egress Fees Creating Vendor-Lock Concerns (Global) | −0.8% | Global | Short term (≤2 years) |

| Data-sovereignty conflicts hindering cross-border hosting | −1.1% | Europe vs US | Medium term (2-4 years) |

| Shortage of Certified Cloud Talent Delaying Migration Projects (Nordics and GCC) | −0.6% | Nordics & GCC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Power-Grid Instability and Rising Energy Tariffs Limiting Data-Center Expansion

Electricity supply shortfalls and surcharges in South Asia and Africa throttle new builds. Data centers consumed 176 TWh of U.S. power in 2023, or 4.4% of national demand, underscoring the tension between compute growth and grid capacity. Operators pivot to onsite solar-plus-battery and micro-grid solutions, inflating capital requirements and elongating deployment schedules.

Data-Sovereignty Conflicts Hindering Cross-Border Hosting

Legal conflicts between the U.S. CLOUD Act and GDPR heighten compliance complexity for multinational corporations. The Sedona Conference highlights the friction in reconciling U.S. discovery obligations with non-U.S. privacy laws, delaying cross-border migrations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organisation Size: SMEs Driving Growth Through Digital Transformation

Large enterprises controlled 70.35% of 2025 revenue, leveraging deep coffers to modernize mainframes, adopt container orchestration, and spin up global DR replicas. In contrast, SMEs are the fastest movers, accelerating at 11.55% CAGR as simplified migration tooling, marketplace credits, and managed DevOps services flatten technical barriers. In African and Latin American markets, more than 90% of SMEs have adopted digital payments, underscoring widespread digital adoption. Governments subsidize training and cloud vouchers, further broadening reach. The absolute data processing and hosting services market size for SMEs is projected to double by 2030, while their slice of overall spending remains under 30% because large-enterprise estates also keep expanding.

SME cloud maturation creates new partner ecosystems. Resellers bundle point-of-sale, analytics, and local-language support, embedding compute costs into service fees. Advanced observability stacks surface anomalies and auto-apply remediation scripts, mitigating the skill gap that once stymied smaller firms. Those efficiencies, in turn, reinforce subscription renewals and incremental upsell, positioning the SME segment as a durable growth flywheel within the broader data processing and hosting services market.

By Offering: Cloud Hosting Revolutionizing Service Delivery Models

Hosting services delivered 63.40% of sector revenue in 2025, anchored by reliable compute, storage, and network primitives. The sub-segment of cloud hosting (IaaS, PaaS, SaaS) commands a 13.85% CAGR to 2031, fueled by elastic scaling, bundled APIs, and declining unit pricing as hyperscalers aggregate demand. Customers increasingly favor workload-optimized tiers, GPU clusters for AI, ARM cores for web tier, and z-parity CICS as a service for financial ledgers. Concurrently, professional services revenue grows as firms seek cloud-native redesign, data pipeline refactor, and FinOps governance. Edge and colocation providers embed cloud-like provisioning into portals, blurring the lines between core and distributed hosting. Over time, integrated pipelines that marry data preparation with compute will erode standalone ETL vendors, folding their economics into the data processing and hosting services market gatekeepers.

Financial flexibility remains a draw. Pay-by-the-second billing and sustained-usage credits lower the total cost of ownership. As energy costs fluctuate, workloads re-balance across regions based on real-time power spot prices, a capability accessible only through cloud automation. The result is a structurally higher utilization rate, translating to margin expansion for providers and cost predictability for tenants.

By Deployment Model: Hybrid and Multi-Cloud Strategies Gaining Momentum

Public cloud owned 57.35% of 2025 spending, yet hybrid & multi-cloud architectures post the steepest 12.22% CAGR through 2031 as firms seek workload portability and jurisdictional compliance. Vendor-neutral control planes orchestrate containers across on-prem, colocation, and hyperscale regions while policy engines enforce data-location and encryption standards. Cross-cloud service mesh enables developers to pair best-of-breed accelerators and managed databases without vendor lock. The data processing and hosting services market size for hybrid deployments is forecast to expand 2.3× within five years, mirrored by toolchain vendors adding automated cost arbitrage and compliance reporting.

End-user confidence rises as reliability metrics improve. Distributed object storage replicates data across cloud boundaries, minimizing RTO and RPO while satisfying local regulators. Cost optimization stems from running dev-test on lower-cost clouds and production on latency-adjacent regions. Enterprises report savings of 18% after adopting dynamic placement algorithms that rebalance compute based on spot pricing and sustainability scores.

By End-User Industry: Retail and E-Commerce Transformation Accelerates Adoption

IT & telecom led spending with a 23.65% share in 2025, but retail & e-commerce now records a 12.64% CAGR to 2031 as merchants digitize supply chains and deploy personalization engines. Global e-commerce sales are projected to capture 23% of retail by 2027, with revenue topping USD 6.4 trillion by 2029. Spiking holiday traffic pushes merchants into autoscaling front-ends and serverless APIs. Real-time fraud detection consumes GPU-accelerated analytics, nudging retailers toward specialized hosting tiers.

BFSI workloads remain lucrative owing to stringent encryption and audit needs. Banks deploy dual-provider active-active architectures that isolate keys from compute, satisfying both resiliency and jurisdictional mandates. Healthcare providers embrace HIPAA-aligned platforms for telemedicine and genomic sequencing. Manufacturing adopts digital twins that ingest continuous sensor streams into AI-based predictive maintenance dashboards. Collectively, industry-specific clouds underpin differentiated service bundles, spiraling sector stickiness, and push the data processing and hosting services market deeper into vertical integration.

Geography Analysis

North America claimed 38.62% of 2025 revenue on the back of vast fiber backbones, generous tax incentives, and dense hyperscale clusters. Loudoun County, Virginia, alone hosts over 30 million square feet of raised floor and is now facing grid-interconnection pauses due to transformer constraints. Providers respond with campus-scale micro-grids, 24×7 renewable PPAs, and reclaimed-heat reuse programs to counter sustainability scrutiny. AWS, Microsoft, and Google collectively earmarked more than USD 255 billion for new U.S. halls in 2025, ensuring the region’s capacity lead. Privacy legislation at the state level, such as California CCPA and Texas privacy bills, could demand that data copies remain in-state, subtly reshaping deployment footprints inside the data processing and hosting services market.

Asia records the fastest 13.18% CAGR as 5G proliferation, digital banking, and AI start-up ecosystems converge. Singapore’s moratorium on new datacenter permits diverts cap-ex toward Johor, Batam, Bangkok, and Hyderabad, all vying to become the region’s latency hubs. Japanese operators exploit underused geothermal in Hokkaido while Chinese hyperscalers replicate domestic super-app stacks to Southeast Asia, blending compute with payments and logistics. Smartphone saturation and real-time translation services multiply data flows, anchoring durable demand.

Europe’s sovereignty agenda steers procurement trends. The EU’s Digital Europe Programme has allocated EUR 900 million to cloud marketplaces and security centers, catalysing domestic capacity. Germany and France vie for AI training clusters by touting nuclear and hydro power mixes. Gaia-X lays interoperability standards, albeit slower than first envisioned. Nordic states leverage cheap hydroelectricity yet grapple with limited fiber routes; Eastern European states woo investors through special economic zones, though geopolitical risk remains a hurdle. Notably, post-Brexit UK relaxes VAT on datacenter gear, attracting trans-Atlantic investment and reinforcing London’s pole position.

Regulatory Landscape

Regulation is tightening around data location, portability, and security obligations for data processing and hosting providers, with the EU acting as a key pace setter for global compliance programs. The EU Data Act became applicable in September 2025, introducing interoperability, termination, and switching-related requirements for data processing services and reinforcing multi-cloud and exit-readiness as procurement criteria for enterprise and public-sector buyers.

In 2026, standards and policy initiatives further link hosting strategy to trust, AI governance, and sovereign capacity. NIST updated its Guidelines for API Protection for Cloud-Native Systems in March 2026, reinforcing zero-trust-aligned controls around API lifecycle risk in cloud environments. The European Commission also proposed the Cloud and AI Development Act in 2026, including a EuroCloud Federation concept for public sector cloud services, while the EU AI Act becomes fully applicable in August 2026 with mandatory data governance requirements for high-risk AI systems (Article 10), shaping how providers design managed AI-ready hosting and compliance attestations.

Value Chain Analysis

The value chain covers upstream component and infrastructure suppliers (servers, GPUs, networking, storage, power distribution equipment, and cooling systems), data center developers and operators (hyperscalers, colocation and bare-metal providers), platform layers (IaaS/PaaS/SaaS, orchestration, security, observability, and FinOps), and downstream enterprise and SME buyers that consume compute, storage, and managed data processing. Market structure is increasingly shaped by co-design of facilities and workloads, including GPU-dense hosting that depends on liquid cooling, higher rack power density, and tighter integration between hardware supply, deployment services, and managed operations.

A binding constraint in 2026 is electrical and grid-related equipment availability rather than facility construction alone, with reported multi-year lead times for high-voltage transformers and switchgear and extended utility interconnection queues in major markets. These bottlenecks steer siting toward secondary metros and brownfield retrofits, elevate the role of energy partners and equipment OEMs, and shift procurement toward pre-leasing capacity and long-lead ordering. On the downstream side, EU portability and switching obligations under the Data Act push providers and integrators to operationalize standardized migration runbooks, interoperability tooling, and contract structures that support hybrid and multi-cloud delivery.

Competitive Landscape

The data processing and hosting services market remains moderately concentrated. AWS, Microsoft Azure, and Google Cloud hold a combined 63% of global cloud services revenue as of Q1 2025, with AWS alone at 29%. AWS accelerates its Trainium2 roadmap, promising 50% lower price-performance for AI training. Microsoft layers vertical stacks like Cloud for Retail and Fabric analytics to entrench sector-specific workflows. Google posts the fastest growth, crediting partnerships with Anthropic and open-source communities that court developer mindshare. Collectively, these giants pledge more than USD 255 billion in U.S. datacenter cap-ex and USD 120 billion across EMEA and APAC in 2025, raising barriers to entry.

Specialist providers seize niches neglected by hyperscalers. CoreWeave and Lambda specialize in GPU clouds with deterministic performance and transparent scheduling, resonating with media, life-science, and research clients. Digital Realty, Equinix, and NTT advance colocation models that bundle dedicated white-space with managed liquid-cool loops. Regional telcos such as MTN and Telefónica overlay 5G network slices with low-latency compute nodes, blurring the edge/mobile divide inside the data processing and hosting services market. Sovereign-cloud joint ventures Capgemini/Orange and T-Systems/Google address public-sector trust gaps through ring-fenced operations.

Pricing models evolve. The wave of egress-fee eliminations after the EU Data Act scrutiny eases migration friction and amplifies multi-cloud adoption. Cost-management vendors like Spot and Zesty ingest real-time bills across providers, promoting automated rightsizing. Hyperscalers shift differentiation toward AI APIs, proprietary vector databases, and turnkey compliance blueprints. As the leading five providers collectively command about an 80% share, the market concentration score stands at 8, indicating an oligopolistic yet vigorously contested arena.

Data Processing And Hosting Services Industry Leaders

GoDaddy Operating Company LLC.

Hostinger International Ltd.

Teradata Corporation

IBM Corporation

Bluehost (Endurance International Group)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

AI-ready capacity buildout broadens the opportunity set beyond traditional colocation and general-purpose cloud, with providers differentiating through power access, high-density cooling, and managed stacks that reduce time-to-deploy for GPU-intensive workloads. A concrete signal is hyperscaler-level investment tied to gigawatt-scale infrastructure: in July 2026, Meta disclosed a USD 50 billion total investment to expand its Richland Parish, Louisiana campus to 5 GW of IT capacity, alongside new transmission, battery storage, and dedicated generation plans. This shifts the market toward energy-integrated campus models and creates whitespace for partners in power delivery, liquid cooling, and regional hosting footprints that can meet latency, sovereignty, and capacity requirements.

Sovereign and in-country expansion programs also drive demand for localized processing and hosting, particularly where regulators and procurement bodies require domestic operations and key control. In July 2026, AWS broke ground on an expansion of its Hyderabad Region data center operations in India as part of a planned USD 21 billion investment in Indian cloud and AI infrastructure from 2026 to 2030, highlighting how large buyers are backing regional capacity to meet data residency and performance requirements. Alongside these hyperscale moves, switching and interoperability rules in Europe (via the EU Data Act) create commercial room for specialist providers and integrators that package migration, compliance evidence, and multi-cloud operations, especially for regulated verticals using managed processing contracts.

Recent Industry Developments

- May 2026: Teradata launched the Teradata Autonomous Knowledge Platform to unify AI, analytics, and data across cloud and hybrid environments. The release targets enterprise teams that need governed data access for AI workflows without extensive data movement, reinforcing hybrid and multi-cloud operating models. It also raises competitive pressure on hosting and platform providers to package integrated data and AI services rather than standalone infrastructure.

- February 2026: GoDaddy announced an integration between its Agent Name Service (ANS) and Salesforce MuleSoft Agent Fabric. The integration connects identity and discovery for AI agents with a mainstream integration platform, moving hosting providers closer to application-level automation and agent orchestration needs. It also supports a broader shift in SMB hosting toward managed, AI-assisted operations that reduce complexity for non-specialist users.

- May 2025: Microsoft confirmed USD 80 billion in AI-centric datacenter investments, including expansions in Texas and Wisconsin. The commitment highlights hyperscalers prioritizing AI-ready capacity and infrastructure upgrades that shift demand toward managed compute and specialized hosting tiers. It also increases the bar for regional providers and colocation operators to secure power, land, and supply chain allocations for competitive buildouts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers third party services that store, run, and manage customer data and workloads, along with paid services that process, clean, format, and prepare data so it can be used for reporting or operations.

Scope exclusions: hardware sales, on premises IT labor, and pure connectivity services are excluded when they are billed as separate line items.

Segmentation Overview

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SME)

- By Offering

- Data Processing Services

- Data Entry Services

- Data Mining Services

- Data Cleansing and Formatting

- Data Scanning and Indexing

- Managed ETL and Analytics

- Hosting Services

- Shared (Reseller) Hosting

- Virtual Private Server (VPS) Hosting

- Dedicated Server Hosting

- Cloud Hosting

- IaaS

- PaaS

- SaaS

- Managed WordPress Hosting

- Application Hosting

- Colocation and Bare-Metal

- Data Processing Services

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid and Multi-Cloud

- By End-user Industry

- IT and Telecommunication

- BFSI

- Retail and E-commerce

- Manufacturing

- Healthcare and Life Sciences

- Media and Entertainment

- Government and Public Sector

- Others (Education, Hospitality, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market frame, build regional demand anchors, and check adoption trends for hosted and processed data services. Public materials were reviewed, including US Census Bureau service industry data, OECD and World Bank digital economy indicators, and ITU connectivity statistics. For operational context, we also used selected NIST publications and academic journals that cover data center efficiency and cloud usage patterns.

To make the inputs more practical, company filings, annual reports, and investor presentations were reviewed for revenue splits, geographic mix, and pricing commentary related to hosting and adjacent managed services. A paid subscription covering company financials and intelligence was used selectively to normalize historical financials, map subsidiaries, and reduce double counting across consolidated entities. This desk research list is illustrative only, and other public sources were also used for cross checks, clarification, and validation.

Primary Interviews and Surveys

Primary work was used to confirm what buyers actually purchase under data processing and hosting contracts, how pricing is structured across workload types, and how demand changes by organization size and end use. We spoke with supply side and demand side practitioners across major regions so secondary assumptions could be corrected, and then we closed key gaps through follow up checks when inconsistencies showed up.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 40% |

| Mid tier: 55% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 17% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where national and regional service spend signals were reconstructed into an addressable pool for outsourced data processing and hosting, then filtered by adoption indicators for cloud hosting, application hosting, and related managed workloads. The totals were corroborated through selective bottom-up approximations, such as sampled provider revenue mapping, channel checks, and volume by typical contract value ranges, which helped adjust for under-reporting in smaller accounts.

Inputs used in the model included data center capacity additions and utilization signals, cloud and hosting adoption by enterprise size, pricing direction for compute and storage bundles, workload mix shifts (web, application, virtual desktop, and backup), and the pace of data creation that drives processing demand. When revenue splits were not disclosed, gaps were handled by using proxy splits from similar public peers, then re-tested through interviews until a stable range was reached.

Forecasts were produced using scenario analysis supported by short trend models, with growth paths linked to variables such as enterprise cloud migration speed, digital service intensity by industry, and regional IT spend resilience. The final forecast was kept traceable so each year change can be explained through a small set of drivers rather than a single blended growth rate.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent demand indicators, supplier commentary, and macro signals that move hosting and processing spend. Variance checks were run at the region and offering level, and outliers were reviewed in a second analyst pass before sign-off.

The model is refreshed annually so the latest financial releases, public statistics, and capacity announcements are reflected in the base year. Interim updates are triggered when material events occur, such as major pricing resets, sudden capacity constraints, or regulation changes that shift hosting locations. Before delivery, a final review is completed so clients receive the most current and internally consistent view.

Mordor Intelligence's Data Processing and Hosting Services Market Size Measured Against Other Published Estimates

Published market sizes for data processing and hosting services can look far apart because the service bundle is not described the same way by every publisher, and because the base year and currency timing also vary. In practice, the biggest swings usually come from what is counted as hosting versus adjacent IT services, and whether figures are built from provider revenue, demand side spend, or a mix of both.

Colocation facility rent and pure data center real estate fees are common add-ons in some estimates, and those sit outside Mordor Intelligence's scope. This keeps the value tied to data processing activities and hosted service revenues that are actually delivered as IT services. Differences also show up when one model assumes faster price erosion for compute and storage than another, or when a forecast uses an aggressive cloud migration path without re-checking it against buyer side contract behavior and regional capacity signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 131.06 B (2026) | |

| Industry Publisher A | USD 124.40 B (2024) | Uses an earlier base year and a different forecast window, and the scope description suggests a broader blend of hosting related activities that may mix application hosting with adjacent infrastructure services, which changes the starting value. |

| Industry Publisher B | USD 110.00 B (2023) | Anchors the market on a 2023 revenue base and emphasizes cloud based processing, which can understate non cloud hosting and certain managed hosting revenues depending on how hybrid workloads are treated. |

The table shows that year selection and what gets bundled into hosting are the two main reasons the numbers spread. By tying the model to clear service revenue definitions, and then re-checking assumptions like pricing direction and workload mix with field inputs, we keep the size line explainable and easier to replicate over time.

Key Questions Answered in the Report

What is the current size of the data processing and hosting services market?

The market stands at USD 131.06 billion in 2026.

How fast will the data processing and hosting services market grow by 2031?

It is projected to expand at a 10.29% CAGR, reaching USD 213.74 billion by 2031.

Which region holds the largest revenue share today?

North America leads with 38.62% market share in 2025.

Why are hybrid and multi-cloud deployments gaining traction?

They deliver workload portability, jurisdictional compliance, and cost optimization, posting a 12.22% CAGR through 2031.

How are hyperscalers addressing vendor-lock concerns?

Major providers have begun eliminating or reducing egress fees, making it easier for customers to adopt multi-cloud strategies .

Which end-user industry is growing the fastest?

Retail & e-commerce workloads register a 12.64% CAGR as merchants digitize customer experiences.

Page last updated on: