Point-of-Care Glucose Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

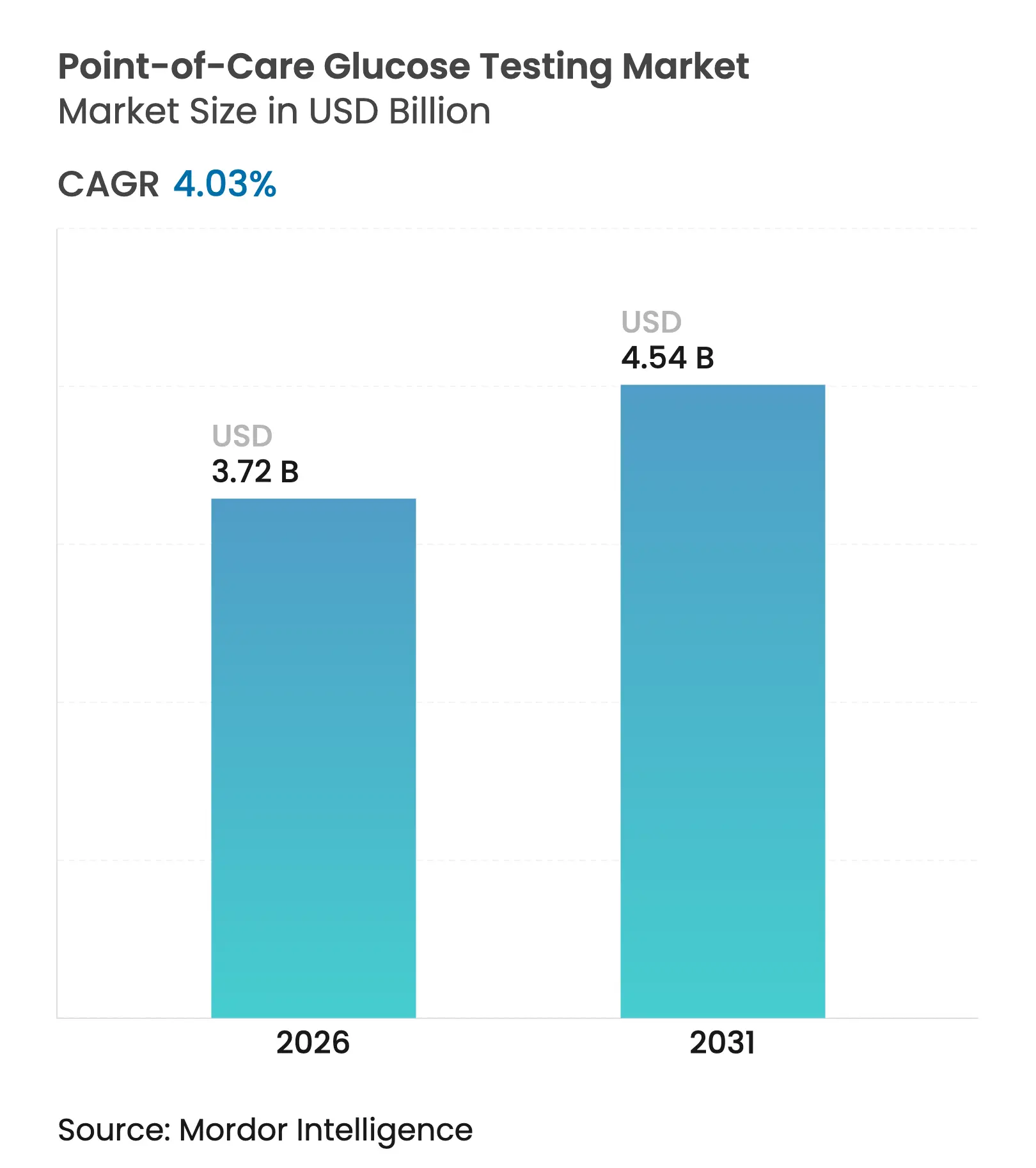

| Market Size (2026) | USD 3.72 Billion |

| Market Size (2031) | USD 4.54 Billion |

| Growth Rate (2026 - 2031) | 4.03 % CAGR |

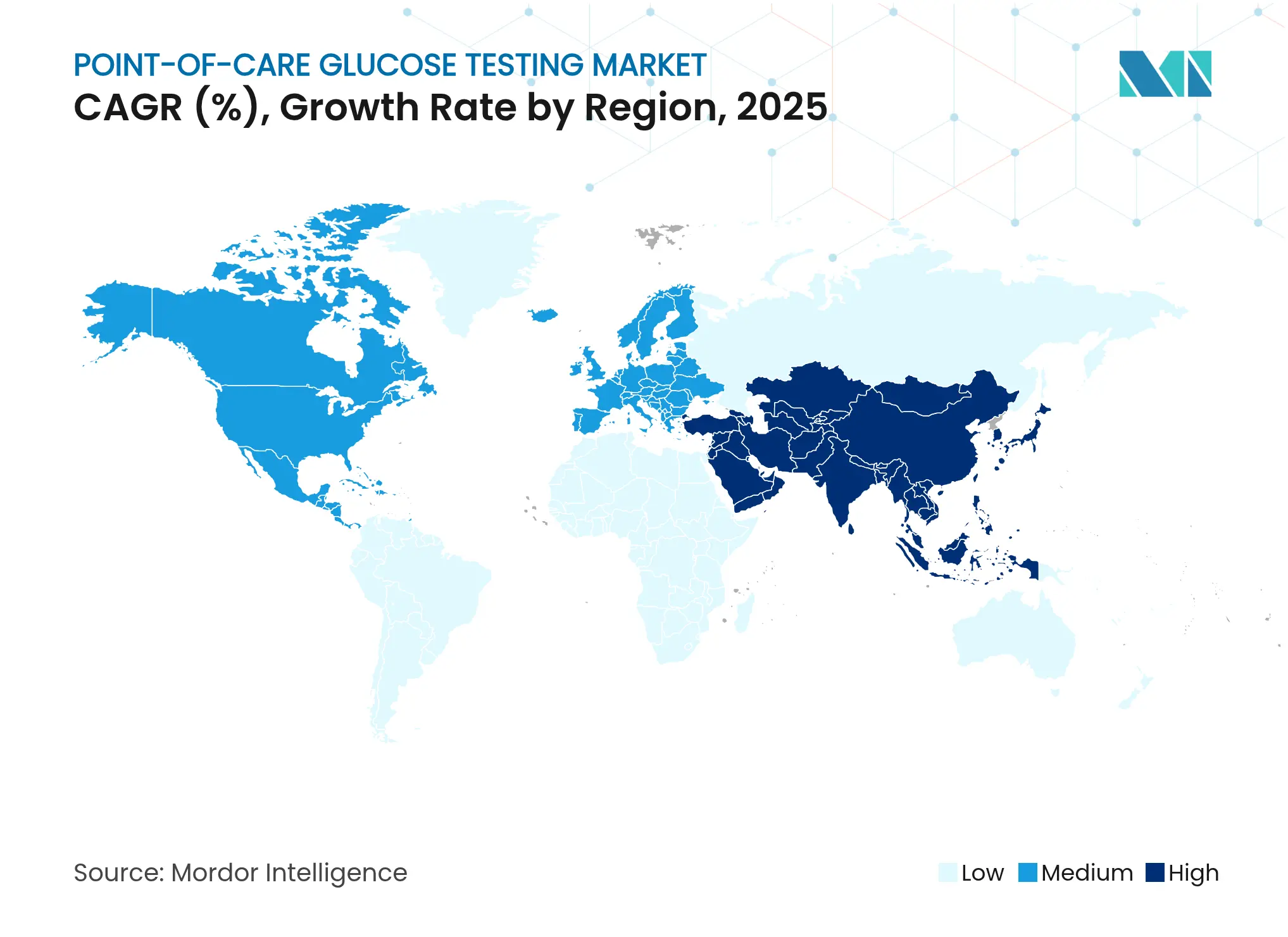

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

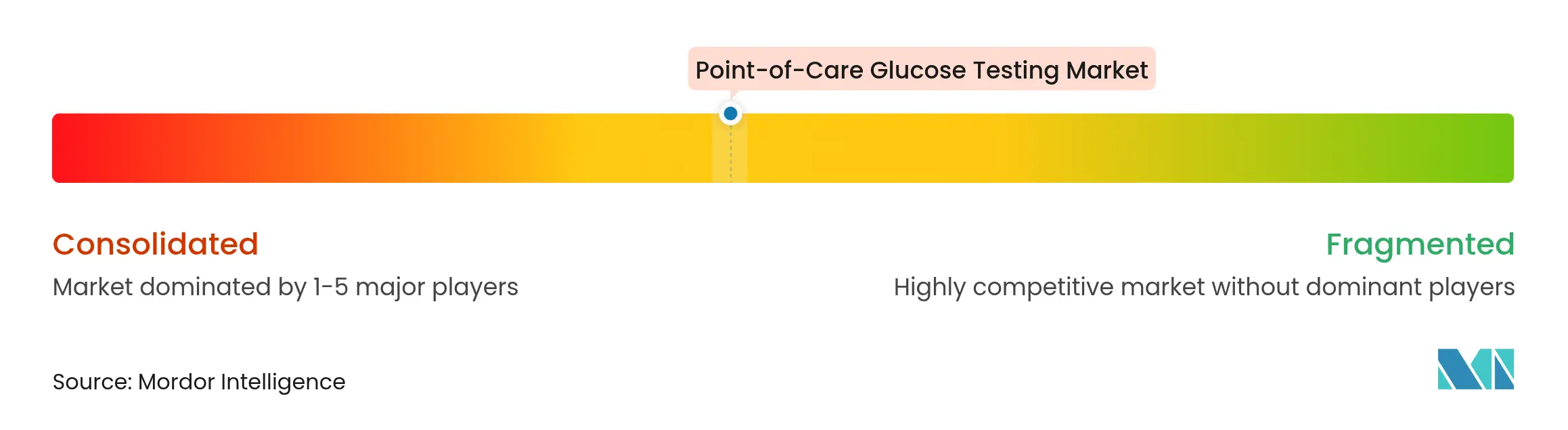

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Point-of-Care Glucose Testing Market Analysis by Mordor Intelligence

point of care glucose testing market size in 2026 is estimated at USD 3.72 billion, growing from 2025 value of USD 3.58 billion with 2031 projections showing USD 4.54 billion, growing at 4.03% CAGR over 2026-2031. Demand is propelled by a steep rise in diabetes prevalence, with the global patient pool expected to climb from 537 million adults in 2021 to 783 million by 2045. Broader access to electronic-medical-record (EMR)-ready meters, rapid penetration of over-the-counter (OTC) continuous glucose monitors, and aggressive government screening initiatives collectively sustain momentum. Established players defend share by embedding network connectivity, while specialists disrupt with digital-health integration. Asia Pacific exhibits the fastest regional growth at a 6.56% CAGR, aided by expanding healthcare infrastructure and earlier diagnosis in China and India.

Key Report Takeaways

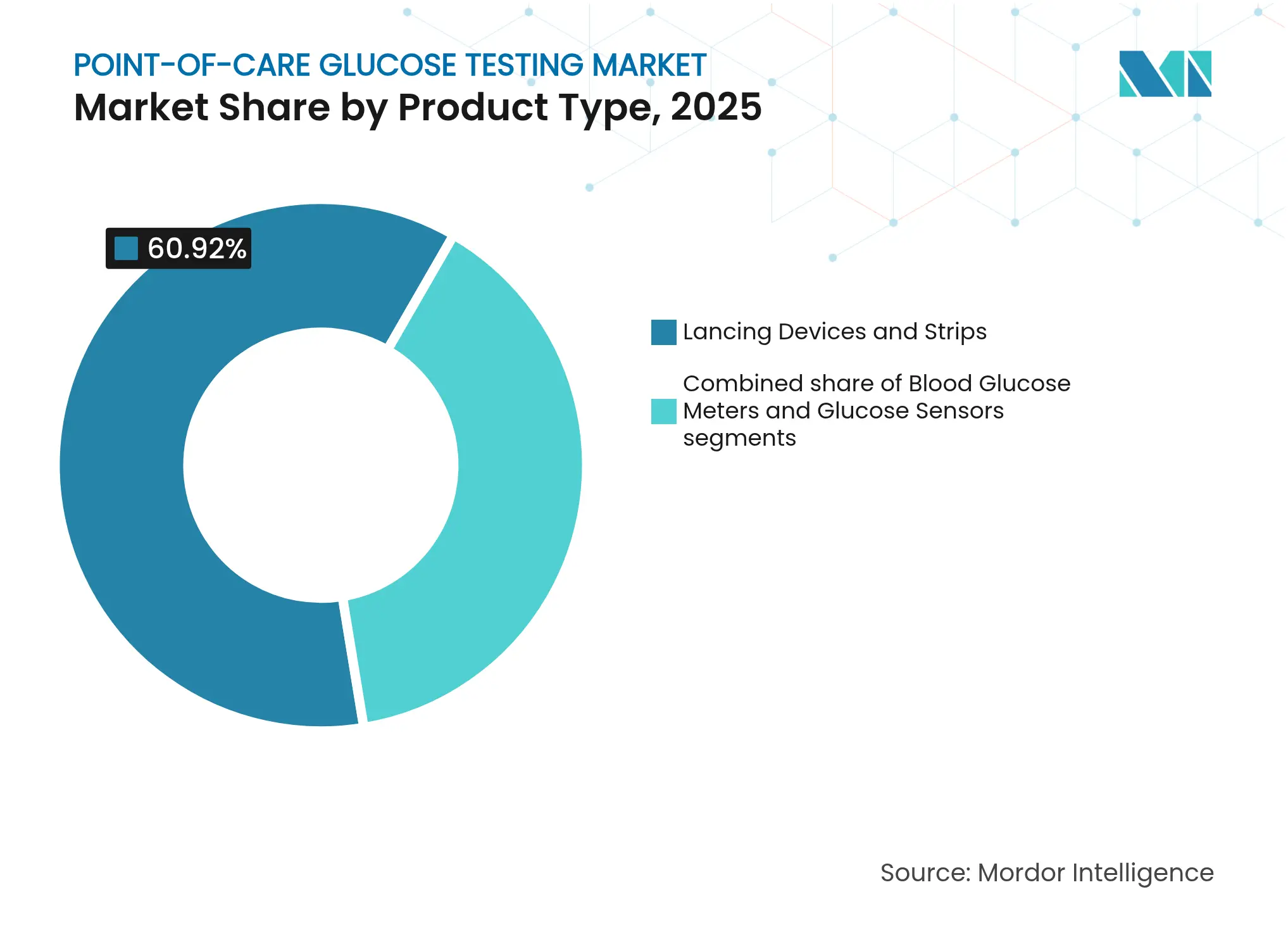

- By product type, lancing devices and strips led with 60.92% of point of care glucose testing market share in 2025, whereas continuous and flash sensors are poised to grow at a 4.76% CAGR to 2031.

- By application, type-2 diabetes dominated at 84.12% in 2025; type-1 diabetes is expected to register the fastest 5.78% CAGR through 2031.

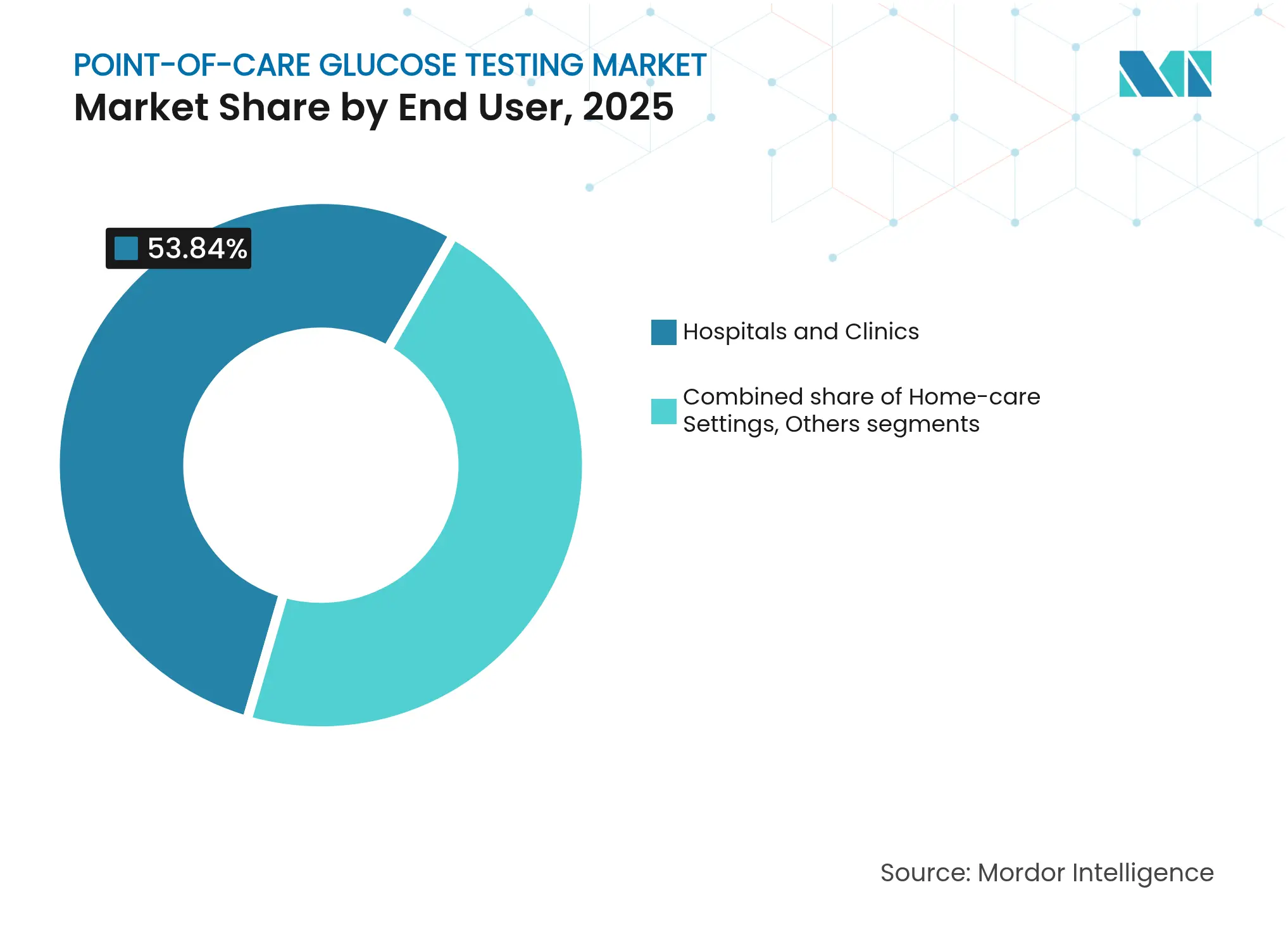

- By end user, hospitals and clinics controlled 53.84% of the point of care glucose testing market size in 2025, while home-care settings are expanding at 5.42% CAGR.

- By mode of prescription, prescription devices accounted for 68.87% in 2025; the OTC channel is forecast to post a 6.18% CAGR, spurred by the FDA’s 2024 clearance of the first OTC CGM.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Point-of-Care Glucose Testing Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rise of EMR-ready networked glucose meters in U.S. hospitals Rise of EMR-ready networked glucose meters in U.S. hospitals | ~+1.2% | North America, with spillover to Europe | Medium term (~ 3-4 yrs) | (~) % Impact on CAGR Forecast:~+1.2% | Geographic Relevance:North America, with spillover to Europe | Impact Timeline:Medium term (~ 3-4 yrs) |

CLIA-waived strip-free meters lowering peri-operative hypoglycemia in ASCs CLIA-waived strip-free meters lowering peri-operative hypoglycemia in ASCs | ~+0.8% | North America, Europe | Short term (≤ 2 yrs) | |||

Government screening drives low-cost meter demand Government screening drives low-cost meter demand | ~+1.0% | Asia Pacific, Middle East and Africa | Medium term (~ 3-4 yrs) | |||

Digital therapeutics bundling with Bluetooth meters boosts replacements Digital therapeutics bundling with Bluetooth meters boosts replacements | ~+0.9% | Global, with early adoption in North America and Europe | Medium term (~ 3-4 yrs) | |||

Infection-control protocols spur single-use safety lancet uptake Infection-control protocols spur single-use safety lancet uptake | ~+0.5% | Global | Short term (≤ 2 yrs) | |||

| Source: Mordor Intelligence | ||||||

Rise of EMR-ready networked glucose meters in U.S. hospitals

Growing connectivity standards are pushing hospitals to deploy glucose meters that auto-upload readings into EMRs, shaving documentation errors by 61% and improving insulin dosing accuracy by 37%. Roche’s cobas pulse platform showcases the shift by integrating Android-based apps and secure Wi-Fi, which accelerates clinical decisions and reduces nursing time on paperwork by 28%. Real-time transmission further cut severe hypoglycemic events by 42%, persuading large hospital systems to replace legacy meters in bulk contracts.

CLIA-waived strip-free meters lowering peri-operative hypoglycemia in ASCs

Ambulatory surgical centers adopt strip-free biosensor platforms that deliver glucose values within seconds and withstand anesthetic interference, enabling peri-operative teams to avert hypoglycemia. New CLIA waivers covering advanced optical sensors accelerate uptake because facilities can now deploy devices without complex validation protocols, saving staff training time and reducing operating-room workflow interruptions.

Government screening drives low-cost meter demand

Universal-coverage laws, such as Canada’s Bill C-64, earmark funds for test strips and meters, broadening access in underserved communities. The WHO’s 2024 inclusion of HbA1c point-of-care tests in its in-vitro diagnostics pre-qualification list has already guided bulk tenders across low-income countries, expanding volumes for cost-efficient manufacturers.

Infection-control protocols spur single-use safety lancet uptake

CDC guidelines now prohibit sharing finger-stick devices, steering hospitals toward auto-disabled, single-use lancets that mitigate blood-borne pathogen risk[1]Source: Centers for Disease Control and Prevention, “Blood glucose monitoring infection-control guidelines,” cdc.gov . Adoption surged during the COVID-19 pandemic and remains elevated as facilities bake infection-control metrics into purchasing scorecards, driving premium-priced lancet volumes upward.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accuracy-related recalls delaying hospital tenders Accuracy-related recalls delaying hospital tenders | ~-0.7% | Global, with higher impact in North America and Europe | Short term (≤ 2 yrs) | (~) % Impact on CAGR Forecast:~-0.7% | Geographic Relevance:Global, with higher impact in North America and Europe | Impact Timeline:Short term (≤ 2 yrs) |

Required Professional Assistance and Lack of Awareness About Glucose Monitoring in Emerging Countries Required Professional Assistance and Lack of Awareness About Glucose Monitoring in Emerging Countries | ~-0.9% | Asia Pacific, Middle East and Africa, South America | Medium term (~ 3-4 yrs) | |||

| Source: Mordor Intelligence | ||||||

Accuracy-related recalls delaying hospital tenders

Product recalls—for example, Abbott’s September 2024 FreeStyle Libre 3 sensor withdrawal after reports of high false readings—often freeze tender processes for 6–9 months and undermine clinician confidence. Peer-reviewed evaluation found 46% of FDA-cleared meters missed ISO 15197:2013 precision targets, prompting administrators to conduct additional validation before re-ordering.

Required professional assistance and lack of awareness

In many rural districts of Asia and Africa, fewer than 25% of diagnosed patients perform regular self-testing, largely because of limited diabetes-education programs and scarce primary-care resources. WHO’s South-East Asia regional review underscores the structural gap: 246 million adults live with diabetes in the bloc, yet essential diagnostics remain inaccessible in a significant share of primary facilities, curtailing adoption potential.

Segment Analysis

By Product Type: Continuous sensors disrupt traditional testing

Continuous and flash sensors are moving the point of care glucose testing market away from episodic strip-based checks. Lancing devices and strips still commanded 60.92% of point of care glucose testing market size in 2025, but sensor shipments are expanding at 4.76% CAGR as providers seek richer glycemic profiles. Dexcom’s G7 posts a mean absolute relative difference of 8.2%, the best among FDA-cleared CGMs, prompting formularies to include sensors for both inpatient and outpatient populations. Meanwhile, Roche enhances strip accuracy through novel enzymatic chemistry and couples it with native EMR connectivity, prolonging relevance for conventional meters.

Clinical performance drives purchase decisions. Hospitals value sensors’ predictive-alert capability, which flags impending hypo- or hyper-glycemia and triggers protocol-based interventions. Conversely, emerging markets continue to favor strips because of lower upfront cost and reliable reimbursement. Manufacturers counter by offering hybrid kits—strip meters with optional Bluetooth modules—to create upgrade paths while preserving affordability. The interplay sustains diverse product mixes across regions, preventing dominance by a single technology while widening patient choice.

Note: Segment shares of all individual segments available upon report purchase

By Application: Type-1 diabetes shows fastest growth

Type-2 cohorts dominate testing volume, representing 84.12% of all strip and sensor sales in 2025. However, point of care glucose testing market share for type-1 diabetes applications is growing more swiftly, propelled by automated insulin delivery systems that hinge on real-time sensor input. Medtronic’s MiniMed 780G coupled with the Simplera Sync disposable sensor earned CE-Mark in January 2025, allowing calibration-free use and driving pediatric adoption in Europe.

Gestational-diabetes monitoring, though smaller in absolute dollars, garners policy emphasis because rigorous glucose control mitigates neonatal complications. ADA’s 2025 Standards of Care instruct obstetric teams to adopt frequent point-of-care monitoring during pregnancy, fostering demand for intuitive meters that sync with prenatal electronic records. Vendors respond with color-coded trend indicators and scheduled reminder alarms, features that enhance adherence in a time-limited clinical scenario.

By End User: Home-care settings driving innovation

Hospitals and clinics controlled 53.84% of 2025 revenue, leveraging networked meters for in-house glucose rounding, intensive-care oversight, and pre-surgical screening. COVID-19 accelerated interest in minimally invasive sensors, enabling nurses to capture values without repeated room entry. Adoption persists as facilities benchmark reduced staff workload and sample-handling errors.

Home-care users are the fastest-growing cohort at 5.42% CAGR. The FDA’s June 2024 authorization of Abbott’s Libre Rio and general-consumer Lingo sensors for OTC sale broadened eligibility beyond insulin-dependent patients. Combined with smartphone dashboards and cloud-delivered coaching, home users can share longitudinal data with physicians, aligning with payer programs that reward remote monitoring. Vendors additionally market subscription models bundling sensors, lancets, and AI-guided feedback, turning device revenue into recurring service streams.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Prescription: OTC growth transforming access

Prescription devices still comprise 68.87% of global units due to clinician oversight requirements and legacy reimbursement structures. Hospitals and endocrinologists value the ability to tailor meter selection based on comorbidities and user dexterity.

The OTC channel, however, is tilting the landscape. Dexcom’s Stelo sensor, cleared in March 2024, targets non-insulin consumers who previously relied on boutique wellness trackers, offering medical-grade accuracy without a doctor’s visit. Analysts expect OTC to approach 39.50% share by 2031 as retailers stock sensors alongside blood-pressure and pulse-ox devices, positioning pharmacies as decentralized diagnostics hubs. Manufacturers are partnering with chain stores for installment-based payment plans to mitigate up-front cost, widening demographic reach.

Geography Analysis

North America accounted for 40.12% of worldwide point of care glucose testing market size in 2025, underpinned by high disease prevalence, advanced reimbursement, and rapid uptake of CGMs. CMS broadened sensor coverage to all insulin users in 2024, removing cost barriers for 1.5 million Medicare beneficiaries and reinforcing double-digit growth for connected solutions. Device makers also benefit from a vibrant digital-health ecosystem that integrates readings with tele-endocrinology platforms, elevating clinical value and patient loyalty.

Europe stands as the second-largest region. Structured procurement in national health systems promotes early technology adoption once cost-effectiveness is demonstrated. The CE-Mark approval of Medtronic’s MiniMed 780G with disposable sensor affirms regulators’ receptivity to hybrid closed-loop designs. Yet, the European Commission’s 2024 study revealing that 87% of public tenders contained import-restrictive clauses could temper non-EU supplier entry, nudging vendors toward local manufacturing.

Asia Pacific is the fastest-growing territory, forecast at a 6.23% CAGR from 2026-2031. Government screening programs, such as India’s National Diabetes Programme, introduce millions to first-time testing each year. Rising middle-class income supports sensor upgrades among urban populations, while smartphone penetration enables app-based coaching even in semi-urban settings. Challenges remain: fragmented reimbursement and uneven clinician distribution slow diffusion in rural areas, but low-cost Bluetooth meters offered below USD 20 per kit are narrowing the access gap.

Competitive Landscape

Market Concentration

Abbott, Roche, and LifeScan jointly controlled majority of global revenue in 2024, marking a moderately concentrated field. Abbott leverages scale in sensor manufacturing plus a software road-map that links Libre data into diet-tracking and exercise-monitoring portals; the firm targets USD 10 billion in Libre receipts by 2028 through multiparameter sensors measuring ketones alongside glucose. Roche integrates its cobas glucose platform with a medication-management app, giving hospitals a turnkey solution that satisfies infection-control and documentation mandates. LifeScan retains strong strip volumes via OneTouch brand loyalty and a subscription model bundling supplies with tele-coaching.

Challengers exploit niches: Dexcom collaborates with Verily on miniaturized sensors suitable for non-diabetics pursuing metabolic wellness, while Senseonics partners with Sequel to pair a 365-day implantable CGM with automated insulin delivery, differentiating on wear-time[2]Source: Senseonics Holdings, “Eversense 365 and Sequel partnership,” senseonics.com . Hardware makers also diversify via M&A; MTD Group’s 2024 purchase of Ypsomed’s pen-needles and meters doubled its disposable-device capacity to 2.5 billion units, elevating its rank to the second-largest pen-needle supplier. Inside China, Yuwell Medical and SiBionics scale domestic sensors to satisfy expanding provincial tenders, while contemplating Europe-bound CE filings.

Platform partnerships intensify. Device OEMs embed APIs that stream real-time glucose feeds into electronic health-record vendors, remote-patient-monitoring dashboards, and insurer wellness apps, creating stickiness that raises switching costs. Strategic investments in cybersecurity and dual-band radio chips secure hospital IT approvals, an increasingly pivotal purchasing criterion.

Point-of-Care Glucose Testing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Abbott secured FDA clearance for a dual-analyte sensor measuring glucose and ketones, broadening metabolic-monitoring capabilities

- April 2025: Senseonics joined forces with Sequel Med Tech to marry its year-long Eversense 365 CGM with Sequel’s twiist automated-insulin-delivery platform

- March 2025: Medtronic obtained CE-Mark for MiniMed 780G equipped with Simplera Sync disposable sensor, removing finger-stick calibration requirements.

Table of Contents for Point-of-Care Glucose Testing Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1Market Overview

- 4.2Drivers

- 4.2.1Growing Strategic Initiatives by the Government and Organizations

- 4.2.2Increasing Pregnancy Rates and Prevalence of Diabetes

- 4.3Restraints

- 4.3.1Required Professional Assistance and Lack of Awareness About Glucose Monitoring in Emerging Countries

- 4.4Porter's Five Forces Analysis

- 4.4.1Bargaining Power of Suppliers

- 4.4.2Bargaining Power of Consumers

- 4.4.3Threat of New Entrants

- 4.4.4Threat of Substitute Products and Services

- 4.4.5Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1By Product Type

- 5.1.1Lancet and Lancing Devices

- 5.1.2Strips

- 5.1.3Meters

- 5.2By Testing Site

- 5.2.1Fingertips

- 5.2.2Alternative Site Testing

- 5.3By End-User

- 5.3.1Professional Diagnostic Centers

- 5.3.2Hospitals & Clinics

- 5.3.3Home Care Settings

- 5.3.4Others

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. MARKET INDICATORS

- 6.1Type-1 Diabetes Population

- 6.2Type-2 Diabetes Population

7. COMPETITIVE LANDSCAPE

- 7.1Company Profiles

- 7.1.1Abbott

- 7.1.2F. Hoffmann-La Roche Ltd

- 7.1.3LifeScan IP Holdings, LLC

- 7.1.4Trividia Health, Inc.

- 7.1.5Ascensia Diabetes Care Holdings AG

- 7.1.6Acon Laboratories Inc.

- 7.1.7ACON Laboratories, Inc.

- 7.1.8Nipro Medical Corporation

- 7.1.9Prodigy Diabetes Care, LLC

- 7.1.10EKF Diagnostics Holdings plc

- *List Not Exhaustive

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

Global Point-of-Care Glucose Testing Market Report Scope

POC testing is a widely used tool to enable the immediate determination of glucose levels in hospitalized patients and facilitate rapid treatment decisions in response to fluctuations in glycemia. The Point-of-Care glucose testing market is segmented into product type, testing site, end-user and geography. By product, the market is segmented into lancet and lancing devices, strips, and meters. By testing site, the market is segmented by fingertips and alternative site testing). By end-user, the market is segmented into professional diagnostic centers, hospitals and clinics, home care settings, and others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America. The report offers the value (USD) for the above segments.