Platelet Aggregation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

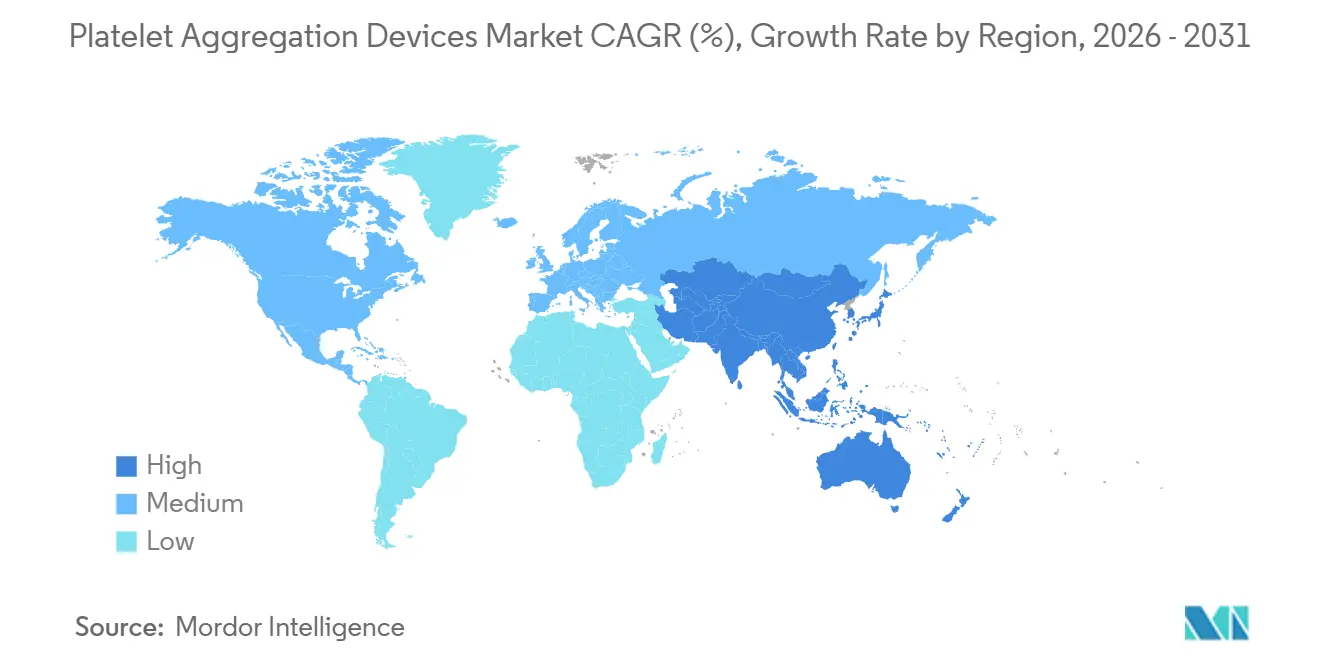

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

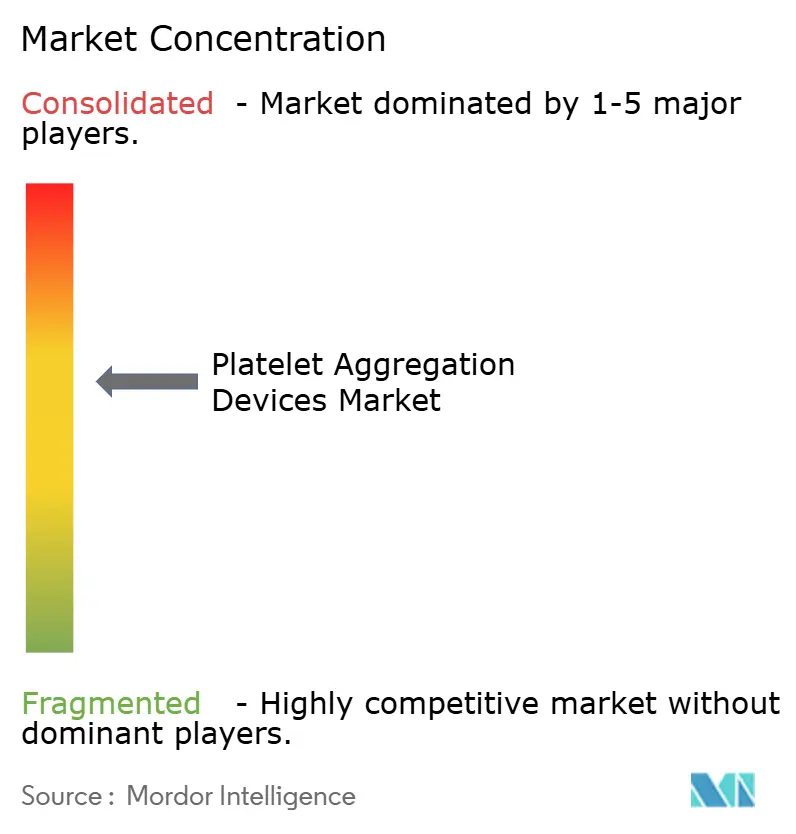

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Platelet Aggregation Devices Market Analysis by Mordor Intelligence

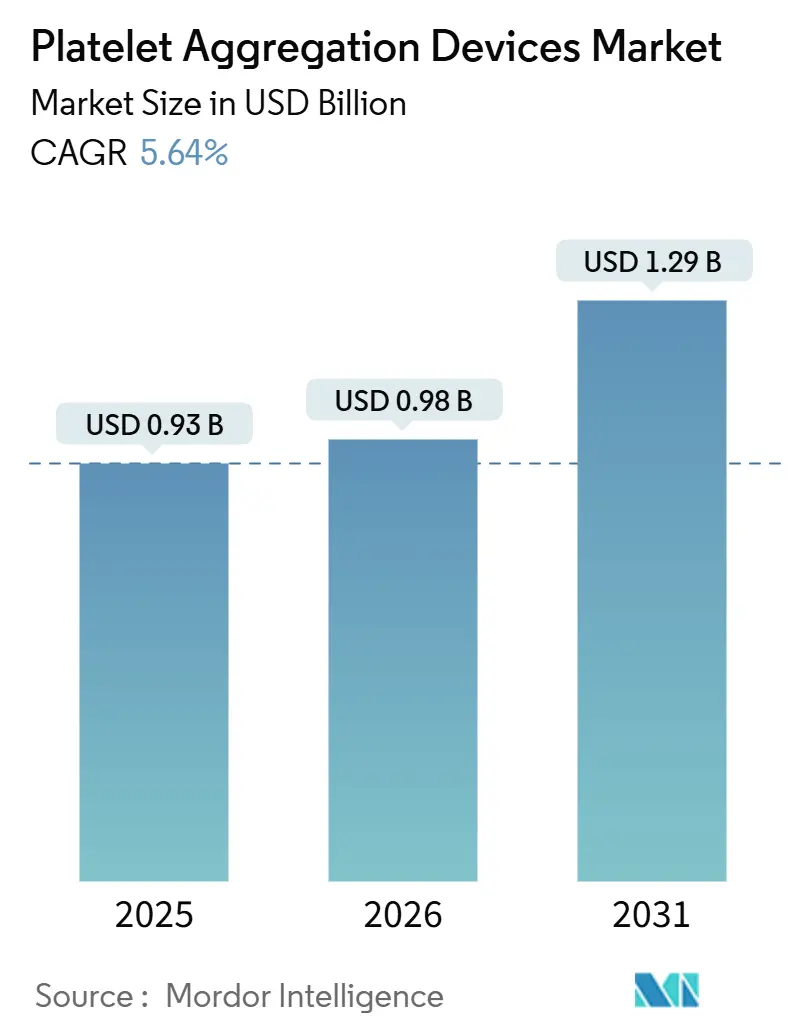

The Platelet Aggregation Devices Market size is projected to expand from USD 0.93 billion in 2025 and USD 0.98 billion in 2026 to USD 1.29 billion by 2031, registering a CAGR of 5.64% between 2026 to 2031.

Automation, miniaturization, and artificial-intelligence-driven interpretation are moving hemostasis testing from manual, plasma-based workflows toward fully integrated whole-blood platforms. Hospital buyers are prioritizing analyzers that shorten turnaround time and enable bedside platelet-function testing because payers now link reimbursement to rapid decision support. Guideline updates from AABB and ICTMG that recommend restrictive platelet transfusion thresholds, together with WHO’s Patient Blood Management framework, further stimulate demand for devices that quantify platelet reactivity at the point of care. Meanwhile, pharmaceutical sponsors have added platelet aggregometry as a mandatory early-phase safety endpoint, nudging contract research organizations to invest in high-throughput platforms compliant with the FDA’s 2025 device guidance on thrombocytopenia monitoring.[1]U.S. Food and Drug Administration. "AI/ML-Enabled Medical Devices: Draft Guidance." FDA, 2024. https://www.fda.gov Against this backdrop, AI-augmented analyzers capable of flagging clopidogrel non-responders in real time are tilting competitive advantage toward vendors that integrate software-as-a-medical-device modules into their hardware roadmaps.

Key Report Takeaways

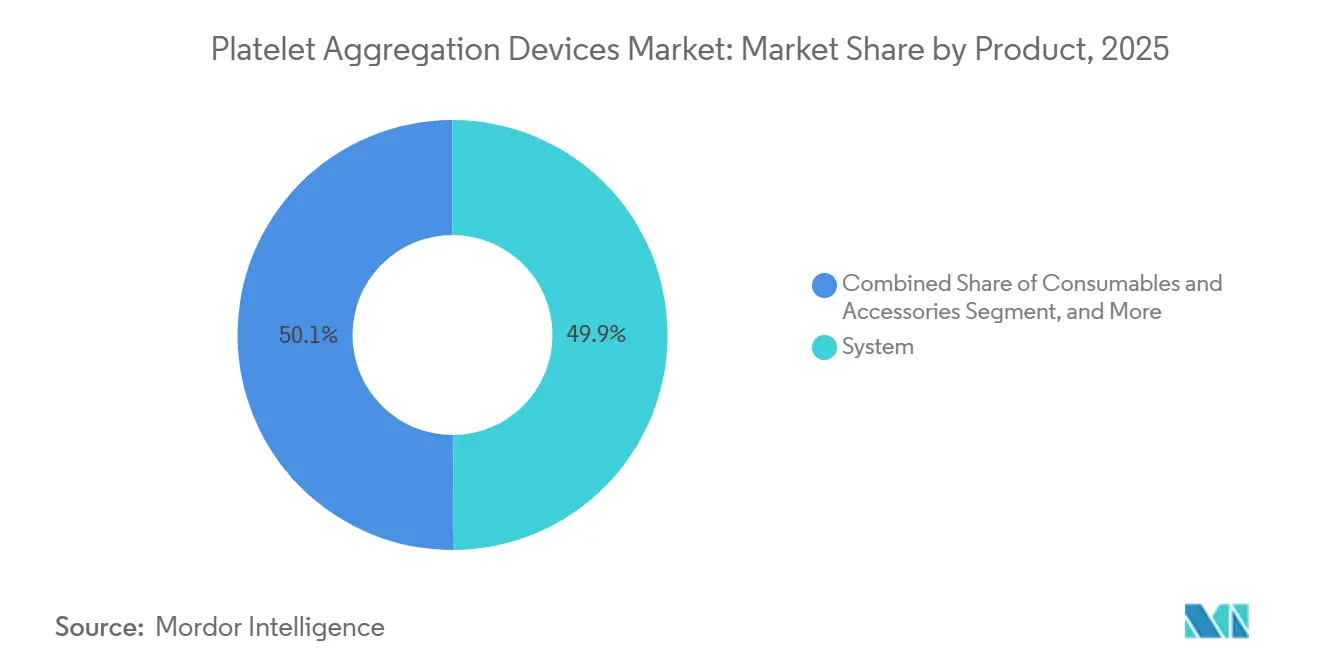

- By product, systems led with 49.90% of platelet aggregation devices market share in 2025, while consumables and accessories are poised to advance at an 8.90% CAGR through 2031.

- By application, clinical testing accounted for 63.50% of revenue in 2025; drug development and toxicology are projected to grow at an 8.78% CAGR through 2031.

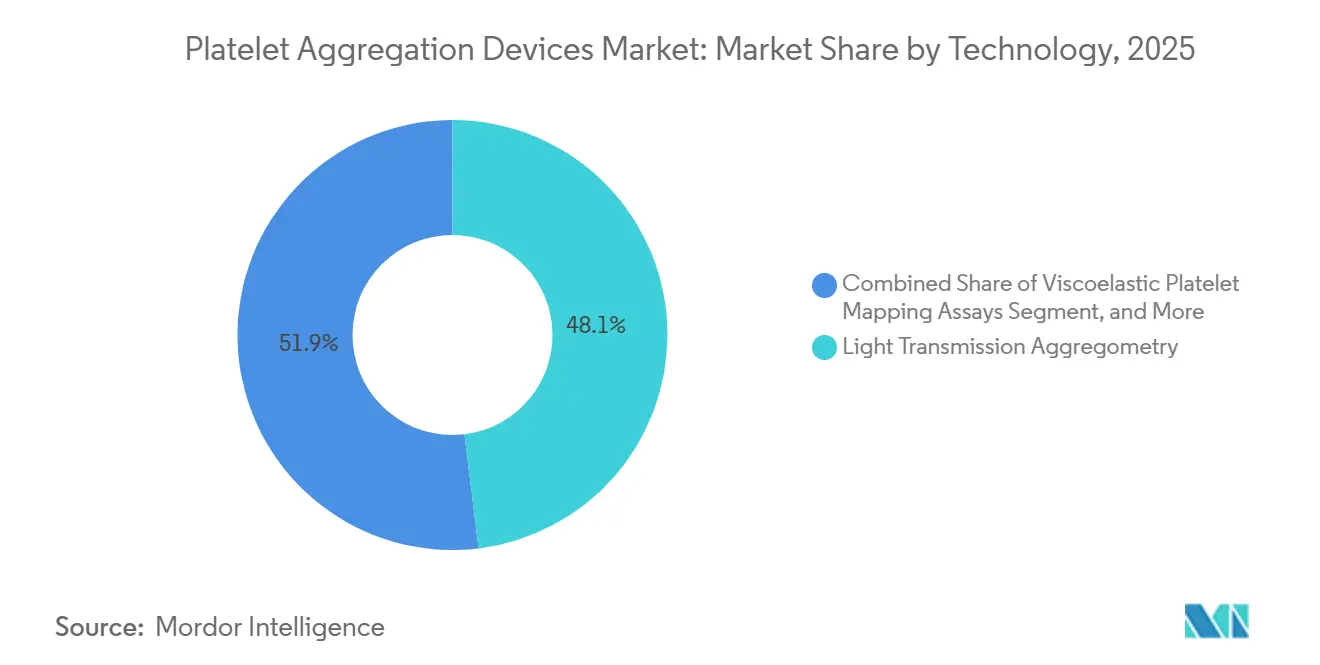

- By technology, light-transmission aggregometry retained a 48.07% share in 2025, whereas microfluidic disc platforms are forecast to accelerate at a 9.23% CAGR.

- By sample type, platelet-rich plasma workflows captured 64.43% of revenue in 2025; whole-blood testing is set to climb at an 8.45% CAGR through 2031.

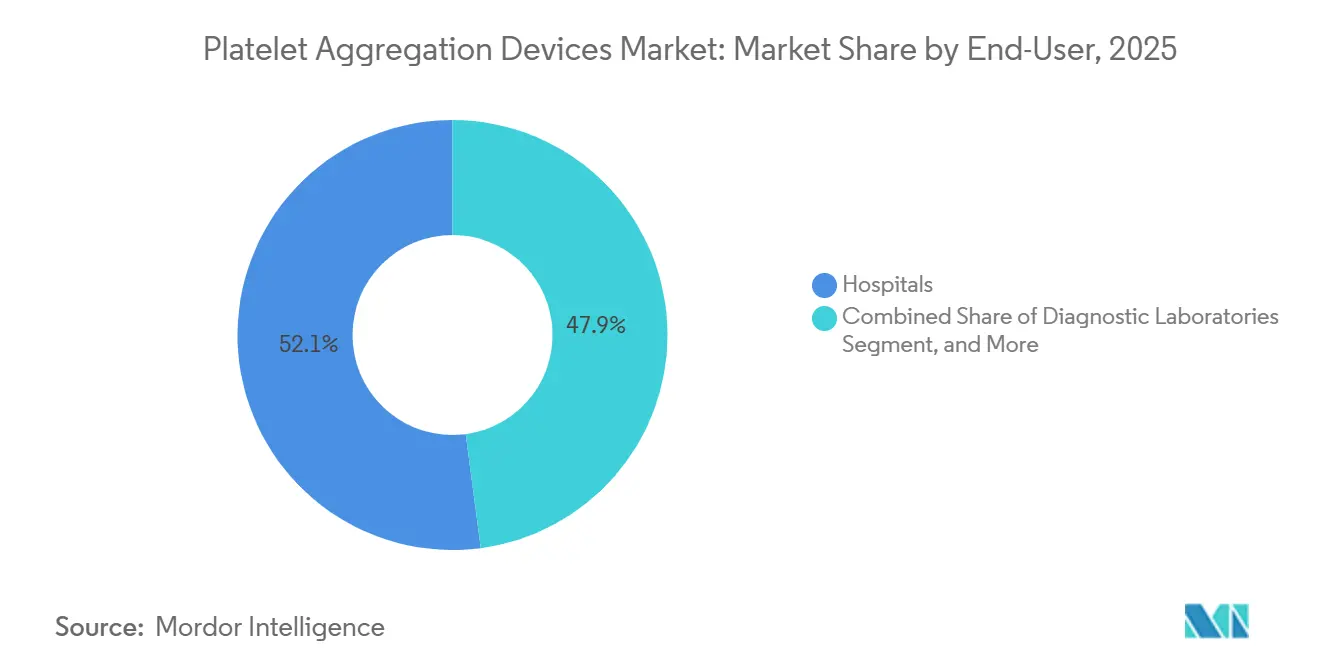

- By end user, hospitals accounted for 52.10% of revenue in 2025, yet research and academic institutes will grow the fastest at a 9.40% CAGR.

- By geography, North America accounted for 39.40% of 2025 revenue, while Asia-Pacific is expected to expand at an 8.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Platelet Aggregation Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising incidence of cardiovascular & bleeding disorders | +1.2% | Global, peak in North America & EU | Medium term (2–4 years) |

| Growing geriatric population base | +0.9% | APAC and Europe | Long term (≥ 4 years) |

| Technological shift to automated/integrated analyzers | +1.5% | North America, Europe, urban APAC | Short term (≤ 2 years) |

| Hospital adoption of point-of-care platelet function testing | +1.0% | North America, Western Europe, GCC | Medium term (2–4 years) |

| AI-driven decision support in antiplatelet therapy | +0.7% | North America, select EU countries | Long term (≥ 4 years) |

| Micro-fluidic disc-based LTA reducing sample volume | +0.3% | Japan, Germany, early global adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Cardiovascular & Bleeding Disorders

Cardiovascular disease prevalence continues to climb, prompting hospitals to increase routine platelet testing volumes. The American Heart Association projects hypertension rates rising to 61% and diabetes to 26.8% by 2050, trends that drive long-term utilization of platelet analyzers.[2]A. Smith et al., “Remote Monitoring of CAR-T Cell Treated Patients,” HemaSphere, journals.lww.com Clinical teams also observe high rates of platelet dysfunction in hematologic therapies such as CAR-T, adding to the complex testing needs of oncology departments. These converging disease burdens intensify demand across the platelet aggregation devices market. National cardiology registries in the United States and the European Union reported an 8% rise in patients receiving dual antiplatelet therapy between 2024 and 2025. Parallel data from the World Federation of Hemophilia counted 418,000 individuals with diagnosed platelet-function disorders in 2024, a 12% increase from 2022.[3]American Heart Association, “Heart Disease and Stroke Statistics-2024 Update: A Report From the American Heart Association,” Circulation, ahajournals.org Interventional cardiologists rely on aggregometers to identify clopidogrel non-responders before percutaneous coronary interventions, while hematologists use the same platforms to phenotype inherited deficiencies, such as Glanzmann thrombasthenia.

Growing Geriatric Population Base

United Nations projections place the global population aged ≥ 65 years at 1.6 billion by 2050, up from 1.0 billion in 2024.[4]R. Brown, “Artificial Intelligence in Thrombosis: Transformative Potential and Emerging Challenges,” Thrombosis Journal, thrombosisjournal.com Aging is associated with endothelial dysfunction and heightened platelet reactivity, complicating anticoagulant management during orthopedic or neurologic procedures. European and North American geriatric wards have begun installing benchtop aggregometers to individualize antiplatelet dosing for hip-fracture repair and stroke rehabilitation. Japanese hospitals, serving the world’s oldest society, run platelet function panels during routine outpatient visits to pre-empt thrombotic events, reinforcing demand for platelet aggregation devices. Vendors that offer low-volume, fully automated platforms capture this demographic-driven spend because more minor sample requirements align with frail-elderly phlebotomy constraints.

Technological Shift to Automated/Integrated Analyzers

Microfluidic chips now process 250 µL whole-blood samples in under 10 minutes while matching gold-standard accuracy, cutting pre-analytical steps and staffing needs.[5]Cerus Corporation, “INT200 Regulatory Clearance 2025,” cerus.com Manual light-transmission aggregometry requires expert technologists, strict temperature control, and roughly 90 minutes from draw to result. Integrated systems now package optical and impedance sensors with pre-loaded reagent cartridges, cutting turnaround time below 30 minutes and slashing operator touches. ISO 18113-5:2024 harmonizes performance claims for devices that bundle multiple hemostasis assays, accelerating clearances and cross-border tenders. Hospitals that consolidated send-out testing into regional core labs during the pandemic find that automated analyzers restore in-house capabilities without rehiring night-shift technologists. Lower staffing overheads, paired with analytics dashboards that merge coagulation, fibrinolysis, and platelet metrics, move procurement toward platforms that future-proof laboratories against reimbursement cuts.

Hospital Adoption of Point-of-Care Platelet Function Testing

Operating rooms, intensive-care units, and emergency departments deploy handheld or cart-mounted aggregometers to refine transfusion decisions in real time. FDA-cleared TDr. PRP-30 device prepares autologous platelet-rich plasma at the bedside, allowing surgeons to adjust dosing mid-procedure. A 2024 multicenter study published in Circulation showed that point-of-care testing shaved 38 minutes off door-to-antiplatelet optimization time and lowered 30-day major adverse cardiac events by 15%.[6]Thrombosis Research, “Whole-Blood Impedance Assay Concordance Study 2025,” thrombosisresearch.com Clinicians treating acute coronary syndrome now stratify therapy based on immediate reactivity measurements, preventing bleed risk in low-reactive patients and escalating therapy in high-reactive cases. As hospitals install integrated perioperative information systems, device connectivity and HL7 messaging become procurement prerequisites, channeling capital budgets toward platforms that satisfy cybersecurity audits and interface seamlessly with EHRs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital & consumable cost of advanced systems | −0.8% | Global; intense in APAC & MEA | Short term (≤ 2 years) |

| Shortage of skilled hemostasis technologists | −0.5% | North America, Europe, urban APAC | Medium term (2–4 years) |

| Regulatory delays for optical-AI hybrid devices | −0.3% | EU, North America | Medium term (2–4 years) |

| Inter-laboratory result variability undermining reimbursement | −0.4% | Global, prominent in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Consumable Cost of Advanced Systems

Fully automated platelet-aggregation workstations list between USD 120,000 and USD 180,000, with annual service contracts adding another USD 15,000–25,000. Consumables cost USD 12–18 per patient, compared with under USD 2 for routine coagulation tests reimbursed under bundled codes. Community hospitals operating on single-digit margins hesitate to invest unless vendors offer reagent-rental contracts that shift capital expense into per-test fees. Even in tertiary centers, cap-ex committees require multidisciplinary utilization cards from cardiology, hematology, and perioperative services to approve a purchase. This cost headwind trims the platelet aggregation devices market CAGR by nearly a percentage point in price-sensitive Asia and Latin America.

Shortage of Skilled Hemostasis Technologists

The U.S. Bureau of Labor Statistics reports 9,000+ job openings for medical laboratory scientists each year against only 4,900 graduates, leaving a 46% vacancy rate.[7]U.S. Bureau of Labor Statistics, “Medical Laboratory Scientist Outlook,” bls.gov Rural laboratories operate with 1 technologist per 1,000 population, forcing some hospitals to outsource aggregometry to reference centers, which adds transport delays. Manufacturers embed video tutorials and automated QC wizards, yet complex differentials such as distinguishing Bernard-Soulier syndrome from immune thrombocytopenia still require expert oversight. Telemedicine hub-and-spoke models partly mitigate the skills gap but do not resolve immediate turnaround-time demands in trauma care. Persisting staff shortages, therefore, cap near-term expansion of the platelet aggregation devices market in advanced economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Advance as Throughput Climbs

Systems generated 49.90% of 2025 revenue, reflecting the legacy installed base of optical and impedance analyzers in hospital core laboratories. Consumables and accessories, however, are set to outpace the overall platelet aggregation devices market with an 8.90% CAGR through 2031, bolstered by single-use microfluidic discs that slash cleaning downtime and cross-contamination risk. Reagent contracts now bundle agonists with software-unlock codes, converting what was once a one-time hardware sale into an annuity stream. As laboratories migrate toward whole-blood impedance methods, demand shifts to new reagent formulations, fragmenting supplier shares and opening space for niche providers of specialty agonists. Accessories such as calibrators and pipette tips hold slim margins but remain indispensable because hospitals must follow manufacturer-validated workflows to safeguard accreditation.

Margins on consumables encourage vendors to preinstall drive locks in their analyzers, forcing hospitals to source supplies exclusively from the original manufacturer to maintain warranty compliance. That lock-in strategy deepens switching costs and reinforces revenue visibility throughout the forecast period. Regional distributors also bundle preventive-maintenance kits with reagent reorder thresholds, increasing annual spend per instrument. Consequently, the platelet aggregation devices market size attributed to consumables will continue to grow steadily, even in mature regions where capital refresh cycles have plateaued.

By Application: Drug Development Becomes a High-Value Niche

Clinical testing accounted for 63.50% of 2025 revenue, as cardiologists and hematologists rely on aggregometry for routine monitoring, preoperative risk assessments, and differential diagnosis of bleeding disorders. The regulatory push for personalized antiplatelet therapy fuels daily test volumes, keeping instrument utilization high in catheterization labs and stroke units. Drug development and toxicology, while smaller, is forecast to expand at an 8.78% CAGR because oncology and cardiovascular trials now require thrombocytopenia surveillance as part of FDA safety checklists. Sponsors demand platforms that output raw kinetic curves for pharmaco-informatics, a capability offered by only a handful of premium devices, thereby commanding higher price points.

Academic consortia investigating platelet involvement in metastasis and neurodegeneration receive European Research Council and NIH grants earmarked for advanced aggregometry.

By Technology: Micro-Fluidics Challenge Incumbent Optical Methods

Light-transmission aggregometry retained 48.07% of 2025 revenue because decades of clinical validation underpin guideline recommendations. Impedance methods appeal to emergency settings by eliminating centrifugation, yet still require electrodes that drive up consumable costs. Viscoelastic platelet mapping, an add-on to thromboelastography, integrates clot formation and platelet function, appealing to cardiac surgery units seeking a single cartridge for comprehensive hemostasis profiling. Microfluidic disc systems are projected to grow at a 9.23% CAGR, the fastest among technology segments, as vendors miniaturize optics and embed machine-learning chips inside disposable discs.

A 2024 Biosensors and Bioelectronics study showed that a six-agonist panel could be performed on 150 µL of whole blood, with results in 12 minutes. Such performance halves turnaround time compared with conventional impedance platforms and meets pediatric phlebotomy volume limits.

By Sample Type: Whole Blood Gains Momentum in Acute Care

Platelet-rich plasma accounted for 64.43% of 2025 revenue because conventional optical assays demand optically clear samples. Yet PRP preparation centrifugation at 150–200 g for 10 minutes, followed by platelet-count adjustment, adds pre-analytical variation and delays. Whole-blood methods will grow at an 8.45% CAGR as emergency departments and operating rooms favor impedance or microfluidic analyzers that accept unprocessed tubes. A 2025 Thrombosis Research article reported 89% concordance between whole-blood impedance and PRP optical tests for aspirin resistance, a threshold sufficient for bedside triage. Rapid-fire trauma protocols now integrate whole-blood platelet-function results with viscoelastic clotting data, enabling balanced transfusion ratios that curb exsanguination.

By End-User: Research Institutes Accelerate Adoption

Hospitals accounted for 52.10% of end-user revenue in 2025, driven by central-lab consolidation and integrated hemostasis workstations that combine coagulation, fibrinolysis, and platelet-function modules. Academic medical centers operate multiple analyzers for 24/7 coverage, whereas community facilities increasingly outsource to reference labs that collect courier samples twice daily. Research and educational institutes will record the fastest growth at 9.40% CAGR through 2031 as NIH and ERC grants finance projects on platelet genetics, cancer metastasis, and neuroinflammation.

Open-architecture systems that export high-frequency aggregation curves to bioinformatics platforms win bids from translational researchers seeking granular kinetic outputs. Contract research organizations, serving pharmaceutical trials, value compliance features like audit trails and 21 CFR Part 11 electronic records, driving premium-tier sales. Diagnostic laboratories, both hospital-affiliated and independent, occupy a stable middle ground, but face payer pressure to bundle coagulation and platelet tests at discounted rates, squeezing margins. Collectively, diversified end-user demand underpins the sustainable expansion of the platelet aggregation devices market.

Geography Analysis

North America accounted for 39.40% of 2025 revenue, driven by hospitals budgeting aggressively for AI-enhanced analyzers and insurers reimbursing high-acuity cardiac procedures. Canada’s Ontario and British Columbia health systems piloted reference-lab hubs that process rural samples overnight, leveraging HL7 interfaces to return results before morning rounds.

Europe enforces stringent evidence requirements under IVDR, pushing manufacturers to concentrate market launches in Germany, France, and the United Kingdom, where notified-body capacity is highest. Germany’s Federal Joint Committee updated hospital quality indicators in 2025 to include platelet-function testing rates for PCI patients, promoting adoption through pay-for-performance incentives. The United Kingdom’s NHS Supply Chain renegotiated framework agreements in 2026, combining consumables and maintenance into outcome-based contracts that reward reductions in downtime.

Asia-Pacific is forecast to grow at an 8.02% CAGR, led by China’s national coagulation-disorder registry, which enrolled 1.2 million patients by end-2025 and mandates platelet-function testing for unexplained bleeding cases. Japan and South Korea, both super-aged societies, prioritize microfluidic disc systems that minimize draw volumes, while Australian trauma centers integrate viscoelastic-plus-platelet cartridges into massive transfusion protocols.

Competitive Landscape

The market is moderately fragmented. Siemens Healthineers, Sysmex, and Werfen retain leadership by bundling hardware, reagents, and informatics into scalable contracts. Siemens and Sysmex maintain a global OEM deal that harmonizes instrument interfaces and reagent menus, lowering the total cost of ownership for large groups. Werfen enhanced its point-of-care portfolio through the 2024 acquisition of Accriva Diagnostics, adding the VerifyNow platform and expanding direct cross-selling reach.

Terumo Blood and Cell Technologies broadens its installed base with automated blood-processing systems that streamline platelet supply for hospitals. Mid-tier suppliers, including Bio/Data Corporation, compete in niche reagent lines and custom agonist panels tailored to translational research. Start-ups focus on chip-based analyzers with smartphone readouts, targeting decentralized and emerging-market buyers. Artificial intelligence features, cloud connectivity, and service-as-a-subscription models differentiate offerings as customers seek outcome-based arrangements. Regulatory expertise and post-market surveillance capacity remain decisive, because tightening rules raise entry barriers and favor firms with mature quality systems. These dynamics ensure steady but competitive progress for vendors active in the platelet aggregation devices market.

Platelet Aggregation Devices Industry Leaders

-

F. Hoffmann-La Roche Ltd

-

Sysmex Corporation

-

Haemonetics Corporation

-

Siemens Healthineers AG

-

Werfen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cerus Corporation secured French and Swiss clearances for INT200, a next-generation LED illumination device that underpins the INTERCEPT Blood System.

- October 2024: Terumo Blood and Cell Technologies introduced the Reveos Automated Blood Processing System in the United States through Blood Centers of America, automating whole-blood separation into components.

Global Platelet Aggregation Devices Market Report Scope

As per the scope of the report, platelet aggregation is a process in which human platelets participate in hemostasis, wound repair, and vessel constriction. It plays a crucial role in inflammation and other pathological situations. The platelet aggregation test involves venipuncture in an anticoagulant medium. This is followed by centrifugation to produce plasma rich in platelets; an aggregometer is then used to assess platelet aggregation.

The platelet aggregation devices market is segmented by product, application, technology, sample type, end-user, and geography. By product, the market is segmented into systems, reagents, consumables, and accessories. By application, the market is segmented into clinical applications, antiplatelet-therapy monitoring, disease & translational research, drug development & toxicology, and others. By technology, the market is segmented into light transmission aggregometry, impedance/multiple-electrode aggregometry, viscoelastic platelet mapping assays, microfluidic disc-based aggregometry, and flow cytometry-based aggregometry. By sample type, the market is segmented into whole blood, platelet-rich plasma (PRP), and washed platelets. By end-user, the market is segmented into hospitals, diagnostic laboratories, blood banks, research & academic institutes, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle-East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers the value (USD) for the above segments.

| Systems |

| Reagents |

| Consumables and Accessories |

| Clinical Applications |

| Antiplatelet-therapy Monitoring |

| Disease & Translational Research |

| Drug Development & Toxicology |

| Others |

| Light Transmission Aggregometry |

| Impedance/Multiple-Electrode Aggregometry |

| Viscoelastic Platelet Mapping Assays |

| Micro-fluidic Disc-based Aggregometry |

| Flow-Cytometry-based Aggregometry |

| Whole Blood |

| Platelet-Rich Plasma (PRP) |

| Washed Platelets |

| Hospitals |

| Diagnostic Laboratories |

| Blood Banks |

| Research & Academic Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Systems | |

| Reagents | ||

| Consumables and Accessories | ||

| By Application | Clinical Applications | |

| Antiplatelet-therapy Monitoring | ||

| Disease & Translational Research | ||

| Drug Development & Toxicology | ||

| Others | ||

| By Technology | Light Transmission Aggregometry | |

| Impedance/Multiple-Electrode Aggregometry | ||

| Viscoelastic Platelet Mapping Assays | ||

| Micro-fluidic Disc-based Aggregometry | ||

| Flow-Cytometry-based Aggregometry | ||

| By Sample Type | Whole Blood | |

| Platelet-Rich Plasma (PRP) | ||

| Washed Platelets | ||

| By End-User | Hospitals | |

| Diagnostic Laboratories | ||

| Blood Banks | ||

| Research & Academic Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the platelet aggregation devices market by 2031?

It is forecast to reach USD 1.29 billion by 2031.

How fast is demand expected to grow in Asia-Pacific?

Asia-Pacific revenue is predicted to register an 8.02% CAGR through 2031.

Which technology segment is expanding the quickest?

Micro-fluidic disc aggregometry is projected to grow at a 9.23% CAGR between 2026 and 2031.

Why are consumables seeing higher growth than systems?

Rising test volumes and the shift to single-use micro-fluidic discs boost consumable sales at an 8.90% CAGR, outpacing hardware refresh cycles.

Which end-user category will add market share fastest?

Research and academic institutes are expected to grow at a 9.40% CAGR through 2031, driven by grant funding for platelet biology.

Page last updated on: