Plastic Sterilization Trays Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

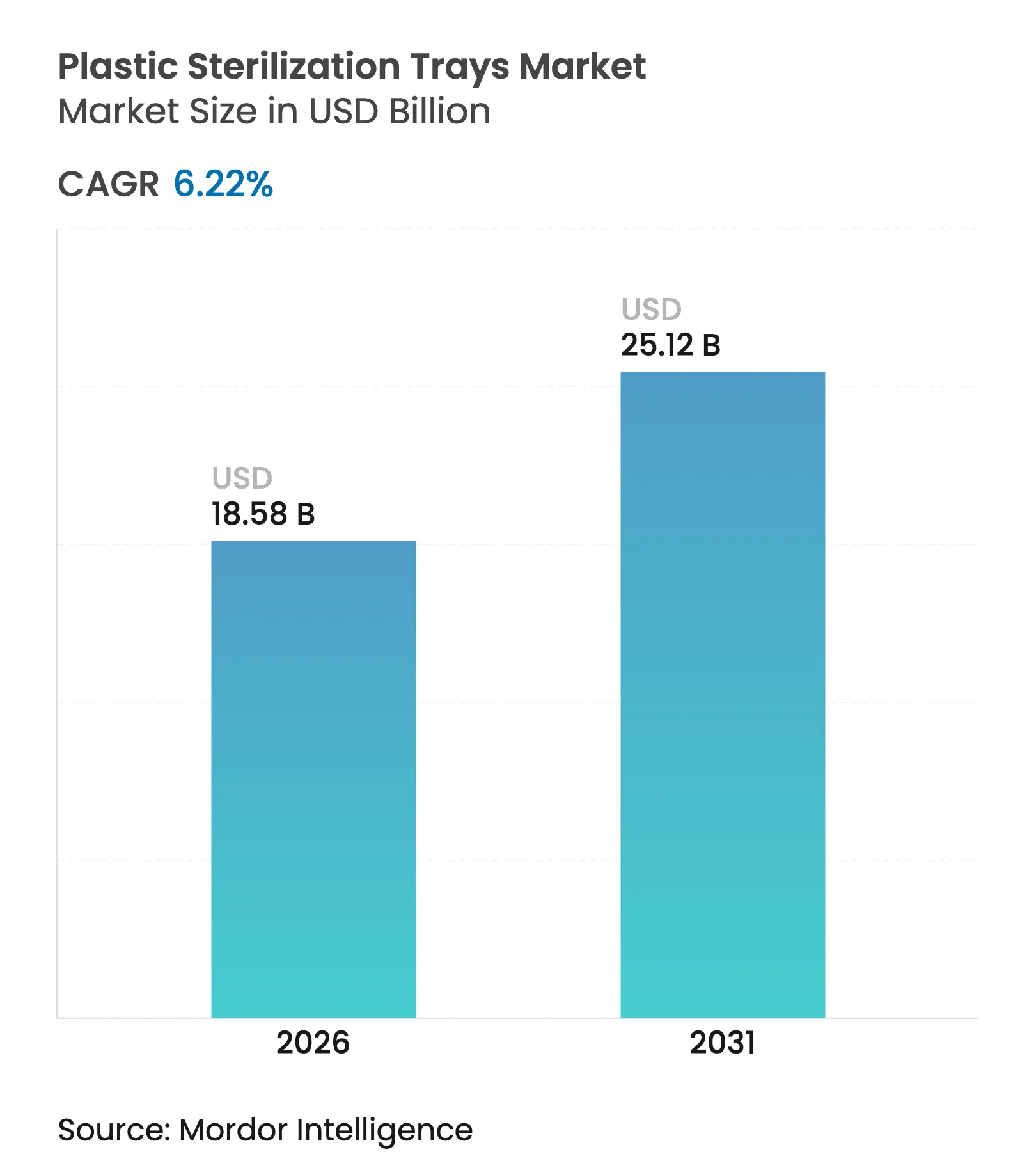

| Market Size (2026) | USD 18.58 Billion |

| Market Size (2031) | USD 25.12 Billion |

| Growth Rate (2026 - 2031) | 6.22 % CAGR |

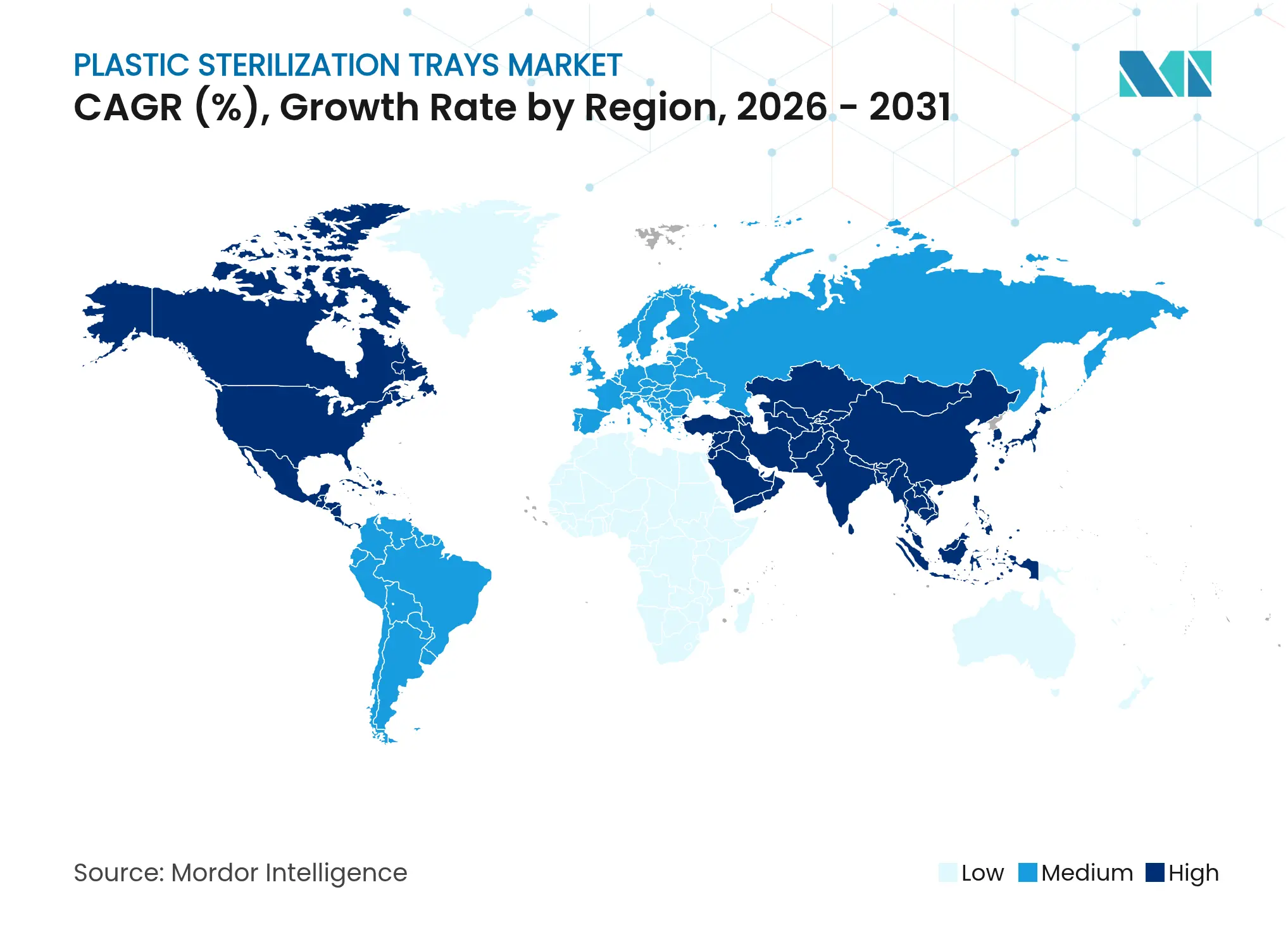

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Plastic Sterilization Trays Market Analysis by Mordor Intelligence

The plastic sterilization trays market size is expected to grow from USD 17.49 billion in 2025 to USD 18.58 billion in 2026 and is forecast to reach USD 25.12 billion by 2031 at 6.22% CAGR over 2026-2031. The expansion reflects rising global surgical volumes, accelerated investment in ambulatory surgery centers, and rapid uptake of high-heat medical-grade polymers that extend tray service life. Healthcare providers are prioritizing reusable trays to trim reprocessing time, while pharmaceutical manufacturers are specifying radiation-compatible systems that safeguard complex biologics. Sustainability mandates in Europe and North America are also nudging procurement toward recyclable copolyesters, prompting suppliers to redesign portfolios around circular-economy criteria. Competitive intensity is heightening as incumbents integrate AI-ready tracking features and pursue targeted acquisitions to strengthen sterilization workflow offerings.

Key Report Takeaways

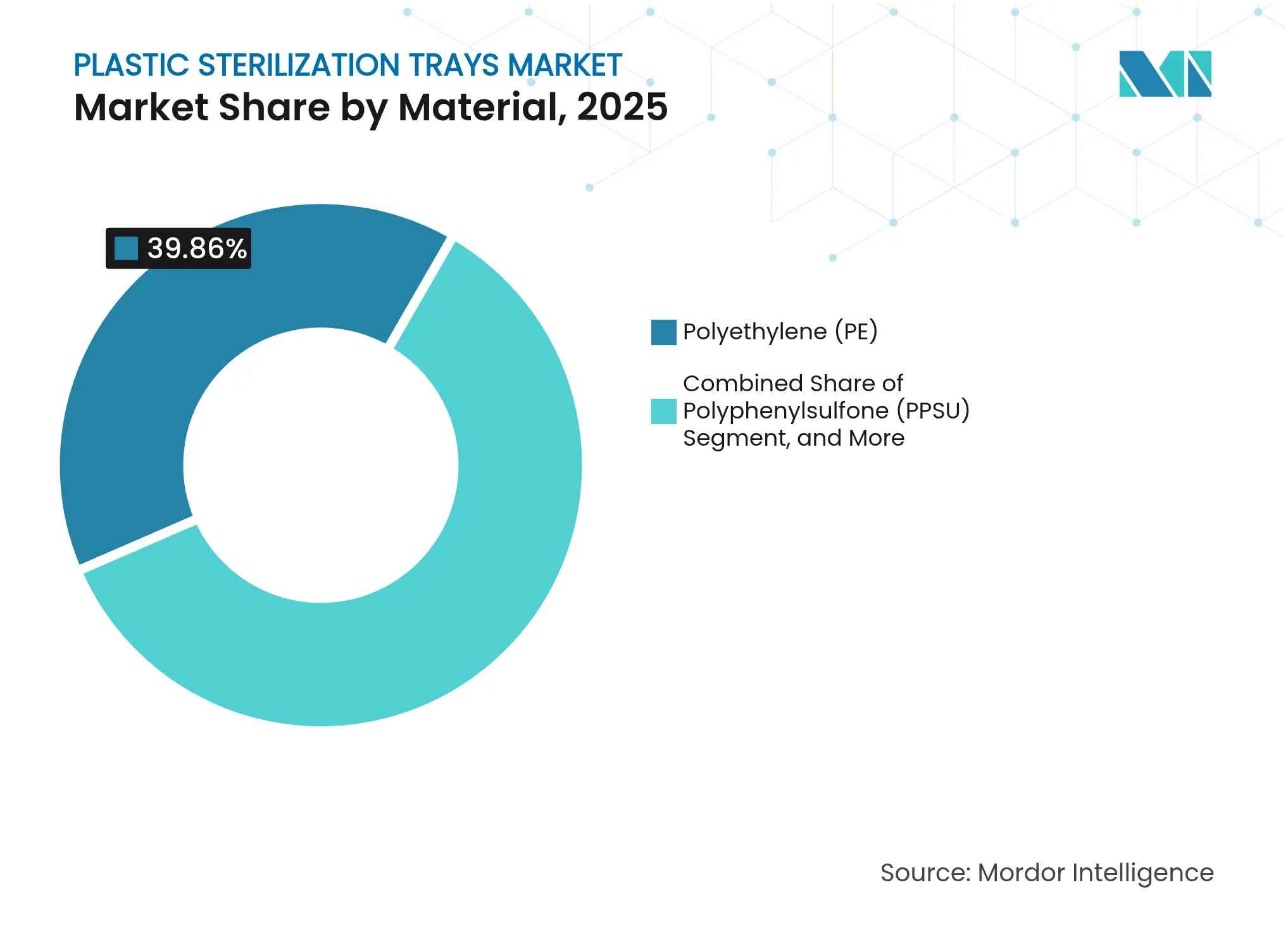

- By material, polyethylene (PE) led with 39.86% revenue share in 2025; polyphenylsulfone (PPSU) is projected to clock the fastest 9.68% CAGR through 2031 .

- By product type, perforated designs captured 65.02% of the plastic sterilization trays market share in 2025, while non-perforated trays are slated to grow at 7.72% CAGR to 2031.

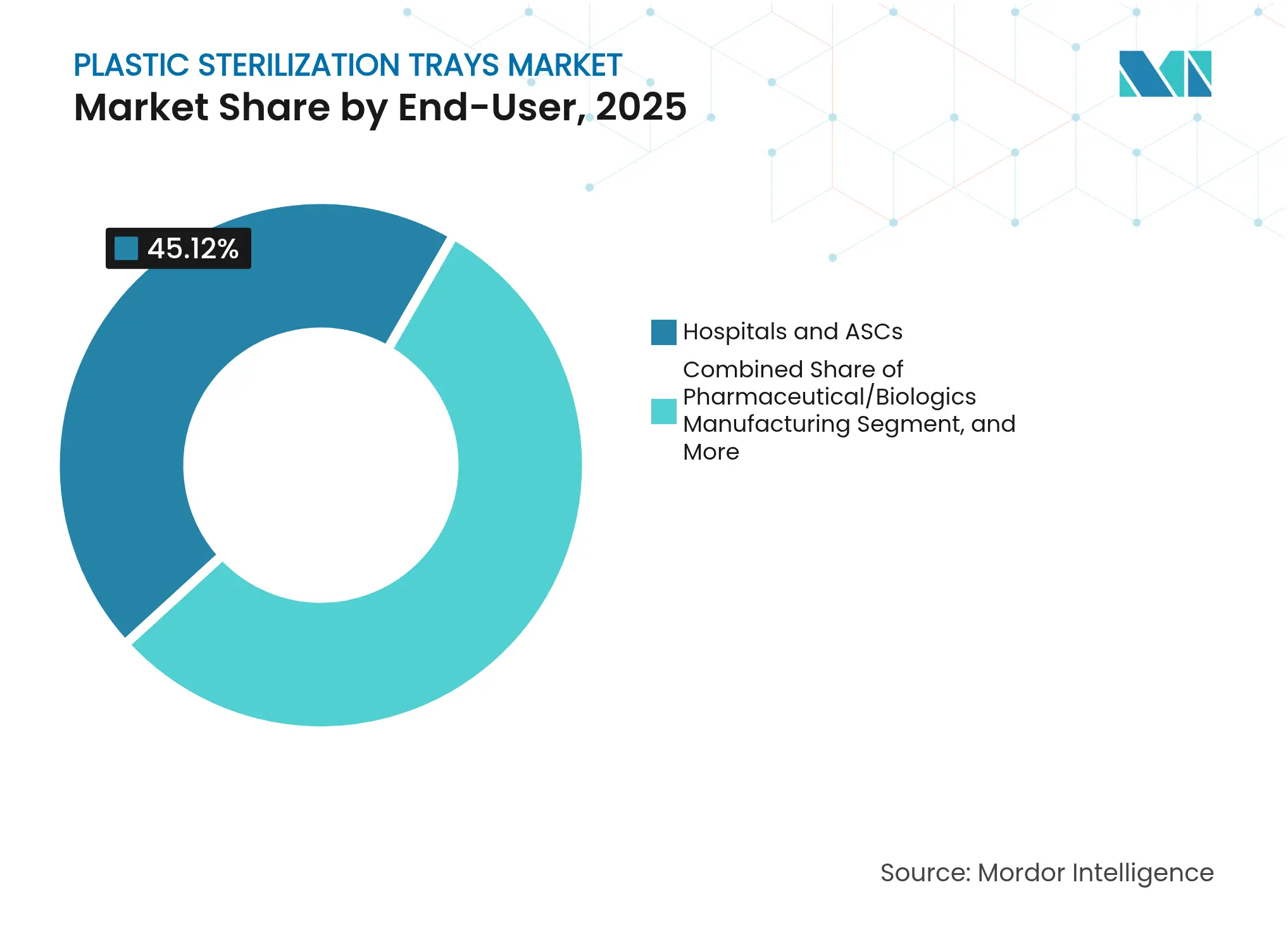

- By end-user, hospitals and ambulatory surgery centers accounted for 45.12% of the plastic sterilization trays market size in 2025; pharmaceutical and biologics manufacturing represents the fastest-growing application at 9.95% CAGR.

- By sterilization compatibility, steam-autoclavable trays commanded 57.66% market share in 2025, whereas gamma and e-beam ready products are expanding at 8.79% CAGR.

- Regionally, North America held 34.21% revenue share in 2025; Asia-Pacific is the high-growth arena with a 9.85% CAGR forecast, underpinned by Japan’s ISO 13485-aligned QMS revisions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastic Sterilization Trays Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Soaring global surgical procedure volumes

Soaring global surgical procedure volumes

| +2.1% | Global, concentration in North America & Asia-Pacific | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

Global, concentration in North America & Asia-Pacific

|

Impact Timeline

:

Medium term (2-4 years)

|

Development of next-gen high-heat plastics

Development of next-gen high-heat plastics

| +1.8% | Global, led by US & European polymer producers | Long term (≥ 4 years) | |||

Hospital push for reusable trays

Hospital push for reusable trays

| +1.4% | North America & Europe | Short term (≤ 2 years) | |||

Expansion of ambulatory surgery centers

Expansion of ambulatory surgery centers

| +1.2% | Asia-Pacific core, spillover to Middle East & Africa | Medium term (2-4 years) | |||

AI-ready color-coded modular trays

AI-ready color-coded modular trays

| +0.9% | North America & selected European markets | Medium term (2-4 years) | |||

Circular-economy procurement preferences

Circular-economy procurement preferences

| +0.7% | European Union, expanding to North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Soaring Global Surgical Procedure Volumes

Ambulatory surgery centers are forecast to expand 21% and reach 44 million procedures by 2034, intensifying demand for efficient sterilization infrastructure.[1]ASC Association, “Ambulatory Surgery Center Growth Projections,” ascassociation.orgAgeing demographics and minimally invasive techniques are accelerating caseloads, pushing hospitals to adopt trays that withstand high-throughput workflows. Operational studies in 2024 showed that reusable plastic systems deliver cost advantages once daily case volumes exceed 15, encouraging widespread switchovers. Singapore’s integrated ASC model cut turnaround times 23% while sustaining zero infection rates after adopting advanced plastic trays. The plastic sterilization trays market benefits directly from this surge as providers seek durable, lightweight solutions that keep pace with rising procedure counts.

Development of Next-Gen High-Heat Medical-Grade Plastics

SABIC enlarged polyetherimide and polyphenylene ether resin lines by 50% and 40% respectively to serve emerging sterilization requirements. These polymers tolerate repeated 134 °C steam cycles and vaporized hydrogen peroxide exposure, aligning with the FDA’s 2024 recognition of VH₂O₂ sterilization . Pharmaceutical majors such as Merck specify PEI-based trays to avoid metal contamination in biologics suites. Although advanced resins command a 15-20% premium, extended lifespans offset upfront costs, reinforcing uptake across premium applications. Consequently, PPSU heads the growth leaderboard within the plastic sterilization trays market.

Hospital Drive for Reusable Trays to Cut Reprocessing Time

Mission Hospital erased 13.8% equipment loss and saved USD 200,000 annually after introducing RFID-enabled trays and tracking platforms. Salem Health Laboratories boosted on-time collections to 98% and trimmed unnecessary testing 73%, translating into USD 13,000 yearly savings . AI analytics from Censis lifted tray throughput 20% without extra staff . These case studies underscore the operational gains that reusable, traceable plastic solutions deliver, supporting rapid installation across surgical hubs.

Expansion of Ambulatory Surgery Centers Worldwide

Tenet Healthcare reported robust 2024 ASC revenue growth as payers channel procedures into cost-efficient outpatient sites . Asia-Pacific governments are relaxing regulations to encourage similar facilities, propelling demand for compact, lightweight trays that integrate with smaller sterilizers. Zimmer Biomet’s collaboration with CBRE to design orthopedic ASC infrastructure highlights commercial momentum . As outpatient surgery volumes climb, the plastic sterilization trays market secures a durable growth vector.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Sustainability backlash against single-use plastics

Sustainability backlash against single-use plastics

| -1.3% | European Union expanding globally | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.3%

|

Geographic Relevance

:

European Union expanding globally

|

Impact Timeline

:

Medium term (2-4 years)

|

Stricter sterilization-validation rules

Stricter sterilization-validation rules

| -0.8% | Global, led by FDA & EU MDR | Short term (≤ 2 years) | |||

Volatile PEI and PPSU resin supply

Volatile PEI and PPSU resin supply

| -0.6% | Global supply chains | Short term (≤ 2 years) | |||

Shift toward disposable procedure packs in niche

specialties

Shift toward disposable procedure packs in niche

specialties

| -0.4% | North America & selected European markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Sustainability Backlash Against Single-Use Plastics Waste

EU PFAS restrictions effective 2025 are eliminating several additives used in medical plastics, forcing tray manufacturers to reformulate materials. Pharmaceutical companies pledging carbon-neutral operations, such as Novartis and Roche, are tightening procurement criteria toward recyclable systems. Yet only 12% of healthcare plastic waste reaches recycling streams, highlighting infrastructure gaps that temper immediate adoption. Infection control teams also flag safety concerns when swapping long-validated plastics, creating a complex trade-off that restrains the plastic sterilization trays market in certain geographies.

Stricter Sterilization-Validation Rules Raising Compliance Costs

The FDA’s 2024 guidance expanded documentation requirements and lifted manufacturer compliance costs by 15-25% . EU MDR has similarly lengthened validation timelines, burdening smaller suppliers with resource-heavy testing. Hospitals must also train staff on new protocols, inflating operational budgets. Although larger players can absorb these costs and even use them as competitive barriers, the aggregate effect weighs on near-term adoption rates within the plastic sterilization trays market.

Segment Analysis

By Material: Advanced Polymers Drive Premium Applications

PE retained 39.86% share in 2025, equating to USD 6.97 billion, because of its low cost and compatibility with both steam autoclave and EtO cycles. The segment benefits from well-established global supply but is constrained in scenarios requiring >120 °C exposure. PPSU is accelerating at a 9.68% CAGR and is expected to outpace other resins through 2031 as biologics plants select chemically inert, radiation-resistant trays. This shift positions PPSU as the focal high-value pocket in the plastic sterilization trays market. Polycarbonate and PEI serve niche demands for optical clarity and high-temperature endurance respectively, while bio-based copolymers are emerging in Europe to meet circular targets.

Demand divergence is sharpening price bands. Hospitals continue to source economical PE trays for standard sets, whereas pharmaceutical buyers accept premiums for PEI or PPSU units that guarantee dimensional stability across multi-modal sterilization. Suppliers are responding with hybrid portfolios that pair commodity resins for general use with advanced polymers for critical processes. Such stratification enables margin preservation even as raw-material volatility persists. Consequently, the plastic sterilization trays market sustains broad material diversity to satisfy disparate performance and cost imperatives.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Perforated Designs Optimize Sterilization Efficiency

Perforated trays accounted for 65.02% revenue in 2025, or USD 11.37 billion, thanks to rapid steam penetration and efficient drying. These attributes underpin their default selection for large instrument sets. Extensive field validation simplifies purchasing approvals, reinforcing dominance. However, solid-wall designs are gaining share driven by precision applications in pharma cleanrooms where particulate control supersedes cycle speed. Solid-wall trays are forecast to grow 7.72% annually, supported by custom foam inserts and shock-absorption liners that secure delicate equipment.

Design innovation now centers on modularity. Hospitals increasingly reorder standardized perforated bases and swap lids or dividers to address changing procedure mixes. Pharmaceutical clients commission molded solid-wall trays with laser-etched identification to support batch traceability. Vendors capable of offering quick-turn customization hold a competitive edge. With sterilization protocols broadening beyond steam, both tray types are being re-engineered for radiation and VH₂O₂ tolerance, sustaining product evolution within the plastic sterilization trays market.

By End-User: Pharmaceutical Manufacturing Drives Innovation

Hospitals and ASCs represented 45.12% or USD 7.89 billion of 2025 spend, reflecting their role as frontline consumers of instrument trays. Their purchasing priorities revolve around durability and turnaround speed, which favor PE-based perforated products. Nevertheless, cost containment pressures push facilities to evaluate total lifecycle expenses, reinforcing interest in longer-lasting high-heat polymers.

Pharmaceutical and biologics manufacturers, while a smaller base, expand at 9.95% CAGR through 2031, propelled by a USD 160 billion investment wave in US capacity. These users demand PPSU or PEI trays validated for gamma or e-beam cycles that avoid thermal stress. Tray purchases are integrated into single-use manufacturing strategies that minimize cross-contamination risks. Clinical research organizations and academic labs show consistent moderate growth, favoring versatile designs that accommodate varied experimental protocols without inflating budgets. As each cohort pursues distinctive performance thresholds, suppliers must tailor offerings across the breadth of the plastic sterilization trays market.

Note: Segment shares of all individual segments available upon report purchase

By Sterilization-Method Compatibility: Gamma Radiation Gains Momentum

Steam-autoclavable formats commanded 57.66% share in 2025 on the strength of entrenched hospital practices. Familiarity with cycle parameters and widespread equipment availability underpin resilience. Yet their dominance is edging downward as pharma producers pivot toward low-temperature or radiation techniques that preserve sensitive biologics. Gamma and e-beam compatible trays therefore post the swiftest 8.79% CAGR and are key growth levers for manufacturers specializing in radiation-stable polymers.

Ethylene oxide remains important for heat-labile devices, though regulatory moves to curb EtO emissions are spurring assessments of VH₂O₂ alternatives that the FDA green-lighted in 2024. Consequently, material science efforts are intensifying around oxidative-resistant plastics. Suppliers that validate trays across multiple modalities can unlock cross-industry opportunities, reinforcing the diversification underway within the plastic sterilization trays market.

Geography Analysis

North America led revenue at USD 5.98 billion in 2025, equivalent to 34.21% market share. High surgical procedure counts and stringent FDA validation standards sustain demand for premium, fully documented tray systems. Strong hospital budgets support replacement of legacy metal sets with light, AI-trackable plastic solutions. Canada and Mexico add momentum via expanding surgical infrastructure and domestic manufacturing incentives, creating a contiguous regional market that values regulatory compliance and supply assurance.

Asia-Pacific is projected to register a 9.85% CAGR, the fastest across regions. Japan’s PMDA alignment with ISO 13485 since March 2024 anchors consistent quality benchmarks. China’s 2024 standards catalogue and anticipated medical device law revisions simplify import pathways for tray vendors with global approvals. India’s CDSCO code of conduct introduces clearer procurement frameworks, underpinning steady growth. Ambulatory surgery center proliferation and public-sector hospital upgrades add layered demand. Local manufacturers are scaling injection-molding capacity, but still depend on imported high-heat resins, offering partnership avenues for global suppliers in the plastic sterilization trays market.

Europe maintains a mature yet innovation-oriented landscape. Circular-economy regulations and PFAS restrictions force material transitions, positioning recyclable copolyesters as a strategic imperative.Germany, France, and the United Kingdom consume the bulk of regional tray volumes owing to established surgical activity and advanced sterilization suites. Eastern Europe delivers incremental growth as healthcare modernization funds unlock procurement of reusable trays that replace ageing metal stock. European buyers increasingly cite environmental scorecards in tender evaluations, rewarding vendors that disclose life-cycle metrics.

Competitive Landscape

Market Concentration

The plastic sterilization trays market remains moderately fragmented. No single player exceeds a 15% revenue contribution, yet larger incumbents leverage global distribution footprints, broad regulatory files, and bundled sterilization equipment to defend share. Stryker’s USD 4.9 billion takeover of Inari Medical in 2024 exemplifies vertical expansion aimed at controlling more of the perioperative value chain. Medline’s USD 950 million purchase of Ecolab’s surgical solutions arm augments its tray and drape range ahead of a planned 2025 IPO. Zimmer Biomet is layering AI-driven guidance and robotic systems onto its tray portfolio through the OrthoGrid acquisition, signaling a pivot to data-rich ecosystems.

Technology partnerships are flourishing. RFID specialists integrate chips directly into tray bases for robust tracking, while software vendors such as Censis embed predictive analytics that flag reprocessing bottlenecks. Material suppliers are co-developing radiation-resistant blends with device makers to secure multiyear supply contracts. Sustainability credentials now influence contract awards, prompting firms to publish recycling programs and carbon-footprint audits. Niche competitors thrive in pharmaceutical segments where customized solid-wall trays command higher margins.

White-space opportunities concentrate on recyclable polymers, AI-enabled inventory management, and integrated validation services that lower compliance overhead. Market entrants with proven circular solutions can carve share as EU regulations bite. Meanwhile, price competition intensifies in the commoditized PE tray tier, compelling manufacturers to automate molding lines and localize production to hedge resin volatility.

Plastic Sterilization Trays Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zimmer Biomet received FDA clearance for Persona Revision SoluTion Femur, expanding nickel-free knee revision options.

- February 2025: Zimmer Biomet reported Q4 2024 net sales of USD 2.023 billion and confirmed plans to acquire Paragon 28 to widen foot and ankle offerings.

- January 2025: MedTech Europe issued sustainability priorities for the forthcoming EU Circular Economy Act.

- December 2024: Zimmer Biomet obtained FDA clearance for OsseoFit Stemless Shoulder System designed for bone preservation.

Table of Contents for Plastic Sterilization Trays Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Soaring global surgical procedure volumes

- 4.2.2Development of next-gen high-heat medical-grade plastics

- 4.2.3Hospital drive for reusable trays to cut reprocessing time

- 4.2.4Expansion of ambulatory surgery centers worldwide

- 4.2.5AI-ready color-coded modular trays for instrument tracking

- 4.2.6Circular-economy purchasing favouring recyclable copolyesters

- 4.3Market Restraints

- 4.3.1Sustainability backlash against single-use plastics waste

- 4.3.2Stricter sterilization-validation rules raising compliance costs

- 4.3.3Volatile PEI and PPSU resin supply inflating tray prices

- 4.3.4Shift toward disposable procedure packs in niche specialties

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Sustainability and Recycling Landscape

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material

- 5.1.1Polyethylene (PE)

- 5.1.2Polycarbonate (PC)

- 5.1.3Polyetherimide (PEI)

- 5.1.4Polyphenylsulfone (PPSU)

- 5.1.5Others Material

- 5.2By Product Type

- 5.2.1Perforated Trays

- 5.2.2Non-Perforated / Solid-Wall Trays

- 5.3By End-User

- 5.3.1Hospitals and ASCs

- 5.3.2Pharmaceutical / Biologics Manufacturing

- 5.3.3Clinical Research Organisations

- 5.3.4Academic and Diagnostic Laboratories

- 5.4By Sterilization-Method Compatibility

- 5.4.1Steam-Autoclavable Trays

- 5.4.2EtO-Compatible Trays

- 5.4.3Gamma / E-Beam-Compatible Trays

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Russia

- 5.5.2.7Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia and New Zealand

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1Middle East

- 5.5.4.1.1United Arab Emirates

- 5.5.4.1.2Saudi Arabia

- 5.5.4.1.3Turkey

- 5.5.4.1.4Rest of Middle East

- 5.5.4.2Africa

- 5.5.4.2.1South Africa

- 5.5.4.2.2Nigeria

- 5.5.4.2.3Egypt

- 5.5.4.2.4Rest of Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Stryker Corporation

- 6.4.2Medline Industries

- 6.4.3Steris plc

- 6.4.4Placon Corporation

- 6.4.5Case Medical

- 6.4.6Kentek Corporation

- 6.4.7Scanlan International

- 6.4.8Key Surgical (Steris)

- 6.4.9Integra LifeSciences

- 6.4.10Sklar Surgical Instruments

- 6.4.11Advin Health Care

- 6.4.12Desco Medical India

- 6.4.13Rumex International

- 6.4.14Zimmer Biomet

- 6.4.15GPC Medical

- 6.4.16KLS Martin Group

- 6.4.17Ace Medical

- 6.4.18G-Flex

- 6.4.19Trimedix

- 6.4.20R.A.C.E. Surgical

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-Space and Unmet-Need Assessment

Global Plastic Sterilization Trays Market Report Scope

Plastic sterilization trays play a critical role in various healthcare and laboratory settings by ensuring the effective cleaning and sterilization of instruments and tools. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The plastic sterilization trays market is segmented by material (Polyethylene (PE), Polycarbonate and Polyetherimide (PEI)), by product type (Perforated and Non-Perforated), by end-user (Hospitals, Drug Manufacturing, Clinical Research Centers and Laboratories) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.