Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.41 Billion |

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

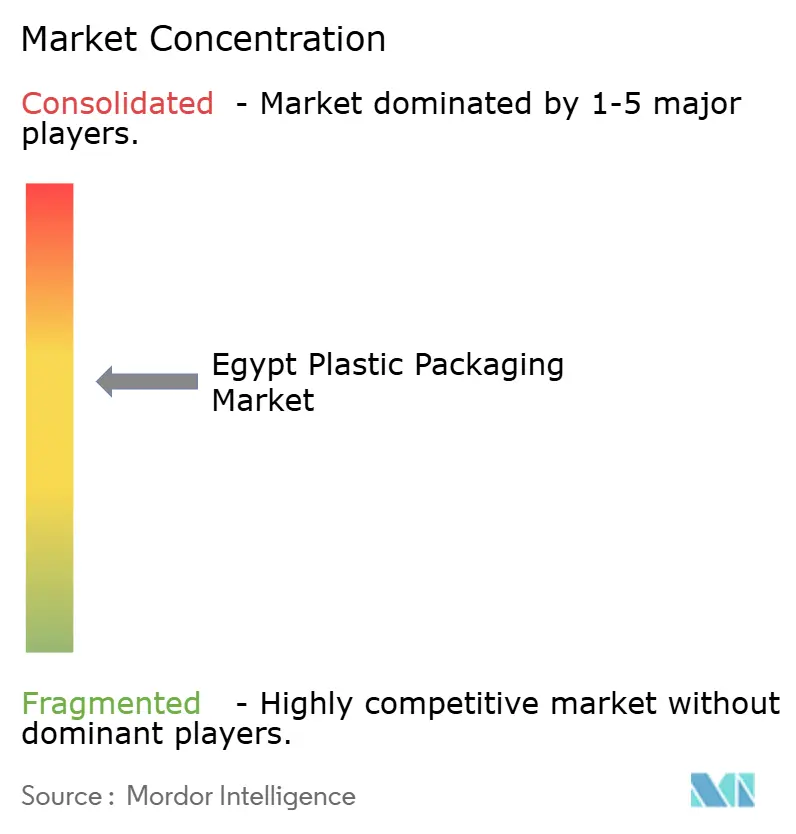

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Plastic Packaging Market Analysis by Mordor Intelligence

The Egypt plastic packaging market size is projected to be USD 2.41 billion in 2025, USD 2.49 billion in 2026 and reach USD 2.94 billion by 2031, growing at a CAGR of 3.37% from 2026 to 2031. A strategically located industrial base, duty-free access to African Continental Free Trade Area members and three-day sea transits to Southern Europe keep freight and lead times lower than Asian sources, drawing export-oriented brand owners into the country. Multinational food and personal-care groups that localize filling lines rely on nearby converters that can certify to ISO 22000 and FSSC 22000, spurring capital inflows into high-speed blow-molding, thermoforming and lamination assets. Polyethylene retains cost leadership because domestic HDPE and LDPE capacity at Alexandria cuts inbound logistics costs, while biodegradable grades see quick uptake wherever single-use bans apply. At the same time, electricity-tariff reforms and crude-linked resin volatility tighten margins, rewarding vertically integrated converters that can hedge feedstock risk or lower energy intensity through lightweighting and co-generation investments.

Key Report Takeaways

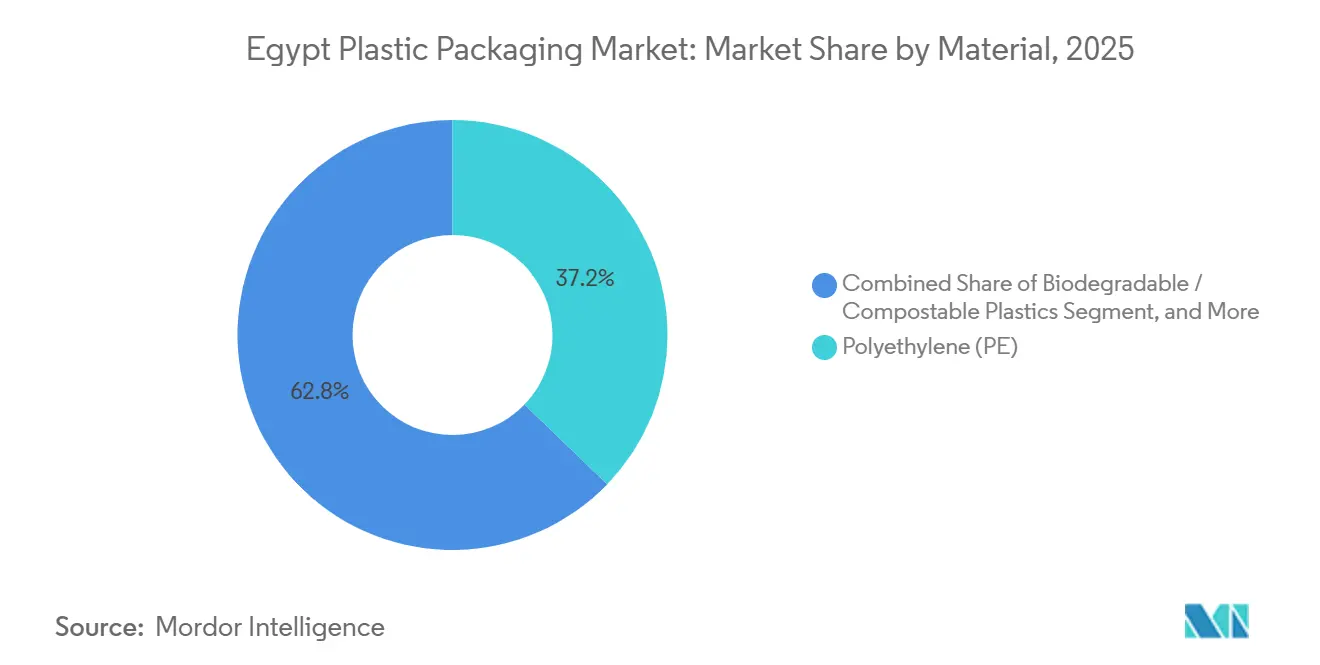

- By material, polyethylene led with 37.21% of Egypt plastic packaging market share in 2025 while biodegradable and compostable plastics booked the fastest 4.52% CAGR through 2031.

- By packaging type, flexible formats captured 60.32% revenue in 2025 and are set for a 3.71% CAGR, whereas rigid formats trail but defend applications that need higher drop resistance.

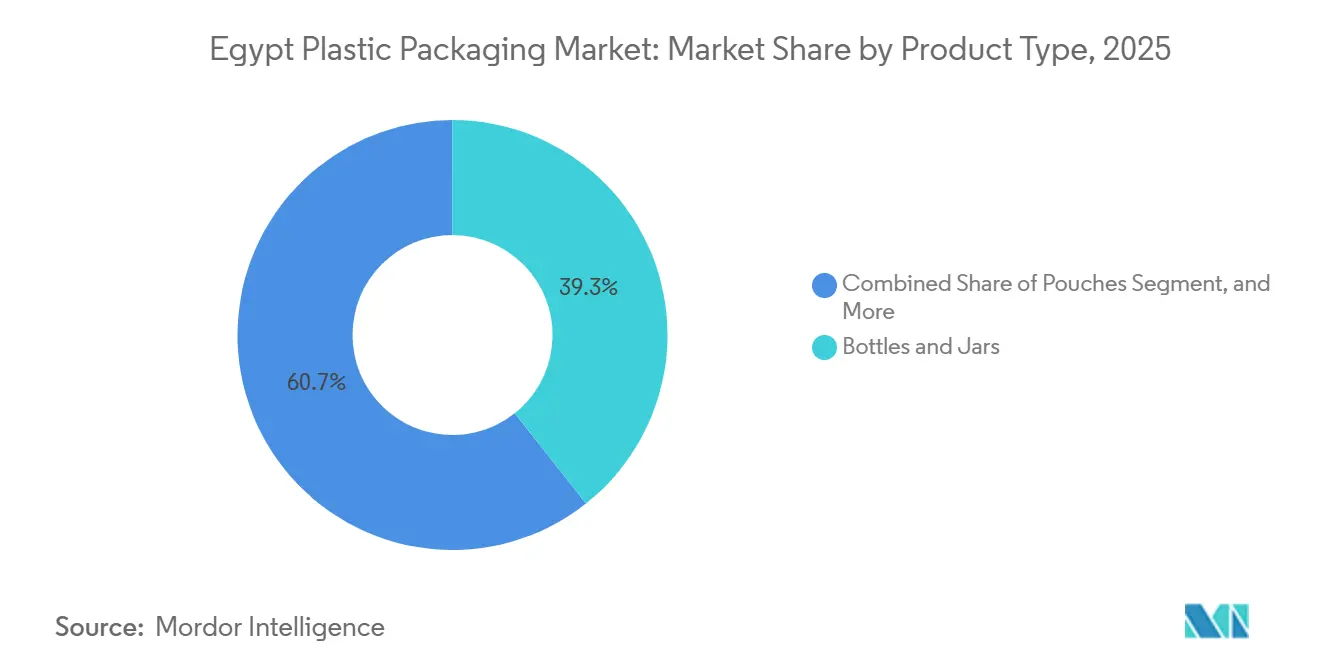

- By product type, bottles and jars accounted for 39.33% of Egypt plastic packaging market size in 2025, yet pouches will outpace all peers at a 4.33% CAGR to 2031.

- By end-user industry, food retained 30.32% demand in 2025, while healthcare shows the strongest momentum with a 4.27% CAGR as European pharmaceutical companies near-shore blister capacity to Egypt.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for flexible food and beverage packs | +1.2% | National, with concentration in Greater Cairo, Alexandria, and Delta governorates | Medium term (2-4 years) |

| Growth in Egyptian FMCG exports | +1.0% | National, with export hubs in Port Said, Suez, and Alexandria | Medium term (2-4 years) |

| Government incentives for local manufacturing | +0.8% | Special Economic Zones in Suez Canal corridor, 10th of Ramadan, and 6th of October cities | Long term (≥ 4 years) |

| Expansion of e-commerce cold-chain packaging | +0.7% | Urban centers: Cairo, Alexandria, Giza, with gradual spread to secondary cities | Short term (≤ 2 years) |

| EU near-shoring of pharma blister lines to Egypt | +0.5% | Industrial zones near Cairo International Airport and Alexandria Port | Medium term (2-4 years) |

| Shipping-cost advantage for domestic PET bottles | +0.3% | National, benefiting local beverage and edible-oil fillers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Flexible Food and Beverage Packs

Flexible formats reduce distribution weight by up to 50%, a vital benefit in Egypt’s fragmented retail system where last-mile logistics can represent 30% of landed cost. Stand-up pouches preserve product integrity without refrigeration, an advantage for mom-and-pop shops that lack stable cold storage. Brand conversions accelerate the shift: major food and personal-care multinationals have switched multiple stock-keeping units from glass jars to retort pouches, cutting breakage and freight expenses. With Egypt generating 4.5-5.0 million tonnes of plastics annually and flexible films already making up about one-third of that waste stream, the dominance of this format is undisputed. Recycling gaps around multi-layer laminates add urgency to mono-material PE or PP structures that still meet barrier needs.

Growth in Egyptian FMCG Exports

Egypt's FMCG export revenue climbed to USD 1.75 billion in 2024 and targets USD 2.4 billion by 2026, a 37% increase that directly translates into packaging demand for shelf-stable foods, personal-care items, and over-the-counter pharmaceuticals bound for Libya, Sudan, and Gulf Cooperation Council markets. Duty-free access across Africa and three-day sailings from Alexandria to Piraeus give Egypt clear logistics and tariff advantages over Asian supply bases. PET bottles and HDPE containers dominate edible-oil, detergent and beverage exports because they tolerate hot-route temperature swings. However, converters must budget for distinct migration tests and labeling to satisfy SASO, EU 1935/2004 and KEBS rules, adding roughly 5-8% to compliance costs. Companies that master multi-jurisdiction regulatory filing keep a competitive edge as volumes scale.

Government Incentives for Local Manufacturing

Ten-year corporate tax holidays, duty-free equipment imports and one-stop customs inside Egypt’s Special Economic Zones reduce total installed costs for new extrusion and molding lines by up to 25%. The 460 km² Suez Canal Economic Zone co-locates resin, masterbatch and finished-pack production, shaving lead times and internal freight. A 2024 public-infrastructure package worth EGP 50 billion (USD 1.6 billion) funded substations, wastewater plants and fiber networks, making greenfield builds more attractive than brownfield retrofits. Power-tariff hikes of 15-20% partly offset these incentives, pushing energy-intensive lines toward solar-hybrid or co-generation solutions. However, electricity-subsidy reforms enacted in mid-2024 raised industrial tariffs by 15 to 20%, partially offsetting SEZ advantages and forcing energy-intensive extrusion lines to invest in co-generation or solar-hybrid systems,.[1]Bloomberg, “Egypt Raises Electricity Tariffs for Industrial Sector 2024,” bloomberg.com Compliance with ISO 14001 and OHSAS 18001 is now a de facto requirement for zone tenancy, aligning with multinational buyer codes.

Expansion of E-Commerce Cold-Chain Packaging

Online grocery penetration in Egypt reached an estimated 4 to 5% of total food retail in 2025, up from negligible levels pre-pandemic, driven by platforms such as Instashop, Rabbit, and Breadfast that promise 60-minute delivery windows in Greater Cairo and Alexandria. Maintaining 2-8 °C along the last mile forces grocers to rely on insulated EPS boxes, gel packs and time-temperature indicators that add USD 0.10-0.15 per parcel. Each order generates close to 200 grams of packaging, nearly double in-store transactions, raising consumer sustainability concerns. Pilots with RFID-tagged reusable totes face reverse-logistics cost barriers but signal the future of urban fulfillment. Converters offering lighter, collapsible insulation solutions are well positioned as order density climbs and cold-chain standards tighten under Egyptian Food Safety Authority oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use plastic bans in tourist governorates | -0.4% | Red Sea, South Sinai, Matrouh, and Alexandria coastal zones | Short term (≤ 2 years) |

| Volatile crude-linked polymer prices | -0.6% | National, affecting all resin-dependent converters | Short term (≤ 2 years) |

| rPET-flake shortages limit recycled content | -0.3% | National, with acute impact on beverage-bottle producers | Medium term (2-4 years) |

| Electricity-subsidy cuts raise extrusion costs | -0.5% | National, most severe for energy-intensive blown-film and thermoforming lines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Linked Polymer Prices

HDPE and PP prices in Egypt follow Brent crude with a four-to-six-week lag, and the floating Egyptian pound magnifies swings. A mid-2024 crude spike to USD 95 per barrel drove an 18% quarter-on-quarter jump in HDPE, compressing commodity-film margins that average 8-12%. Lacking local futures instruments, converters either absorb shocks or pass them through in 30-60-day contract cycles, risking customer defections to Turkish or Saudi suppliers with steadier feedstock. Vertically integrated players with resin offtake agreements mitigate exposure, while spot buyers face existential pressure during prolonged peaks, accelerating industry consolidation.

Electricity-Subsidy Cuts Raise Extrusion Costs

The July 2024 removal of industrial power subsidies increased tariffs by 15-20%, immediately lifting operating costs for blown-film, sheet-extrusion and thermoforming lines. Energy can represent 8-10% of cash cost on thin-gauge film, so the hike erodes already tight spreads unless converters invest in variable-frequency drives, heat-recovery or on-site solar. Some processors shifted night-shift output to off-peak tariffs, but capacity constraints limit the strategy. The tariff shock underscores financing gaps for green energy upgrades, although lenders now bundle concessional loans with equipment suppliers to ease adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PE Dominates, Biodegradables Gain Traction

Polyethylene claimed 37.21% of Egypt plastic packaging market share in 2025 thanks to its availability, process versatility and cost advantage tied to domestic HDPE supply. LDPE and LLDPE maintain leadership in stretch, shrink and heavy-duty sacks, while HDPE continues to anchor blow-molded bottles and crates. PET, sourced from nearby Middle Eastern PTA producers, underpins the beverage segment because of its clarity and gas-barrier qualities, yet rising rPET scarcity threatens recycled-content pledges. Polypropylene fills caps, closures and thin-wall deli tubs that demand elevated heat tolerance. In contrast, polystyrene and EPS retain niche roles in insulation but face headwinds in tourist areas under single-use bans. Biodegradable and compostable resins, although 30-50% costlier, will post a 4.52% CAGR through 2031 as resorts, municipalities and international brand owners escalate sustainability targets.

A 52% informal-sector recycle rate concentrates on PET and HDPE, leaving flexible multi-layer films landfilled or burned. Social enterprise BariQ has recycled 15 billion PET bottles since 2020, exporting all recovered flake to Europe and North America where food-grade demand pays premiums. Local recycler Clipsico Pack moves 60-70 containers monthly of baled PET and HDPE to Turkey and Italy, reflecting Egypt’s tight integration with global secondary-resin flows. The big technical gap sits with laminated pouches combining PE, PET and foil, which evade mechanical recycling. Mono-material barrier laminates could trim flexible-pack waste by up to 40% and represent the next material battleground.

By Packaging Type: Flexible Formats Lead

Flexible packaging captured 60.32% revenue in 2025 and will advance at a 3.71% CAGR, propelled by stand-up pouches, sachets and form-fill-seal films that lower transport costs, maximize shelf aesthetics and run on high-throughput equipment. Snack, powdered-beverage and pet-treat brands value reclosable zippers and laser scoring that improve consumer convenience. Retort pouches enable ambient logistics for ready-to-eat meals, eliminating USD 0.20-0.30 per kilogram in cold-chain spend, a decisive margin in Egypt’s hot climate. Digital printing, still nascent, promises cost-effective short production runs that let marketers test flavors and limited editions without inventory bloat. However, absent chemical-recycling scale, multilayer film disposal remains an unsolved challenge.

Rigid formats held the remaining 39.68% share, with PET bottles continuing to dominate carbonated soft drinks and water, and HDPE containers anchoring dairy, oil and household chemicals. Lightweighting has trimmed average PET bottle weight from 22 grams to 18 grams over a decade, saving resin and freight. Blow-molded bottles also afford striking embossing and in-mold labeling that differentiate brands in cluttered supermarket aisles. Yet growth slows as beverage categories mature and flexible alternatives nibble at sauces and condiments traditionally sold in glass or rigid plastic.

By Product Type: Bottles Dominate, Pouches Surge

Bottles and jars generated 39.33% of Egypt plastic packaging market size in 2025, driven by 1.2-1.4 billion PET bottles consumed annually in beverages and widespread HDPE usage in personal care and detergents. Glass-to-plastic shifts in edible oil, sauces and pharmaceutical syrups continue because plastic cuts breakage and transport fuel by about 30%. rPET-flake shortages, however, impede attainment of 25-30% recycled-content goals and force costly imports from Europe.

Pouches are on course for a 4.33% CAGR to 2031, powered by dairy, baby food and juice brands that favor lightweight, spouted and retort-ready structures. Portion control, improved shelf visibility and compatibility with e-commerce fulfill urban consumer demands. Thermoformed tubs, cups and trays remain staples for yogurt, hummus and deli salads, while industrial IBCs cater to bulk liquids. Clamshells and blisters fill niche roles in electronics and pharmaceuticals.

By End-User Industry: Food Leads, Healthcare Accelerates

Food represented 30.32% of demand in 2025 as manufacturers pursue shelf-life extension through MAP, vacuum sealing and oxygen-barrier films. Egypt’s 105 million population, growing 1.8% yearly, steers steady uptake of ready-to-eat snacks, bakery and frozen options that suit urban lifestyles. Retail consolidation under hypermarkets compresses converter margins by pushing annual price concessions, incentivizing automation and material savings.

Healthcare will post the segment’s fastest 4.27% CAGR through 2031 the fastest among end-users, as Egypt's pharmaceutical exports surge and domestic demand for over-the-counter medicines rises with an aging population and expanding health-insurance coverage.[2] World Health Organization, “Egypt’s Pharmaceutical Industry Overview 2024,” who.int Spurring demand for EU-GMP compliant blister packs, sterile pouches and injection vials. Cleanroom production and stringent validation raise capital hurdles that favor experienced suppliers. Beverages, cosmetics and other industries round out demand, each with separated regulatory expectations that splinter supply chains.

Geography Analysis

Egyptian plastic-packaging capacity clusters in the Nile Delta and Greater Cairo corridor, where proximity to consumers, ports and resin feedstock shortens supply lines and enables just-in-time deliveries. The 460 km² Suez Canal Economic Zone and 10th of Ramadan City host integrated complexes that pair resin cracking, masterbatch compounding and finished-pack production. Alexandria handles close to 60% of container traffic, letting converters ship to Southern Europe within three days, a timeline impossible for Asian rivals.

The Delta governorates—Qalyubia, Gharbia and Dakahlia—specialize in agricultural films, consuming roughly 200,000-250,000 tonnes of LDPE annually for greenhouse and silage wraps. These commodity segments operate on thin spreads and highly seasonal cycles, yet local presence trims inbound freight and offers service speed that foreign suppliers cannot match.

Upper Egypt remains logistics-challenged, relying on trucked-in packs from Cairo and Alexandria. To spread economic development, the government now pairs enhanced tax breaks with land grants for converters that build plants in Assiut, Sohag and Qena. Moreover, Egypt’s tariff-free status within the African Continental Free Trade Area positions it as a springboard for shipments to Nairobi, Lagos and Johannesburg, though exporters must still navigate KEBS, NAFDAC and SABS protocols that add 3-5% to landed cost.

Competitive Landscape

The Egypt plastic packaging market is moderately fragmented, with the ten largest converters holding about 40-45% of revenue and many smaller processors serving regional niches. Global multinationals—Amcor, Huhtamäki, ALPLA and Uflex—run high-speed, highly automated lines and rely on parent-company R and D for lightweighting, barrier coatings and digital printing. Their ISO 22000 and BRC certifications meet multinational buyer mandates and win export orders.[3]International Organization for Standardization, “ISO 22000 Food Safety Management Systems,” iso.org

Local champions such as Rotografia, NatPack, Taghleef Industries and Coveris Flexibles Egypt compete on shorter lead times, flexible minimums and relationships with small and medium food processors. Rotografia’s gravure expertise targets premium confectionery wraps, while NatPack’s blow-molding footprint supplies edible-oil and detergent players. Backward integration is still rare, though some converters have added masterbatch compounding or forward-integrated into contract-packing to boost margins.

White-space opportunities pivot on aseptic-carton alternatives for ambient juice, child-resistant ISO 8317 closures and mono-material laminates that improve recyclability. Technology investments focus on inline vision systems that inspect at 200 meters per minute, reducing waste and customer returns, and on algorithm-driven lightweighting that cuts resin by 8-12%. Converters seeking future differentiation are already pursuing RecyClass or ISCC PLUS certifications to verify circular-economy compliance.

Egypt Plastic Packaging Industry Leaders

Amcor Plc

Huhtamaki Oyj

Uflex Limited

Rotografia Group S.A.E.

ALPLA Werke Alwin Lehner GmbH & Co KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ministry of Industry and Ministry of Housing announced establishment of new five million square meter industrial zone connecting 6th of October City to Alexandria, featuring integrated infrastructure and direct railway connections to Alexandria port.

- March 2025: Egypt implemented Extended Producer Responsibility framework for shopping bags to combat plastic waste risks, establishing new regulatory requirements for packaging manufacturers and importers nationwide.

- February 2025: Food Export Council announced record processed food exports of USD 6.1 billion in 2024, representing 21% increase and driving substantial packaging demand across multiple product categories.

- January 2025: Amcor plc will expand flexible-packaging capacity by 20% at its 10th of Ramadan site, adding high-barrier lamination lines for retort pouches and blister-web substrates, a USD 15 million outlay that creates 80 new jobs.

Egypt Plastic Packaging Market Report Scope

Plastic packaging refers to any type of packaging made from plastic materials that is used to protect, store, transport, and present products. It is widely used across industries such as food and beverages, pharmaceuticals, cosmetics, electronics, and e-commerce.

The Egypt Plastic Packaging Market Report is Segmented by Material (Polyethylene, Polyethylene Terephthalate, Polypropylene, Polystyrene and Expanded PS, Biodegradable/Compostable Plastics, Other Materials), Packaging Type (Rigid, Flexible), Product Type (Bottles and Jars, Tubs/Cups/Bowls/Trays, Intermediate Bulk Containers, Pouches, Other Product Types), End-User Industry (Food, Beverage, Healthcare, Cosmetics and Personal Care, Other End-User Industries).. The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Polyethylene (PE) |

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP) |

| Polystyrene (PS) and Expanded PS |

| Biodegradable / Compostable Plastics |

| Other Materials |

By Packaging Type

| Rigid |

| Flexible |

By Product Type

| Bottles and Jars |

| Tubs, Cups, Bowls and Trays |

| Intermediate Bulk Containers |

| Pouches |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Healthcare |

| Cosmetics and Personal Care |

| Other End-User Industries |

| By Material | Polyethylene (PE) |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP) | |

| Polystyrene (PS) and Expanded PS | |

| Biodegradable / Compostable Plastics | |

| Other Materials | |

| By Packaging Type | Rigid |

| Flexible | |

| By Product Type | Bottles and Jars |

| Tubs, Cups, Bowls and Trays | |

| Intermediate Bulk Containers | |

| Pouches | |

| Other Product Types | |

| By End-User Industry | Food |

| Beverage | |

| Healthcare | |

| Cosmetics and Personal Care | |

| Other End-User Industries |

Key Questions Answered in the Report

What is driving growth in Egypt's plastic packaging industry?

The Egypt plastic packaging market is forecast to reach USD 2.94 billion by 2031, reflecting a 3.37% CAGR from 2026.

Which material currently dominates demand?

Polyethylene leads with 37.21% market share in 2025 because of its versatility and domestic supply security.

Which product format is expanding the fastest?

Pouches are projected to post a 4.33% CAGR to 2031 as dairy, baby food and condiment brands migrate from glass or rigid plastic.

Why is healthcare packaging growing so quickly?

EU near-shoring of blister lines and rising pharmaceutical exports will push healthcare demand at a 4.27% CAGR through 2031.

What is the main sustainability hurdle?

Egypt lacks large-scale recycling for multi-layer flexible laminates, prompting a pivot toward mono-material PE or PP structures to enable mechanical recovery.

How will energy costs influence converters?

July 2024 electricity-tariff hikes of 15-20% encourage investment in lightweighting, variable-frequency drives and solar-hybrid power to safeguard margins.

Page last updated on: