Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 70 Billion |

| Market Size (2026) | USD 73.73 Billion |

| Market Size (2031) | USD 95.56 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Plastic Packaging Market Analysis by Mordor Intelligence

The Europe plastic packaging market size is expected to grow from USD 70 billion in 2025 to USD 73.73 billion in 2026 and is forecast to reach USD 95.56 billion by 2031 at 5.33% CAGR over 2026-2031. This trajectory highlights the sector’s ability to withstand new regulatory costs, energy price shocks, and supply chain volatility while unlocking opportunities through e-commerce expansion, increased recycling capacity, and stable food demand. Heightened EU mandates on recycled content now reward companies that can secure high-quality rPET at scale, giving vertically integrated players a cost edge. E-commerce parcel growth has increased demand for lightweight, protective packaging formats that strike a balance between material reduction and product safety. Rapid investment in AI-enabled sorting systems is narrowing the gap between recycled-material supply and brand-owner targets, while bio-based polymers attract capital as FMCG groups pursue fossil-free packaging. At the same time, volatile virgin-resin prices and differing national tax regimes oblige manufacturers to revise pricing strategies quickly or risk margin erosion.

Key Report Takeaways

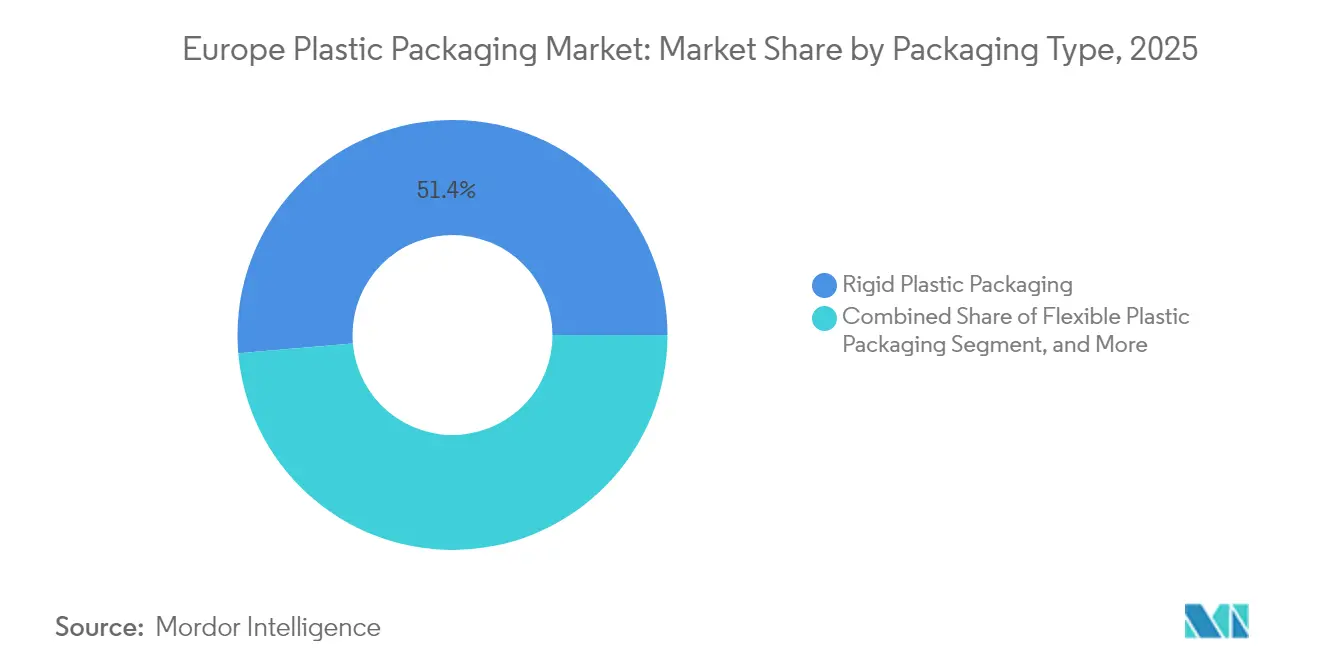

- By packaging type, the rigid plastic packaging segment accounted for 51.35% of the Europe plastic packaging market share in 2025.

- By material, the Europe plastic packaging market for bioplastics & bio-based plastics is expected to advance at an 10.95% CAGR between 2026-2031.

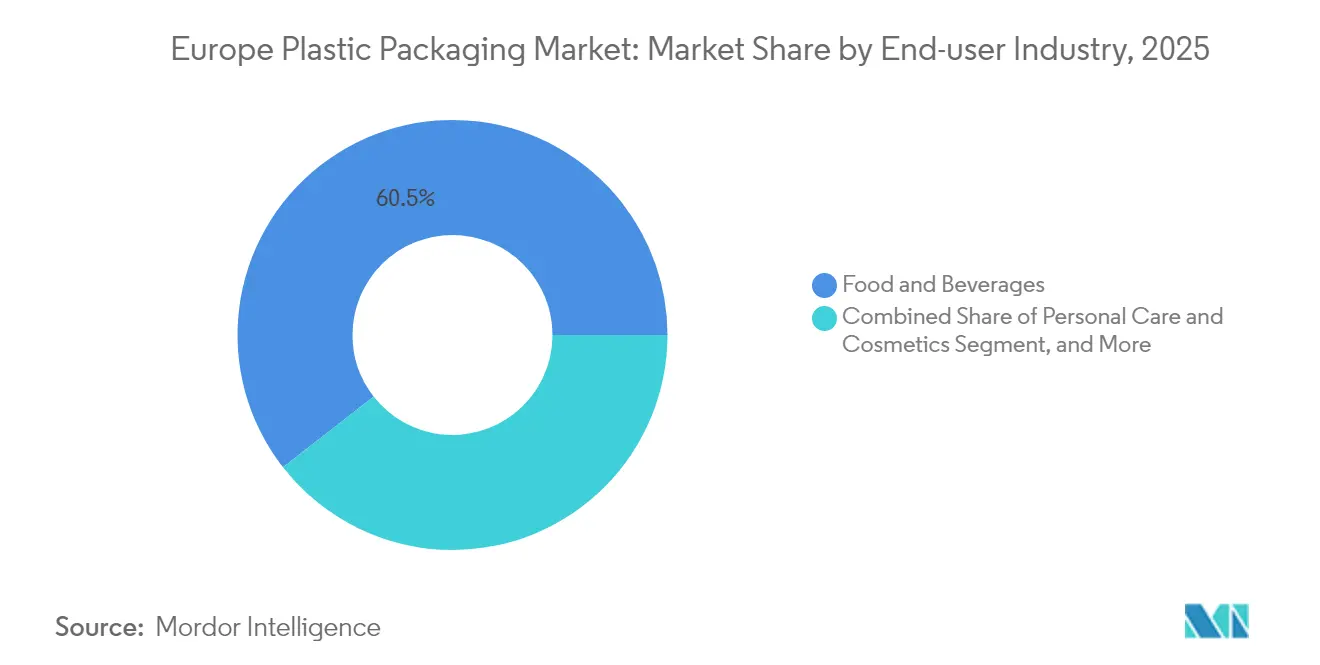

- By end-user industry, the food and beverages segment commanded 60.55% of the Europe plastic packaging market size in 2025.

- By geography, Germany held 23.75% of the European plastic packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU recycled-content mandates | +1.2% | EU-wide, strongest in Germany, Netherlands, Belgium | Medium term (2-4 years) |

| E-commerce demand for lightweight formats | +0.8% | Western Europe centric | Short term (≤ 2 years) |

| Food-grade rPET capacity in DACH | +0.6% | Germany, Austria, Switzerland | Medium term (2-4 years) |

| FMCG shift to mono-material pouches | +0.4% | Early adoption in Nordic countries | Long term (≥ 4 years) |

| AI-enabled high-yield sorting | +0.3% | Germany, Netherlands, France | Medium term (2-4 years) |

| Pharma cold-chain demand for rigid PET | +0.2% | Key pharma hubs across EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Packaging-Waste Targets Accelerating Recycled Content Mandates

The Packaging and Packaging Waste Regulation (PPWR), effective February 11, 2025, sets a 30% recycled-content threshold in PET food packs by 2030, establishing uniform compliance rules that favor large-scale recyclers. [1]PackagingLaw.com Staff, “The New EU Packaging and Packaging Waste Regulation—Highlights and Challenges Ahead,” packaginglaw.comEco-modulated EPR fees now tilt material-selection decisions toward easily recyclable designs, prompting companies such as ALPLA to lift Polish food-grade rPET output from 30,000 tpa to 54,000 tpa. The removal of PFAS in food contact layers deepens the need for alternative barrier technologies while reinforcing the competitive moat of firms with certified rPET capacity.

E-commerce Boom Boosting Lightweight Protective Formats

A structural surge in online shopping has increased parcel volumes and intensified pressure to reduce packaging weight per shipment. Brand owners are adopting mono-material cushions that cut material use by 25% yet safeguard products in high-velocity fulfillment networks. [2]Packaging Europe Editorial Team, “Recyclable Mono-Polypropylene Pouch Revealed by Capri-Sun,” packagingeurope.comPPWR rules that favor source-reduction dovetail with courier incentives to trim dimensional weight, amplifying demand for thin-gauge films and recyclable mailers produced by flexible-packaging converters.

Food-Grade rPET Capacity Expansions Across DACH Region

Producers in Germany, Austria, and Switzerland are adding tray-to-tray PET recycling loops to secure food-contact resin and mitigate import risk. Faerch’s Cirrec unit now processes the equivalent of 1.2 billion PET trays per year, helping close Europe’s 3.5 million-ton rPET gap. [3]Plasticker Reporters, “German Plastics Production 2024 Review,” plasticker.deDACH leadership in testing protocols and logistics makes the region a benchmark for circular rigid-packaging models.

FMCG Shift to Mono-Material Pouches for Curb-Side Collection

Global brands are replacing multilayer laminates with single-polypropylene structures that meet curb-side recycling criteria without sacrificing barrier performance. Capri-Sun’s PP pouch cuts CO₂ by 25% and exemplifies how redesign plus consumer acceptance can unlock scale for mono-material flexibles. Nordic nations supply proof points for collection efficacy, encouraging broader EU rollout.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile virgin-resin prices | -0.9% | EU-wide, acute in Germany, Netherlands | Short term (≤ 2 years) |

| PPWR compliance-cost overhang | -0.6% | EU-wide with differing national burdens | Medium term (2-4 years) |

| Food-contact rPET scarcity | -0.4% | Severe in DACH | Medium term (2-4 years) |

| Anti-dumping duties on PET imports | -0.2% | Central and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin Resin Prices Linked to Energy Crisis

Energy expense now consumes up to 70% of the cost of goods for some converters as natural-gas prices remain more than fourteen times their ten-year average, leading to production curtailments and 2,068 insolvencies in the German packaging sector in February 2025. The decoupling of virgin and recycled pricing complicates procurement hedges and shrinks working-capital buffers for SMEs.

PPWR Draft Creating Compliance-Cost Overhang

Mandatory design-for-recycling rules, recyclability certification, and new tracking systems oblige companies to accelerate R&D outlays at a time of tight liquidity. Smaller converters face steep learning curves for digital product passports and recycled-content verification, heightening consolidation risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Established Rigid Leadership, Agile Flexible Growth

Rigid formats accounted for 51.35% of the European plastic packaging market share in 2025 thanks to their proven performance in dairy, pharma, and industrial chemicals. The European plastic packaging market size for rigid applications is projected to grow steadily as high-barrier PET and HDPE containers comply with strict shelf-life and safety norms. Consolidation, exemplified by Faerch’s purchase of PACCOR, is yielding scale efficiencies and reinforcing closed-loop tray recycling infrastructure. However, cost pass-through remains challenging when resin price spikes outpace customer contracts.

Flexible packaging trails in share yet leads in momentum, advancing at a 5.18% CAGR through 2031 as e-commerce and click-and-collect dominate retail logistics. Lightweight mailers, stand-up pouches, and mono-PE films help shippers cut freight emissions. The European plastic packaging market size for flexible formats gains additional lift from PPWR incentives that reward material minimization. Success depends on commercializing curb-side compatible mono-material films and securing supply of compatible recyclates to satisfy brand-owner pledges.

By Material Type: PET Dominates but Bio-Based Formats Accelerate

PET maintained a 28.65% share in 2025 because of its versatility, clarity, and extensive bottle-to-bottle recycling network. Yet rPET premiums, anti-dumping rules, and Asian import competition erode margins, prompting converters to diversify resin portfolios. The European plastic packaging market size tied to PET may plateau unless food-grade pellet supply expands in lockstep with PPWR quotas.

Bio-based polymers, including PLA and PHA, record the highest 10.95% CAGR as FMCG brands target carbon neutrality. Capacity ramp-ups from 2.4 million t in 2021 to 7.6 million t by 2026 illustrate investor confidence. Although higher priced than incumbents, bio-based resins attract end-users aiming to decouple from fossil-fuel volatility. Their drop-in compatibility with existing lines shortens adoption cycles, provided compostability labels align with local infrastructure.

By End-User Industry: Food Stability Meets E-commerce Disruption

Food and beverage brands represented 60.55% of demand in 2025, relying on mature supply chains and proven shelf-life validation. The European plastic packaging market size attached to food will continue to advance as chilled, ready-meal, and functional-beverage categories grow. Yet retailers now penalize excessive secondary packaging, nudging suppliers toward thinner films and high-recycled-content trays.

In contrast, e-commerce parcel volumes are climbing at a 9.12% CAGR through 2031, pushing converters to deliver shippable, frustration-free formats. Poly-mailers and inflatable cushions must endure rough handling while meeting recyclability checks at curb-side. Healthcare, cosmetics, and industrial components form resilient mid-sized subsectors where stringent regulatory or technical specs preserve value, albeit at slower growth trajectories than e-commerce.

Geography Analysis

Germany remains the anchor of the European plastic packaging market with a 23.75% share in 2025, supported by EUR 100 billion in annual plastics turnover and 310,000 employees. However, elevated power tariffs and recessionary consumer demand limited 2024 production growth to 3% and drove a 3% revenue drop to EUR 26.7 billion. For 2025, a 0.5% output contraction is expected as converters rationalize capacity and accelerate renewable-energy sourcing. Despite these headwinds, Germany’s dense network of 28 chemical parks and over 40 clusters continues to attract R&D in barrier technologies and AI-sorting pilots.

Poland exhibits the fastest growth at a 6.65% CAGR thanks to its USD 688 billion food-processing base and a retail packaged-food channel forecast to hit USD 50.3 billion by 2028. Foreign investors such as Saica Group have entered via acquisitions that add corrugating and converting scale, signaling confidence in sustained volume expansion. Nonetheless, Poland’s collection infrastructure lags Western peers, prompting the government to levy fees on plastic takeaway packs as an interim waste-management measure.

Elsewhere, the United Kingdom, France, Italy, Spain, and Russia comprise sizable but heterogeneous demand pools. The Netherlands leads on fossil-free packaging goals, while Belgium attains 79.2% recycling rates. Nordic countries, leveraging advanced fiber-based innovations and deposit systems, outperform on circularity metrics. Across Europe, total packaging value is poised to rise from EUR 153 billion in 2024 to EUR 186 billion by 2029, with sustainability directives catalyzing capital spending on recyclate procurement, barrier-coating upgrades, and digital tracking.

Competitive Landscape

The European plastic packaging market features moderate fragmentation but is trending toward consolidation as compliance costs soar. Amcor’s all-stock merger with Berry Global will create a global giant targeting USD 650 million in annual synergies and USD 180 million in combined R&D, illustrating the scale imperative. Larger entities are best placed to absorb the expense of PPWR audits, digital product passports, and renewable-energy transitions.

Technology leadership has emerged as a key differentiator. Early adopters of AI-driven sortation enjoy superior yield and access to high-grade recyclates that command brand-owner premiums. DS Smith’s TailorTemp launch demonstrates how innovation in temperature-controlled fiber-based packs can open high-margin pharma channels. Similarly, partnerships such as Amcor-NOVA Chemicals on mechanically recycled PE help lock in feedstock and satisfy 30% recycled-content pledges.

At the same time, smaller regional converters face margin pressure from resin cost swings and capital-intensive upgrades. Many are exploring niche plays in decorative finishes, short-run digital printing, or specialty dispensing to avoid direct competition with integrated majors. The race to secure food-contact rPET remains intense; firms without captive capacity often sign multiyear offtake agreements or pursue joint ventures with recyclers to guarantee supply.

Europe Plastic Packaging Industry Leaders

Amcor PLC

Sealed Air Corporation

Mondi Group

ALPLA Werke GmbH

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DS Smith launched TailorTemp recyclable temperature-controlled pack, keeping pharma products cool for 36 hours and cutting CO₂ by 40%.

- January 2025: Amcor and Berry Global scheduled shareholder votes for mid-2025 completion of all-stock merger targeting USD 650 million in synergies.

- January 2025: Amcor signed MoU with NOVA Chemicals to source mechanically recycled PE for flexible films.

- November 2024: DS Smith announced EUR 34 million capacity boost in Hungary focusing on automation and sustainability.

Europe Plastic Packaging Market Report Scope

Packaging solutions that are durable, lightweight, and comfortable have augmented the usage of plastics as a packaging material across the region. Plastic packaging vendors are now implementing new ways of functioning in the packaging industry.

Europe's plastic packaging market is segmented by type (rigid plastic packaging and flexible plastic packaging), material type (pe, pp, pvc, and pet), end-user industry (food, healthcare and pharmaceutical, beverage, cosmetics, and personal care), and country (United Kingdom, Germany, France, Spain, Italy, Poland, Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Packaging Type

| Rigid Plastic Packaging |

| Flexible Plastic Packaging |

| Industrial & Bulk Plastic Packaging |

By Material Type

| PET |

| Polyethylene (HDPE, LDPE, LLDPE) |

| Polypropylene |

| Polystyrene & EPS |

| PVC |

| Bioplastics & Bio-based Plastics |

| Recycled Plastics (rPET, rHDPE, rPP) |

By End-user Industry

| Food & Beverages |

| Personal Care & Cosmetics |

| Healthcare & Pharmaceuticals |

| Household & Industrial Chemicals |

| E-commerce & Retail Fulfilment |

| Automotive & Industrial Components |

Geography (Country Level)

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Poland |

| Sweden |

| Norway |

| Denmark |

| Finland |

| Belgium |

| Austria |

| By Packaging Type | Rigid Plastic Packaging |

| Flexible Plastic Packaging | |

| Industrial & Bulk Plastic Packaging | |

| By Material Type | PET |

| Polyethylene (HDPE, LDPE, LLDPE) | |

| Polypropylene | |

| Polystyrene & EPS | |

| PVC | |

| Bioplastics & Bio-based Plastics | |

| Recycled Plastics (rPET, rHDPE, rPP) | |

| By End-user Industry | Food & Beverages |

| Personal Care & Cosmetics | |

| Healthcare & Pharmaceuticals | |

| Household & Industrial Chemicals | |

| E-commerce & Retail Fulfilment | |

| Automotive & Industrial Components | |

| Geography (Country Level) | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Sweden | |

| Norway | |

| Denmark | |

| Finland | |

| Belgium | |

| Austria |

Key Questions Answered in the Report

How large is the European plastic packaging market in 2026?

The sector is valued at USD 73.73 billion in 2026 and is expected to reach USD 95.56 billion by 2031, growing at a 5.33% CAGR.

Which packaging type dominates demand?

Rigid formats lead with 51.35% share because of their suitability for dairy, pharma, and chemical products, although flexible formats are growing faster at a 5.18% CAGR.

Why is PET facing supply challenges despite high demand?

Food-grade rPET supply lags regulatory targets, commanding premiums and encouraging investments such as ALPLA’s expansion in Poland to bridge the gap.

What makes Poland the fastest-growing market in Europe?

Strong food-processing output and rising packaged-food retail sales, combined with foreign manufacturing investment, are driving a 6.65% CAGR.

Page last updated on: