Plastic Antioxidant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.69 Billion |

| Market Size (2031) | USD 7.33 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

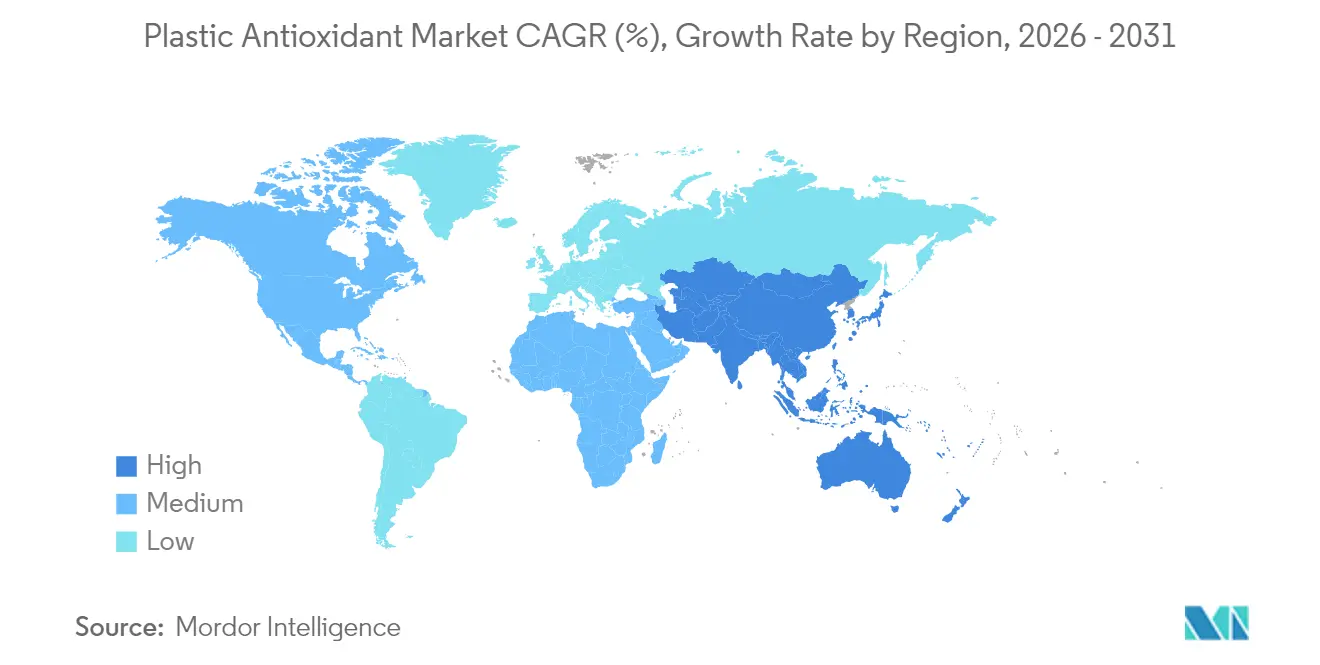

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Antioxidant Market Analysis by Mordor Intelligence

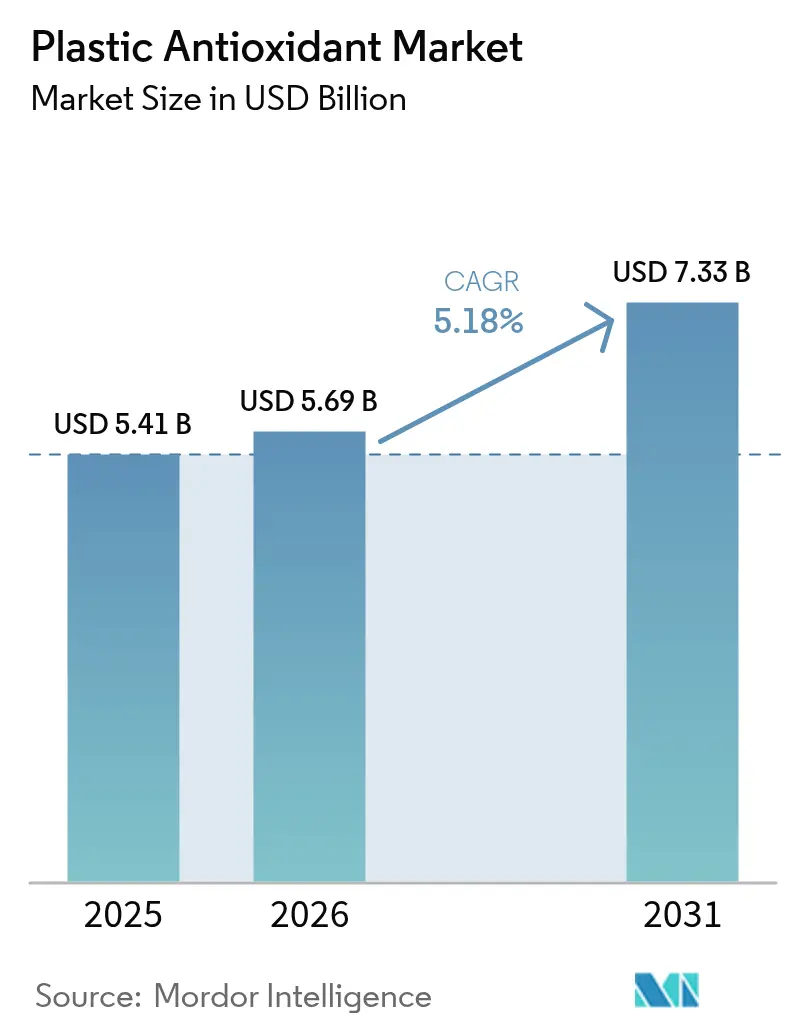

The Plastic Antioxidant Market size was valued at USD 5.41 billion in 2025 and estimated to grow from USD 5.69 billion in 2026 to reach USD 7.33 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031). Heightened demand for lightweight, durable polymers in automotive, packaging, construction and electronics is reinforcing reliance on advanced stabilization chemistry. Regulatory moves toward circular-economy targets are accelerating uptake of high-performance antioxidant blends that allow recycled resins to match virgin-grade performance. Integrated feedstock strategies, such as chemically recycled benzene supply agreements, are giving leading producers cost and sustainability advantages. Accelerating Asian production capacity, especially in China and India, is reshaping global supply chains, while North American and European end users prioritize additive systems cleared for stringent food-contact and medical standards. Short-term margin pressure from volatile phenol and phosphorus prices is encouraging backward integration, portfolio rationalization and the launch of nonylphenol-free grades.

Key Report Takeaways

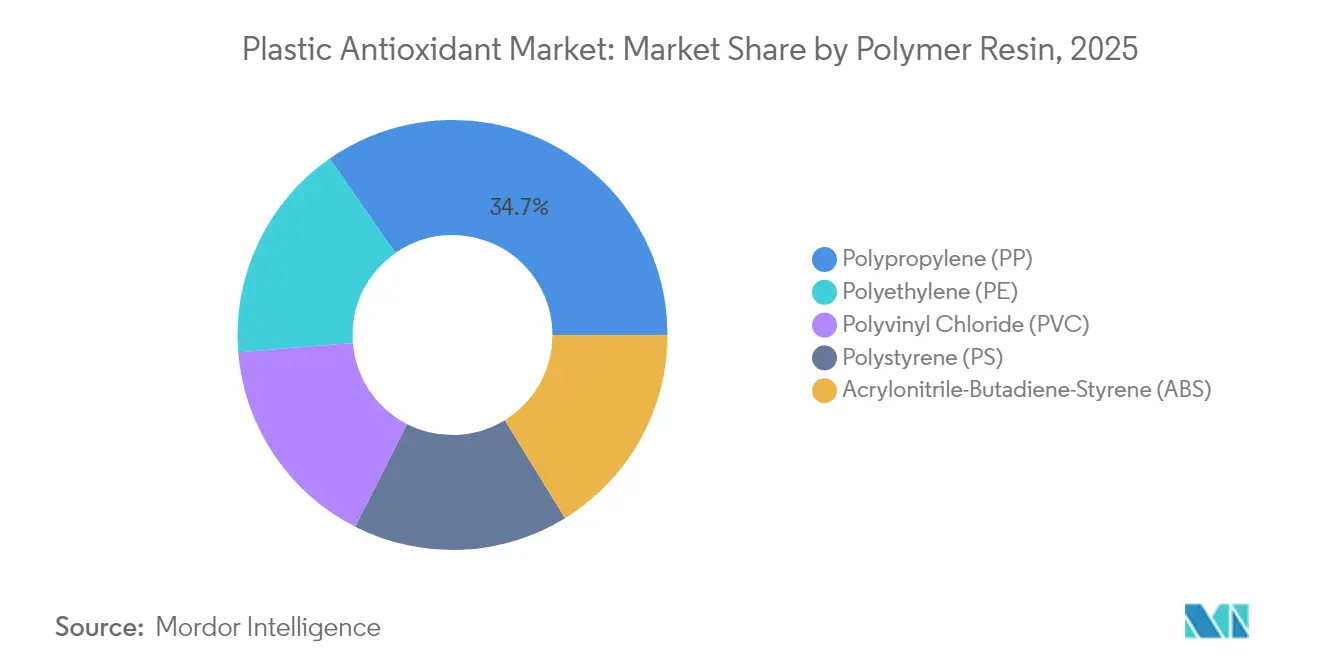

- By polymer resin, polypropylene led with 34.68% of plastic antioxidant market share in 2025; polyethylene is advancing at a 5.95% CAGR through 2031.

- By antioxidant type, phenolic additives captured 39.72% revenue share in 2025, while phosphite/phosphonite systems are projected to expand at a 6.18% CAGR to 2031.

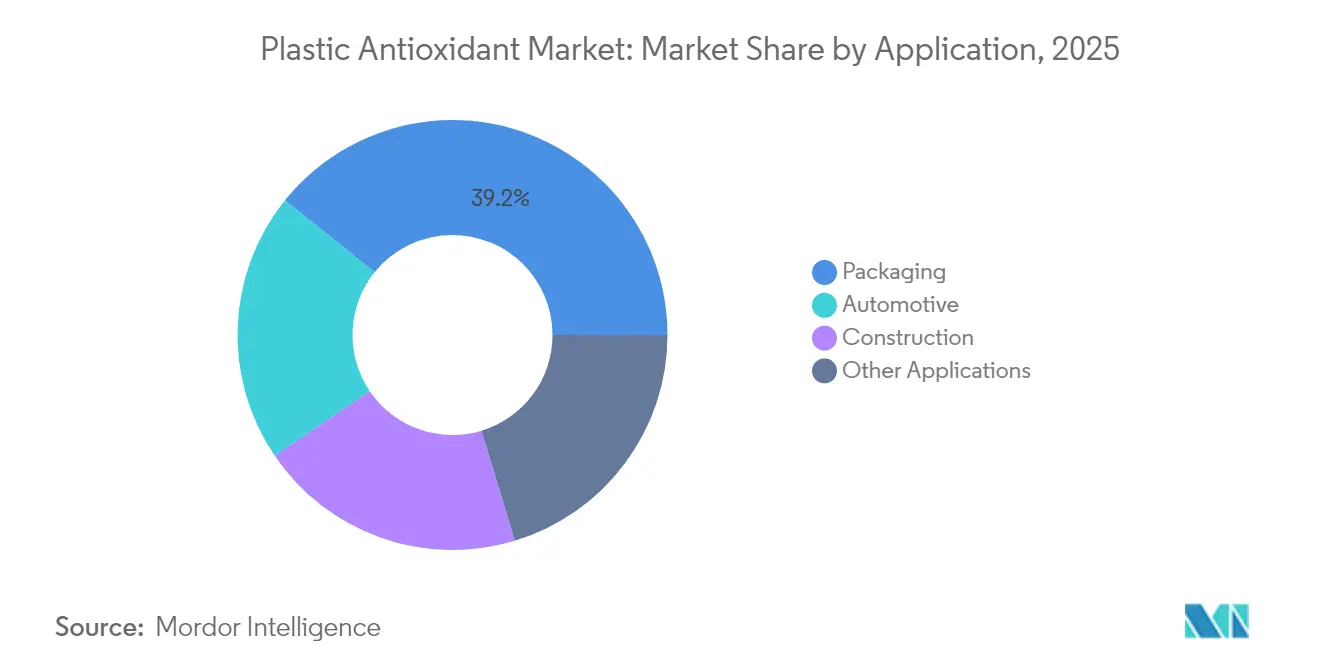

- By application, packaging accounted for 39.22% of the plastic antioxidant market size in 2025, whereas the automotive segment is set to grow at a 6.01% CAGR through 2031.

- By region, Asia-Pacific held 36.40% of 2025 revenue and is poised for the fastest growth at a 6.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plastic Antioxidant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replacement of conventional materials by metals with plastics | +1.8% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Rising polypropylene demand in automotive & rigid packaging | +1.5% | Global, concentrated in automotive hubs (Germany, Japan, China, USA) | Short term (≤ 2 years) |

| Growth of recycled polyolefins requiring high-performance stabilizers | +1.2% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Longer service-life requirements for 3D-printed polymer parts | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Surging photovoltaic back-sheet film capacity additions | +0.6% | Asia-Pacific dominant, with China leading installations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Replacement of Conventional Materials by Metals with Plastics

Automakers now incorporate plastic components that represent 15% of vehicle weight, demanding antioxidants that withstand continuous heat, UV radiation and mechanical stress[1]BASF SE, “Irganox® and Irgafos® Antioxidants,” basf.com. Sophisticated sterically hindered phenolic–phosphite blends have become customary for under-hood PP, delivering long-term thermal stability without compromising processing efficiency. Construction piping and insulation use similar systems to assure multi-decade service in aggressive outdoor environments. Rapid electric-vehicle adoption amplifies this trend because lighter parts lengthen driving range while facing higher operating temperatures. Consequently, integrated stabilizer packages tailored for metal-replacement grades are driving incremental demand throughout the plastic antioxidant market.

Rising Polypropylene Demand in Automotive & Rigid Packaging

Polypropylene components in engine compartments frequently face service temperatures above 120 °C, making tailored antioxidant packages indispensable. Dual systems combining Irganox 1010 with Irgafos 168 limit melt-flow decline during compounding and prolong part durability. Food-grade rigid packaging further tightens migration limits, encouraging nonylphenol-free phosphites that comply with evolving FDA and EU thresholds. The parallel push to incorporate recycled PP in bumper fascia and interior trim reinforces the need for restabilization, sustaining volume growth for value-added antioxidant solutions within the plastic antioxidant market.

Growth of Recycled Polyolefins Requiring High-Performance Stabilizers

Mechanical recycling exposes polymers to multiple heat histories that strip out legacy stabilizers and shorten molecular chains. Formulations such as BASF’s IrgaCycle restore viscosity and impact strength, enabling converters to place recyclate into higher-value packaging and consumer goods. Emerging European mandates for minimum recycled content magnify this requirement, lifting premium-grade antioxidant consumption. Suppliers able to couple processing-aid functionality with odor-neutralization are winning share among compounders pursuing closed-loop initiatives, further enlarging the plastic antioxidant market.

Longer Service-Life Requirements for 3D-Printed Polymer Parts

Laser-sintered polyamide powders experience prolonged exposure to 180 °C during build cycles, accelerating thermo-oxidative degradation. Incorporating hindered phenolic additives such as Irganox 1098 preserves mechanical integrity across multiple powder reuses, lowering material costs for service-grade prints. Medical device makers additionally explore biocompatible carrier systems that release antioxidants at controlled rates to arrest degradation in vivo. These developments broaden application breadth and underpin steady growth in the plastic antioxidant market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global & regional regulations on plastic additives | -1.4% | Europe leading, North America following, Asia-Pacific adapting | Medium term (2-4 years) |

| Toxicity & migration concerns prompting additive-free polymers | -0.9% | Global, with strongest impact in food contact applications | Long term (≥ 4 years) |

| Volatile phosphorus & phenol feedstock prices | -0.7% | Global, with Asia-Pacific most affected by supply disruptions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Global & Regional Regulations on Plastic Additives

The EU has proposed classifying TNPP as an SVHC, compelling formulators to eliminate nonylphenol moieties and redesign portfolios. Clariant’s PFAS-free antioxidant line exemplifies proactive compliance, but smaller suppliers face disproportionate testing costs. Divergent regional thresholds for migration into food pose additional burdens, prompting multinational converters to demand globally cleared antioxidant grades. Compliance complexity encourages consolidation, raising entry barriers yet tempering growth for the plastic antioxidant market.

Toxicity & Migration Concerns Prompting Additive-Free Polymers

Analytical studies reveal inner plastic packaging can contain 24 mg/kg of synthetic antioxidants that partially migrate into foods. Reactive stabilization chemistries, where antioxidant fragments are grafted onto polymer chains, are gaining traction because they curb leaching while sustaining protection. Brands in cosmetics and pharmaceuticals increasingly specify low-migration polyolefins, nudging research toward bio-based or covalently bound alternatives. These shifts could reduce volume growth but simultaneously open higher-margin niches in the plastic antioxidant industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Resin: Polypropylene Dominance Drives Thermal Stability Innovation

Polypropylene controlled a 34.68% plastic antioxidant market share in 2025, reflecting its central role in lightweight automotive and rigid-food packaging applications. Its high-temperature processing profile necessitates antioxidant packages that limit melt-flow decline and maintain color. Polyethylene is expanding at a 5.95% CAGR, supported by booming flexible packaging and the push to include recycled content. Novel PP compounds incorporating phenolic–phosphite blends now achieve endurance thresholds once reserved for engineering resins, cementing PP’s leadership within the plastic antioxidant market.

Demand for PVC in pipe, cable and geomembrane requires antioxidants that delay dehydrochlorination and maintain toughness over decades, particularly under pressure cycling and temperature extremes. PS and ABS benefit from primary–secondary antioxidant combinations that arrest thermal-oxidative chain scission during injection molding. Research into bio-derived stabilizers such as phenyl propionates suggests longer-term potential to reduce fossil-based ingredients, hinting at future differentiation across resin families within the plastic antioxidant market.

By Antioxidant Type: Synergistic Combinations Enhance Protection Efficacy

Phenolic additives delivered 39.72% revenue in 2025 by virtue of their free-radical scavenging efficiency. Secondary phosphite and phosphonite antioxidants are projected to outpace the base market at a 6.18% CAGR through 2031. Food-contact clearances for nonylphenol-free grades such as WESTON 705 and 705 T are accelerating migration-sensitive applications. Custom blends tuned to resin type, processing temperature and residence time are increasingly specified in supply contracts, stabilizing demand for multipurpose formulations across the plastic antioxidant market.

Advances in organophosphite chemistry focus on higher hydrolytic stability and lower color contribution, enabling processors to reduce loading yet sustain performance. Such efficiency gains cut additive costs per kilogram of compound and lower extractables, making phosphites central to premium packaging, wire and cable compounds, and e-mobility parts. Blends with hindered amines or UV absorbers provide total protection packages, allowing suppliers to upsell turnkey stabilizer systems rather than single molecules.

By Application: Packaging Leadership Drives Food Safety Innovation

Packaging secured 39.22% of 2025 sales as converters rely on antioxidants to extend shelf life, maintain clarity and prevent taste transfer. Recycled-content mandates are prompting line extensions that restore mechanical strength and optics in rPET and rPE films without exceeding migration limits. Meanwhile, the automotive segment’s 6.01% CAGR through 2031 stems from electric-vehicle adoption, which raises operating temperatures and heightens the need for durable polymers.

Construction remains a steady volume outlet because underground piping, insulation and geomembranes must resist oxidation during prolonged exposure to moisture and soil chemicals. Electronics and medical devices, though smaller, command premium antioxidant grades certified for biocompatibility or low ionic contamination. 3D printing represents an emerging application in which feedstocks loaded with antioxidants secure repeat powder reuse without compromising mechanical integrity, adding incremental volume to the plastic antioxidant market.

Geography Analysis

Asia-Pacific captured 36.40% revenue in 2025 and is advancing at a 6.08% CAGR to 2031, underpinned by expanding petrochemical hubs and surging local consumption in automotive and packaging. BASF and Evonik have both expanded Nanjing operations to shorten lead times and embed technical service close to customers. Regional OEMs appreciate on-the-ground formulation support that helps navigate shifting Chinese GB standards and India’s BIS approvals. Growing middle-class demand for packaged foods and appliances further lifts local antioxidant consumption, ensuring Asia-Pacific remains the keystone of the plastic antioxidant market.

North America exhibits mature but resilient growth as stringent FDA food-contact regulations drive continuous reformulation of additives with superior toxicological profiles. Strong recycling initiatives encourage uptake of restabilization packages designed to raise recycled resin content in personal-care and household products. BASF’s long-term benzene feedstock deal with Encina illustrates strategic moves to secure low-carbon raw materials for antioxidant production. Rapid electric-vehicle assembly in the USA and Canada requires antioxidants capable of enduring thermal and electrical loads, supporting premium-grade demand.

Europe’s trajectory hinges on environmental policy leadership. REACH and the Single-Use Plastics Directive stimulate development of PFAS-free and low-migration antioxidant grades, lifting R&D intensity and driving differentiation in the plastic antioxidant market. Mandatory recycled-content thresholds in packaging accelerate adoption of high-performance stabilizers suited for contaminated feedstreams. Germany, France and Italy remain core demand centers owing to advanced automotive and food-processing sectors, while Eastern Europe grows as manufacturing relocates eastward. Nordic nations and Benelux promote bio-based stabilizers via green-public-procurement schemes, creating early-stage niches for innovative suppliers.

Competitive Landscape

Global supply remains moderately fragmented. BASF, Clariant and Evonik anchor the tier-one group through backward-integrated raw material positions, multi-continent plants and application labs that customize formulations per customer and regulatory regime. Their portfolio depth, including phenolics, phosphites, thioesters and HALS, enables bundled sales, reinforcing customer stickiness in the plastic antioxidant market. Sustainability credentials, from mass-balance attribution to life-cycle-assessment data, serve as key differentiators in tender processes for multinational brand owners.

Medium-sized specialists such as SI Group and Addivant concentrate on niche high-purity stabilizers approved for medical and infant-care applications, competing through rapid regulatory filings and tailored blends. Asian challengers, led by Songwon and Dover Chemical’s Chinese joint ventures, leverage cost-effective manufacturing and rising domestic demand to chip away at incumbent shares, particularly in commodity phenolics. Intellectual-property disputes around novel phosphite synthesis methods underscore the strategic value of process know-how.

Plastic Antioxidant Industry Leaders

Clariant

BASF

ADEKA Corporation

SI Group Inc.

Songwon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: SI Group announced that the U.S. Food & Drug Administration (FDA) has granted Food Contact Notification (FCN) 2326 for its phosphite antioxidants, WESTON 705 and WESTON 705T. This FCN expands the permissible use of these phosphite antioxidants to include polyethylene terephthalate (PET) polymers.

- December 2023: BASF introduced Irgastab PUR 71, an advanced antioxidant engineered to enhance regulatory compliance and improve performance in polyols and polyurethane foams. This launch underscores BASF's commitment to innovation in the chemical industry.

Global Plastic Antioxidant Market Report Scope

The plastic antioxidant market report includes:

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyvinyl Chloride (PVC) |

| Polystyrene (PS) |

| Acrylonitrile-Butadiene-Styrene (ABS) |

| Phenolic Antioxidants |

| Phosphite and Phosphonite Antioxidants |

| Antioxidant Blends |

| Packaging |

| Construction |

| Automotive |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Polymer Resin | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Polyvinyl Chloride (PVC) | ||

| Polystyrene (PS) | ||

| Acrylonitrile-Butadiene-Styrene (ABS) | ||

| By Antioxidant Type | Phenolic Antioxidants | |

| Phosphite and Phosphonite Antioxidants | ||

| Antioxidant Blends | ||

| By Application | Packaging | |

| Construction | ||

| Automotive | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Why is Asia-Pacific the largest regional market for plastic antioxidants?

Asia-Pacific combines expansive polymer manufacturing capacity with fast-growing automotive and packaging consumption, resulting in a 36.40% revenue share in 2025 and the fastest 6.08% CAGR outlook to 2031.

Which polymer drives the majority of antioxidant demand?

Polypropylene accounts for 34.68% of 2025 demand thanks to its broad use in automotive and rigid packaging that require robust thermal-oxidative stability.

How are regulations influencing antioxidant development?

EU REACH, FDA food-contact rules and national bans on nonylphenol derivatives are accelerating non-toxic, low-migration and PFAS-free antioxidant chemistries.

Which antioxidant types are growing fastest?

Phosphite and phosphonite secondary antioxidants are forecast at a 6.18% CAGR to 2031 because they synergize with phenolics to protect polymers during high-temperature processing.

Page last updated on: