Low Profile Additives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

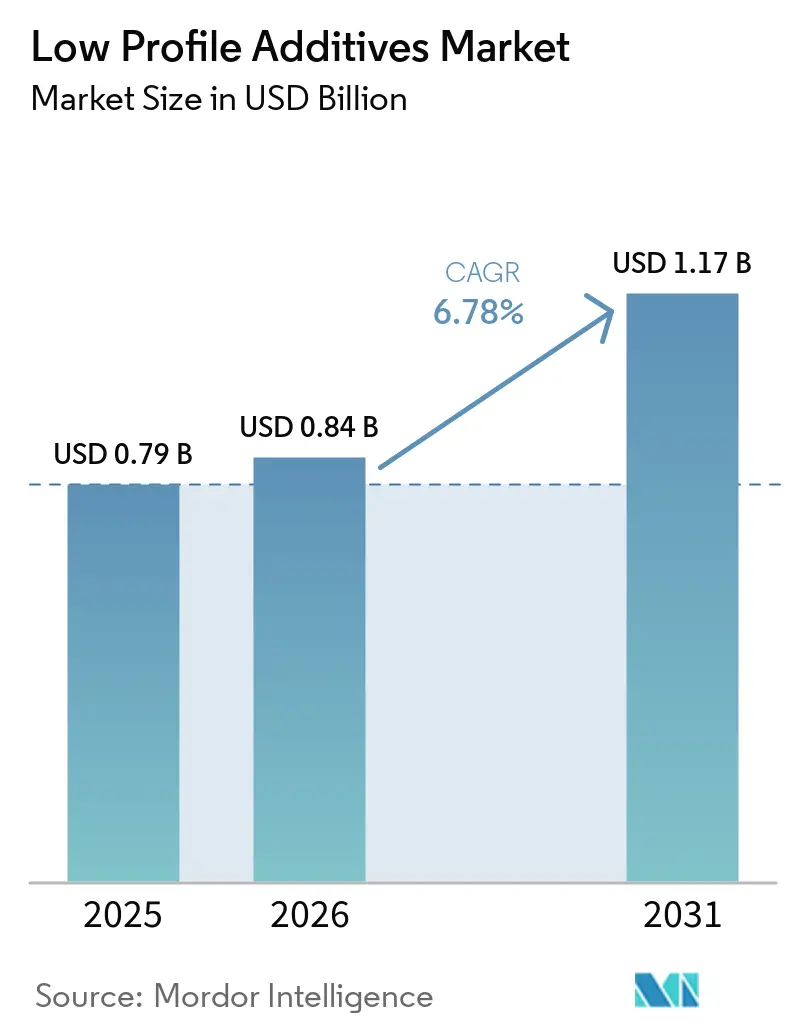

| Market Size (2026) | USD 0.84 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Low Profile Additives Market Analysis by Mordor Intelligence

Low Profile Additives Market size in 2026 is estimated at USD 0.84 billion, growing from 2025 value of USD 0.79 billion with 2031 projections showing USD 1.17 billion, growing at 6.78% CAGR over 2026-2031. Rising demand for high-performance composites in electric vehicles, construction reinforcements, and precision industrial parts is sustaining this growth trajectory. Automakers are adopting low profile additives to control shrinkage in Sheet Molding Compound (SMC) and Bulk Molding Compound (BMC) components, ensuring Class A surface quality. Parallel momentum stems from infrastructure projects that replace steel rebar with fiber-reinforced plastics, while bio-based chemistries are gaining policy support. Competitive intensity is moderate yet rising as suppliers race to integrate renewable feedstocks and differentiate on compoundability and surface aesthetics.

Key Report Takeaways

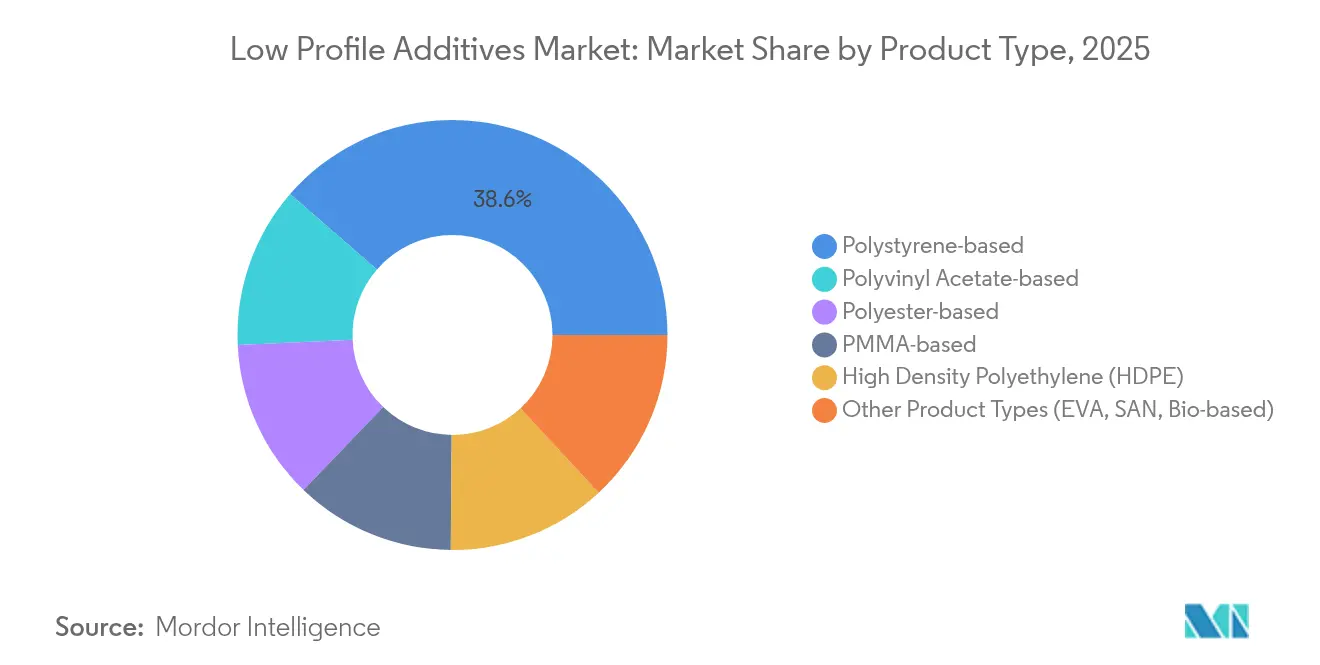

- By product type, polystyrene-based grades led with 38.62% low profile additives market share in 2025; bio-based “Other” grades are forecast to expand at 8.74% CAGR through 2031.

- By application, injection and compression molding accounted for 54.38% of the low profile additives market size in 2025 and are advancing at 8.15% CAGR to 2031.

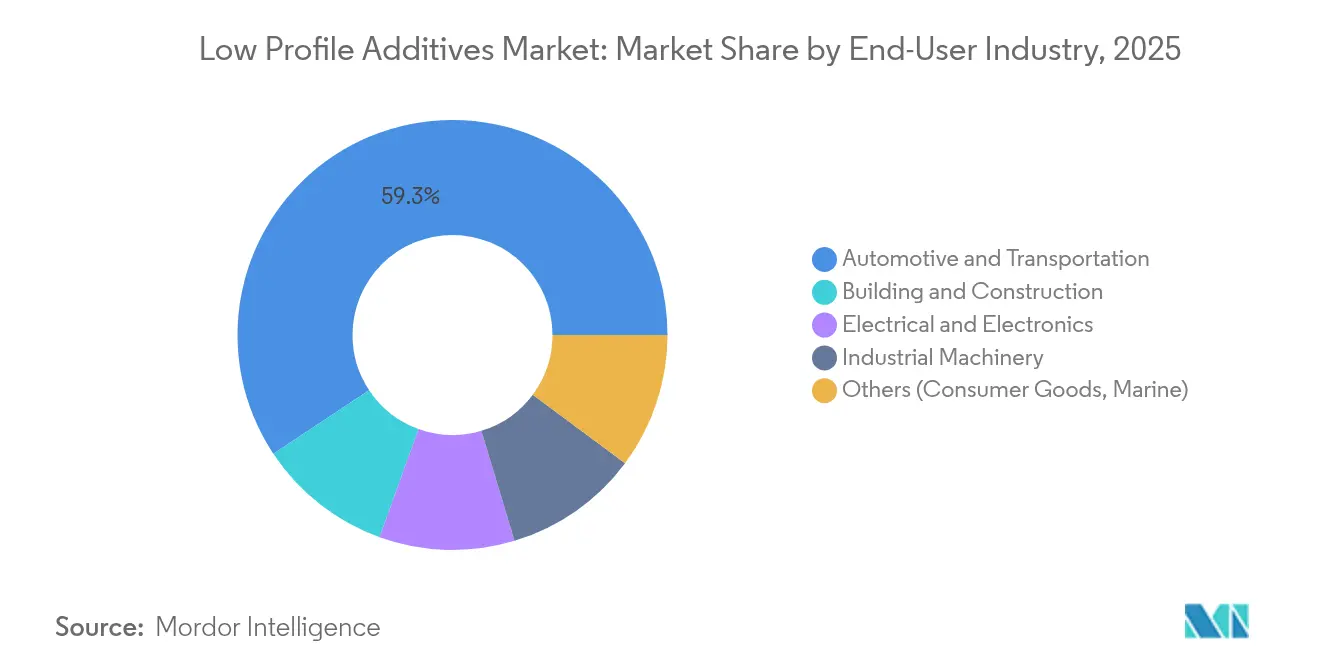

- By end-user industry, automotive and transportation commanded 59.32% revenue share of the low profile additives market in 2025 and is set to progress at 8.42% CAGR through 2031.

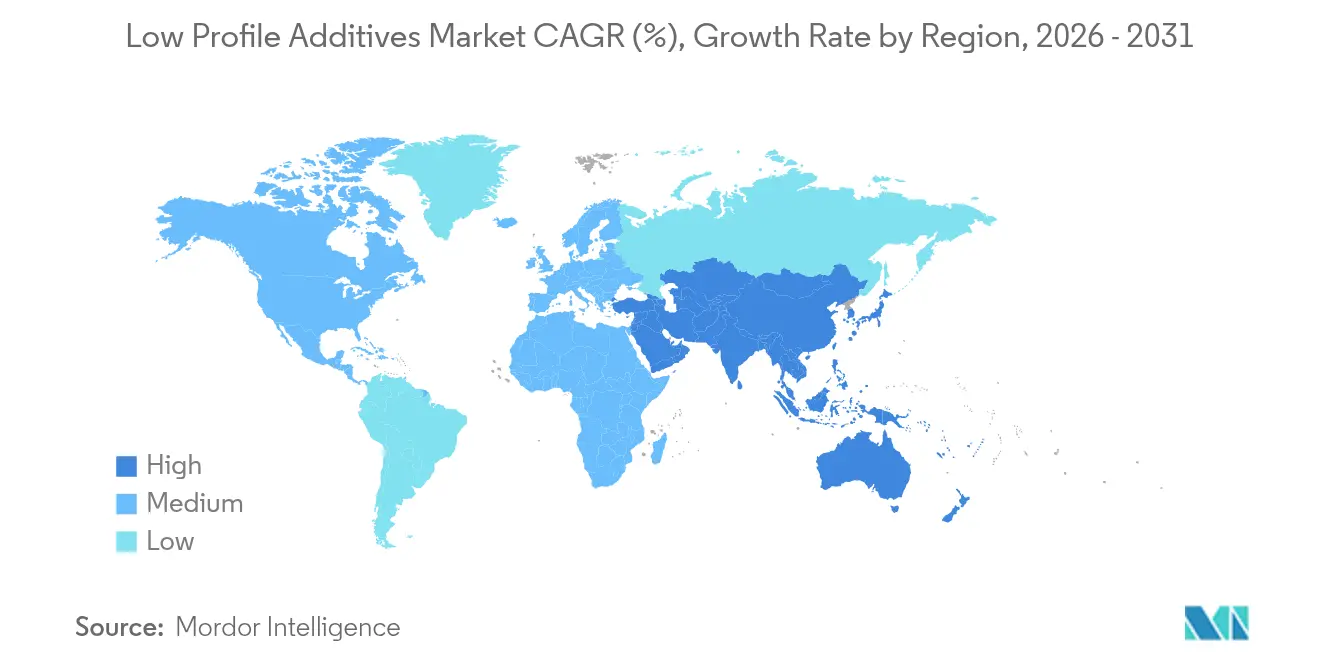

- By region, Asia-Pacific dominated with 44.12% share of the low profile additives market in 2025, while posting 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Low Profile Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Demand for High-performance SMC Formulations from Automotive Industry | +1.5% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Accelerated EV Lightweighting Mandates | +1.8% | Global, led by Europe and China | Short term (≤ 2 years) |

| Replacement of Steel Rebar with Fiber-reinforced Plastics | +1.2% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Emerging Applications in Fiber-reinforced Plastics (FRP) | +0.9% | Global, with early adoption in wind energy and infrastructure | Medium term (2-4 years) |

| Growing Emphasis on Bio-based LPAs from Lignin & Castor Oil | +0.6% | Europe and North America, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increase in Demand for High-performance SMC Formulations from Automotive Industry

Automakers are scaling SMC to mold battery enclosures, body panels, and structural inserts that need flawless Class A finishes. Low profile additives limit volumetric shrinkage, securing dimensional stability under thermal cycling. Dow’s polyurethane-carbon fiber spar cap demonstrates cure efficiencies exceeding 90%, exemplifying how next-generation additives support high-speed presses. Larger vehicle platforms and thick-section parts further raise shrinkage control requirements, making advanced low profile additives indispensable across Asia-Pacific’s fast-growing electric vehicle hubs.

Accelerated EV Lightweighting Mandates

The European Union’s CO₂ rules and China’s New Energy Vehicle quotas spur rapid fiber-reinforced plastic adoption. Low profile additives underpin these composites by preventing sink marks and waviness even in multi-material assemblies. University of Virginia research shows weight savings of 31% in graphene-modified cement composites, a proxy for similar mass-reduction prospects in auto structures. Rising battery range expectations will continue to pull lightweight composites, sustaining additive demand.

Replacement of Steel Rebar with Fiber-reinforced Plastics

Infrastructure owners are shifting to FRP rebar for corrosion-free service life. Röchling’s Durostone launch illustrates pultruded bars where low profile additives guarantee consistent surface topology during continuous processing[1]"Fiberline supplies carbon profiles for wind turbines,” CompositesWorld, compositesworld.com . Marine piers and coastal bridges benefit most, given saltwater exposure. As building codes update, civil contractors specify FRP more frequently, solidifying long-term additive uptake.

Growing Emphasis on Bio-based LPAs from Lignin & Castor Oil

Policy incentives in Europe and North America encourage renewable feedstocks. Evonik’s lignin-derived specialties and BASF’s biomass balance pathway show petroleum substitution without performance loss[2]“Biomass-balance route for EPS,” BASF, basf.com. OEMs value lower carbon footprints, driving exploratory trials of bio-based low profile additives despite scaling challenges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Polymerization Shrinkage of Unsaturated Polyester Resin with Crosslinking Styrene Monomer | -0.8% | Global, particularly affecting high-volume applications | Short term (≤ 2 years) |

| Competition from Thermoplastic Composites | -0.7% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Limited Repairability of Thermoset Parts | -0.5% | Global, with stronger impact in Europe due to circular economy regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Polymerization Shrinkage of Unsaturated Polyester Resin with Crosslinking Styrene Monomer

UPR-styrene systems inherently contract during cure, generating voids and print-through that low profile additives must counteract. Suppliers experiment with reactive diluents and modified crosslinkers to curb shrinkage, but such tweaks add cost and cycle-time complexity. Automotive Class A finishes set a high bar, pressuring formulators to keep innovating even in fast-moving, high-volume lines.

Competition from Thermoplastic Composites

Recyclable thermoplastic composites are gaining favor in bumper beams and battery trays where end-of-life regulations matter more than surface gloss. Covestro’s polyurethane infusion resins shorten cycle times and challenge traditional thermosets in wind blades. As automakers pursue circularity targets, thermoplastics may siphon volumes from the low profile additives industry unless suppliers pivot toward circular thermoset systems

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polystyrene Dominance Faces Bio-based Challenge

Polystyrene-based grades retained 38.62% low profile additives market share in 2025 through proven cost-performance balance in automotive SMC. The low profile additives market size for “Other” product types-largely bio-based-should rise swiftly, expanding at 8.74% CAGR to 2031 as OEMs chase carbon reduction credits.

Polyvinyl acetate and PMMA variants occupy niches that demand impact strength or optical clarity, while high-density polyethylene grades suit budget-sensitive parts. Polyester-based offerings, both pure and PU-modified, tackle corrosive or high-temperature environments. BASF’s biomass-balance EPS underscores how incumbent suppliers blend sustainability with incumbent processes.

By Application: Injection Molding Leads Across All Metrics

Injection and compression molding contributed 54.38% of the low profile additives market size in 2025, propelled by automotive exterior panels and consumer appliances. This application bracket is also charting the fastest 8.15% CAGR as electric vehicle platforms multiply.

Pultrusion is flourishing in FRP rebar and wind energy spar caps, evidenced by Fiberline’s multiyear contract wins. Resin transfer molding covers aerospace control surfaces where void-free consolidation and tight tolerances matter. Dow’s rapid-cure polyurethane systems exemplify cross-application versatility.

By End-User Industry: Automotive Supremacy Accelerates

Automotive and transportation absorbed 59.32% of 2025 revenue and will maintain the lead with 8.42% CAGR, cementing the low profile additives market as a direct beneficiary of electrification. Class A fascia, battery lids, and under-body shields rely on shrinkage-free SMC.

Building and construction follow, driven by FRP rebar adoption in corrosive structures. Growing investments in the Steel Rebar market and corrosion-resistant reinforcement materials are further increasing the demand for advanced low profile additive solutions. Electrical and electronics count on additives that moderate coefficient of thermal expansion and deliver low-dielectric properties, as shown by NSG’s glass flakes. Industrial machinery, marine, and consumer goods together contribute steady incremental demand.

Geography Analysis

Asia-Pacific dominated the low profile additives market with 44.12% share in 2025 and an 7.55% CAGR outlook to 2031. China’s electric vehicle surge and state-backed infrastructure rollouts underpin composite adoption, while local suppliers scale thermoset capacity. India’s automotive expansion and South Korea’s electronics exports add tailwinds. BASF’s Nanjing site enlargement underscores strategic focus on regional production.

North America ranked second, buoyed by EV platform launches, aerospace rebuilds, and wind-repowering campaigns. The United States houses advanced resin labs and pultrusion lines, while Mexico’s proximity to OEM plants fuels part localization. Dow’s wind-blade resin programs highlight regional technical prowess.

Europe follows, characterized by strict sustainability requirements that hasten bio-based low profile additives uptake. Germany’s premium auto brands adopt composites for body-in-white elements, and Nordic nations channel renewables investments into large turbine blades. Evonik’s lignin programs and BYK’s VOC-free surfactants typify the innovation thrust.

Competitive Landscape

The low profile additives market features a moderate concentration where the top five suppliers hold roughly 45% revenue. Global majors—ALTANA, Evonik, Arkema—leverage integrated resin portfolios, technical service labs, and distribution breadth to anchor key accounts. Mid-sized specialists such as AOC, Ashland, and Composites One focus on region-specific or application-specific chemistries.

M&A is reshaping the field: Nippon Paint Holdings’ USD 2.3 billion purchase of AOC positions the paint conglomerate to cross-sell composite resins throughout its customer network. Technology is a prime battleground; BYK’s silicone-free defoamers and rheology aids widen its automotive credentials. Suppliers able to industrialize bio-based or recyclable thermoset systems will gain first-mover pricing power as OEMs formalize Scope 3 targets.

Low Profile Additives Industry Leaders

-

Polynt S.p.A

-

Arkema

-

Ashland

-

Poliya

-

AOC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Clariant introduced AddWorks PPA, a PFAS-free processing aid aimed at improving the efficiency of polyolefin film extrusion while addressing sharkskin defects. This innovation aligns with the industry's growing demand for sustainable and high-performance solutions.

- July 2023: INEOS consolidated its North American composites headquarters in Columbus, Ohio, integrating its low profile additives R&D and commercial teams. This strategic move is expected to enhance collaboration and streamline operations within the region.

Global Low Profile Additives Market Report Scope

The scope of the low profile additives market report includes:

| Polystyrene-based | |

| Polyvinyl Acetate-based | |

| PMMA-based | |

| High Density Polyethylene (HDPE) | |

| Polyester-based | Pure Saturated Polyester |

| PU-modified Saturated Polyester | |

| Other Product Types (EVA, SAN, Bio-based) |

| Injection and Compression Molding (SMC/BMC) |

| Pultrusion |

| Resin Transfer Molding (RTM) |

| Hand Lay-Up |

| Spray-Up |

| Automotive and Transportation |

| Building and Construction |

| Electrical and Electronics |

| Industrial Machinery |

| Others (Consumer Goods, Marine) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Polystyrene-based | |

| Polyvinyl Acetate-based | ||

| PMMA-based | ||

| High Density Polyethylene (HDPE) | ||

| Polyester-based | Pure Saturated Polyester | |

| PU-modified Saturated Polyester | ||

| Other Product Types (EVA, SAN, Bio-based) | ||

| By Application | Injection and Compression Molding (SMC/BMC) | |

| Pultrusion | ||

| Resin Transfer Molding (RTM) | ||

| Hand Lay-Up | ||

| Spray-Up | ||

| By End-User Industry | Automotive and Transportation | |

| Building and Construction | ||

| Electrical and Electronics | ||

| Industrial Machinery | ||

| Others (Consumer Goods, Marine) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Low Profile Additives Market size?

The low profile additives market is valued at USD 0.84 billion in 2026 and is forecast to expand at a 6.78% CAGR between 2026 and 2031.

Which application segment leads demand for low profile additives?

Injection and compression molding hold 54.38% market share and show the fastest 8.15% CAGR through 2031.

Why are bio-based low profile additives gaining traction?

Policy incentives and OEM carbon-reduction targets drive interest in lignin- and castor-oil-derived chemistries that match performance while lowering environmental impact.

Which region dominates the low profile additives market?

Asia-Pacific leads with 44.12% share in 2025, supported by China’s electric vehicle production and infrastructure spending.

Page last updated on: