PLA Barrier Coated Beverage Board Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

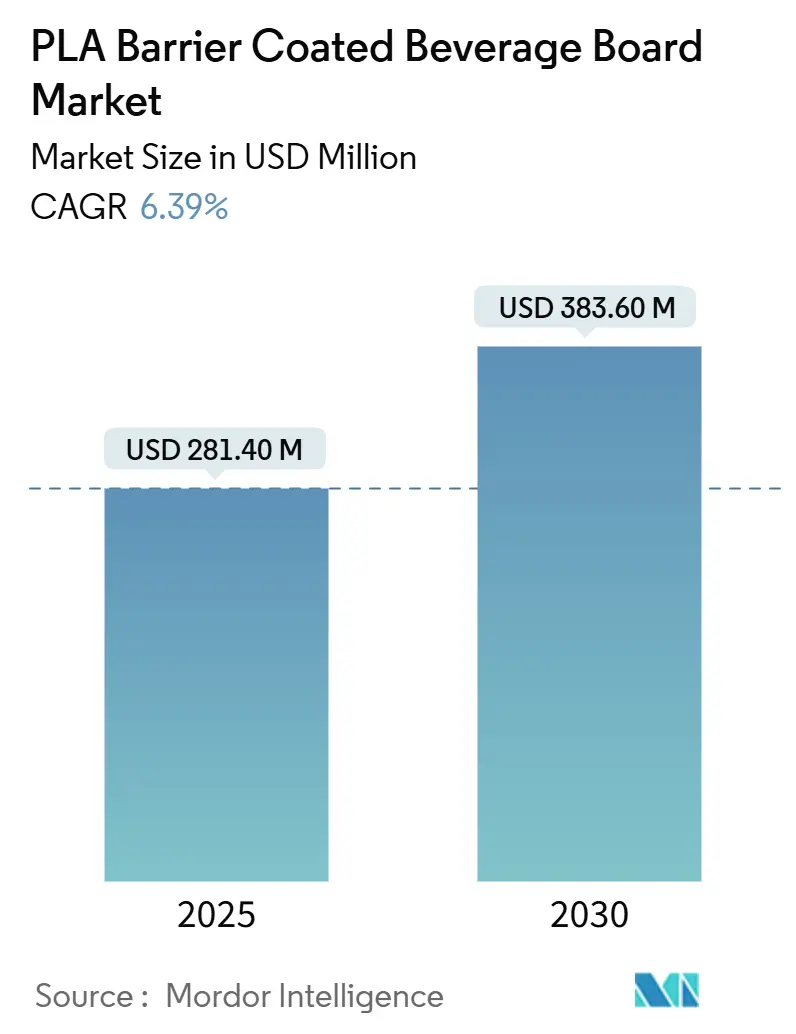

| Market Size (2025) | USD 281.40 Million |

| Market Size (2030) | USD 383.60 Million |

| Growth Rate (2025 - 2030) | 6.39% CAGR |

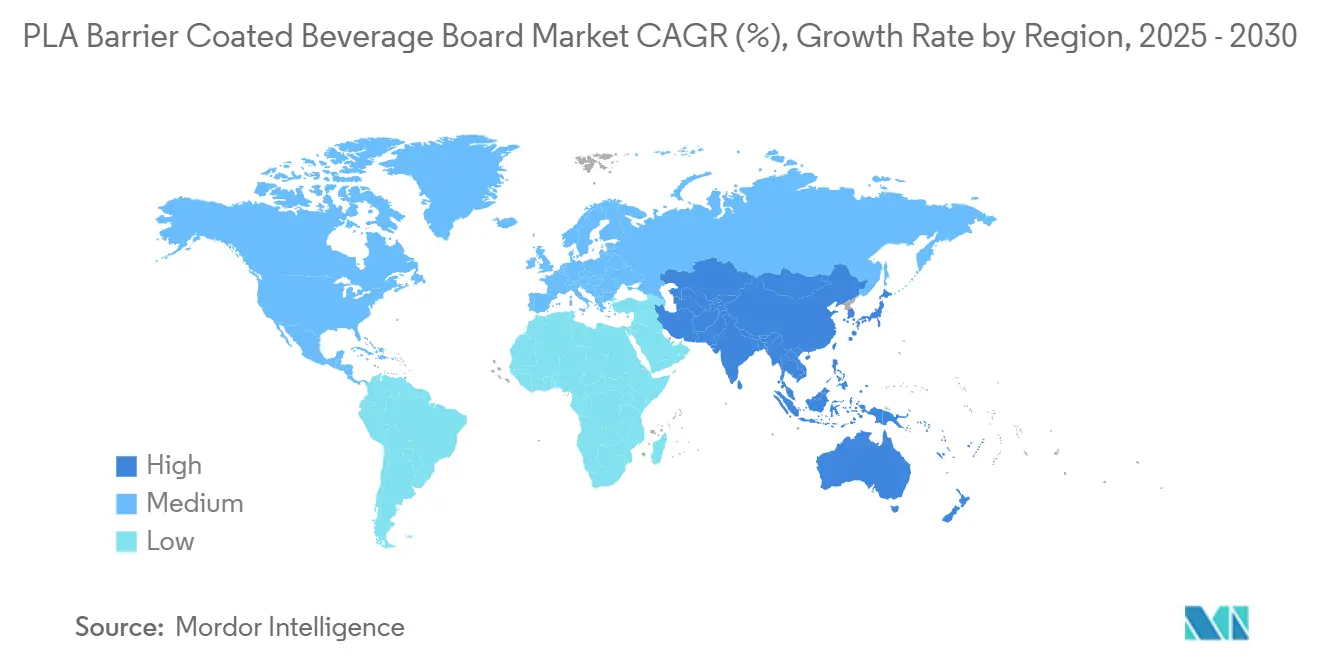

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PLA Barrier Coated Beverage Board Market Analysis by Mordor Intelligence

The PLA barrier coated beverage board market size is USD 281.4 million in 2025 and is projected to reach USD 383.6 million by 2030, reflecting a 6.39% CAGR EUROPA.EU. Robust growth stems from regulatory restrictions on bisphenol A and polyethylene liners, brand-owner sustainability mandates, and evidence that polylactic acid (PLA) disintegrates faster than organic waste in commercial composters. Industrial composting capacity is expanding alongside PLA supply investments, while technical advances in nanocellulose-PLA multilayers have cut oxygen transmission by 98% . Europe currently leads adoption, but capacity additions in Thailand and China will shift production economics during the forecast period. Competition centers on integrated mills that can scale cost-effective coating lines and secure lactic-acid feedstocks.

Key Report Takeaways

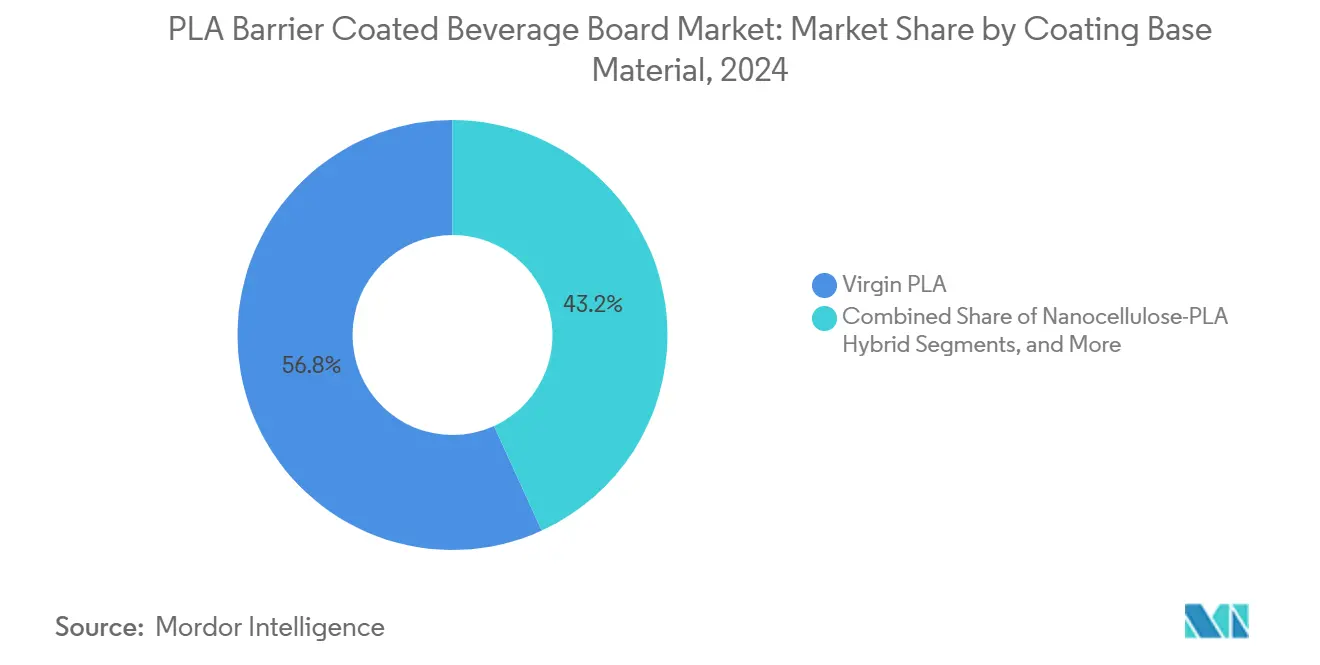

- By coating base material, virgin PLA led with 56.82% of PLA barrier coated beverage board market share in 2024.

- By packaging format, paper cups commanded 61.64% of the PLA barrier coated beverage board market size in 2024.

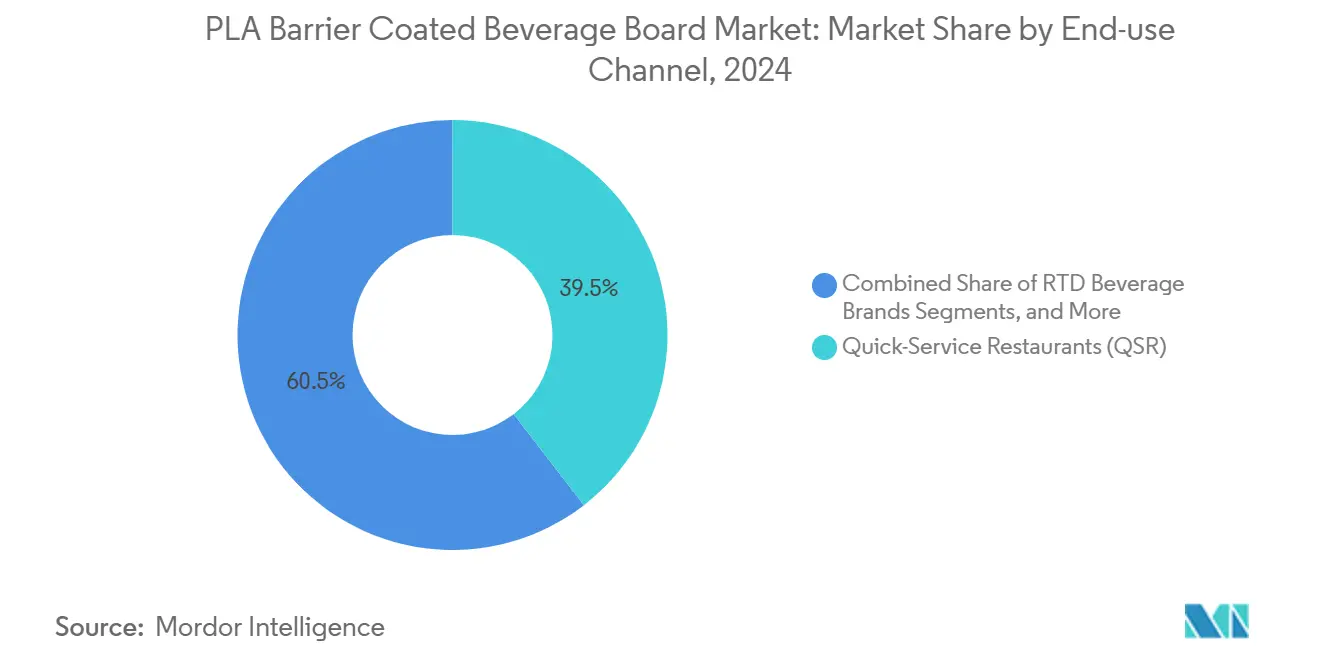

- By end-use channel, the PLA barrier coated beverage board for ready-to-drink beverage brands is projected to grow at a 5.93% CAGR between 2025-2030.

- By geography, the PLA barrier coated beverage board for Asia-Pacific region is projected to grow at a 7.64% CAGR between 2025-2030.

Global PLA Barrier Coated Beverage Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for compostable single-use beverage packaging | +1.2% | Global with early adoption in North America and EU | Medium term (2-4 years) |

| Regulatory bans on polyethylene-lined cups in key regions | +1.8% | Europe and North America core, expanding to APAC | Short term (≤ 2 years) |

| Brand-owner sustainability commitments and fiber-switch targets | +1.1% | Global led by multinational QSR and beverage brands | Medium term (2-4 years) |

| Technical advances in high-speed PLA extrusion coating lines | +0.9% | Manufacturing hubs in APAC, technology transfer to EU/NA | Long term (≥ 4 years) |

| Premiumization of RTD functional drinks requiring high-clarity barriers | +0.7% | North America and Europe, emerging in urban APAC | Medium term (2-4 years) |

| Brewery shift to hot-fill fiber beer cups for CO₂ reduction | +0.4% | Europe and North America craft brewing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Compostable Single-Use Beverage Packaging

Growing awareness of microplastics has accelerated preference for packaging that truly biodegrades. Meta-analysis of more than 30,000 studies confirms that PLA hydrolyzes without leaving persistent fragments, unlike petroleum plastics. Mandatory EU recycling targets of 65% by 2025 and 70% by 2030 amplify municipal pressure to divert organic waste streams. Urban consumers now accept price premiums for certified compostable cups as disposal fees feed directly into local budgets. This behavioral change meshes with expanding curbside organics collection, sustaining demand for PLA barrier coated beverage board market solutions.

Regulatory Bans on Polyethylene-Lined Cups in Key Regions

The EU ban on bisphenol A in food-contact articles, effective January 2025, removes a mainstream barrier technology and accelerates PLA adoption. China, Japan, and Australia have enacted or drafted food-contact and recyclability rules that impose substance restrictions and recyclability obligations. These frameworks convert temporary compliance programs into structural market shifts. As regional regulators align, the PLA barrier coated beverage board market gains durable momentum over polyethylene incumbents.

Brand-Owner Sustainability Commitments and Fiber-Switch Targets

Beverage and QSR multinationals now link executive compensation to packaging metrics. Carlsberg targets fully renewable or recyclable packs and a 50% cut in virgin fossil plastic. Ball Corporation plans 85% recycled content by 2030. Procurement specifications therefore favor bio-based coatings. The PLA barrier coated beverage board market benefits because suppliers that meet fiber-switch targets gain access to multi-year offtake contracts.

Technical Advances in High-Speed PLA Extrusion Coating Lines

Process innovation has narrowed the operating-cost gap with polyethylene. Continuous multilayer extrusion delivers nanocellulose-PLA coatings that match commercial line speeds while cutting oxygen ingress almost completely. Heat-treatment lifts PLA crystallinity to 42% within 15 minutes at 100 °C, making hot-fill fiber cups feasible. NatureWorks’ USD 350 million Thai plant will supply 75,000 tons annually from 2025, easing raw material bottlenecks

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production cost of PLA coatings versus PE | -1.4% | Global manufacturing, acute in price-sensitive markets | Short term (≤ 2 years) |

| Limited industrial composting infrastructure | -0.8% | North America and developing APAC regions | Medium term (2-4 years) |

| Supply volatility of lactic-acid feedstock post-pandemic | -0.6% | Global supply chains, concentrated in agricultural regions | Medium term (2-4 years) |

| Heat-resistance limits restricting microwaveable applications | -0.5% | Consumer convenience applications globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Production Cost of PLA Coatings Versus PE

Even after energy-efficient evaporation steps trim costs by 90%, PLA still carries a premium over polyethylene. Capital spending for high-temperature screws and corrosion-resistant barrels raises converter entry barriers. Corbion reports industry-wide capacity utilization near 55%, so fixed costs spread over fewer tons maintain price differentials. Unless mandates remove PE from the market, near-term margin pressure persists for the PLA barrier coated beverage board market.

Limited Industrial Composting Infrastructure

Certification alone does not guarantee proper disposal. Industrial composting sites remain patchy outside Western Europe. Studies by North American environmental agencies show many PLA-lined cups still head to landfill because haulers lack PLA-ready facilities. Australia’s regulators note similar gaps in collection and consumer education. Infrastructure misalignment undermines the environmental value proposition that underpins premium pricing in the PLA barrier coated beverage board industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Base Material: Virgin PLA Dominates While Hybrids Accelerate

Virgin PLA controlled 56.82% of 2024 revenue in the PLA barrier coated beverage board market, supported by mature supply chains and compliance track records. Nanocellulose-PLA hybrids are growing at 7.21% CAGR as multilayer processing reaches commercial scale and delivers 98% lower oxygen ingress. Recycled PLA remains niche because post-consumer streams are limited and food-contact rules are stringent.

Hybrid coatings address previous performance gaps, enabling hot-fill and long-shelf-life applications that once defaulted to polyethylene. As converters license slot-die technology, hybrid volumes will climb, narrowing cost gaps and lifting the overall PLA barrier coated beverage board market size at the material level.

By Beverage Packaging Format: Paper Cups Lead While Bottles Accelerate

Paper cups retain 61.64% share thanks to entrenched QSR demand and swift regulatory wins on single-use plastics. Paper bottles post the highest 6.17% CAGR, propelled by premium functional drinks and craft brew launches. Liquid cartons grow steadily in dairy while bag-in-box liners remain technical outliers.

Paper bottles marry tactile fiber appeal with low carbon weight. Billerud’s recent board upgrades show how suppliers tailor density and stiffness for bottle shapes, easing line changeovers. As clarity and barrier demands rise, the PLA barrier coated beverage board market captures incremental value from this format shift.

By End-Use Channel: QSR Scale Meets Brand Direct Adoption

Quick-service restaurants supplied 39.53% of 2024 demand, leveraging global buying power. RTD beverage brands, however, are set to outpace all channels with a 5.93% CAGR. Coffee chains hold steady while institutional caterers remain price sensitive.

McDonald’s has already converted 86.7% of front-of-house packs to renewable or recycled inputs. Direct brand adoption in RTD drinks adds high-margin orders to the PLA barrier coated beverage board market because premium labels accept unit-cost premiums to secure sustainability credentials.

Geography Analysis

Europe commanded 34.07% of global revenue in 2024 for the PLA barrier coated beverage board market, anchored by a stringent chemicals policy and extensive composting networks. The EU BPA prohibition effective January 2025 removes a key rival barrier material, locking in long-term PLA demand. Municipal organic waste programs in Germany and France underpin consumer confidence in compostable cups.

Asia-Pacific is the fastest expanding region at 7.64% CAGR through 2030. China’s food-contact rules, Japan’s Positive List, and Thailand’s 75,000-ton PLA plant collectively create fertile ground for local production and intra-region exports. Manufacturing cost advantages offset higher logistics fees to Europe and North America, so regional converters increasingly pursue domestic beverage accounts.

North America posts steady growth as corporate procurement fills regulatory gaps. Large QSR chains and craft brewers specify compostable fiber packs even when municipal composting access is uneven. California and several Northeast states invest in organics processing, gradually easing end-of-life constraints. As public-private funding expands facilities, the PLA barrier coated beverage board market gains a broader North American footprint.

Competitive Landscape

The PLA barrier coated beverage board market displays moderate fragmentation. Top five suppliers control just under 40% of sales, leaving room for innovator entry. Smurfit Westrock, born from the Smurfit Kappa and WestRock merger, pursues cost synergies and renewable fiber branding with USD 34 billion combined revenue.[1]WestRock, “Transaction to Create a Global Leader in Sustainable Packaging,” WESTROCK.COM Graphic Packaging allocates USD 1 billion to its Waco coated-board mill that supports sustainable beverage formats.[3]Graphic Packaging, “2024 Form 10-K,” INVESTORS.GRAPHICPKG.COM

Specialty Asian laminators target contract runs for European private-label grocers, leveraging lower labor costs. Technology partnerships proliferate; Huhtamaki’s Blueloop program aligns converters with compounders to streamline end-of-life tests.[2]Huhtamaki, “Roadshow Presentation,” HUHTAMAKI.COM White-space opportunities persist in heat-resistant PLA grades and certified recycled PLA lines.

Supply security remains a strategic issue. Corbion’s analysis shows 55% utilization, suggesting limited buffer during demand spikes. NatureWorks’ new president prioritizes feedstock diversification, while upstream sugarcane processors in Thailand sign multi-year agreements that stabilize lactic-acid flows

PLA Barrier Coated Beverage Board Industry Leaders

Huhtamaki Oyj

Stora Enso Oyj

Graphic Packaging International, LLC

International Paper Company

Smurfit WestRock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: EU ban on bisphenol A in food-contact materials became effective, creating immediate demand for PLA barrier alternatives

- October 2024: Australia issued a packaging reform consultation that proposes mandatory recyclability and recycled-content thresholds

- July 2024: Smurfit Westrock reported USD 3 billion second-quarter sales and underscored fiber-based packaging focus

- June 2024: China’s mandatory express-packaging standard GB 43352-2023 took effect, limiting heavy metals and encouraging PLA barrier systems

Global PLA Barrier Coated Beverage Board Market Report Scope

The PLA Barrier Coated Beverage Board Market Report is Segmented by Coating Base Material (Virgin PLA, Recycled PLA, Blended PLA, and Nanocellulose-PLA Hybrid), Beverage Packaging Format (Paper Cups, Liquid Cartons, Paper Bottles, Sleeved Aluminum Cans, and Bag-In-Box Liners), End-Use Channel (Quick-Service Restaurants (QSR), Coffee Shops and Cafes, On-the-go Retail, Institutional Catering, and RTD Beverage Brands), and Geography (North America, Europe, South America, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin PLA |

| Recycled PLA |

| Blended PLA (PLA + additives) |

| Nanocellulose-PLA Hybrid |

| Paper Cups |

| Liquid Cartons |

| Paper Bottles |

| Sleeved Aluminum Cans |

| Bag-in-Box Liners |

| Quick-Service Restaurants (QSR) |

| Coffee Shops and Cafes |

| On-the-go Retail |

| Institutional Catering |

| RTD Beverage Brands |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Coating Base Material | Virgin PLA | ||

| Recycled PLA | |||

| Blended PLA (PLA + additives) | |||

| Nanocellulose-PLA Hybrid | |||

| By Beverage Packaging Format | Paper Cups | ||

| Liquid Cartons | |||

| Paper Bottles | |||

| Sleeved Aluminum Cans | |||

| Bag-in-Box Liners | |||

| By End-use Channel | Quick-Service Restaurants (QSR) | ||

| Coffee Shops and Cafes | |||

| On-the-go Retail | |||

| Institutional Catering | |||

| RTD Beverage Brands | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the PLA barrier coated beverage board market?

It stands at USD 281.4 million in 2025 and is set to reach USD 383.6 million by 2030.

Which region leads in adoption of PLA barrier coated beverage boards?

Europe accounts for 34.07% of global revenue due to stringent chemical policies and composting capacity.

Which coating material grows fastest within this segment?

Nanocellulose-PLA hybrids grow at 7.21% CAGR because they cut oxygen ingress by 98%.

Why are paper bottles gaining popularity for beverages?

They combine premium branding with lower carbon weight and now achieve required shelf life through improved PLA barriers.

What limits faster PLA adoption in emerging markets?

Higher coating costs and limited industrial composting infrastructure slow penetration despite regulatory interest.

Page last updated on: