Frontotemporal Disorders Treatment Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

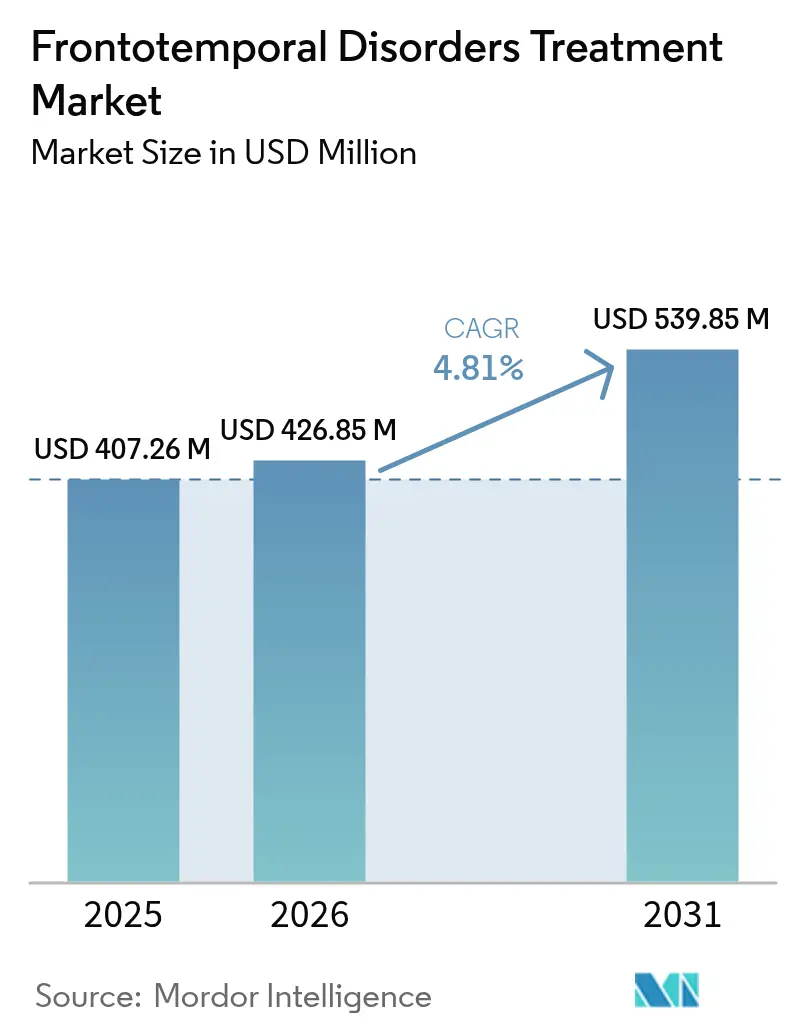

| Market Size (2026) | USD 426.85 Million |

| Market Size (2031) | USD 539.85 Million |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

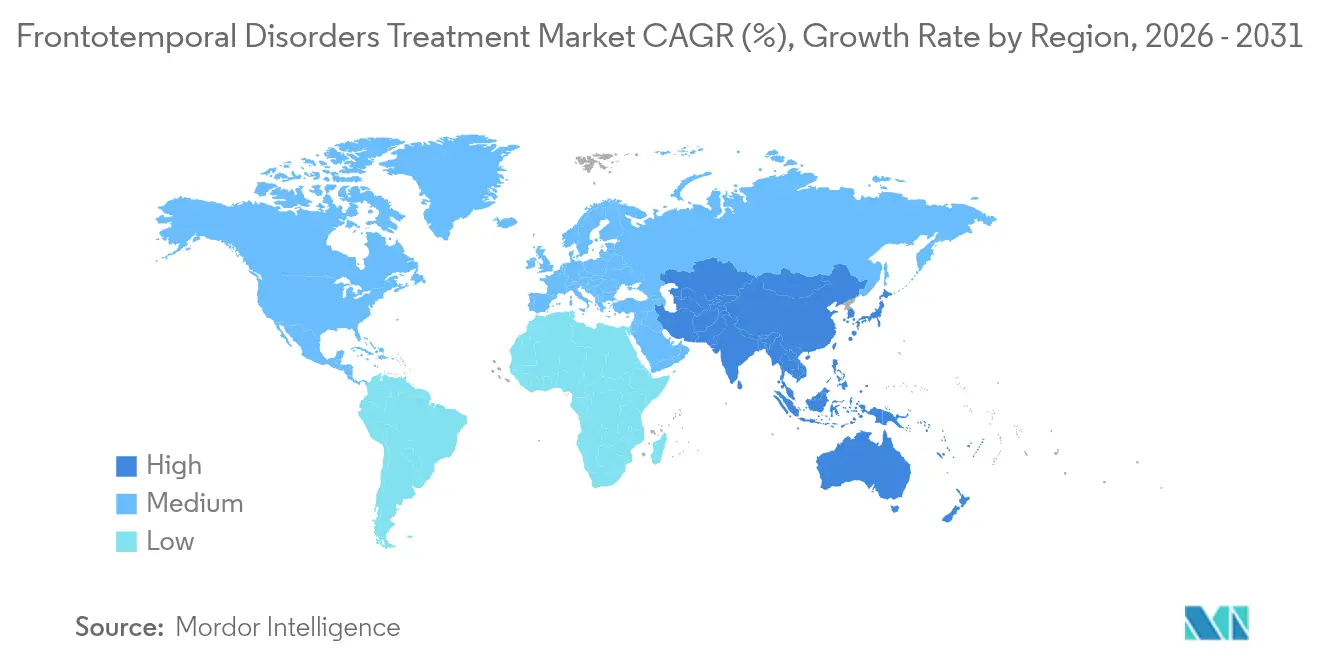

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frontotemporal Disorders Treatment Market Analysis by Mordor Intelligence

The frontotemporal disorders treatment market size was valued at USD 407.26 million in 2025 and estimated to grow from USD 426.85 million in 2026 to reach USD 539.85 million by 2031, at a CAGR of 4.81% during the forecast period (2026-2031). Steady expansion is underpinned by the first wave of disease-modifying gene therapies, wider biomarker-based diagnostics, and sustained public funding for rare neurodegenerative research. Antipsychotics still anchor revenues, yet clinical momentum has shifted toward progranulin-targeted antibodies and adeno-associated-virus vectors that promise earlier intervention. Hospitals retain a central role in complex infusion delivery, but payer support for at-home care is nudging volumes toward retail channels. Regionally, North America benefits from Medicare coverage decisions that shorten the adoption curve for breakthrough assets, while Asia-Pacific capitalizes on rapid dementia prevalence growth to post the fastest regional gains. Investor confidence remains high, demonstrated by multiple USD 100 million-plus rounds funneled into precision-medicine startups.

Key Report Takeaways

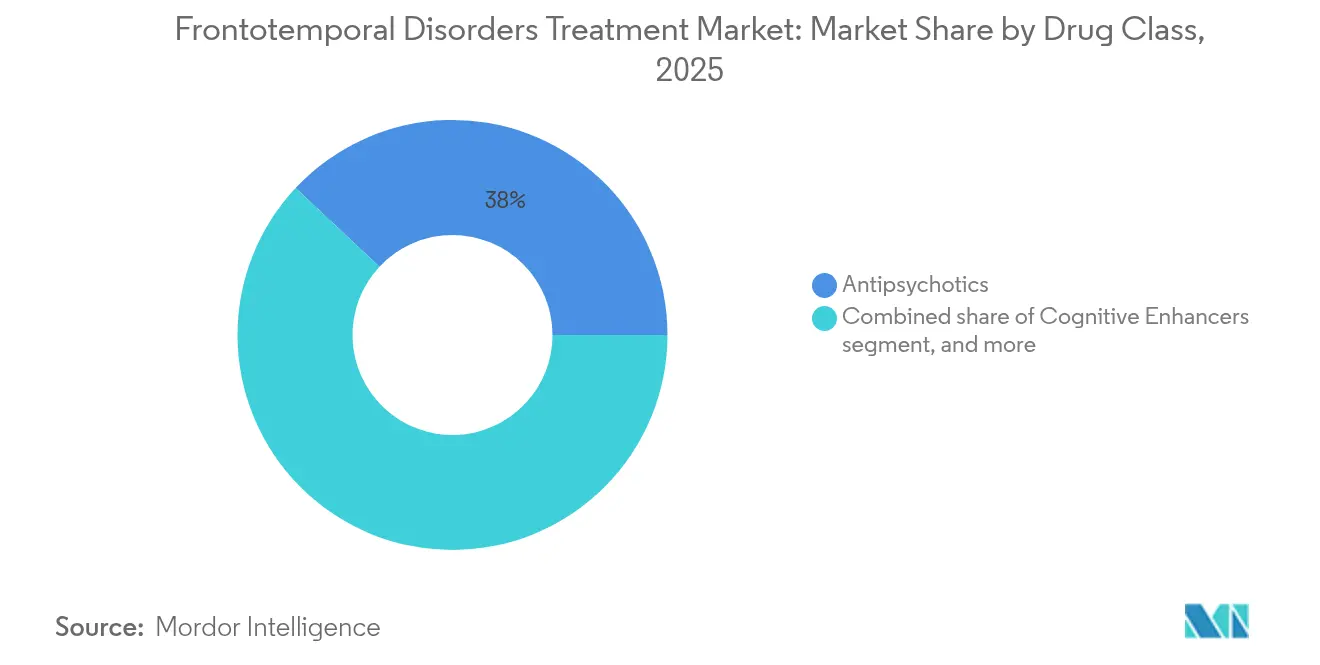

- By drug class, antipsychotics held 38.02% of the frontotemporal disorders treatment market share in 2025; CNS stimulants are forecast to expand at a 7.05% CAGR through 2031.

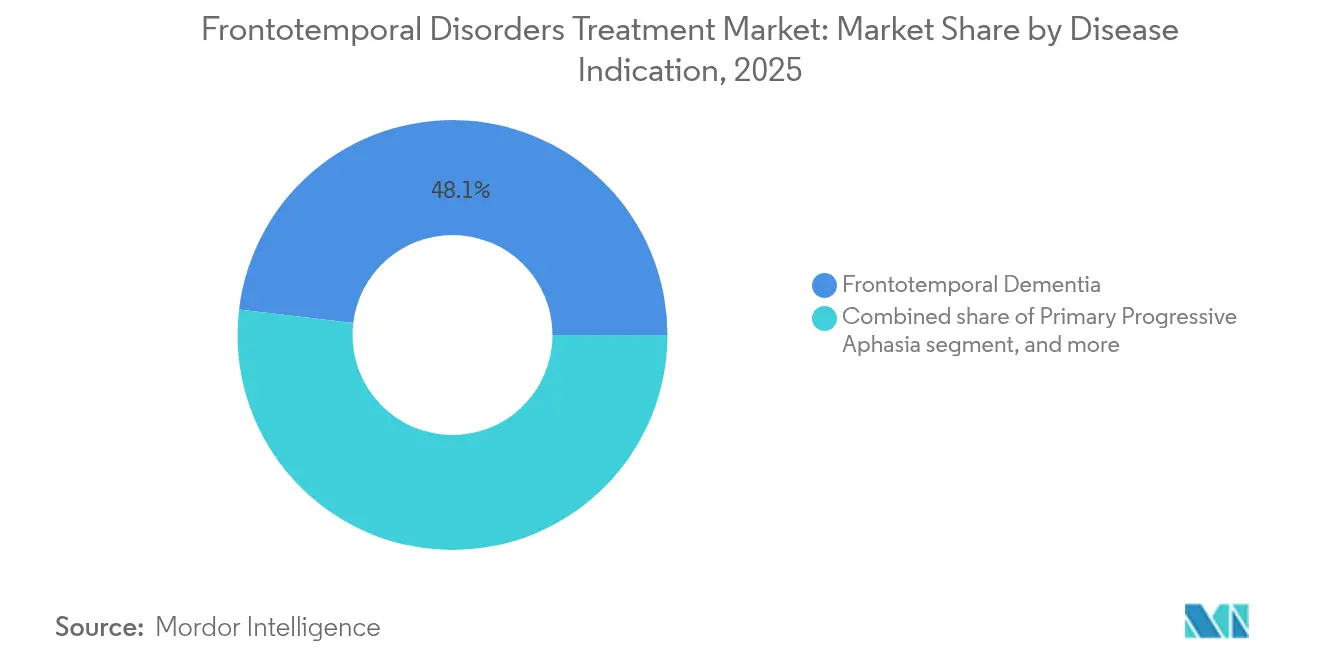

- By disease indication, frontotemporal dementia accounted for 48.10% share of the frontotemporal disorders treatment market size in 2025, while movement disorders are advancing at an 7.78% CAGR through 2031.

- By distribution channel, hospital pharmacies controlled 45.60% revenue share in 2025; retail pharmacies record the highest projected CAGR at 8.12% to 2031.

- By geography, North America led with 41.10% share in 2025 and Asia-Pacific is projected to rise at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frontotemporal Disorders Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global dementia burden | +1.2% | Global – strongest in North America & Europe | Long term (≥ 4 years) |

| Government funding and orphan drug incentives | +0.8% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advancements in neurodegenerative biomarkers | +1.0% | Global, led by North America | Medium term (2-4 years) |

| Pipeline expansion of disease-modifying therapies | +1.5% | Global, early gains in North America | Long term (≥ 4 years) |

| Increasing venture capital in neurotherapeutics | +0.7% | North America & Europe, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Growing diagnostic awareness and screening programs | +0.9% | Asia-Pacific & emerging markets; support from developed EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Dementia Burden

Frontotemporal disorder prevalence is accelerating worldwide, with Asia-Pacific now mirroring Western incidence patterns after fast urbanization and increased life expectancy. Health systems respond by embedding biomarker-based triage into neurology pathways, aligning with the FDA’s 2024 guidance that encourages surrogate endpoint use in trials[1]Office of the Commissioner, “Rare Neurodegenerative Disease Grant Program,” FDA, fda.gov. The U.S. GUIDE Dementia Model introduced coordinated caregiver reimbursement, broadening patient support networks[2]Centers for Medicare & Medicaid Services, “GUIDE Dementia Model,” Medicare, medicare.gov. Budget planners warn that delayed diagnosis inflates long-term care costs, creating impetus for earlier screening programs across primary care.

Government Funding and Orphan Drug Incentives

Federal and philanthropic bodies have earmarked significant grants—such as the U.S. Department of Defense’s USD 650 million 2025 Alzheimer’s Research Program—to stimulate translational dementia studies[3]U.S. Congress, “FY 2025 Defense Appropriations Act,” Congress.gov, congress.gov. Orphan-drug status continues to compress review timelines; latozinemab secured breakthrough status, potentially slicing 6–12 months from evaluation. Global alliances, exemplified by the Treat FTD Fund’s USD 10 million extension through 2035, mitigate commercial risk and maintain momentum for rare-disease pipelines.

Advancements in Neurodegenerative Biomarkers

Blood-based assays that read progranulin or neurofilament light now enable risk stratification outside tertiary centers, reducing trial-screen failure rates and shaving months off recruitment. Smartphone cognitive-testing apps show sensitivity on par with clinic visits and correlate with MRI-measured atrophy. The YWHAG:NPTX2 protein ratio outperforms legacy panels in forecasting cognitive decline, guiding enrichment of disease-modifying trials.

Pipeline Expansion of Disease-Modifying Therapies

AviadoBio’s AVB-101 attracted an Astellas option deal worth up to USD 2.18 billion, underscoring confidence in progranulin gene-replacement platforms. PR006A elevated cerebrospinal progranulin into the normal range for 75% of treated subjects at 12 months, validating vector delivery approaches. Parallel small-molecule programs—such as benzoxazole derivatives that correct lysosomal dysfunction—illustrate pharmacological diversification beyond monoclonal antibodies.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited disease-modifying treatment approvals | –0.9% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| High development and therapy costs | –0.6% | Global, varying by healthcare-funding model | Long term (≥ 4 years) |

| Clinical trial recruitment challenges | –0.7% | Global, acute in ultra-rare genetic subtypes | Short term (≤ 2 years) |

| Reimbursement uncertainties for novel therapies | –0.5% | North America & EU; emerging Asia-Pacific payers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Disease-Modifying Treatment Approvals

Late-stage attrition remains high; Roche terminated a tau-antibody program after suboptimal efficacy, returning rights to partner UCB. The FDA demands rigorous surrogate-endpoint validation, compelling sponsors to run parallel biomarker studies that extend timelines[4]Regulatory Affairs Professionals Society, “Surrogate Endpoints in Neuro Trials,” RAPS, raps.org. Misdiagnosis—estimated near 70% in early FTD referrals—adds enrollment complexity, forcing firms to widen geographic footprints for trials.

High Development and Therapy Costs

Vector-based one-time infusions push six-figure price points as firms build manufacturing suites and maintain long-term registries. Medicare’s Leqembi budget impact foreshadows similar scrutiny for FTD gene therapies, with payers signalling tighter evidence-development mandates. Specialized neurosurgical delivery confines access to academic centers, raising equity concerns and reinforcing the need for value-based contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Antipsychotics Maintain Volume Leadership While Stimulants Surge

Antipsychotics retained 38.02% revenue share of the frontotemporal disorders treatment market in 2025, cushioning overall sales while clinical practice transitions toward mechanism-based drugs. Uptake persists because behavioral symptoms remain ubiquitous across FTD phenotypes. CNS stimulants post the highest 7.05% CAGR through 2031 as physicians probe executive-function benefits and leverage emerging data on dopaminergic modulation. The frontotemporal disorders treatment market size for stimulants is forecast to outpace legacy sedatives, reflecting broader cognitive-enhancement strategies. Novel cholinergic and O-GlcNAcase modulators anchor early-stage portfolios, but widespread use depends on definitive efficacy beyond symptomatic relief. Biologic entrants—namely sortilin-blocking antibodies—could reorder class dynamics if late-phase readouts confirm disease-slowing benefits.

Precision-therapy momentum complicates formulary decisions: payers view traditional antipsychotics as low-cost stopgaps yet recognize rising off-label expenditures on cognitive agents. Manufacturers respond by bundling digital-monitoring apps that capture patient-reported outcomes, aiming to justify higher prices via real-world performance data. As vaccination-style gene therapies enter specialty pharmacies, dosage frequency shifts from chronic daily pills to single procedures, altering lifetime revenue curves across classes.

By Disease Indication: Movement Disorders Accelerate on Diagnostic Clarity

Frontotemporal dementia dominated with 48.10% share of the frontotemporal disorders treatment market in 2025, driven by well-established diagnostic criteria and reimbursement familiarity. Movement-disorder variants, however, are set to grow the fastest at an 7.78% CAGR as tau- and alpha-synuclein-targeting drugs align more tightly with phenotype-specific biomarkers. The frontotemporal disorders treatment market share for movement disorders stands to expand as imaging protocols that differentiate PSP from corticobasal degeneration become mainstream. Improved phenotype delineation also encourages targeted trial enrollment, boosting statistical power and drawing incremental capital toward niche indications.

Clinical-practice guidelines now recommend early speech-language therapy for primary progressive aphasia, but limited therapist availability constrains addressable volume. Device-assisted neurostimulation strategies are gaining foothold, yet reimbursement remains patchy outside academic hubs. Cross-indication lessons from Parkinson’s device programs may shorten learning curves and normalize procedures, but long-term cost-utility data are still evolving.

By Distribution Channel: Retail Pharmacy Uptake Reflects Shift to Home Care

Hospital pharmacies held 45.60% share of frontotemporal disorders treatment market size in 2025, rooted in infusion oversight and neurosurgical coordination. The growth of administration-at-home models now lifts retail pharmacies at an 8.12% CAGR, aided by Medicare reimbursement for subcutaneous antibodies delivered outside inpatient settings. Retail chains are expanding specialized counselling teams to manage neurobehavioral side effects and handle cold-chain biologics.

Online platforms secure modest but rising volumes through caregiver subscription models for oral symptom-control drugs; yet stringent controlled-substance rules and remote-monitoring demands restrain penetration into high-value gene therapies. Hospitals, cognizant of revenue leakage, pilot joint-venture infusion suites that extend clinical oversight into community settings. Collaboration between health-system pharmacies and home-care nurses is essential to maintain pharmacovigilance while meeting patient preference for fewer hospital visits.

Geography Analysis

North America accounted for 41.10% of global revenue in 2025, supported by early-access pathways such as FDA breakthrough designation and structured Medicare payment models covering cognitive-assessment visits. Strong biopharma clusters in California and Massachusetts anchor high trial density, ensuring that most transformative assets debut locally. Payers leverage real-world data networks to negotiate outcomes-based contracts, smoothing uptake for premium-priced innovations.

Asia-Pacific registers the quickest 6.18% CAGR to 2031, benefiting from aging demographics and rapid neurology infrastructure build-out. China’s introduction of blood-based FTD screening kits, pending regulatory clearance, is expected to shorten diagnosis by nearly one year, accelerating therapy initiation. Japanese insurers experiment with bundled payment models for gene-therapy follow-up, setting a precedent for neighboring markets. In India, the rise of urban super-specialty hospitals brings magnet centers capable of handling neurosurgical gene-vector infusions, though unequal rural access persists.

Europe remains an innovation contributor through cross-border research consortia spearheaded by the European Medicines Agency and Horizon Europe grants. Budget constraints lead some national health systems to stagger patient eligibility for high-cost therapies; nonetheless, Germany’s AMNOG framework offers predictable price negotiation timelines that attract launches. Regulatory realignment post-Brexit introduces additional dossier preparation for the United Kingdom, yet its accelerated access collaborative continues to prioritize rare neurodegenerative submissions.

Regulatory Landscape

Regulation for frontotemporal disorders (FTD) therapies is shaped by rare-disease pathways and heightened evidentiary scrutiny for neurodegeneration endpoints, with the US FDA and the European Medicines Agency (EMA) as key reference regulators. In the United States, FDA actions and interactions during 2025-2026 highlighted both acceleration tools and tighter trial-design requirements, including orphan and breakthrough designations for FTD assets, alongside expectations for clinically interpretable endpoints and robust confirmatory evidence in ultra-rare genetic subtypes.

In Europe, the EMA continues to use orphan designation as a central mechanism for FTD programs, including an orphan designation granted in November 2024 for a medicine targeting frontotemporal dementia (EU/3/24/2981). In 2026, advocacy input also became more visible as stakeholders such as the Association for Frontotemporal Degeneration (AFTD) submitted public comments to the FDA on rare-disease evidentiary standards, alongside ongoing US government planning signals through NIH and the National Institute on Aging (NIA) around Alzheimer and related dementias research priorities that include FTD.

Competitive Landscape

The frontotemporal disorders treatment market skews toward moderate fragmentation as incumbent neurology firms share space with gene-therapy specialists and AI-driven startups. Biogen maintains brand recognition through Alzheimer’s monoclonal antibodies and extends that expertise with antisense tau programs that now enjoy FDA fast-track status. Roche refocuses pipeline capital on blood-brain-barrier-crossing antibodies after discontinuing a prior tau asset, while partnering with RNA-editing ventures to spread risk.

Alector’s latozinemab validates the sortilin-blockade concept and may serve as a bellwether for immuno-neurotherapeutics. AviadoBio leverages intrathalamic delivery vectors and secured a capital influx via Astellas to progress AVB-101, highlighting growing big-pharma appetite for external gene-therapy platforms. Asceneuron advances an oral OGA inhibitor financed by a USD 100 million round led by Novo Holdings, signalling venture willingness to underwrite differentiated small molecules.

Competition increasingly centers on integrated diagnostic-therapeutic packages: players pair blood-based assays with treatment algorithms to lock in brand loyalty. Artificial-intelligence tools that predict protein-folding dynamics accelerate target validation and shorten lead-optimization cycles, attracting cross-sector partnerships with cloud-computing firms. With multiple first-in-class entries forecast this decade, marketing strategies will pivot from broad neurologist detailing to genotype-driven, center-of-excellence outreach.

Frontotemporal Disorders Treatment Industry Leaders

Teva Pharmaceutical Industries Ltd.

Pfizer Inc.

AstraZeneca PLC

Biogen Inc.

Lundbeck A/S

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One major opportunity remains the absence of any US FDA-approved therapy specifically indicated for frontotemporal dementia, which keeps symptomatic management as the current standard while leaving whitespace for subtype-defined, mechanism-based products. Recent regulatory designations reflect sustained sponsor interest and potential route-to-market advantages for targeted candidates, including FDA Orphan Drug Designation (November 2024) for CervoMed's neflamapimod and FDA Breakthrough Therapy Designation for Alector's latozinemab in FTD due to progranulin gene mutation (FTD-GRN).

Near-term opportunity is increasingly tied to program selection, trial enrichment, and endpoints that account for genetic and clinical heterogeneity. This shift also follows Alector's Phase 3 INFRONT-3 clinical setback in October 2025, when the program did not meet its primary endpoint and led to discontinuation of the open-label extension and continuation study. Development activity continues across multiple biological pathways and modalities, including gene therapy for genetic forms of FTD such as AviadoBio's AVB-101 and symptom-focused studies such as the Johns Hopkins University Phase 2 trial of vortioxetine initiated in March 2025 for behavioral variant FTD, which in turn supports ongoing demand for biomarkers and trial-ready patient identification tools that improve recruitment efficiency and measurement sensitivity.

Recent Industry Developments

- July 2026: CervoMed completed enrollment in its Phase 2a clinical trial of neflamapimod in nonfluent variant primary progressive aphasia (nfvPPA), a subtype within the frontotemporal dementia spectrum. Completing enrollment de-risks near-term execution and keeps momentum on a subtype-focused development strategy aligned to clearer clinical phenotypes.

- May 2025: Sanofi agreed to acquire Vigil Neuroscience for USD 10.00 per share, adding the TREM2 agonist VG-3927 to its neurodegeneration pipeline. The deal broadened large-pharma participation in neuroinflammation-linked approaches that can be applied across dementias, influencing partnering interest and competitive positioning for smaller FTD-focused developers.

- October 2024: Astellas secured an option-license agreement valued up to USD 2.18 billion for AviadoBio's AVB-101 gene therapy program. The structure signaled continued willingness to fund high-cost, high-complexity genetic-FTD modalities and supported further clinical and manufacturing investment around AAV-based approaches.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of therapies used to manage frontotemporal disorders in diagnosed patients, counted as revenues from prescription treatments across routine and specialty care settings, and captured at the point of distribution through pharmacies.

Scope exclusions: We exclude diagnostics, imaging, caregiver services, and long term care facility costs that are not tied to prescription treatment sales.

Segmentation Overview

- By Drug Class

- Cognitive Enhancers

- Antipsychotics

- Antidepressants

- CNS Stimulants

- Other Drug Classes

- By Disease Indication

- Frontotemporal Dementia

- Primary Progressive Aphasia

- Movement Disorders

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work is used to set the outer boundaries for the model and to anchor the patient and treatment context before we start quantifying value. We reviewed public health and epidemiology sources, such as the US CDC, WHO, OECD health statistics, and national health agencies that publish dementia related burden and care pathway references. We also used peer reviewed neurology journals to confirm diagnosis patterns for frontotemporal dementia, primary progressive aphasia, and related movement presentations.

To convert context into market inputs, we relied on documents that are easy to verify, such as FDA and EMA drug labels and safety updates, national reimbursement notes where available, and trade association releases on rare disease research. Company filings, investor decks, and reputable press were used to understand therapy uptake timing and distribution channel mixes. Where needed for cross checks, paid subscriptions supporting company financials and intelligence, patent databases, and news and financials were referenced to validate timelines and commercialization signals. The sources listed here are illustrative, and many additional public references were consulted to collect data, test assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure test the sizing logic and to confirm real world treatment behavior when public data is thin for rare neurodegenerative conditions. We spoke with a mix of prescribers, pharmacists, payer-facing roles, and industry participants so adoption timing, typical persistence, and channel splits could be validated across major regions. Inputs from these discussions were then used to adjust assumptions on treated share, therapy mix, and how pricing changes are applied year to year.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 43% |

| Mid tier: 50% | Functional/Unit leaders: 36% | EMEA: 31% |

| Smaller Players: 19% | Managers: 50% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a demand-pool build that uses diagnosed prevalence as the main anchor, which is then filtered through treated share and the expected therapy mix used in practice. A top-down approach is applied by reconstructing spend from the treated population across key indications and then allocating value by channel based on how medicines are actually dispensed. To keep the total realistic, selective bottom-up checks are run using sampled price-per-therapy and volume proxies, followed by supplier and channel checks to adjust any obvious over or under counting.

A few variables drive most of the work in this market model, even though more are tracked in the background. These include diagnosed prevalence trends, prescribing intensity by symptom cluster (behavioral symptoms vs language impairment), therapy class mix (such as antidepressants and antipsychotics), distribution channel splits across hospital, retail, and online pharmacies, and expected pricing progression as labels expand or competition changes. When data is missing for a country, we use regional analogs with similar care pathways and then apply a conservative adjustment after validation calls.

For forecasting, scenario analysis is used so the model can reflect uncertainty around new therapy launches, the speed of biomarker based diagnosis, and reimbursement expansion. The final curve is set only after expert feedback has aligned with macro signals, such as aging demographics and neurology specialist access, so the story remains explainable and repeatable.

Data Validation & Update Cycle

Validation happens in layers, because a single check rarely catches the full picture in a rare disease treatment market. Model outputs are compared against independent signals such as indication level treatment intensity, channel mix reasonableness, and implied spend per treated patient, which is then reviewed for outliers by a second analyst. If a country result looks inconsistent with epidemiology or access realities, interviews are revisited and the assumption is corrected before sign off.

Reports are refreshed annually, and interim updates are made when material events occur, such as a key regulatory decision, a major label change, or a pricing shift that impacts uptake. Before delivery, an analyst performs a fresh pass on inputs and calculations so clients receive the latest updated view.

Mordor Intelligence's Frontotemporal Disorders Treatment Market Size Compared With Other Published Estimates

Published market numbers for this space can vary a lot, since the condition is rare and the line between treatment and broader disease management is not always drawn the same way. Differences also come from the year chosen as the base, which symptoms are counted as in-scope therapy demand, and how pricing changes are applied across geographies.

By checking indication-level treated share and refreshing channel-weighted pricing assumptions each cycle, Mordor Intelligence keeps this estimate tied to prescription treatment sales (hospital, retail, and online pharmacies) rather than bundling diagnostics and supportive services into the same total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 426.85 M (2026) | |

| Trade Journal A | USD 396.10 M (2025) | Uses an adjacent scope labeled as FTD management, and the total appears to include diagnostics and supportive care along with treatment, which changes the boundary and the base year. |

| Global Consultancy B | USD 241.36 M (2024) | Represents a broader FTD market framing with a smaller stated 2024 value, and limited visibility on treated-share logic, channel coverage, and pricing update timing. |

The spread across estimates mostly comes down to what is counted inside the market and how the starting year is selected. When treatment revenues are separated cleanly from diagnostics and services, and when treated share and channel mix are validated, the resulting market value is easier to trace back to real demand drivers and to update in a consistent way year after year.

Key Questions Answered in the Report

What is the projected size of the frontotemporal disorders treatment market in 2031?

The market is forecast to reach USD 539.85 million by 2031, growing at a 4.81% CAGR.

Which drug class currently generates the highest revenue?

Antipsychotics lead with 38.02% share of 2025 global revenue.

Which region will grow the fastest through 2031?

Asia-Pacific is projected to expand at a 6.18% CAGR, outpacing all other regions.

What therapy has the first FDA breakthrough designation for FTD?

Latozinemab, an anti-sortilin antibody for progranulin mutations, secured breakthrough status in January 2025.

Why are retail pharmacies gaining market share?

Medicare coverage for home-infusion antibodies and the rise of subcutaneous formulations are shifting volumes from hospital to retail settings.

How fragmented is the competitive landscape?

The market scores 6/10 on concentration, indicating moderate fragmentation with the top five players controlling about 60% of revenue.

Page last updated on: