Hyperhidrosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 731.77 Million |

| Market Size (2031) | USD 959.12 Million |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

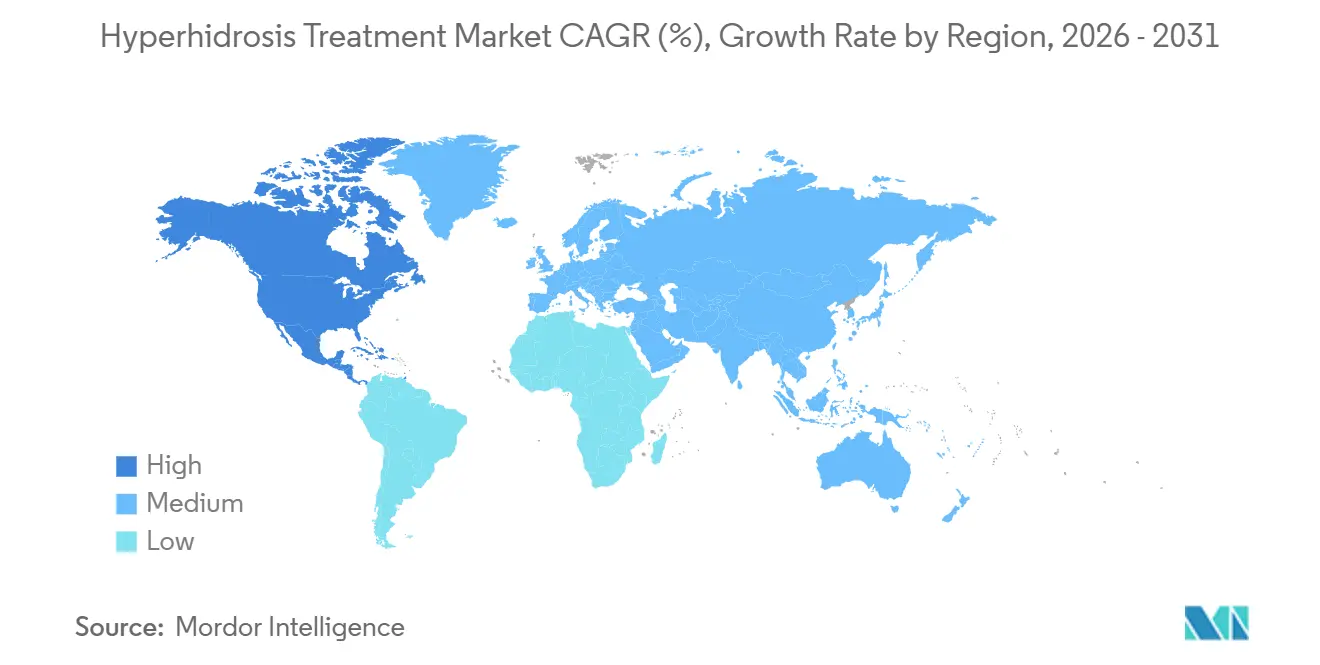

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyperhidrosis Treatment Market Analysis by Mordor Intelligence

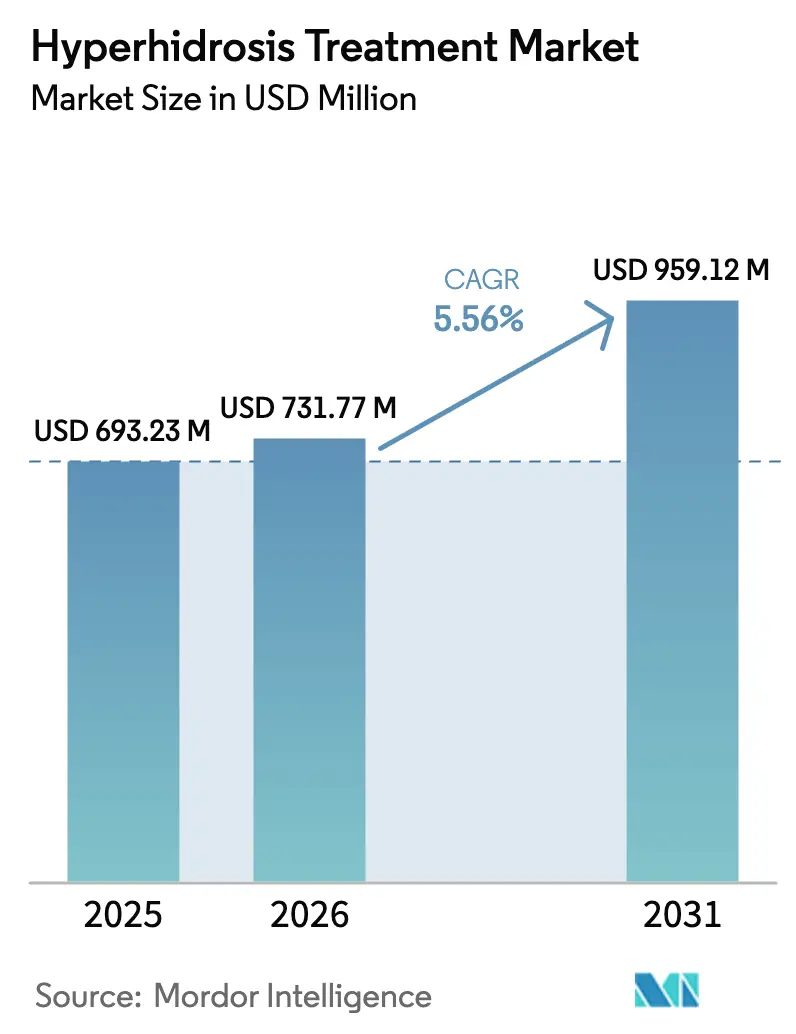

The Hyperhidrosis Treatment Market size is expected to grow from USD 693.23 million in 2025 to USD 731.77 million in 2026 and is forecast to reach USD 959.12 million by 2031 at 5.56% CAGR over 2026-2031.

The industry is transitioning from traditional surgical approaches to precision biologics, energy-based devices, and digitally enabled topical therapies. The U.S. Food and Drug Administration’s approval of sofpironium bromide (Sofdra) in June 2024 underscores the growing acceptance of non-invasive treatment pathways. This development, coupled with Candesant Biomedical’s successful financing for its Brella patch, reflects strong investor confidence in outpatient solutions. While botulinum toxin A injections remain a key revenue driver, the emergence of EU MDR-certified microwave thermolysis platforms and direct-to-consumer tele-dermatology services is expanding patient access and reshaping competitive strategies. Reimbursement policies remain a critical factor: U.S. payers require antiperspirant step therapy before approving prescription topicals, whereas Europe and Japan are showing increased flexibility toward injectables and device-based procedures. Furthermore, the growth of e-commerce subscriptions and home-use iontophoresis kits is driving incremental demand beyond traditional clinical settings, adding a sustainable growth dimension to the hyperhidrosis treatment market.

Key Report Takeaways

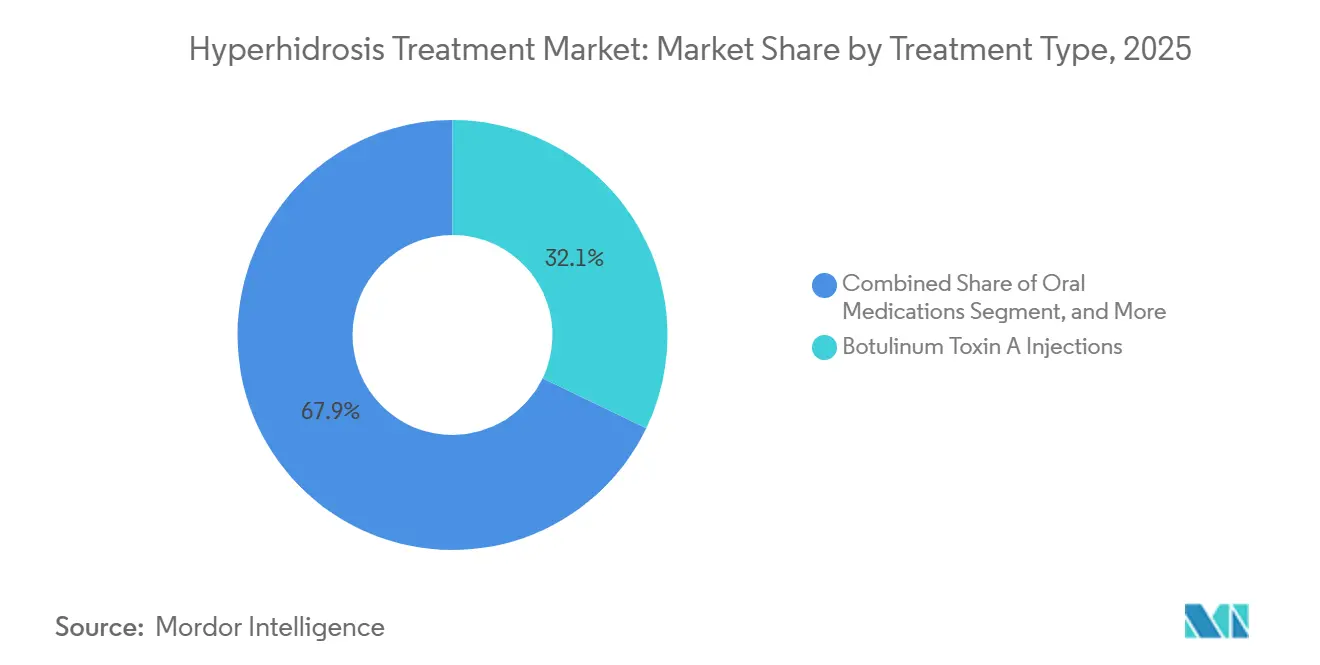

- By treatment type, botulinum toxin A injections held 32.13% of hyperhidrosis treatment market share in 2025, whereas microwave thermolysis is projected to post the fastest 7.54% CAGR through 2031.

- By disease type, primary focal hyperhidrosis accounted for 75.35% of 2025 demand, while secondary generalized cases are set to expand at a 7.43% CAGR to 2031.

- By site, axillary hyperhidrosis accounted for 50.45% of the 2025 volume, but palmar cases will drive growth at a 7.88% CAGR over the forecast horizon.

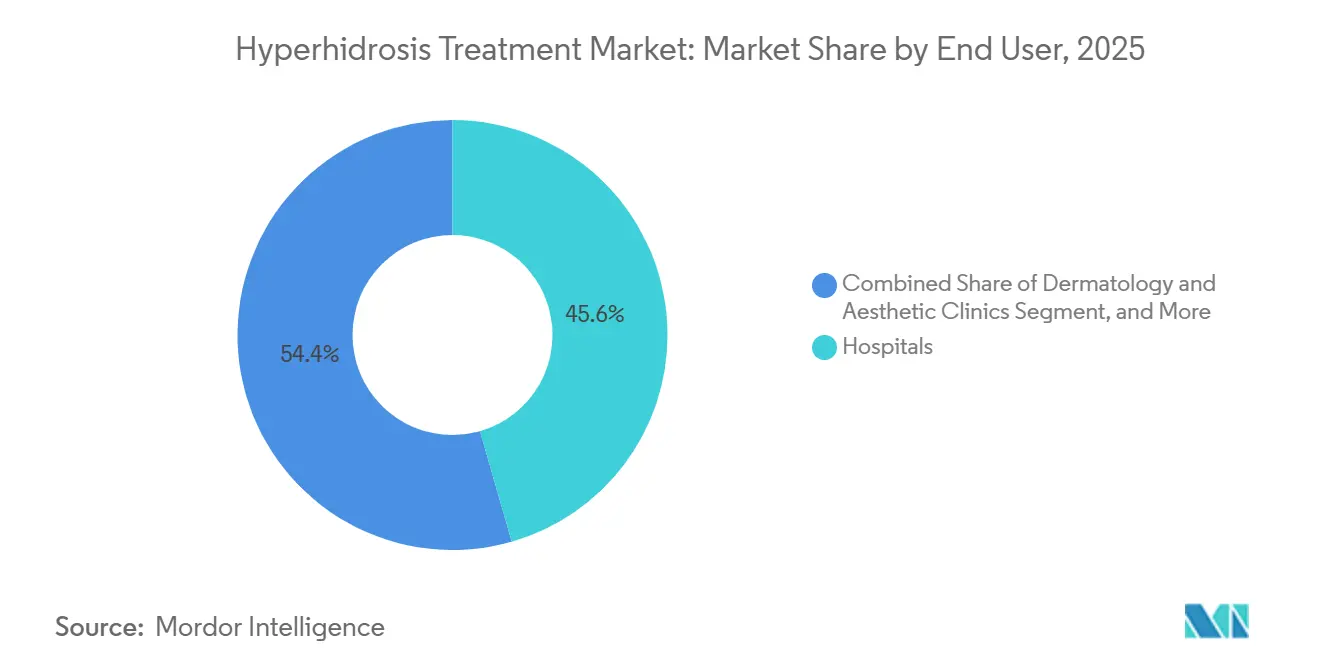

- By end user, dermatology and aesthetic clinics accounted for 45.56% of 2025 revenue, while home-care and OTC channels are forecast to grow at an 8.76% CAGR.

- By distribution channel, retail pharmacies accounted for 52.17% of 2025 sales, yet e-commerce is expected to grow at an 8.54% CAGR through 2031.

- By geography, North America contributed 42.56% of 2025 turnover, but Asia-Pacific is anticipated to log the fastest 6.43% CAGR on the back of Japanese product launches.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hyperhidrosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence and Diagnosis of Hyperhidrosis | +0.9% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Rising Demand for Minimally and Non-Invasive Treatment Modalities | +1.2% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Regulatory Approvals of Innovative Topical and Device-Based Therapies | +1.0% | North America, Europe, APAC spillover | Medium term (2-4 years) |

| Technological Advancements in Energy-Based and Digital Platforms | +0.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Growing Consumer Awareness and Quality-of-Life Focus | +0.7% | Global | Medium term (2-4 years) |

| Expansion of Tele-Dermatology and Direct-to-Consumer Channels | +0.6% | North America, Europe, APAC urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence and Diagnosis of Hyperhidrosis

Epidemiological data indicate that sweating disorders affect 4.8% of the U.S. population, or 15.3 million individuals, and 5.5% of Sweden's population, underscoring their significant prevalence in high-income markets. The adoption of tools such as the Hyperhidrosis Disease Severity Scale has streamlined payer documentation processes and accelerated clinical presentation timelines. The FDA approval of Sofdra, following the successful CARDIGAN trial, has established objective responder endpoints as critical benchmarks for reimbursement. Simultaneously, advocacy initiatives are driving patient engagement, effectively converting unmet needs into treated prevalence within the hyperhidrosis treatment market.

Rising Demand for Minimally and Non-Invasive Treatment Modalities

High compensatory sweating rates of 40%-89% following endoscopic thoracic sympathectomy have driven patients toward reversible treatment options[1]Health Products Regulatory Authority, “Risk Assessment of ETS,” hpra.ie. Candesant’s FDA-cleared Brella patch delivers a quick, three-minute, office-based solution with a 63.6% responder rate, eliminating the need for systemic drug exposure. Similarly, MiraDry’s dual-frequency microwave thermolysis has received EU MDR clearance, positioning it to enter more stringent European markets by 2025. These advancements are driving growth in the hyperhidrosis treatment market by addressing patient demand for effective, non-surgical, and low-maintenance solutions.

Regulatory Approvals of Innovative Topical and Device-Based Therapies

With Sofdra now approved in the United States and under PMDA review in Japan, the topical anticholinergic segment is regaining momentum after a six-year stagnation. Recent updates from the European Medicines Agency (EMA) to botulinum toxin labeling, along with EU Medical Device Regulation (MDR) certification for devices, are standardizing clinical dosing and safety data. This regulatory alignment is facilitating faster payer acceptance. As a result, the hyperhidrosis treatment market, supported by a strong pipeline, is well-positioned for accelerated cross-regional launches, enabling quicker recovery of R&D investments.

Technological Advancements in Energy-Based and Digital Platforms

MiraDry’s 84% sweat-reduction data at 12 months using dual-frequency delivery show that device engineering continues to narrow the durability gap versus surgery. Real-time thermal feedback in fractional lasers is reducing adverse events below 5%. Digital advances matter as well: Botanix’s tele-prescribing portal handles asynchronous photo consults, achieving 40% of Sofdra’s first-half sales online. Technology is broadening geographies and demographics served by the hyperhidrosis treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs and Limited Reimbursement Coverage | -0.8% | Global, acute in emerging markets & U.S. uninsured | Short term (≤ 2 years) |

| Limited Long-Term Efficacy of Existing Therapies | -0.5% | Global | Medium term (2-4 years) |

| Adverse Events and Safety Concerns with Surgical and Energy Devices | -0.4% | Global, higher scrutiny in Europe post-MDR | Medium term (2-4 years) |

| Supply Chain and Pricing Volatility of Key Therapeutic Inputs | -0.3% | Global, tightest in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Limited Reimbursement Coverage

Monthly outlays of USD 580-700 for Qbrexza demand prior authorization, capping mainstream adoption[2]Cigna, “Coverage Policy for Hyperhidrosis Treatments,” cigna.com. Botulinum toxin reimbursements are quantity-limited, and miraDry’s USD 2,000-3,000 fee is seldom covered, painting a price-sensitive reality for the hyperhidrosis treatment market. In lower-income regions, generic aluminum chloride remains the only viable choice, muting near-term premium-therapy penetration.

Limited Long-Term Efficacy of Existing Therapies

Antibody development reduces botulinum toxin response in up to 3% of repeat recipients, while topical anticholinergic adherence wanes after six months due to side effects. Iontophoresis maintenance every 9-10 days deters busy patients. Surgical sympathectomy’s compensatory-sweating risk fuels regret litigation, signaling an unsolved need for lasting, low-burden solutions within the hyperhidrosis treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Injectables Lead, Energy Devices Surge

Botulinum toxin A injections captured 32.13% of 2025 demand, translating to robust cash flow for AbbVie’s flagship product line, while Cigna and Blue Cross cover axillary administrations once aluminum chloride fails[3]. Yet microwave thermolysis outpaces the hyperhidrosis treatment market size with a 7.54% CAGR, leveraging miraDry’s EU MDR clearance and 84% 12-month sweat-reduction data to attract clinics seeking capital-light, single-session revenue.

Topical anticholinergics such as Sofdra lessen systemic exposure, filling safety gaps left by Qbrexza. Meanwhile, home iontophoresis systems tested at 9-10-day efficacy cycles supply palmar and plantar sufferers with an OTC workaround, though regimen fatigue remains a headwind. ETS volumes slide further as reversible device options proliferate, leaving surgery a shrinking niche inside the hyperhidrosis treatment market.

By Disease Type: Primary Focal Dominates, Secondary Cases Accelerate

Primary focal hyperhidrosis generated 75.35% of 2025 turnover, buoyed by established diagnostic grading and multiple FDA-approved modalities. Insurer alignment around HDSS scoring eases claim workflows, reinforcing its dominant share within the hyperhidrosis treatment market.

Secondary generalized hyperhidrosis is rising at 7.43% CAGR as oncology regimens and metabolic comorbidities swell patient counts; 30%-50% of hormone-therapy recipients experience problematic sweating, opening demand for systemic anticholinergics and adjunct topicals. Selective M3 antagonists in early pipelines could offer lower side-effect loads, signaling future competition for entrenched oral options.

By Site of Hyperhidrosis: Axillary Sites Lead, Palmar Cases Gain

Axillary presentations owned 50.45% of 2025 procedure volume, underpinned by Sofdra, Qbrexza, and injectables that fit a well-reimbursed care pathway. Device players such as Brella and miraDry specifically target underarm glands, reinforcing incumbent dominance.

Palmar hyperhidrosis, however, is forecast to eclipse overall hyperhidrosis treatment market growth at a 7.88% CAGR, propelled by home-use iontophoresis kits and emergent fast-dry gels aimed at hand-sweating professionals. Plantar and craniofacial sites remain tougher to treat, but clinical-strength wipes and refined laser protocols are making incremental inroads.

By End User: Clinics Dominate, Homecare Channels Surge

Dermatology and aesthetic clinics delivered 45.56% of 2025 revenue thanks to procedure-heavy injectables and microwave thermolysis sessions, each of which fit high-throughput practice economics. Hospitals manage complex secondary cases yet remain volume-constrained.

Home care and OTC demand is set to grow at an 8.76% CAGR as direct-to-consumer brands leverage e-commerce scale. SweatBlock’s towelette subscriptions and Dermadry’s USD 499 kits let consumers bypass appointment queues, extending the hyperhidrosis treatment market size beyond brick-and-mortar care.

By Distribution Channel: Retail Pharmacies Lead, E-Commerce Accelerates

Retail pharmacies filled 52.17% of 2025 prescriptions, driven by PBM-routed Qbrexza and Sofdra volumes and a constant stream of OTC aluminum chloride refills. Pharmacist counseling improves persistence, anchoring current dominance.

E-commerce should post an 8.54% CAGR through 2031 as Amazon and regional e-pharmacies scale auto-ship routines and co-pay assistance plug-ins. Botanix’s integrated script-to-door model already funnels 40% of Sofdra’s sales through digital touchpoints, foreshadowing wider channel shift across the hyperhidrosis treatment market.

Geography Analysis

In 2025, North America captured 42.56% of sales, buoyed by favorable coverage policies, high per-capita spending, and a swift embrace of biologics. Cigna's 2024 update, which removed the requirement for iontophoresis trials prior to injectable authorizations, streamlined treatment initiation. Meanwhile, Sofdra's direct-to-consumer debut gained momentum online, and U.S. consumers are benefiting from reduced out-of-pocket expenses due to cross-border procedure tourism in Mexico. This dynamic creates a landscape where revenue in the hyperhidrosis treatment market is both accelerated and redistributed.

Europe made strides, bolstered by botulinum toxin reimbursement parity and the July 2025 EU MDR nod for microwave thermolysis in Germany, France, and Italy. The EMA's standardized labeling boosted clinician dosing confidence. However, France's stringent cost-effectiveness evaluations tempered the entry of premium topicals. Despite these challenges, statutory coverage for severe cases solidifies Europe's pivotal role in the hyperhidrosis treatment arena.

Asia-Pacific is set to expand at a 6.43% CAGR, spearheaded by Japan. Here, Maruho's glycopyrronium tosylate formulation, with a 3.75% concentration, boasted a 51.6% responder rate in late-stage trials. China's growing aesthetic demand and India's 35% boom in e-pharmacy broaden the market's reach, even as modest household incomes dampen prescription rates. Meanwhile, Australia and South Korea, driven by a surge in private clinic demand, contribute to the region's status as the fastest-growing in the hyperhidrosis treatment market.

Regulatory Landscape

Regulation of hyperhidrosis treatments spans drug and device pathways, which creates different evidence and compliance requirements by modality and region. In the United States, the FDA approved Sofdra (sofpironium bromide 12.45% topical gel) in June 2024 for primary axillary hyperhidrosis in patients aged 9 years and older, reinforcing the NDA route for topical anticholinergics alongside established products such as glycopyrronium-based therapies and botulinum toxin type A for axillary use. The market also depends on FDA device oversight for iontophoresis and energy-based platforms used in clinics and home settings.

In Europe and the United Kingdom, product access is shaped by regulator-led labeling and conformity routes for devices. The UK MHRA granted marketing authorization for Axhidrox (glycopyrronium bromide 1% cream) on June 9, 2025 for severe primary axillary hyperhidrosis in adults, while EU-level actions such as EMA updates to botulinum toxin labeling support more standardized dosing and safety expectations across member states. Separately, in July 2026 the FDA published a proposed rule to modernize drug establishment registration and listing to accommodate distributed manufacturing and strengthen visibility for foreign establishments supplying the US, shifting near-term compliance and documentation focus toward globally sourced APIs and finished products.

Value Chain Analysis

The hyperhidrosis treatment value chain begins with pharmaceutical-grade APIs, including anticholinergics such as sofpironium bromide and glycopyrronium salts, and biologic drug substance for neurotoxins. This is followed by formulation, fill-finish, and quality systems that support prescription products and specialty devices. CDMOs play an outsized role in scaling and de-risking supply for newer topical therapies; for example, Piramal Pharma Solutions announced a manufacturing and supply partnership with Botanix SB Inc. in May 2026 to support development and validation of sofpironium bromide API using a twin-site strategy across Michigan and Canada, reflecting a move toward resilient, multi-site sourcing for critical inputs.

Downstream, products move through dermatologist and aesthetic clinic networks for procedure-based care, including botulinum toxin injections and microwave thermolysis, and through retail pharmacies and e-commerce for prescription topicals and OTC regimens. Market access increasingly depends on payer documentation and channel enablement, including tele-dermatology for prescription capture, while device pathways add their own controls and testing expectations. The FDA final rule published in June 2026 created a Class II category with special controls for skin patches intended to treat hyperhidrosis, clarifying requirements such as clinical performance and shelf-life documentation that can affect design, manufacturing validation, and time-to-market for emerging patch-based solutions.

Competitive Landscape

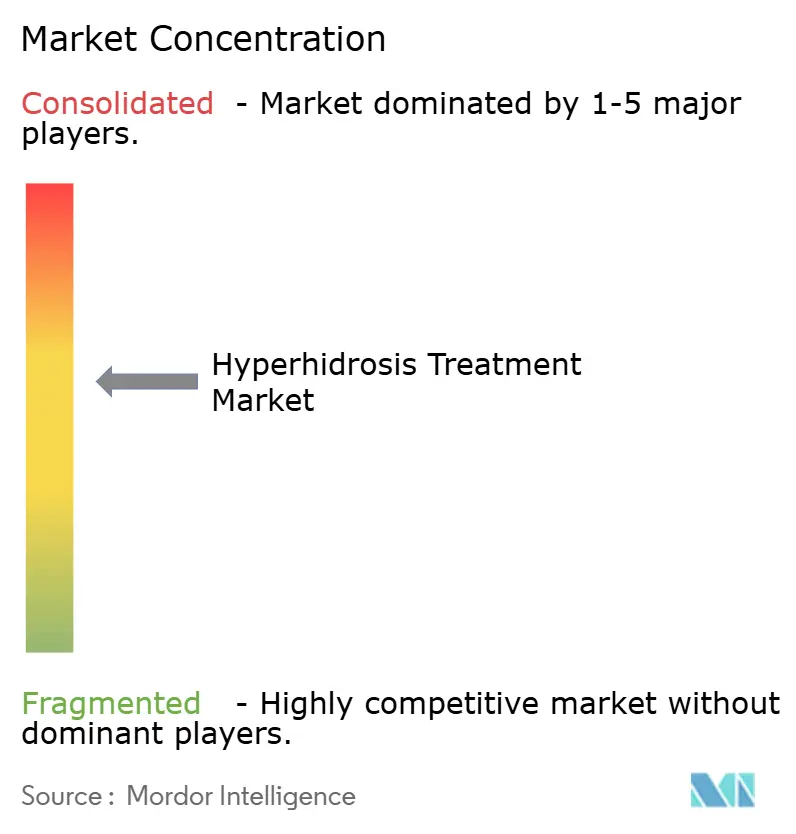

The hyperhidrosis treatment market is moderately fragmented. The injectables segment is led by AbbVie, Merz Pharma, and Revance. In Q3 2024, AbbVie achieved a therapeutic turnover of USD 848 million, driven by its Botox Savings incentive program. Organon's USD 1.2 billion acquisition of Dermavant highlights big pharma's strategic focus on late-stage topical franchises, potentially challenging Qbrexza’s market share.

Digital-first entrants are gaining traction in the market. Botanix captured 40% of Sofdra’s initial demand through telehealth channels, while Candesant’s Brella patch, with its 12-month durability claim, threatens to disrupt repeat neurotoxin treatments. Iontophoresis device providers Dermadry and Hidrex are targeting cost-conscious consumers with products priced between USD 499-950, gradually eroding the market share of traditional clinic operators.

Technology-driven collaborations are increasing. In 2025, Dermata partnered with Revance to develop combined topical and injectable regimens to extend the efficacy of neurotoxins. With advancements such as microneedle-delivered neurotoxins and selective muscarinic antagonists in the pipeline, market leaders must adopt an acquisitive approach to remain competitive in the rapidly evolving hyperhidrosis treatment landscape.

Hyperhidrosis Treatment Industry Leaders

AbbVie Inc.

Eli Lilly (Dermira)

Sientra Inc.

Merz Pharma

Brickell Biotech Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is most visible in non-axillary sites and in options that reduce maintenance burden relative to repeat injections or frequent device sessions. Clinical trial activity points to where companies and investigators are probing expansion beyond underarm indications, including palmar and frontal hyperhidrosis: a pilot open-label study (NCT06881394, registered February 2025) evaluates topical cyanoacrylate for palmar hyperhidrosis, while a separate study initiated in November 2025 (NCT07561580) evaluates intradermal botulinum toxin type A for frontal hyperhidrosis, with a primary completion timing set in 2026. These efforts align with market signals that palmar cases are increasingly managed through home-use and OTC pathways, but durable prescription solutions remain limited.

A second opportunity area sits at the intersection of convenience, outpatient delivery, and clearer device entry requirements. The FDA approval of Sofdra in June 2024 expands the addressable prescription topical segment in the United States. In addition, the FDA final rule published in June 2026 establishing Class II special controls for hyperhidrosis skin patches provides a defined regulatory route for patch-based devices that can support quick office-based or hybrid care delivery. Together, these developments support product strategies that combine prescription capture through tele-dermatology with retail and e-commerce fulfillment, alongside differentiated device or patch offerings designed to meet specified performance and documentation standards.

Recent Industry Developments

- May 2026: Piramal Pharma Solutions announced a manufacturing and supply partnership with Botanix SB Inc. to support development and validation of sofpironium bromide API, including a twin-site strategy across Michigan and Canada. The move strengthens upstream capacity and redundancy for a newly commercialized topical anticholinergic category, reducing supply risk as prescription demand scales across channels.

- April 2025: AbbVie submitted a Biologics License Application to the US FDA for trenibotulinumtoxinE (TrenibotE) for the treatment of moderate to severe glabellar lines, supported by Phase 3 data in more than 2,100 patients. While not a hyperhidrosis label filing, the program signals continued innovation investment in next-generation neurotoxins, a modality central to clinic-based sweat management.

- September 2024: Organon completed its acquisition of Dermavant for up to USD 1.2 billion, adding late-stage topical dermatology assets to its portfolio. Consolidation of topical franchises raises competitive pressure on incumbent prescription anticholinergics and can expand commercialization resources behind dermatology-focused offerings relevant to hyperhidrosis care pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paid treatments used to manage hyperhidrosis (excessive sweating), across drugs, procedures, and devices that reduce sweat production or block sweat glands, measured as treatment revenues across key care settings and channels.

Scope exclusions: We exclude non-medical home remedies and general skin care products that are not positioned or used as hyperhidrosis treatments.

Segmentation Overview

- By Treatment Type

- Topical Antiperspirants & Anticholinergics

- Botulinum Toxin A Injections

- Iontophoresis Devices

- Microwave Thermolysis

- Endoscopic Thoracic Sympathectomy (ETS)

- Laser & Energy-Based Therapies

- Oral Medications

- Other Treatment Types

- By Disease Type

- Primary Focal Hyperhidrosis

- Secondary Generalised Hyperhidrosis

- By Site of Hyperhidrosis

- Axillary (Underarms)

- Palmar (Hands)

- Plantar (Feet)

- Craniofacial

- Other Site of Hyperhidrosis

- By End User

- Hospitals

- Dermatology & Aesthetic Clinics

- Ambulatory Surgical Centers

- Homecare & OTC Channels

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- E-Commerce

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the treated population, diagnosis patterns, and therapy adoption in major regions before model assumptions were finalized. Public sources that helped shape the structure included sources such as the US Centers for Disease Control and Prevention (for health statistics context), the US FDA (labels and approvals), the National Institutes of Health and peer reviewed journals (clinical usage and outcomes), and the World Health Organization (health system indicators and comparability across countries).

We also reviewed company filings, investor presentations, earnings call transcripts, and reputable press coverage to track product launches, access changes, and demand signals around dermatology and outpatient procedures. For cross checks, we used paid subscriptions for company financials and intelligence, patent databases, and an import/export shipment-level database where device and consumable flows were relevant. These desk sources are illustrative, and other public references were also used to complete data collection, validation, and open-question clarification.

Primary Interviews and Surveys

Primary work focused on structured interviews and short surveys with dermatology clinics, hospital pharmacy stakeholders, ambulatory surgical centers, distributors, and a few device-focused specialists to confirm what is actually used and paid for in routine care. Because this is a global market, we balanced input across APAC, EMEA, and the Americas so differences in pricing, channel mix, and procedure uptake could be reflected, and then closed the open gaps from desk research before the final totals were signed off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 52% |

| Mid tier: 52% | Functional/Unit leaders: 32% | EMEA: 30% |

| Smaller Players: 17% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

Our model starts with a top-down build that converts epidemiology and diagnosis pools into a treated cohort by site and care setting, then applies therapy mix and average annual cost of therapy to reconstruct total demand in value terms. That demand pool is checked with selective bottom-up approximations, such as sampled country pricing, channel markups, and limited roll ups of procedure volumes in outpatient settings, so totals can be corrected when one input looks overstated.

Key inputs used (illustrative) included prevalence and diagnosed share for focal and secondary disease, site mix (axillary, palmar, plantar, craniofacial), procedure penetration for botulinum toxin and energy based options, refill and retreatment intervals, and region level price ranges by channel (hospital pharmacy, retail pharmacy, and e-commerce). When a country level data series was not clean, we filled gaps using proxy markets with similar care pathways and income bands, then validated the implied treatment cost per patient with primary feedback.

For forecasting, scenario analysis was used around adoption and pricing because step changes often come from access, awareness, and reimbursement updates rather than smooth demand growth. Assumptions for uptake and price progression were aligned to what respondents expect for new launches, procedure substitution, and the shift of care toward dermatology and outpatient centers.

Data Validation & Update Cycle

Outputs were triangulated across multiple lenses so one noisy data series would not drive the final number. We compared the implied treated patients, procedure counts, and per patient spending with independent signals, and then investigated variances that broke expected relationships, such as sudden price jumps that did not match label changes or channel shifts.

Before sign off, the model goes through multi step analyst reviews, and re-contacts are triggered when a key assumption moves the result beyond a reasonable band for a region or treatment type. The report is refreshed annually, and interim updates are made when material events occur, such as major approvals, access changes, or safety related updates. Prior to delivery, a fresh pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Hyperhidrosis Treatment Market Sizing Compared With Other Published Estimates

Published market values for hyperhidrosis treatment do not always match because the underlying math depends on what is counted as a treatment, how procedure revenues are handled, and how fast pricing is assumed to change across regions. Timing also matters, since some publishers use an older currency conversion point or keep assumptions unchanged for too long.

Services and related goods that are bundled into a factory-gate revenue view sit outside Mordor Intelligence's scope, which keeps the total focused on treatment revenues tracked through care settings and channels that patients and providers actually pay for.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.69 B (2025) | |

| Global Market Report A | USD 1.58 B (2024) | Uses a factory-gate framing that can bundle creator-level services and related goods into the value, which can lift totals versus a treatment-spend view. The base year also differs, and the chain of pricing from manufacturer level to care channel is not always made explicit. |

| Industry Research Portal B | USD 0.71 B (2024) | Uses a different base year and forecast window, and the treatment mix and retreatment frequency assumptions are not clearly tied back to site level practice patterns. Some estimates also smooth adoption too evenly across regions, which can shift the current-year value. |

Taken together, the spread mainly comes from how revenues are defined (treatment spend versus factory-gate style totals), the year used as the starting point, and how procedure frequency and channel pricing are modeled. By keeping the inputs tied to treated cohort sizing, site mix, and realistic price ranges by channel, the final number stays transparent and repeatable when the same steps are applied country by country.

Key Questions Answered in the Report

What is the projected size of the hyperhidrosis treatment market by 2031?

It is forecast to reach USD 959.12 million by 2031, expanding at a 5.56% CAGR from 2026.

Which therapy currently holds the largest share in treating excessive sweating?

Botulinum toxin A injections led with 32.13% hyperhidrosis treatment market share in 2025.

Which region will post the fastest growth in demand for sweat-management solutions?

Asia-Pacific is expected to grow at 6.43% CAGR, helped by Japanese topical launches and wider device adoption.

How long does microwave thermolysis like miraDry typically last?

Dual-frequency miraDry data showed 84% sweat reduction sustained 12 months after a single session.

Why is Sofdra gaining attention among dermatologists?

Sofdra offers topical anticholinergic efficacy with reduced systemic exposure and is available through direct-to-consumer tele-prescribing.

Are home-use devices effective for palmar hyperhidrosis?

Iontophoresis kits such as Dermadry's system achieve dryness for 9-10 days per session, supporting regular but clinic-free management.

Page last updated on: