Ceramic Matrix Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

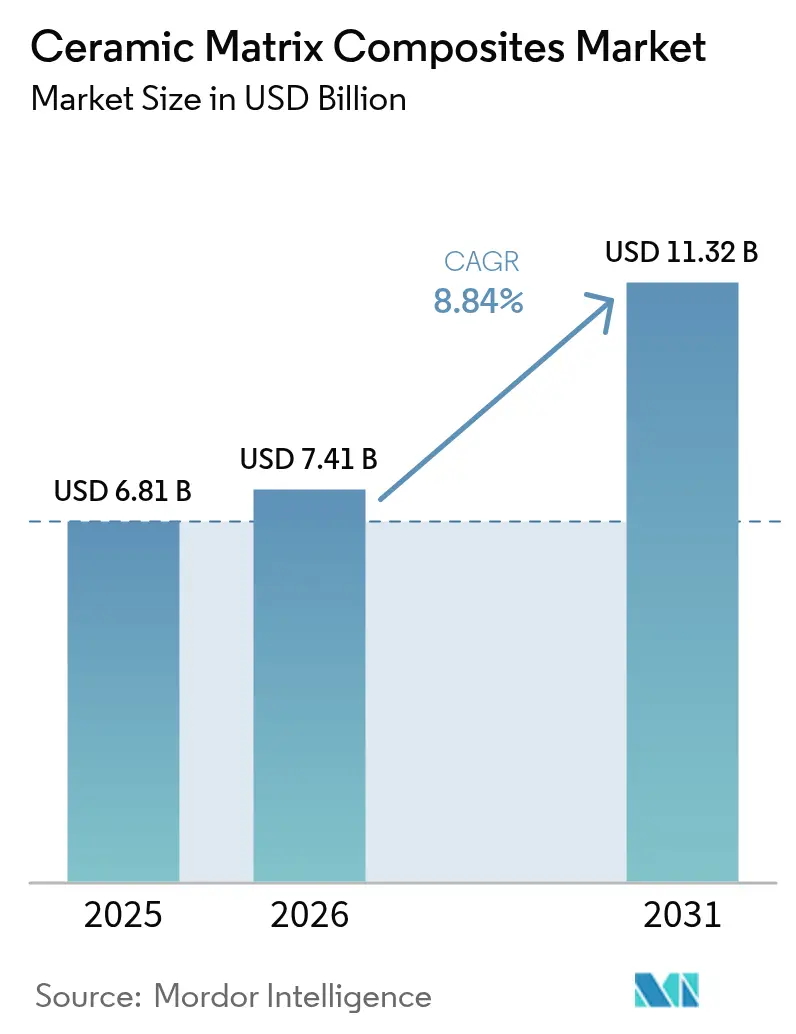

| Market Size (2026) | USD 7.41 Billion |

| Market Size (2031) | USD 11.32 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

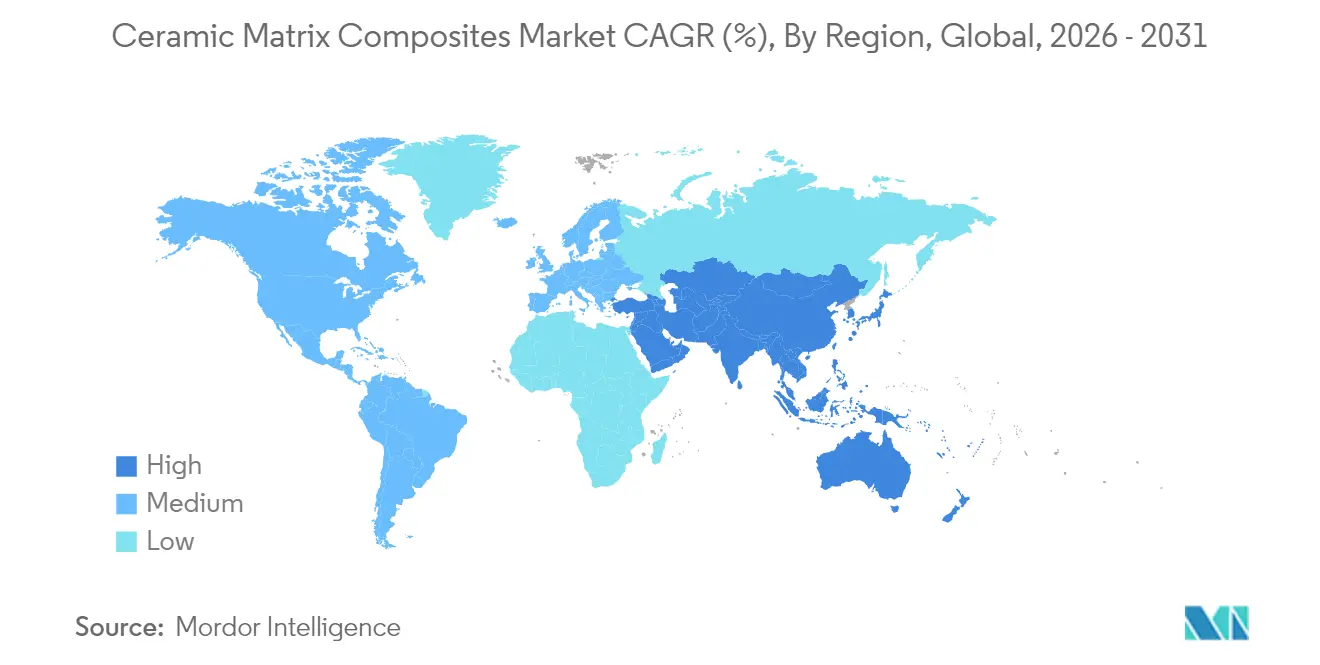

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ceramic Matrix Composites Market Analysis by Mordor Intelligence

Ceramic matrix composites market size in 2026 is estimated at USD 7.41 billion, growing from 2025 value of USD 6.81 billion with 2031 projections showing USD 11.32 billion, growing at 8.84% CAGR over 2026-2031. Expansion rests on the material’s ability to combine the toughness of metals with the heat resistance of ceramics, a balance that unlocks performance gains for aerospace engines, hypersonic systems, and industrial gas turbines. Investment in lightweight propulsion, stricter fuel-burning standards, adoption of variable-fuel turbines, and the search for longer-life high-temperature parts shape the current demand outlook. Cost-down progress in automated fiber placement and reactive melt infiltration is compressing cycle times and closing the cost gap with nickel super-alloys, while government grants for advanced‐materials plants are de-risking capacity additions. A wider set of end users—from chemical processors to fusion-energy developers—now specify CMCs, reflecting a more diversified opportunity mix that supports long-term growth resilience.

Key Report Takeaways

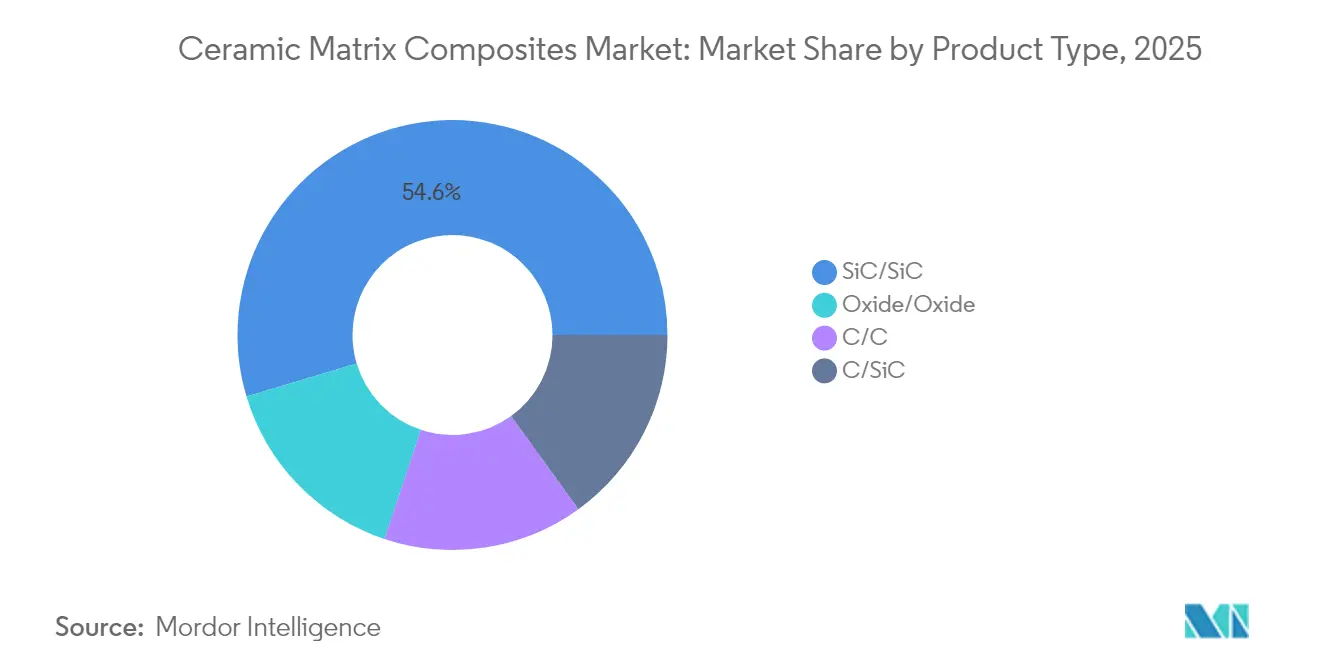

- By product type, SiC/SiC composites led with 54.62% of ceramic matrix composites market share in 2025, and are expected to grow at the fastest CAGR of 10.83% through 2031.

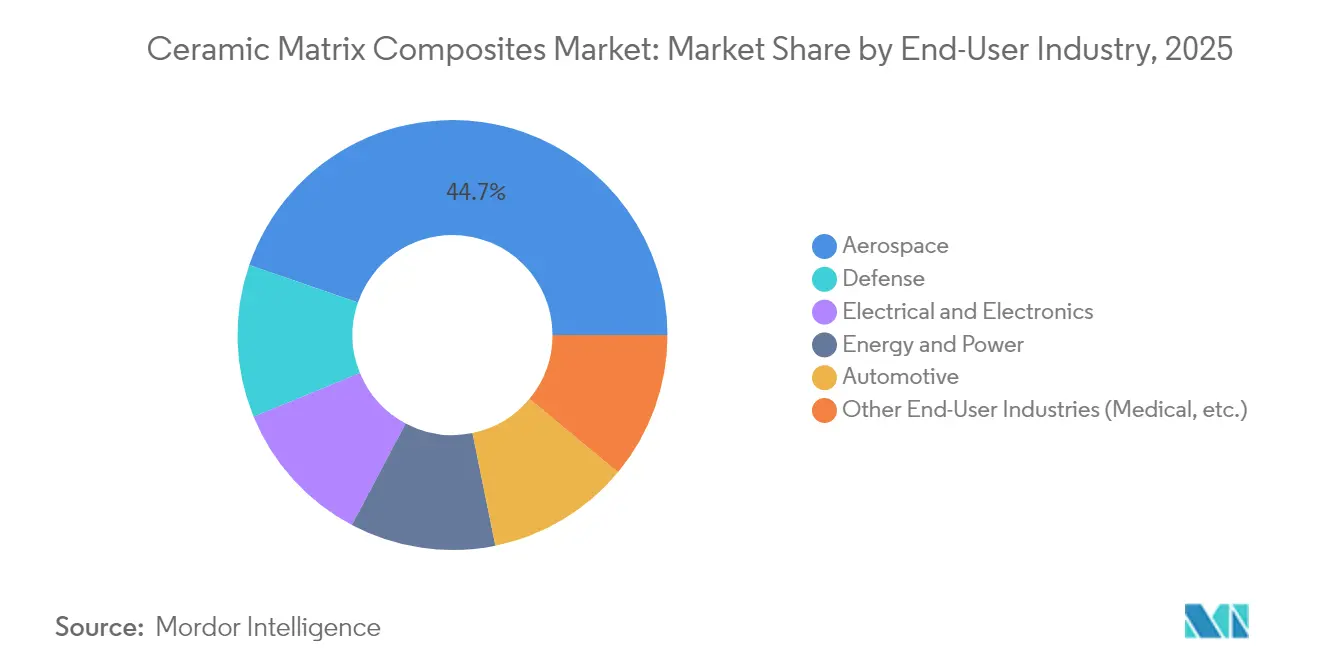

- By end-user industry, aerospace accounted for 44.72% revenue in 2025; defense is the fastest segment, advancing at a 8.91% CAGR through 2031.

- By geography, North America captured 37.55% of the ceramic matrix composites market size in 2025, while Asia-Pacific is forecast to expand at a 10.56% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Ceramic Matrix Composites Market*

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing defense-grade thermal barrier applications | +2.1% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Lightweight vehicle platforms demand | +1.8% | Global, with APAC leading automotive adoption | Long term (≥ 4 years) |

| Growing renewable gas-turbine retrofits | +1.4% | Europe & North America, expanding to APAC | Medium term (2-4 years) |

| Hypersonic vehicle R&D acceleration | +1.2% | North America, Europe, China | Short term (≤ 2 years) |

| Increasing Application of Ceramic Matrix Composites in Defense Sector | +0.9% | Global, led by major defense spenders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Defense-Grade Thermal Barrier Applications

Defense agencies now treat thermal capability as a primary design filter. Hypersonic munitions programs in the United States require materials that remain structurally stable above 2,000 °C, a threshold that eliminates most super-alloys. Lockheed Martin’s test series highlights the need for CMCs in electronics ruggedization and aero-shell protection. The premium prices defense contractors accept for survivability accelerate early CMC qualification, generating learning curves that benefit other sectors. Carbon-fiber reinforced silicon carbide composites have demonstrated reusable performance after multiple high-heat cycles, an advantage that shifts life-cycle cost equations.

Lightweight Vehicle Platforms Demand

Electric and autonomous vehicle programs pursue aggressive mass-reduction targets because every kilogram saved improves driving range and cooling efficiency. Ceramic matrix composites weigh up to 65% less than nickel-based alloys yet retain functional strength at exhaust temperatures. Demonstration ceramic gas turbines in Japan reached thermal efficiencies above 40% while cutting component weight by double-digit percentages[3]M. Kohyama et al., “Advances in SiC Fiber Technology,” sciencedirect.com Source: CompositesWorld Editorial, “SCANCUT Project Cuts CMC Machining Time by 70%,” compositesworld.com . Automotive production volumes push suppliers toward near-net-shape processes such as automated fiber placement that convert hours-long layups into minute-level cycles.

Growing Renewable Gas-Turbine Retrofits

Variable-fuel turbines that balance solar and wind intermittency need hot-section parts capable of rapid load swings and higher firing temperatures. CMC vanes reduce cooling air bleed, translating to a 2–3 percentage point system efficiency gain. Oxide-oxide composites retain strength at 1,100 °C and can reach surface temperatures of 1,300 °C with coatings, making them attractive for combined-cycle plants in Europe’s flexible-grid mandate. The trend broadens the ceramic matrix composites market beyond aerospace, diversifying revenue streams.

Hypersonic Vehicle R&D Acceleration

Mach 5-plus flight tests produce skin temperatures above 1,500 °C and introduce steep thermal gradients. Stratolaunch’s Talon-A2 reusable demonstrator used CMCs for aero-shells that survived multiple sorties, validating performance and refurbishment economics. Ultra-high temperature CMCs based on carbon fiber and zirconium oxycarbide now approach 3,500 °C capability, positioning the material set for scramjet inlets and control surfaces. Government roadmaps identify CMC manufacturing capacity as a dual-use infrastructure priority, unlocking federal funds for pilot lines.

Restraints Impact Analysis of Ceramic Matrix Composites Market*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost vs. super-alloys | -1.9% | Global, most acute in price-sensitive markets | Long term (≥ 4 years) |

| Complex multi-step manufacturing routes | -1.3% | Global, affecting scalability and quality consistency | Medium term (2-4 years) |

| Stricter fibre-dust emission norms | -0.8% | Europe & North America, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost vs. Super-Alloys

CMC parts still cost 3–5 times more than comparable metallic parts due to high-temperature fiber draw and lengthy infiltration steps. The SCANCUT project cut machining time by 70% through novel milling paths, and similar automation breakthroughs are narrowing the gap. Total cost of ownership improves as CMC lifetimes lengthen, but initial acquisition price remains a hurdle for price-sensitive power and automotive users. GE’s USD 200 million Alabama facility targets cost parity at scale geaerospace.

Complex Multi-Step Manufacturing Routes

Chemical vapor and polymer infiltration require days of furnace time, constraining throughput and yield. Integrated with automated tape laying, reactive melt infiltration has proven cycle-time reductions while preserving density. Flash-assisted sintering now achieves 99% dense parts in under 10 minutes, hinting at production paradigms that rival traditional casting. Digital twins and AI-driven controls promise tighter process windows yet need capital and skills to deploy at factory scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Ceramic Matrix Composites Market Segment Analysis

By Product Type:

SiC/SiC Dominance Drives InnovationSiC/SiC composites held 54.62% ceramic matrix composites market share in 2025 and are projected to grow at an 10.83% CAGR to 2031. Integration of finer pitch fibers delivering strengths above 2 GPa has expanded their structural envelope. The ceramic matrix composites market size for SiC/SiC applications is forecast to rise sharply as new jet engine cores qualify shrouds, combustor liners, and nozzle extensions. Carbon/carbon systems maintain niches in rocket nozzles where oxidation can be controlled, and oxide/oxide grades gain traction in industrial heat exchangers that value inherent oxidation stability over peak temperature.

Process advances include nano-engineered interphases that mitigate fiber damage during thermal cycling. Mitsubishi Chemical Group’s carbon-fiber-based C/SiC, qualified for 1,500 °C exposure, shows how hybrid chemistries extend temperature ceilings for space vehicles. The additive deposition of SiC slurry onto woven preforms makes complex cooling passages not feasible with legacy layups. Such innovations maintain the lead of the SiC/SiC family and attract investment from turbine primes.

By End-User Industry:

Aerospace Leadership Meets Defense AccelerationThe aerospace segment generated 44.72% revenue in 2025, benefiting from long-running qualification programs that placed CMC shrouds and nozzles into thousands of commercial engines. The ceramic matrix composites market size for aerospace is expected to expand steadily as new single-aisle platforms enter service with CMC-rich cores. Defense shows the quickest growth at a 8.91% CAGR, propelled by hypersonic glide vehicle and scramjet prototypes that demand ultra-high temperature bodies. The ceramic matrix composites market share of defense remains smaller but climbs each year as programs move from prototype to low-rate initial production.

Industrial gas turbines represent a mid-growth tier as utilities retrofit combined-cycle stations for frequent starts. Automotive volumes remain limited to demonstration exhausts and brake discs, yet the pivot to battery-electric cars makes high-temperature lightweight enclosures desirable for thermal modules. Electrical and electronics users tap the dielectric and thermal-spread qualities of oxide CMCs for power modules where silicon carbide chips operate hotter than legacy silicon parts.

Geography Analysis

North America Ceramic Matrix Composites Market

Due to dense aerospace and defense ecosystems, North America commanded 37.55% of the ceramic matrix composites market revenue in 2025. The region houses vertically integrated supply chains that span SiC fiber draw, component layup, machining, and engine assembly. Government initiatives like the Institute for Advanced Composites Manufacturing Innovation funnel grants toward pilot lines, underpinning local capacity. Rolls-Royce and GE place multi-year orders that smooth demand cycles and justify further plant expansions.

China and Japan Ceramic Matrix Composites Market

Asia-Pacific delivers the fastest 10.56% CAGR through 2031 as China and Japan escalate strategic materials programs. National plans seek supply independence for high-performance fibers, with milestone targets set for 2035. Automotive electrification also stimulates regional demand for lightweight, thermally resilient parts. Lower labor costs and proactive subsidies enable competitive export pricing, positioning the region as a significant consumer and global ceramic matrix composites market supplier.

Europe Ceramic Matrix Composites Market

Europe maintains a steady share through turbine retrofits that support renewable-heavy grids and through new aircraft engine demonstrators such as Rolls-Royce UltraFan. EU research networks pool public and private funds to mature oxide-oxide grades suitable for industrial furnaces, widening application scope. Strict emission regulations create a positive policy environment for efficiency-raising materials like CMCs, reinforcing European demand.

Competitive Landscape

The ceramic matrix composites market is highly fragmented, dominated by aerospace leaders such as General Electric Company, Rolls-Royce, and Safran, which employ proprietary fiber chemistries and infiltration processes. Their forward integration ensures component reliability and accelerates qualification cycles, creating significant entry barriers.

Smaller material specialists focus on industrial and fusion-energy sectors with unique performance requirements. Licensing additive manufacturing patents enables cost-effective production of complex parts, while collaborations like UKAEA’s work on fusion-grade silicon carbide/silicon carbide advance scalable solutions.

Ceramic Matrix Composites Industry Leaders

General Electric Company

Rolls-Royce

Safran

SGL Carbon

CoorsTek Inc.

- *Disclaimer: Major Players sorted in no particular order

Ceramic Matrix Composites Market Companies Covered in this Report

- 3M

- applied thin films inc.

- CeramTec GmbH

- COIC

- CoorsTek Inc.

- General Electric Company

- HTMS Ltd.

- KYOCERA Corporation

- LANCER SYSTEMS

- Mitsubishi Chemical Group Corporation

- Pratt & Whitney

- Rolls-Royce

- Safran

- SGL Carbon

- Starfire Systems Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

Market Opportunities and Future Outlook

Capacity build-outs and deeper vertical integration around silicon-carbide fiber, prepreg/tape, and hot-section component fabrication offer a near-term whitespace for scaling supply, supported by the market base of USD 7.41 billion in 2026 and continued pull from high-volume aero-engine programs. GE Aerospace has put named investments behind this bottleneck, including new Huntsville, Alabama factories focused on silicon carbide fibers and CMC tape, alongside expansion funding for its North Carolina CMC manufacturing footprint. This points to fiber availability, tape conversion, and repeatable part throughput as key constraints for wider adoption in LEAP and GE9X-class platforms.

Defense and extreme-environment R&D are also widening the application map beyond commercial engines, creating entry points for oxide-based and ultra-high-temperature CMC variants, as well as manufacturing routes that reduce cycle time and qualification risk. In the United Kingdom, a government-backed, pilot-scale oxide-oxide CMC manufacturing capability anchored by Cross Manufacturing with support from Dstl, the University of Oxford, and the National Composites Centre highlights an opportunity around sovereign supply chains and defense-grade qualification pathways. Parallel programs such as AeroVironment’s Air Force Research Laboratory CAMP contract and General Atomics Electromagnetic Systems with Oak Ridge National Laboratory reflect ongoing procurement and lab-to-factory partnerships that can translate process advances, including faster infiltration and automation, into producible CMC components for hypersonic and other high-heat aerospace environments.

Recent Industry Developments in Ceramic Matrix Composites Market

- May 2026: GE Aerospace announced a USD 105 million expansion of its ceramic matrix composites manufacturing plants in Asheville and West Jefferson, North Carolina. The added capacity increases output of CMC components used in high-temperature engine sections, supporting supply readiness for programs such as LEAP and GE9X.

- February 2026: GE Aerospace announced a USD 200 million investment to build two new factories in Huntsville, Alabama, dedicated to manufacturing silicon carbide fibers and CMC tape. Bringing fiber and intermediate forms closer to internal component production tightens vertical integration and reduces exposure to upstream supply constraints.

- February 2025: Safran reported ANA Holdings ordered CFM International LEAP engines for Boeing 737 MAX and Airbus A321neo fleets. The order activity supports sustained production of the LEAP engine family, which is a key commercialization pathway for CMC hot-section parts at scale.

Ceramic Matrix Composites Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market is defined as the revenue generated from ceramic matrix composite materials and related intermediate forms sold into end-use manufacturing, where ceramic fibers are embedded in a ceramic matrix to deliver high-temperature mechanical performance.

Scope exclusions: We exclude polymer matrix composites, conventional monolithic ceramics, and R&D-only prototype coupons that are not sold as commercial products.

Segments Covered in This Report

- By Product Type

- C/C

- C/SiC

- Oxide/Oxide

- SiC/SiC

- By End-user Industry

- Automotive

- Aerospace

- Defense

- Energy & Power

- Electrical & Electronics

- Other End-User Industries (Medical, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Turkey

- Russia

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- Nigeria

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base on where CMC demand comes from and how it shifts with aerospace, defense, and industrial activity. We rely on public sources such as USGS materials statistics, the US International Trade Commission trade data, FAA and EASA aviation activity publications, and energy releases from agencies such as the US EIA and IEA, along with selected peer-reviewed materials journals.

Next, we connect those signals to supply-side context using company filings, annual reports, investor presentations, conference slide decks, and reputable industry press coverage. Where needed, we also use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export datasets to cross-check capacity additions and downstream build rates. The specific desk sources named above are illustrative and not exhaustive, and many other public documents were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to sanity-check assumptions that are not fully visible in public documents, including adoption timing, pricing logic, and qualification cycles. We speak with a mix of raw material suppliers, component fabricators, OEM and Tier supplier engineering and sourcing teams, and aftermarket or MRO-linked contacts, covering APAC, EMEA, and the Americas so regional build rates and trade flows are not over-assumed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 45% |

| Mid tier: 43% | Functional/Unit leaders: 38% | EMEA: 30% |

| Smaller Players: 21% | Managers: 48% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up combined logic, where the main total is reconstructed from end-market demand pools and then checked against supply-side signals. For CMCs, the top-down layer uses aircraft production and engine delivery trends, expected CMC content on key platforms, industrial and power turbine build and retrofit activity, and qualification and ramp timelines that influence when volumes show up.

To corroborate and adjust, we run selective bottom-up approximations using sampled average selling prices by product form, channel checks on conversion yields and scrap rates, and roll-ups from a limited set of publicly visible supplier revenue disclosures where product splits are discussed. If a bottom-up datapoint is missing, we apply conservative penetration bands by application and then narrow them using interview feedback on program wins, capacity utilization, and near-term constraints. Forecasts are produced through scenario analysis supported by a light multivariate regression, where sector indicators are used to keep growth aligned with aircraft build rates, defense spending signals, and power generation additions.

Data Validation & Update Cycle

Validation is done in steps so the final outputs do not depend on a single input. We compare the model totals with independent signals such as import and export movement, patenting momentum, disclosed capex and capacity expansions, and implied material intensity from aerospace and turbine build plans.

Outliers are flagged and re-checked, and assumptions that drive big swings, like penetration, yield loss, and pricing steps, are reviewed by a second analyst before sign-off. Reports are refreshed annually, and interim updates are triggered when there are material events such as platform rate changes, capacity expansions, or policy shifts impacting defense and energy. Before delivery, we do a final pass so clients receive an updated view tied to the latest releases and recent interview feedback.

Mordor Intelligence's Ceramic Matrix Composites Cmcs Market Size Compared With Other Published Estimates

It is normal to see different market size values for CMCs because publishers may count different product forms, include different end-use baskets, and choose different base years. Even when the currency is the same, the number can shift if price escalation, yield loss, and the timing of aerospace ramps are treated differently.

The biggest gaps usually come from whether the estimate includes only commercialized CMC material sales or also adds fabricated parts and adjacent high-temperature ceramic value, and from how quickly high-volume engine programs are assumed to ramp. Currency conversion timing and whether the model is updated after major engine rate revisions can also move the result, since demand is concentrated in a few applications that scale unevenly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.81 B (2025) | |

| Global Consultancy A | USD 8.79 B (2025) | This figure appears to use a broader value pool that captures more downstream product value, and it also assumes a faster near-term ramp that lifts the base-year total. |

| Industry Research House B | USD 14.41 B (2024) | The number is materially higher and is likely explained by a wider inclusion set across components and applications, plus a different year basis and pricing uplift that is not tightly tied back to platform-level adoption and yield constraints. |

Overall, the spread in published values is mainly a scope and timing issue, not a simple math mismatch. When only commercial CMC materials and intermediate forms are counted, and aerospace ramp timing is cross-checked against engine deliveries and qualification lead times, the estimate stays closer to observable demand signals, as modeled by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the Ceramic Matrix Composites Market?

The market is worth USD 7.41 billion in 2026 and is forecast to grow to USD 11.32 billion by 2031.

Which segment leads the market by product type?

SiC/SiC composites command 54.62% ceramic matrix composites market share in 2025 and are growing fastest at an 10.83% CAGR.

Which region is expanding most rapidly?

Asia-Pacific is projected to register a 10.56% CAGR through 2031 due to industrialization and government support for advanced materials.

Why are CMCs critical for hypersonic vehicles?

They maintain structural strength above 2,000 °C, resist oxidation, and enable reusable designs required for hypersonic flight profiles.

What remains the biggest barrier to wider adoption?

Production cost remains 3–5 times higher than super-alloys, although new automated routes are narrowing the gap.

Page last updated on: