North America Precision Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

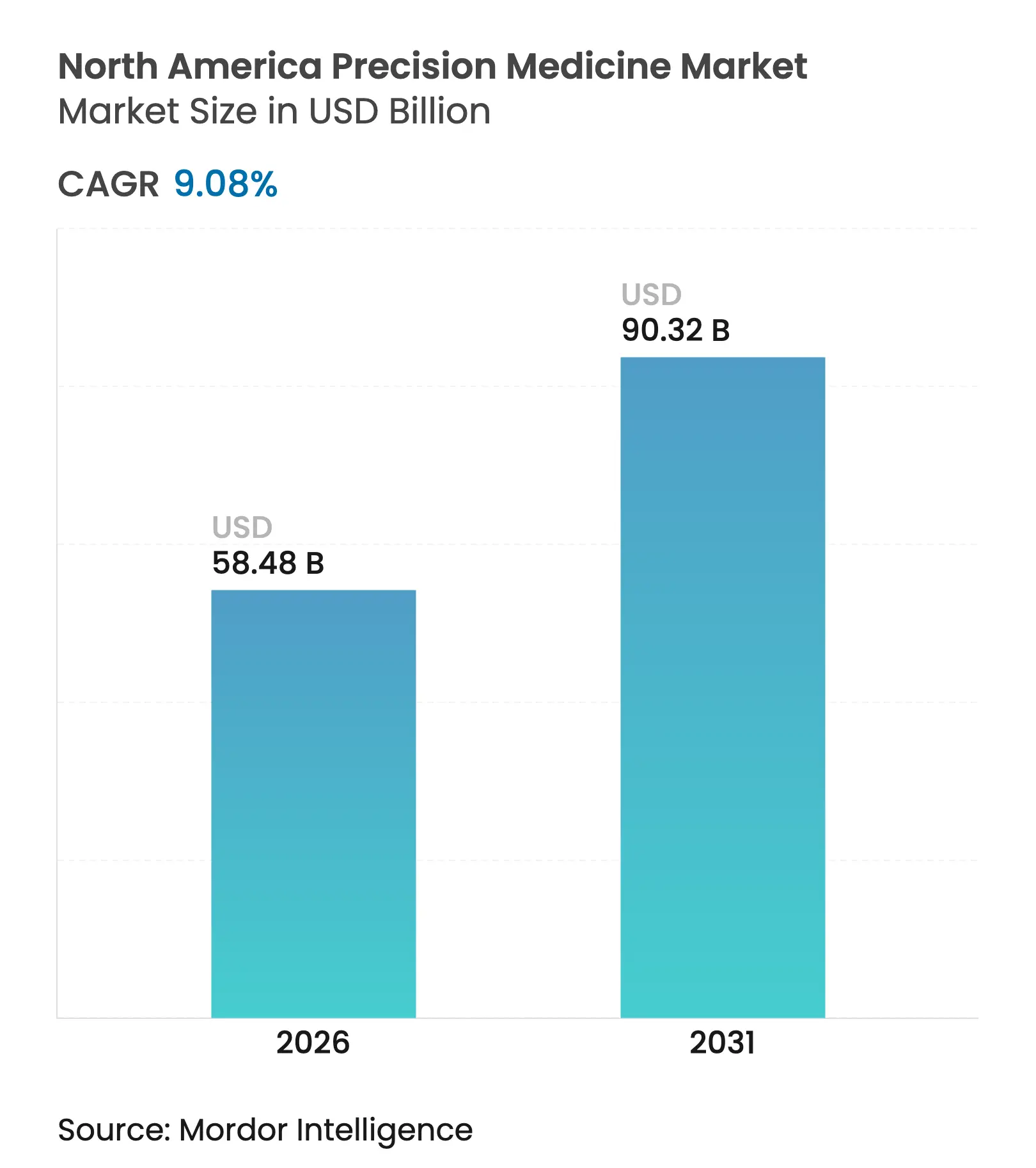

| Market Size (2026) | USD 58.48 Billion |

| Market Size (2031) | USD 90.32 Billion |

| Growth Rate (2026 - 2031) | 9.08 % CAGR |

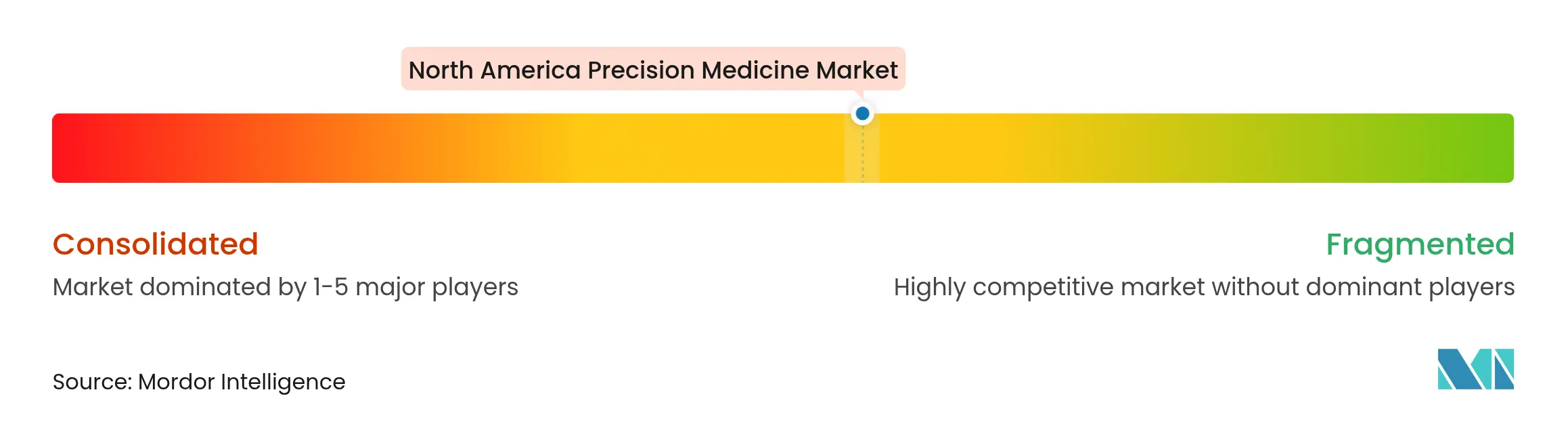

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Precision Medicine Market Analysis by Mordor Intelligence

Declining genome-sequencing costs, government-funded research programs, and fast-evolving AI diagnostics keep the North America precision medicine market on a strong growth trajectory. The Food and Drug Administration’s 2025 accelerated approval of linvoseltamab-gcpt illustrates a regulatory system that keeps pace with precision therapeutics while genomic sequencing costs. Hospitals now embed genomic tests in routine oncology decision-making, and AI-powered digital twins enable physicians to model potential treatment paths before a first drug is prescribed. As a result, data assets, not finished drugs alone, are becoming the strategic currency of the North America precision medicine market, and incumbent firms are racing to secure them.

Key Report Takeaways

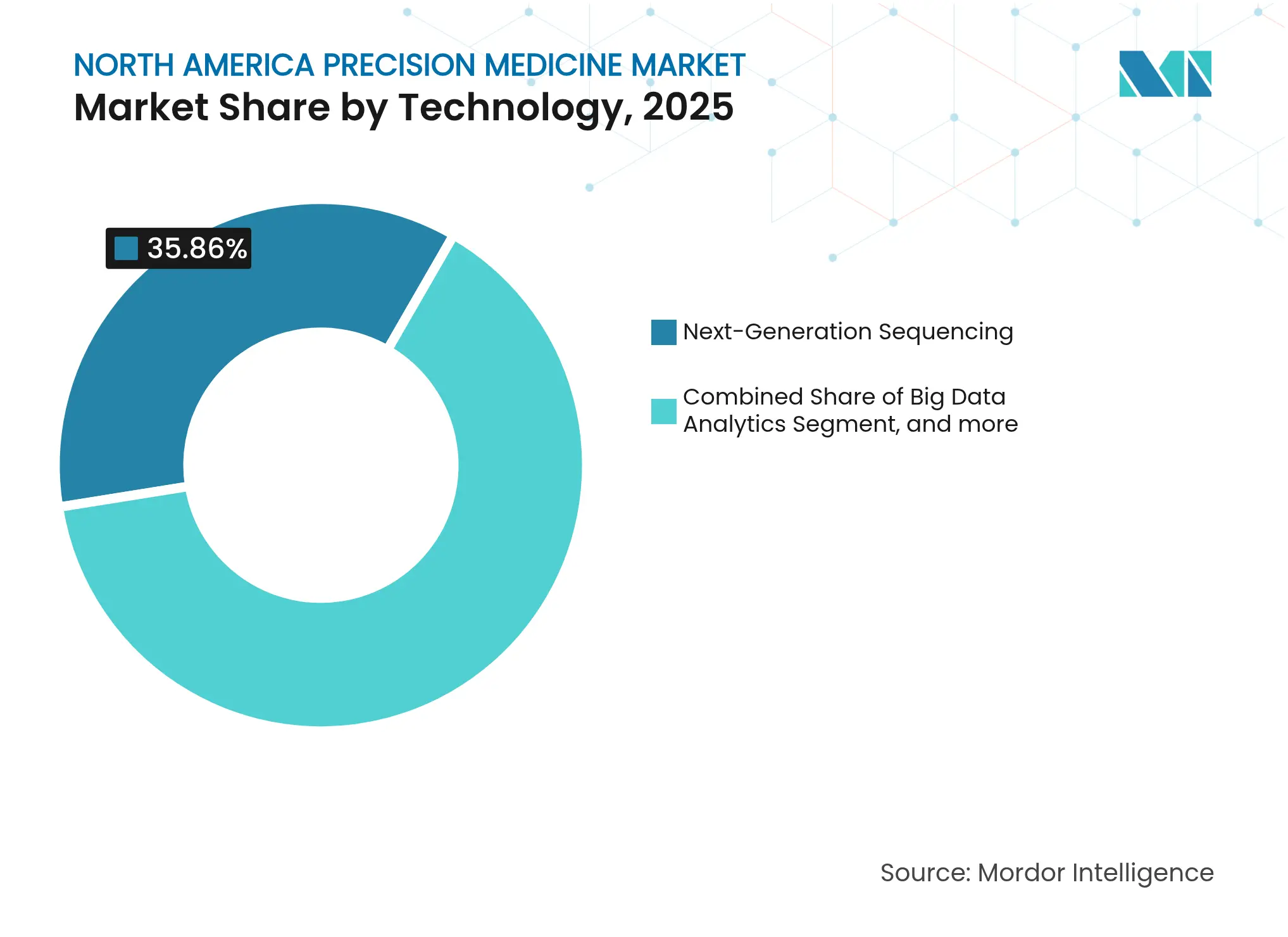

- By technology, next-generation sequencing captured 35.86% of the North America precision medicine market share in 2025 while AI & machine learning is projected to post the fastest 13.29% CAGR through 2031.

- By application, oncology led with 41.02% revenue share in 2025; rare & genetic disorders is forecast to expand at a 15.87% CAGR to 2031.

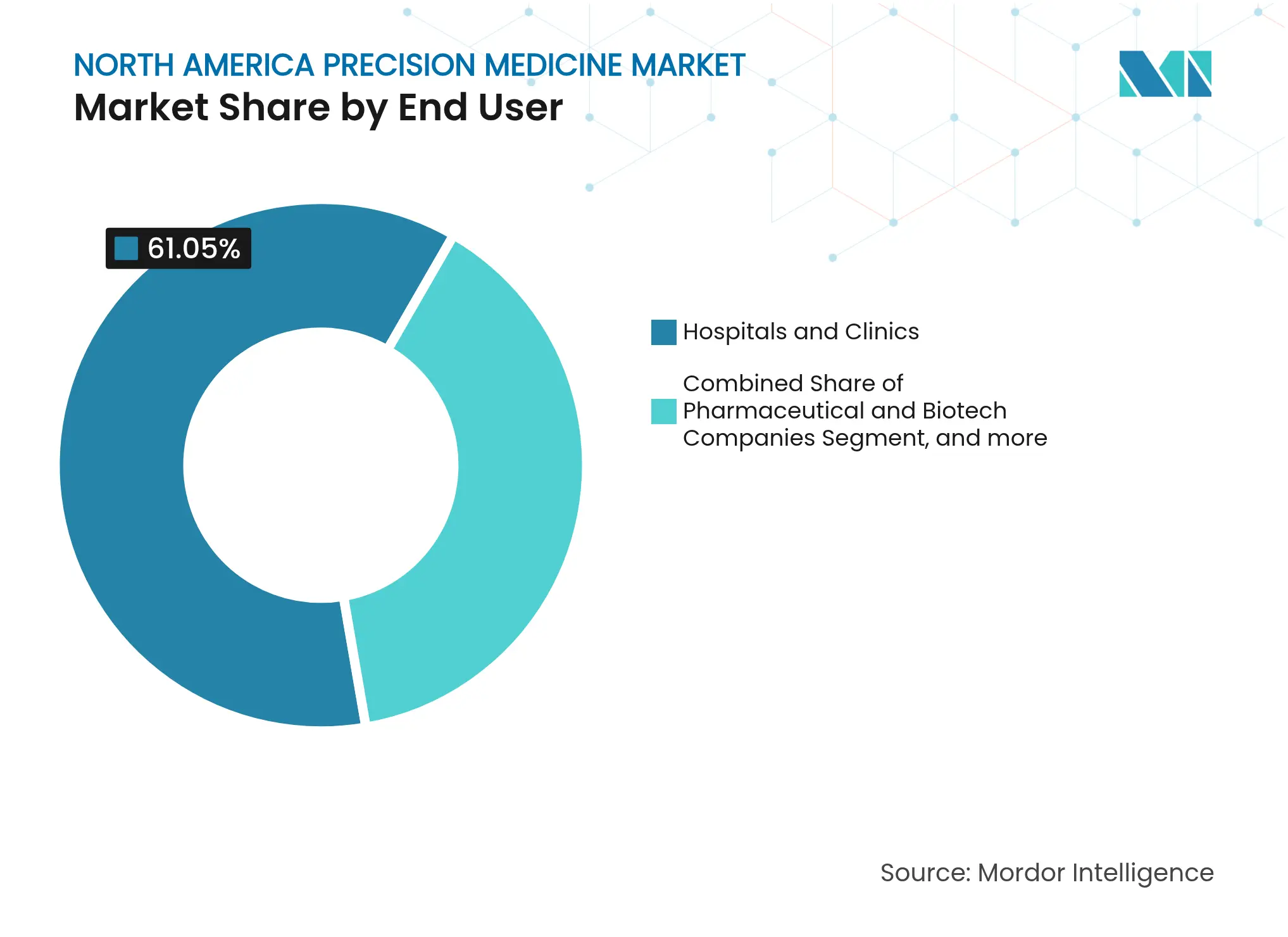

- By end user, hospitals & clinics retained 61.05% share of the North America precision medicine market size in 2025, whereas research & academic institutes record the highest projected 17.67% CAGR through 2031.

- By country, the United States dominated with 84.04% market share in 2025; Mexico is advancing at a 19.35% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Precision Medicine Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Plummeting

cost of next-generation sequencing

Plummeting

cost of next-generation sequencing

| +2.1% | Region-wide | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

+2.1%

|

Geographic

Relevance

:

Region-wide

|

Impact

Timeline

:

Medium term

(2-4 years)

|

Government-led

precision medicine initiatives

Government-led

precision medicine initiatives

| +1.8% | United States, Canada, Mexico | Long term (≥4 years) | |||

Rising

chronic disease burden

Rising

chronic disease burden

| +1.5% | Region-wide | Long term (≥4 years) | |||

AI-driven

digital twin & predictive modeling

AI-driven

digital twin & predictive modeling

| +1.2% | United States, Canada | Short term (≤2 years) | |||

Employer-funded

precision health benefits

Employer-funded

precision health benefits

| +0.9% | United States | Medium term (2-4 years) | |||

Expansion of

multi-omics platforms

Expansion of

multi-omics platforms

| +0.7% | Research centers | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Plummeting Cost of Next-Generation Sequencing (NGS)

NGS price compression remains the most transformative catalyst for the North America precision medicine market. Illumina’s engineering roadmap cut whole-genome sequencing costs to USD 600 in 2024 and industry analysts project USD 100 sequencing rods within two years.[1]Illumina, “Cost Trajectory Statements,” illumina.com Clinical labs deploy these affordable assays for tumor profiling, rare-disease diagnosis, and newborn screening in a single workflow. The FDA’s 2024 clearance of the TruSight Oncology Comprehensive assay signals stable regulatory uptake of broad-panel NGS tests. Roll-to-roll fluidics is poised to push throughput higher while preserving accuracy, removing prior bottlenecks created by batch-flow reactors. Hospitals in large metro areas integrate same-week genomic reporting, shortening time-to-therapy and lowering per-patient inpatient costs. Rural clinics, however, still face infrastructure gaps, so equitable access will depend on decentralized sample-prep kits and cloud pipelines

Government-Led Precision Medicine Initiatives

Federal and provincial programs underpin the long-run demand curve for the North America precision medicine market. The National Institutes of Health All of Us Research Program has released genomic files for 245,388 participants, with nearly half from historically under-represented groups.[2]National Institutes of Health, “PRIMED-AI Funding Opportunity,” nih.gov Canada pledged USD 200 million to a multi-omics data initiative that ties into provincial electronic health records, and Mexico’s MexOMICS Consortium now maintains three national disease registries to guide targeted therapy trials. The FDA’s final rule on laboratory-developed tests creates clearer validation pathways and aligns oversight of hospital-run assays with commercial kits. Industry follows public capital: venture-backed companies focusing on AI companion diagnostics raised USD 3.1 billion across the region in 2024, double the 2023 figure. These network effects accelerate knowledge spillovers, reinforcing a virtuous cycle of research translation and private investment.

Rising Chronic Disease Burden

Chronic diseases lift baseline demand for the North America precision medicine market as payers search for interventions that shift costs from late-stage care to early-stage prevention. Centers for Disease Control and Prevention data show that multiple chronic conditions among U.S. adults climbed from 21.8% in 2013 to 27.1% in 2023.[3]Centers for Disease Control and Prevention, “Multiple Chronic Conditions Trends 2013-2023,” cdc.gov Cardiovascular disease alone is expected to impose USD 1.4 trillion in annual costs by 2050, up from USD 393 billion in 2020. Hypertension prevalence is projected to reach 61.0% of adults by 2050, while diabetes could affect 26.8% of the population, magnifying the economic imperative for individualized risk stratification. Precision polygenic risk scoring supports early lifestyle or pharmacologic interventions, and insurers increasingly reimburse such screens. Younger cohorts now present with multimorbidity sooner, making lifetime preventive genetics even more compelling for employers and payers.

AI-Driven Digital Twin & Predictive Modeling

The convergence of advanced analytics with clinical genomics is accelerating. The NIH’s PRIMED-AI program funds multi-modal AI tools that merge imaging, genomics, and electronic health records to forecast treatment response. FastGlioma, an intraoperative model, detects residual brain tumor tissue in ten seconds with 92% accuracy, guiding surgeons in real time. The FDA’s draft guidance on AI model credibility outlines how sponsors can pre-specify performance monitoring plans so that iterative learning remains compliant. Digital twins now simulate how a patient’s drug metabolism, comorbidities, and social determinants influence outcomes, enabling dose adjustments before adverse events emerge. Health systems deploying such engines report shorter length-of-stay metrics, unlocking capacity without new beds.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of

targeted therapeutics

High cost of

targeted therapeutics

| −1.4% | Region-wide | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

−1.4%

|

Geographic

Relevance

:

Region-wide

|

Impact

Timeline

:

Medium term

(2-4 years)

|

Data privacy

& cybersecurity concerns

Data privacy

& cybersecurity concerns

| −1.1% | United States, Canada | Short term (≤2 years) | |||

Supply-chain

vulnerabilities for sequencing reagents

Supply-chain

vulnerabilities for sequencing reagents

| −0.8% | Region-wide | Short term (≤2 years) | |||

Under-representation

in genomic databases

Under-representation

in genomic databases

| −0.6% | Global, NA focus | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Targeted Therapeutics

Price points for gene and cell therapies remain several orders of magnitude above traditional drugs, hampering broader adoption within the North America precision medicine market. The FDA’s 2024 nod for Kebilidi, a gene therapy for aromatic L-amino acid decarboxylase deficiency, involved list prices beyond USD 4 million per course, straining payer budgets. GSK’s USD 1 billion acquisition of IDRx, whose lead asset serves a tumor population of only 6,000 U.S. patients, underscores the economics that drive high unit costs. Manufacturers justify pricing by citing limited addressable populations and complex viral-vector supply chains, yet payer skepticism persists. Companion diagnostics, genetic counseling, and post-treatment monitoring further raise total cost of care. Until innovative payment models such as outcomes-based annuities scale, high prices will temper growth in some segments.

Data Privacy & Cybersecurity Concerns

Rising cyber-risk dampens consumer willingness to share genomic data. A 2023 breach at 23andMe exposed sensitive ancestral profiles and reignited calls for stricter genomic-privacy statutes. University of Portsmouth researchers demonstrated proof-of-concept attacks against DNA sequencers, showing malicious code can hide inside biological samples that then compromise networked systems. The U.S. National Institute of Standards and Technology updated its Genomic Data Cybersecurity Framework in 2024, recommending zero-trust architectures and fine-grained consent management. Healthcare providers allocate greater capital to encryption and tokenization, but interoperability requirements still mandate data exchange, enlarging the attack surface. Public perception remains fragile; any additional large-scale breach could slow enrollment in ongoing population genomics drives.

Segment Analysis

By Technology: NGS Infrastructure Dominates While AI Accelerates

Next-generation sequencing (NGS) held 35.86% of the North America precision medicine market share in 2025, underscoring its status as the backbone of most clinical workflows. Several hundred U.S. hospitals now keep benchtop sequencers in-house, pushing volumes high enough that reagent bulk contracts drive per-sample costs down. The North America precision medicine market size for NGS services is projected to climb at a steady 7.86% CAGR through 2031 as coverage expands into infectious-disease surveillance and newborn screening. Illumina’s platform refreshes and Thermo Fisher’s commercialization of on-board informatics both lower tech-staff requirements, widening the customer base.

Artificial intelligence and machine learning posted the fastest 13.29% CAGR, a pace that could lift its revenue contribution from single digits today to double-digits by the end of the decade. Hospitals increasingly integrate AI triage into molecular tumor boards, where predictive analytics recommend therapy sequences and flag clinical-trial eligibility. Start-ups occupy niches such as single-cell data interpretation, while cloud giants supply elastic compute for whole-genome pipelines. Together, hybrid solutions blur the line between sequencing hardware and software value creation, positioning AI as the natural overlay on NGS datasets.

Note: Segment shares of all individual segments available upon report purchase

By Application: Oncology Leadership Faces Rare-Disease Acceleration

Oncology accounted for 41.02% of North America precision medicine market revenue in 2025 and benefits from a robust regulatory environment that routinely approves biomarker-driven therapeutics. Companion diagnostic reimbursement is now standard for lung, breast, and colorectal cancers, leading to routine testing of actionable variants at first diagnosis. Meanwhile, immuno-oncology combinations leverage patient-specific neoantigen profiles, and AI pathology peppers clinical trials with adaptive end-points.

The rare & genetic disorder segment is expanding at 15.87% CAGR, the fastest among all applications. Orphan-drug incentives, CRISPR-based in-vivo editing, and newborn screening mandates combine to create rapid pipelines even for ultra-small populations. Public-private consortia fund registry harmonization so that R&D teams can achieve statistical power without multi-year recruitment cycles. As sequencing costs continue to fall, clinicians anticipate standard inclusion of rare-disease panels in pediatric care, a dynamic that elevates both testing volumes and therapeutic demand.

By End User: Academic Research Institutes Drive Innovation

Research & academic institutes exhibit an 17.67% CAGR as universities pivot from discovery science toward translational programs that partner directly with health systems. Grants flow toward platform technologies that shorten the bench-to-bedside interval, such as rapid functional-genomics screens and population-based biobanks. These institutes also anchor graduate training that feeds scarce bioinformatics talent into the labor market.

Hospitals & clinics retained a dominant 61.05% share of 2025 revenue, reflecting their control of patient pipelines and reimbursement relationships. Many deploy hybrid operating models: in-house testing for high-volume assays and send-outs for complex panels. Integrated delivery networks use combined electronic medical records and genomic repositories to automate clinical-decision support alerts. As they adopt AI triage, data governance and shared infrastructure with academic partners grow tighter, smoothing translation of research findings into routine care.

Note: Segment shares of all individual segments available upon report purchase

By Country: Mexico Emerges as High-Growth Market

The United States contributed 84.04% of North America precision medicine market revenue in 2025, anchored by large payer budgets, deep capital markets, and an established FDA framework. Federal contracts such as the NIH All of Us Biobank shield U.S. sequencing demand from cyclical reimbursement changes.

Mexico, while starting from a smaller base, is set to expand at 19.35% CAGR. Incentives in the 2025-2030 National Development Plan allocate public funds to genomic infrastructure, and Bayer’s USD 55 million plant expansion in Lerma targets regional supply of precision-manufactured biologics. The MexOMICS registries now provide local reference genomes that improve assay sensitivity for admixed populations. Cross-border collaborations with Texas-based institutions further accelerate technology transfer and workforce training.

Canada maintains steady growth as federal and provincial agencies co-finance nationwide multi-omics projects. A USD 200 million genomics data platform interlinks with provincial health-record systems, facilitating real-world evidence studies that resonate with regulators and payers.

Geography Analysis

The United States dominates the landscape through well-defined reimbursement pathways, mature clinical-trial infrastructure, and the world’s largest installed base of high-throughput sequencers. The All of Us Research Program, with data from 245,388 sequenced participants, consistently supplies diverse reference genomes that inform both academic research and commercial drug discovery. The FDA’s 2024 rule governing AI-enabled device software functions further clarifies oversight, enabling sponsors to launch adaptive algorithms with predetermined change-control plans. Rising chronic disease prevalence particularly cardiovascular disease, projected to cost USD 1.4 trillion annually by 2050 creates a policy mandate for early diagnosis and tailored intervention.

Canada leverages universal healthcare and coordinated provincial programs to execute large-scale multi-omics pilots. The federal USD 200 million Genome Canada initiative finances data infrastructures that permit inter-provincial sharing while honoring stringent privacy rules. British Columbia invested USD 6 million in eight genomics projects spanning cancer and infectious diseases, demonstrating how provinces align research investment with population-health priorities. Indigenous and remote communities remain a focus area for inclusion so that variant catalogues reflect Canada’s full demographic profile.

Mexico is evolving into a regional innovation hub. The MexOMICS Consortium’s three databases TwinsMX, LupusRGMX, and MEX-PD deliver foundational variant catalogs tailored to local genetic structure. The government supports CRISPR research for hemophilia B therapy through the National Institute of Health Security, marking its entrance into advanced gene-editing trials. Shoring up laboratory accreditation and data-exchange standards will be crucial to sustain momentum and ensure cross-border interoperability with U.S. and Canadian collaborators.

Competitive Landscape

Market Concentration

The North America precision medicine market presents moderate concentration. Illumina, Thermo Fisher, and Oxford Nanopore supply most sequencing hardware, while Roche, Pfizer, and Novartis drive large-scale companion-diagnostic portfolios. Consolidation is accelerating; Regeneron acquired 23andMe’s 15 million-customer genetic database for USD 256 million to enrich target-discovery algorithms. GSK spent USD 1 billion on IDRx to secure a late-stage targeted oncology candidate targeting a niche tumor population. Illumina’s partnership with Tempus AI indicates that incumbents no longer view analytics upstarts as peripheral but as essential to platform extension into cardiology and neurology.

Emerging firms specialize in software layers atop commodity sequencing. Mursla Bio focuses on organ-specific extracellular vesicle profiling and claims liver-cancer detection sensitivities exceeding 90% in early trials. Recursion and Exscientia merged to form an AI-enabled drug-discovery entity that pairs high-content imaging with generative chemistry, compressing lead-identification timelines. Supply-chain resilience is now a competitive differentiator; 75% of life-sciences executives polled by industry groups plan continued digitization and dual-sourcing, a shift that favors vertically integrated firms able to guarantee reagent continuity.

Regulatory technology compliance shapes rivalry. Firms with mature quality-management systems can deploy real-time learning algorithms without repeated FDA pre-market submissions, providing a speed advantage. Data assets determine bargaining power; genomic repositories exceeding one million linked health records enable in-silico trial simulations, lowering R&D risk. Consequently, partnerships that combine data lakes with AI toolkits are expected to proliferate over the next five years.

North America Precision Medicine Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mursla Bio launched an AI Precision Medicine Platform built on organ-specific extracellular vesicle isolation from blood, achieving high sensitivity and specificity for early-stage liver cancer detection through its EvoLiver program while expanding applications to cardiometabolic and neurological conditions.

- April 2025: Illumina and Tempus AI announced a strategic partnership to drive genomic testing beyond cancer applications, leveraging Tempus's multimodal data and Illumina's sequencing technologies to standardize molecular testing across cardiology, neurology, and other medical fields.

- May 2024: OM1 launched three new products: OM1 Orion, OM1 Lyra, and OM1 Polaris, all utilizing the PhenOMTM platform. This advanced artificial intelligence-powered digital phenotyping platform is designed to enhance personalized medicine and clinical research.

- March 2024: Mirador Therapeutics launched following a successful funding round exceeding USD 400 million from prominent life sciences investors. The firm aims to advance precision therapies targeting immune-mediated inflammatory and fibrotic conditions.

Table of Contents for North America Precision Medicine Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Plummeting Cost of Next-Generation Sequencing (NGS)

- 4.2.2Government-Led Precision Medicine Initiatives

- 4.2.3Rising Chronic Disease Burden

- 4.2.4AI-Driven Digital Twin & Predictive Modeling

- 4.2.5Employer-Funded Precision Health Benefits

- 4.2.6Expansion of Multi-Omics Platforms

- 4.3Market Restraints

- 4.3.1High Cost of Targeted Therapeutics

- 4.3.2Data Privacy & Cybersecurity Concerns

- 4.3.3Supply Chain Vulnerabilities for Sequencing Reagents

- 4.3.4Under-Representation in Genomic Databases

- 4.4Porter’s Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers/Consumers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitute Products

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Technology

- 5.1.1Big Data Analytics

- 5.1.2Bioinformatics

- 5.1.3Next-Generation Sequencing (NGS)

- 5.1.4AI & Machine Learning

- 5.1.5Companion Diagnostics

- 5.1.6Genomics

- 5.1.7Proteomics

- 5.1.8Metabolomics

- 5.1.9Epigenomics

- 5.1.10Transcriptomics

- 5.2By Application

- 5.2.1Oncology

- 5.2.2Central Nervous System (CNS)

- 5.2.3Immunology

- 5.2.4Cardiovascular

- 5.2.5Respiratory

- 5.2.6Rare & Genetic Disorders

- 5.2.7Other Application

- 5.3By End User

- 5.3.1Pharmaceutical & Biotech Companies

- 5.3.2Hospitals & Clinics

- 5.3.3Diagnostic & Clinical Laboratories

- 5.3.4Research & Academic Institutes

- 5.3.5Other End Users

- 5.4By Country

- 5.4.1United States

- 5.4.2Canada

- 5.4.3Mexico

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1F. Hoffmann-La Roche Ltd.

- 6.3.2Illumina Inc.

- 6.3.3Thermo Fisher Scientific Inc.

- 6.3.4AstraZeneca

- 6.3.5Pfizer Inc.

- 6.3.6Bristol-Myers Squibb

- 6.3.7Biogen Inc.

- 6.3.8Novartis AG

- 6.3.9Medtronic

- 6.3.10Qiagen N.V.

- 6.3.11Quest Diagnostics Inc.

- 6.3.12Laboratory Corporation of America Holdings

- 6.3.13Myriad Genetics Inc.

- 6.3.14Exact Sciences Corp.

- 6.3.15Guardant Health Inc.

- 6.3.1623andMe Holding Co.

- 6.3.17Astarte Medical

- 6.3.18Agilent Technologies Inc.

- 6.3.19Abbott Laboratories

- 6.3.20Foundation Medicine Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

North America Precision Medicine Market Report Scope

As per the scope of the report, precision medicine, a combination of molecular biology techniques and system biology, is an emerging approach to disease treatment and prevention.

The North America precision medicine market is segmented by technology, application, and geography. The technology segment is further divided into big data analytics, bioinformatics, gene sequencing, drug discovery, companion diagnostics, and other technologies. The other technology segment includes nanotechnology and lab-on-a-chip technology, among others. The application segment is further segmented into oncology, CNS, immunology, respiratory, and other applications. The other applications include cardiovascular diseases and rare diseases, among others. The geography segment is further divided into the United States, Canada, and Mexico. The report offers the value (in USD) for the above segments.