Photoresist Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

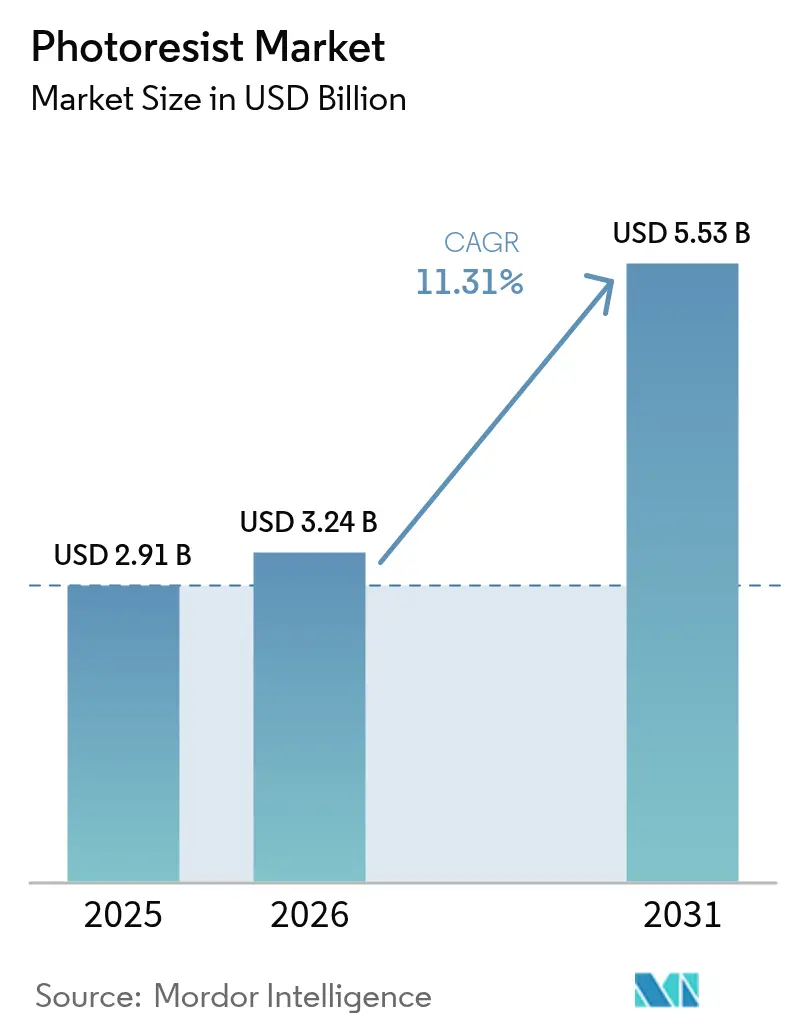

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 5.53 Billion |

| Growth Rate (2026 - 2031) | 11.31% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photoresist Market Analysis by Mordor Intelligence

The Photoresist Market size is projected to be USD 2.91 billion in 2025, USD 3.24 billion in 2026, and reach USD 5.53 billion by 2031, growing at a CAGR of 11.31% from 2026 to 2031. Structural shifts underway in semiconductor manufacturing are amplifying demand: extreme-ultraviolet (EUV) lithography is moving from pilot lines to high-volume production, and government-backed fab-localization programs are redrawing supply chains for critical materials such as photoresist. Mature 193-nanometer ArF immersion formulations continue to anchor the cost-optimized nodes used in automotive microcontrollers, but next-generation metal-oxide dry resists are now essential at sub-5-nanometer logic, where photon shot noise and line-edge roughness threaten yield. Supply resilience considerations have also intensified as the U.S. and EU CHIPS Acts channel a significant amount into local wafer-fabrication capacity, compelling resist suppliers to duplicate blending and quality-assurance assets within North America and Europe.

Key Report Takeaways

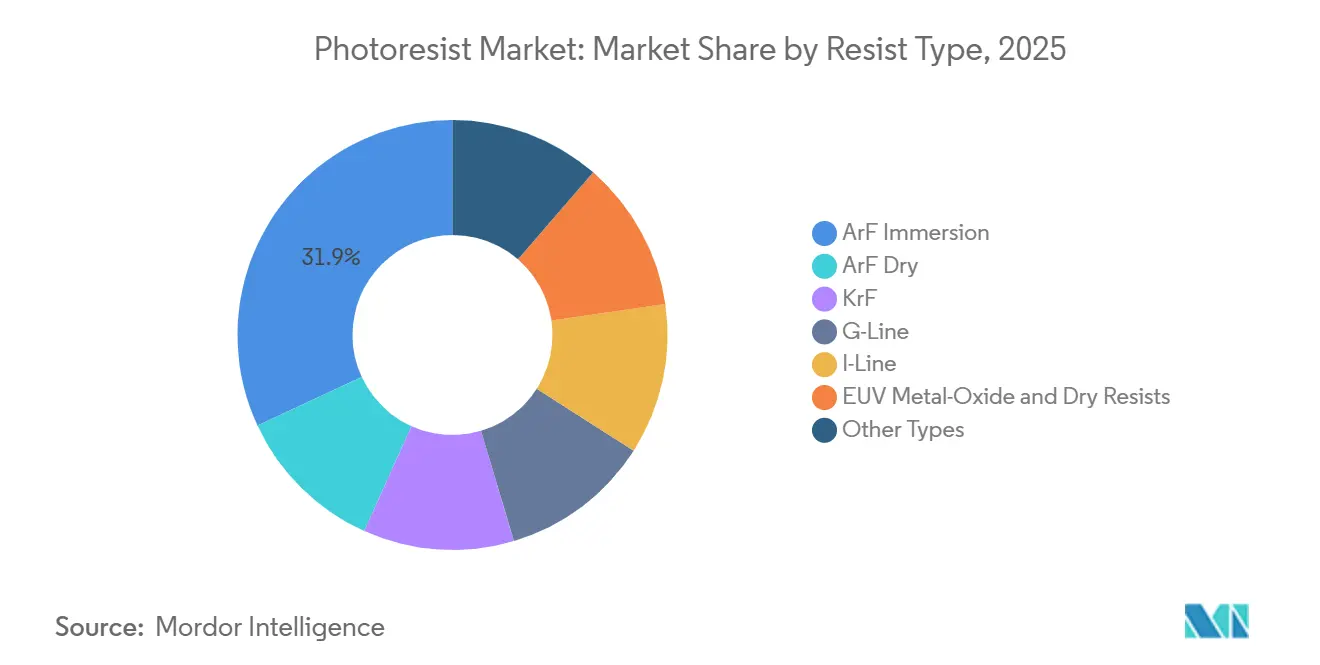

- By resist type, ArF immersion held 31.92% of the Photoresist market share in 2025, whereas EUV metal-oxide and dry resists are projected to expand at a 12.94% CAGR through 2031.

- By tone, positive resists commanded 71.51% revenue share in 2025; negative resists post the fastest 11.38% CAGR to 2031.

- By application, semiconductors and ICs accounted for 54.77% of the Photoresist market size in 2025, while advanced packaging is set to grow at a 11.95% CAGR through 2031.

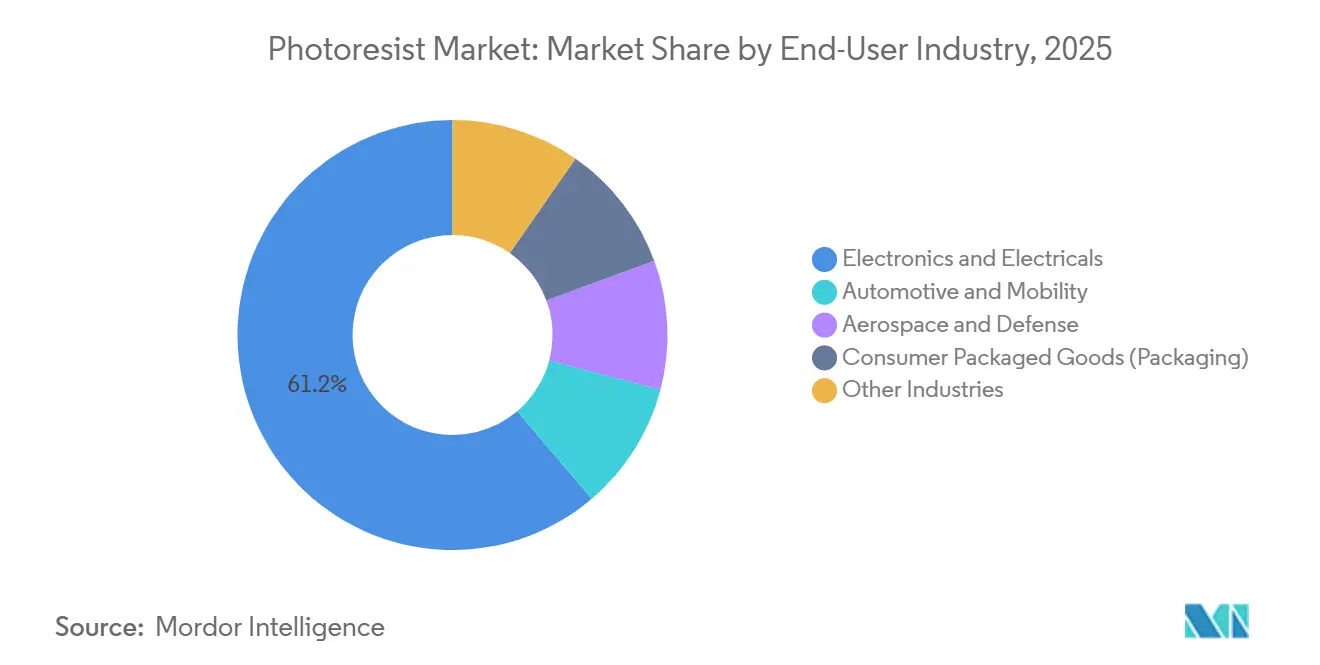

- By end-user industry, electronics and electricals accounted for 61.22% of the market size in 2025, while automotive and mobility are set to grow with the fastest CAGR of 11.86% through 2031.

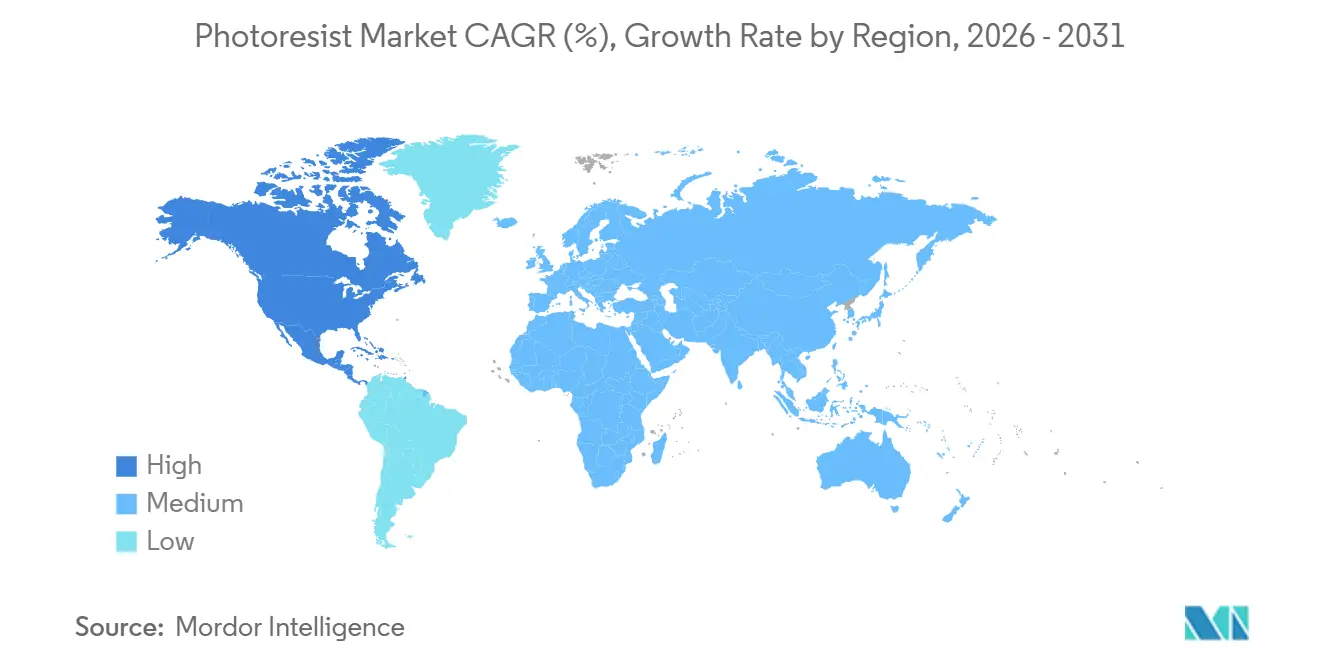

- By geography, the Asia-Pacific held the largest share of 72.34% of the market in 2025. However, North America is expected to witness the fastest growth at a CAGR of 11.49% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photoresist Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from semiconductor and AI accelerators | +3.2% | Global, with APAC core and North America acceleration | Medium term (2-4 years) |

| Accelerated EUV lithography adoption and High-NA roadmap | +2.8% | APAC (Taiwan, South Korea), North America (Intel fabs), Europe (IMEC pilot lines) | Long term (≥ 4 years) |

| 5G/IoT proliferation expanding wafer starts | +1.9% | Global, with APAC manufacturing concentration | Medium term (2-4 years) |

| Government fab-incentive programs (US/EU Chips Acts) | +2.4% | North America, Europe, with supply-chain spillover to APAC | Long term (≥ 4 years) |

| Metal-oxide dry-deposited resists boosting EUV throughput | +1.0% | APAC leading-edge fabs, North America pilot lines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Semiconductor and AI Accelerators

Worldwide capital expenditure on wafer-fabrication equipment is slated to rise between 2026 and 2028, reflecting heavier AI-accelerator requirements in hyperscale data centers[1]Semi, “Global Fab Equipment Spending Outlook 2026,” semi.org. Alphabet doubled its outlays for tensor-processing units in 2025, raising overlay-tolerance specifications that directly increase photoresist consumption per wafer. Intel’s Lunar Lake processors integrate on-package memory using through-silicon vias, adding specialized redistribution-layer lithography steps that further drive resist intensity. Because advanced chiplet architectures raise the number of masking passes, resist demand is decoupling from smartphone unit cycles, sustaining growth even as handset shipments level off. TSMC locked in multiyear EUV-resist supply agreements for its Arizona fab two years before ramp to guarantee chemistry availability, underscoring the material’s strategic role.

Accelerated EUV Lithography Adoption and High-NA Roadmap

In 2024, ASML rolled out its inaugural 0.55 numerical-aperture High-NA EUV scanner, an innovation that facilitates 8-nanometer half-pitch patterning, sidestepping the expenses of multi-patterning. Intel has pledged allegiance to High-NA for its 18-angstrom node, while Samsung and TSMC eye sub-3-nanometer integration post-2027. High-NA optics grapple with absorption coefficients exceeding 10 µm-¹ at 13.5 nm. This is a challenge zone, as traditional chemically-amplified compositions falter with line-edge roughness. While metal-oxide alternatives, derived from tin-oxo clusters, satisfy absorption criteria, they bring forth stochastic defects. This challenge has spurred a collaborative effort between JSR and Lam Research, aiming to reduce defect density. Their co-optimization strategy forges a closer bond between resist suppliers and tool manufacturers, setting a higher barrier for industry newcomers.

5G/IoT Proliferation Expanding Wafer Starts

Global wafer starts tied to 5G radios and IoT sensors continue to swell as network operators densify small-cell footprints and enterprises instrument factories and logistics assets. KrF and ArF dry resists remain vital here because analog front-ends and microcontrollers sit on cost-sensitive 90- to 28-nanometer nodes that must balance die size and RF performance. Incremental volume from these devices cushions fabs against advanced-node cyclicality. As IoT deployments move from proof-of-concept to scale, the cumulative masking layers surge, extending demand momentum into the medium term.

Government Fab-Incentive Programs (US/EU CHIPS Acts)

Under the U.S. CHIPS and Science Act, TSMC received funding, Intel got funding, Samsung was awarded funding, and Micron secured funding, all while backing private investments. Meanwhile, Europe, through its Chips Act, mobilized funding, designating funding for Intel's project in Magdeburg and funding for a joint fabrication facility by STMicroelectronics and GlobalFoundries. The terms of these subsidies emphasize local material content. As a result, Tokyo Ohka Kogyo established a technical center in Oregon, and Merck KGaA expanded its campus in Arizona. Such developments disrupt the previously Asia-dominated resist supply chain, introducing regional bottlenecks and complicating qualification processes.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent HSE rules on solvents and photo-acid generators | -0.9% | Global, with EU REACH and U.S. EPA enforcement leading, spillover to APAC manufacturing | Short term (≤ 2 years) |

| Supply-chain concentration and export-control exposure | -0.7% | APAC supply base (Japan, South Korea), North America and EU demand centers, China isolated markets | Medium term (2-4 years) |

| Yield risk from stochastic defects in sub-10 nm patterning | -0.8% | APAC leading-edge fabs (Taiwan, South Korea), North America High-NA pilot lines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent HSE Rules on Solvents and Photo-Acid Generators

The U.S. EPA classified several PFAS solvent families as hazardous in 2024, mandating costly abatement or substitution at resist-blending plants within two years[2]U.S. Environmental Protection Agency, “PFAS Final Rule 2024,” epa.gov. The EU added triphenylsulfonium salts to its REACH authorization list in 2025, imposing sunset dates that accelerate reformulation campaigns and tilt research and development budgets away from high-performance chemistry toward compliance work[3]European Chemicals Agency, “Candidate List Update 2025,” echa.europa.eu. Tokyo Ohka Kogyo disclosed that a significant amount of its 2025 research and development spend was consumed by solvent reformulations, reinforcing a trend where only the largest suppliers can carry simultaneous compliance and node-transition programs. Industry lobbying secured a five-year carve-out for EUV resists, yet environmental-advocacy lawsuits threaten to shorten the grace period, injecting regulatory uncertainty into capacity-planning models.

Supply-Chain Concentration and Export-Control Exposure

Japan's top suppliers dominate ArF and EUV chemistries. This geographic monopoly came to light in 2024 when the U.S. added specific precursors to its Entity List, halting shipments to Chinese fabs operating at 14-nanometer and smaller. In response, China rolled out subsidies for local producers like Jiangsu Nata. However, these domestic materials lag behind their Japanese counterparts in terms of defect density. Now, fabs face a dilemma: they can either dual-source, incurring extra metrology and inventory costs, or shift procurement closer to U.S. or EU lines to tap into available incentives. Resist vendors are at a crossroads: they can either establish manufacturing in multiple regions or lose market share in areas where export regulations render supply unfeasible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resist Type: Metal-Oxide Chemistries Redefine EUV Economics

ArF immersion held 31.92% of the photoresist market share in 2025, while EUV metal-oxide and dry resists are forecast to expand at a 12.94% CAGR, capturing incremental photoresist market size from sub-5-nanometer logic nodes.

Chemically amplified ArF immersion remains the price-performance leader for 28- to 7-nanometer automotive and connectivity chips, delivering solid yields on fully-depreciated scanners. KrF, g-line, and i-line formulations persist in analog and MEMS lines, buffering suppliers against EUV-cycle volatility. Conversely, tin- and hafnium-based metal-oxide systems enable the High-NA EUV roadmap with 2-nm line-edge roughness performance, albeit at higher exposure dose and cost. Toolmakers and chemistry suppliers are co-designing deposition-etch sequences that promise to cut cycle time, which, if realized at scale, could swing total cost of ownership toward metal-oxide in the outer years of the forecast.

By Tone: Negative Resists Gain in Double-Patterning Schemes

Positive-tone chemistries commanded 71.51% share in 2025, yet negative-tone resists are climbing at an 11.38% CAGR, driven by their robustness in self-aligned double-patterning and EUV contact layers.

Advanced packaging flows favor the thicker films and aqueous developers of positive-tone materials, but sub-7-nanometer logic increasingly uses negative-tone for via layers that would otherwise collapse under rinse stress. Suppliers are releasing switchable-tone hybrids that toggle through bake-temperature adjustments, allowing fabs to maintain a single base chemistry across multiple layers and dilute qualification overhead, thereby augmenting photoresist market size gains from tone diversification.

By Application: Advanced Packaging Outpaces Logic and Memory

Semiconductors and ICs held a 54.77% share, yet advanced packaging is advancing at an 11.95% CAGR, underscoring a pivot from pure scaling to heterogeneous integration.

Fan-out wafer-level packaging and chip-on-wafer stacks use 2-µm redistribution lines that require triple masking passes compared with wire-bond flows. TSMC’s CoWoS platform and Intel’s Foveros 3D stacking both hike resist layers per finished device, inflating photoresist market size beyond what front-end volume alone would imply. Flat-panel displays and printed-circuit boards remain mid-teen contributors, while MEMS, sensors, and photomasks offer niche but fast-evolving formulation requirements that diversify supplier revenue.

By End-User Industry: Automotive Electrification Accelerates Chip Intensity

Electronics and electricals accounted for 61.22% of demand in 2025, although automotive and mobility are forecast to log an 11.86% CAGR through 2031 as vehicle semiconductor content climbs.

Powertrain electrification and driver-assistance radars rely on 180- to 28-nm nodes that remain on mature exposure tools but add masking layers for redundancy and safety. Infineon reported record automotive revenue in 2025, citing thick-film trench resists for silicon-carbide MOSFETs as a growth vector. Aerospace and defense, though smaller, commands high margins for radiation-tolerant resists, while emerging smart-packaging labels point to future thin-film opportunities.

Geography Analysis

Asia-Pacific captured 72.34% of the photoresist market in 2025. This dominance is largely attributed to Taiwanese and South Korean fabs, which handle the majority of the world's leading-edge wafers. Meanwhile, North America is set to increase its foothold, with an 11.49% CAGR. Thanks to the CHIPS Act, projects in Arizona, Ohio, and Texas are on track to contribute significantly to the global 2- to 5-nm capacity by 2028. This surge is prompting suppliers to establish blending lines closer to their customers.

Europe is experiencing moderate growth, driven by Intel's investment in Magdeburg and a joint venture between STMicroelectronics and GlobalFoundries in France. However, Europe still relies on imports for its EUV resists. China faces challenges due to export controls on advanced photoresists. As a countermeasure, it's aggressively expanding its 28-nm capacity and is heavily investing in ArF dry and KrF chemistries. Yet, the nation grapples with developing its domestic High-NA capability.

India and the Middle East are emerging as significant players in the photoresist landscape. Micron's assembly-test facility in Gujarat and Tata-Powerchip's fab agreement signify India's inaugural moves into wafer fabrication. Concurrently, Abu Dhabi's Mubadala is spearheading a packaging cluster, initially dependent on imported KrF resists. While these developments offer suppliers a chance to diversify away from the Asia-Pacific stronghold, the immediate volume impact is minimal.

Competitive Landscape

The Photoresist market is consolidated. DuPont and Merck KGaA are widening portfolios via acquisition, bundling anti-reflective coatings, cleaning chemistries, and resists to simplify fabs’ supply chains. Patent filings for metal-oxide formulations jumped in 2024-2025, with FUJIFILM and Sumitomo entering the race. Equipment vendors may forward-integrate further, a scenario that could commoditize standalone resist supply and compress supplier margins. Meanwhile, stringent solvent regulations are shrinking the viable vendor pool, amplifying the competitive moat for firms with compliance scale.

Photoresist Industry Leaders

TOKYO OHKA KOGYO CO., LTD.

JSR Corporation

FUJIFILM Corporation

Shin-Etsu Chemical Co., Ltd.

DuPont

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Asahi Kasei Corporation, responding to the surging demand for advanced semiconductor packages, particularly in applications such as artificial intelligence (AI) servers, has launched the TA Series of Sunfort dry film photoresist.

- February 2025: Sumitomo Chemical Co., Ltd. announced plans to expand its photoresist development and quality evaluation facilities for front-end and back-end semiconductor manufacturing processes at its Osaka Works in Japan.

Global Photoresist Market Report Scope

Photoresists are light-sensitive polymeric resins formulated for use in a photolithographic process, where they serve as masking materials for the transferal of images into an underlying substrate via etching processes. The growing demand for photoresists in semiconductors, which eventually find application in the electronics and automobile industries, is propelling market growth.

The photoresist market is segmented by resist type, tone, application, end-user industry, and geography. By resist type, the market is segmented into ArF Immersion, ArF Dry, KrF, G-Line, I-Line, EUV Metal-Oxide and Dry Resists, and Other Types. By tone, the market is segmented into Positive and Negative. By application, the market is segmented into Semiconductors and ICs, Advanced Packaging (Fan-Out WLP, RDL), Flat-Panel Displays (LCD/OLED), Printed Circuit Boards, MEMS and Sensors, and Other Applications. By end-user industry, the market is segmented into Electronics and Electricals, Automotive and Mobility, Aerospace and Defense, Consumer Packaged Goods (Packaging), and Other Industries. The report also covers the market size and forecasts for the photoresist market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| ArF Immersion |

| ArF Dry |

| KrF |

| G-Line |

| I-Line |

| EUV Metal-Oxide and Dry Resists |

| Other Types |

| Positive |

| Negative |

| Semiconductors and ICs |

| Advanced Packaging (Fan-Out WLP, RDL) |

| Flat-Panel Displays (LCD/OLED) |

| Printed Circuit Boards |

| MEMS and Sensors |

| Other Applications |

| Electronics and Electricals |

| Automotive and Mobility |

| Aerospace and Defense |

| Consumer Packaged Goods (Packaging) |

| Other Industries |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resist Type | ArF Immersion | |

| ArF Dry | ||

| KrF | ||

| G-Line | ||

| I-Line | ||

| EUV Metal-Oxide and Dry Resists | ||

| Other Types | ||

| By Tone | Positive | |

| Negative | ||

| By Application | Semiconductors and ICs | |

| Advanced Packaging (Fan-Out WLP, RDL) | ||

| Flat-Panel Displays (LCD/OLED) | ||

| Printed Circuit Boards | ||

| MEMS and Sensors | ||

| Other Applications | ||

| By End-User Industry | Electronics and Electricals | |

| Automotive and Mobility | ||

| Aerospace and Defense | ||

| Consumer Packaged Goods (Packaging) | ||

| Other Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the photoresist market in 2031?

It is forecast to reach USD 5.53 billion by 2031, reflecting an 11.31% CAGR from USD 3.24 billion in 2026.

Which region is growing fastest for photoresists?

North America leads with an 11.49% CAGR, supported by CHIPS Act-funded fabs coming online after 2026.

Why are metal-oxide resists significant for future lithography?

They enable High-NA EUV patterning below 5 nm by offering higher photon absorption and better etch selectivity than organic chemistries.

How do environmental regulations affect resist suppliers?

New EPA and REACH rules on PFAS solvents and photo-acid generators force costly reformulation, favoring large vendors with compliance scale.

What factors drive photoresist demand in the automotive sector?

Electric-vehicle powertrain and ADAS chips increase lithography layers per car, pushing automotive resist demand toward an 11.86% CAGR.

Page last updated on: