Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Trillion |

| Market Size (2031) | USD 1.12 Trillion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tobacco Market Analysis by Mordor Intelligence

The tobacco market size was valued at USD 0.95 trillion in 2025 and is estimated to grow to USD 0.98 trillion in 2026, reaching USD 1.12 trillion by 2031, registering a CAGR of 3.32% between 2026 and 2031. This demonstrates structural resilience and gradual value growth despite increasing regulatory, social, and public health challenges. Market expansion is primarily driven by the persistence of nicotine dependence and established consumption habits, which maintain a stable demand base among adult users worldwide. Continuous product innovation, including advancements in aerosol science, device engineering, and oral nicotine delivery systems, is shifting the industry from a volume-focused cigarette market to a more technology- and science-oriented ecosystem. The industry's harm-reduction positioning, which promotes product switching over cessation, helps retain consumers within regulated nicotine categories. Furthermore, strong brand loyalty, habitual consumption patterns, and extensive retail availability continue to support repeat purchasing behavior.

Key Report Takeaways

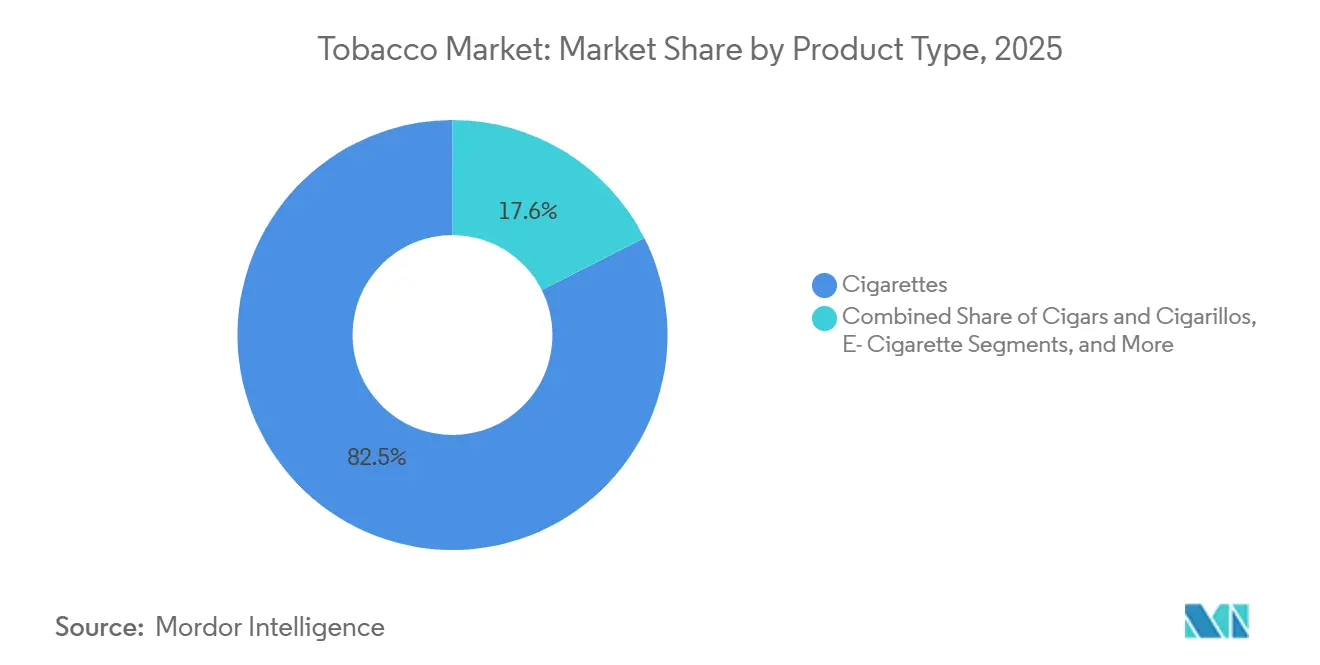

- By product type, cigarettes retained 82.45% of the 2025 value, whereas heated tobacco is forecast to post a 3.76% CAGR through 2031, the fastest rate among all formats.

- By category, mass accounted for 84.36% of revenue in 2025, while the premium segment is projected to grow at a CAGR of 4.18% by 2031.

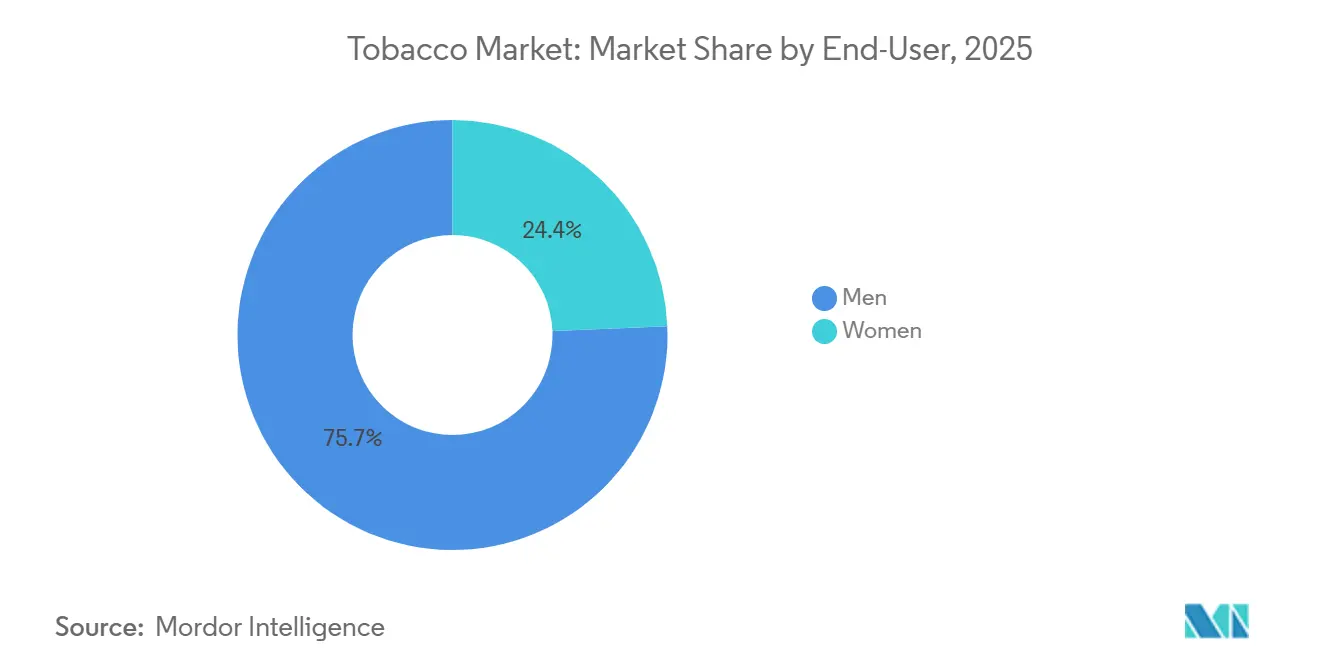

- By end user, men accounted for 75.65% of the 2025 volume, yet the women segment is expected to grow at 4.08% annually from 2026 to 2031.

- By distribution channel, convenience and grocery stores provided 52.47% of sales in 2025, while online retail is set to log a 5.03% CAGR, the swiftest channel growth to 2031.

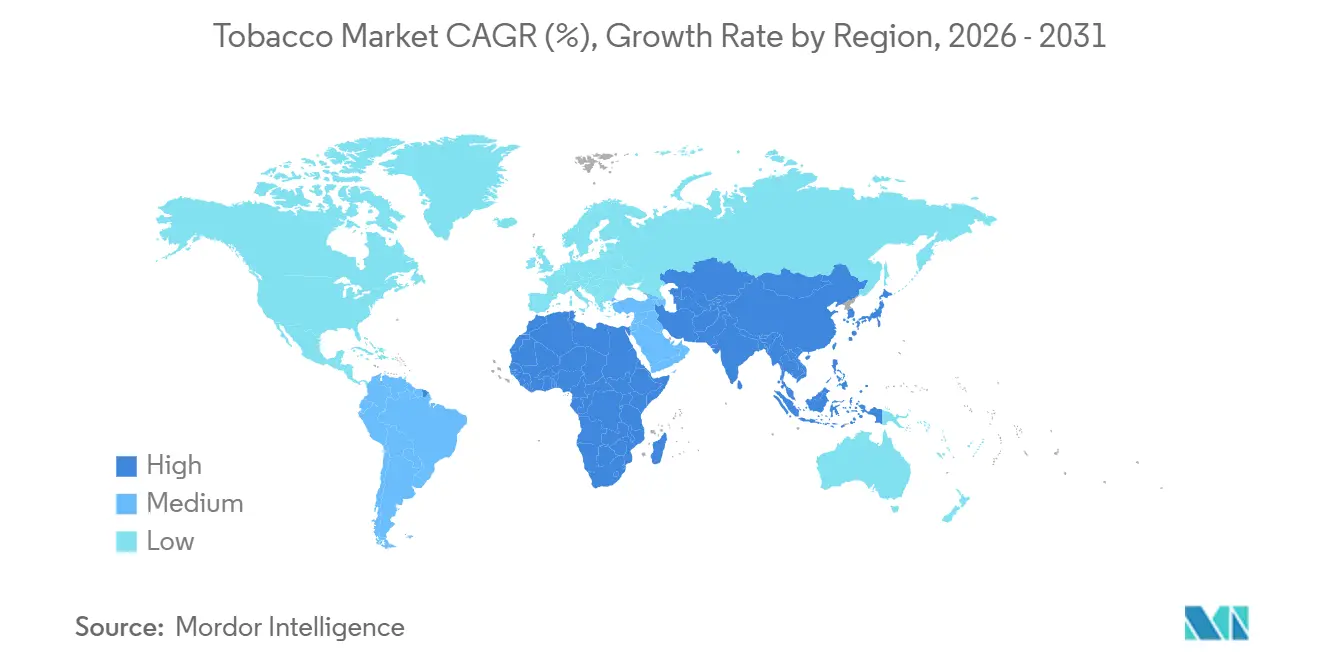

- Asia-Pacific captured the largest geography-level tobacco products market share at 44.56% in 2025, and its regional market is forecast to advance at a 3.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tobacco Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product innovation and alternative nicotine formats | +0.7% | Global, with Asia-Pacific and Europe leading adoption | Medium term (2-4 years) |

| Harm-reduction and reduced-risk product positioning | +0.6% | North America, Europe, Japan; regulatory acceptance critical | Long term (≥ 4 years) |

| Urbanization and lifestyle stress factors | +0.5% | Asia-Pacific core (India, Indonesia, China), spill-over to the Middle East and Africa | Long term (≥ 4 years) |

| Strong brand loyalty and habit persistence | +0.5% | Global, especially mature markets with established brands | Short term (≤ 2 years) |

| Flavor innovation and sensory differentiation | +0.6% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Marketing through packaging and point-of-sale strategies | +0.6% | Global, constrained by plain-packaging mandates in select markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Product innovation and alternative nicotine formats

Product innovation and the development of alternative nicotine formats are becoming significant growth drivers for the global tobacco market, reshaping its long-term structure and growth trajectory. As regulatory pressures, public health awareness, and social stigma surrounding combustible cigarettes increase, tobacco companies are shifting their focus toward science-based, non-combustible, and smoke-free alternatives, including heated tobacco products, nicotine pouches, oral nicotine lozenges, and other reduced-risk platforms. These innovations are fostering market growth by retaining adult smokers within the nicotine ecosystem, promoting switching over to cessation, and expanding consumption opportunities beyond traditional smoking environments. For example, in October 2024, British American Tobacco launched OMNI, a global initiative aimed at advancing the vision of a smokeless world. OMNI is a science-driven platform designed to encourage evidence-based discussions on Tobacco Harm Reduction, supporting the industry's strategic transition toward reduced-risk products and transparent scientific communication.

Harm-reduction and reduced-risk product positioning

Harm-reduction and reduced-risk product positioning are driving the market, influencing both regulatory engagement and consumer adoption patterns. As awareness of smoking-related health risks continues to grow, tobacco manufacturers are increasingly shifting their portfolios toward products designed to reduce exposure to harmful and potentially harmful constituents, rather than relying solely on combustible formats. This approach is fostering market growth by retaining adult nicotine users who might otherwise quit and encouraging a transition from cigarettes to non-combustible alternatives such as nicotine pouches, heated tobacco products, and oral nicotine formats. For example, in December 2025, the Food and Drug Administration (FDA) authorized the marketing of six nicotine pouch products through the Premarket Tobacco Product Application (PMTA) pathway [1]Source: Food and Drug Administration (FDA), "FDA Authorizes 6 Nicotine Pouch Products", fda.gov. The FDA determined that these products contain lower levels of most harmful and potentially harmful constituents (HPHCs) compared to other oral and smokeless tobacco products, representing a significant regulatory endorsement of harm-reduction claims. Such approvals enhance consumer confidence, support manufacturer investment in science-based innovation, and accelerate the legitimization of this product category.

Urbanization and lifestyle stress factors

Urbanization and lifestyle-related stress factors significantly drive demand, particularly by reinforcing habitual consumption among adult users in rapidly urbanizing regions. Accelerated urban development is associated with high-density living, demanding work environments, longer commuting hours, and elevated occupational stress, all of which contribute to sustained tobacco use as a coping mechanism. In urban settings, smoking is often integrated into daily routines, such as work breaks, social interactions, and late-night leisure activities, promoting frequent and repetitive consumption patterns. Urban lifestyles also increase exposure to convenience retail outlets, kiosks, and 24/7 stores, ensuring consistent product availability and reinforcing habitual purchasing behavior. This urban-driven demand is especially prominent in Asia-Pacific markets. For example, the National Bureau of Statistics of China reported that approximately 67% of China’s population resided in urban areas in 2024, illustrating the scale at which urban lifestyle pressures influence consumption behavior [2]Source: National Bureau of Statistics of China, "Degree of urbanization in China", stats.gov.cn. As urban populations continue to expand, the combination of stress-intensive work cultures, the social normalization of smoking among adult users, and easy retail accessibility sustains baseline tobacco demand.

Strong brand loyalty and habit persistence

Strong brand loyalty and habitual persistence remain key factors driving demand stability in the tobacco market, even amidst tightening regulations, increasing health awareness, and the rise of alternative nicotine products. Tobacco consumption is closely tied to nicotine dependence and long-established behavioral routines, where smoking becomes an integral part of daily life through fixed usage moments such as morning rituals, work breaks, social interactions, and stress-relief activities. Over time, these routines reinforce habits, making cessation or brand switching challenging for many adult users. Brand loyalty is further reinforced by consistent sensory experiences, including taste, nicotine delivery, draw resistance, and mouthfeel, which smokers become accustomed to and hesitant to change. Even in highly regulated environments with restrictions on advertising and promotion, tobacco brands sustain loyalty through product familiarity, pack recognition, and consistent availability, ensuring repeat purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent tobacco control regulations | -0.3% | Global, with Europe and North America most restrictive | Long term (≥ 4 years) |

| Supply chain and raw material constraints | -0.2% | Global, acute in Africa and Latin America sourcing regions | Short term (≤ 2 years) |

| Rising social stigma around smoking | -0.2% | North America, Europe, Australia; emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Public smoking bans and anti-smoking campaigns | -0.2% | Global, with enforcement variability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent tobacco control regulations

Stringent tobacco control regulations continue to act as a significant restraint on the global tobacco market, limiting consumption, marketing flexibility, and long-term volume growth in both developed and emerging regions. Governments are increasingly focusing on public health by implementing comprehensive smoke-free laws, advertising bans, packaging restrictions, and product usage limitations. These measures collectively reduce consumption opportunities and diminish brand visibility. Such regulations restrict where and when tobacco products can be used, disrupting habitual smoking patterns that traditionally drive repeat consumption. Smoke-free workplace policies and public-space bans have notably reduced daily smoking frequency, particularly among urban and office-based consumers, while also contributing to the social denormalization of smoking behavior. In September 2024, the European Commission proposed extending the coverage of smoke-free environments, urging member states to adopt laws that fully protect citizens from exposure to tobacco smoke in enclosed public places, workplaces, and public transport [3]Source: European Commission, "Commission proposes to extend coverage of smoke-free environments", commission.europa.eu.

Supply chain and raw material constraints

Supply chain and raw material constraints pose a significant challenge to the market, creating volatility, operational risks, and long-term uncertainty throughout the tobacco value chain. Tobacco production is heavily reliant on agricultural inputs, climatic conditions, and farmer participation, making the availability and quality of tobacco leaves highly vulnerable to climate variability, extreme weather events, and changes in cultivation practices. Factors such as rising temperatures, irregular rainfall, droughts, and floods in major tobacco-growing regions are increasingly impacting crop yields, leaf quality, and curing processes, resulting in an inconsistent supply of raw materials. Additionally, declining farmer interest in tobacco cultivation, driven by regulatory pressures, sustainability concerns, and stricter agricultural standards, is significantly reducing the scale of tobacco farming in several producing countries. These combined challenges are intensifying supply chain disruptions, emphasizing the need for proactive measures, such as sustainable farming practices, technological advancements, and policy interventions, to stabilize raw material availability and ensure long-term market resilience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heated Tobacco Drives Portfolio Rotation

In 2025, cigarettes accounted for 82.45% of the global tobacco market, highlighting their central role in driving overall market performance despite regulatory challenges and the rise of alternative nicotine products. Cigarettes remain the most widely consumed tobacco product worldwide due to entrenched consumer habits, efficient nicotine delivery, and widespread availability across both formal and informal retail channels. The segment benefits from decades of strong brand loyalty, with adult smokers exhibiting low switching tendencies and consistent repeat consumption. Additionally, deeply ingrained nicotine dependence patterns contribute to stable demand across developed and emerging markets alike.

Heated tobacco products (HTPs) are the fastest-growing segment in the global tobacco market, with a projected CAGR of 3.76% through 2031. These products are increasingly driving the industry's next phase of growth as adult smokers seek alternatives to traditional cigarettes that offer the sensory experience of tobacco while minimizing combustion-related smoke, ash, and odor. The segment's growth is further supported by technological advancements, such as precision heating systems, controlled temperature mechanisms, and proprietary tobacco sticks. These innovations enhance product consistency and user experience while fostering high switching costs and brand loyalty.

By Category: Premium Segment Outpaces Mass Despite Inflation

Mass market tobacco products held a significant 84.36% share in 2025, firmly establishing themselves as the primary driver of volume and demand in the global tobacco market. This dominance is attributed to the segment's ability to support high-frequency, habitual consumption on a large scale. Factors such as widespread availability, standardized product formats, and broad consumer familiarity contribute to its strong position. Mass market cigarettes and tobacco products cater to established smoking behaviors, where consumers prioritize consistency, accessibility, and nicotine delivery over premium features or novelty. The segment benefits from extensive distribution across formal and informal retail channels, including convenience stores, kiosks, street vendors, and duty-free outlets, ensuring a steady supply and rapid inventory turnover. Additionally, the affordability of these products plays a critical role in maintaining their widespread appeal, particularly in price-sensitive markets.

The premium tobacco category is projected to grow at a CAGR of 4.18% through 2031, indicating a gradual but significant shift toward value-driven consumption within the global tobacco market. This growth is fueled by premiumization trends among adult smokers, who increasingly prioritize product quality, brand prestige, refined sensory experiences, and perceived sophistication over sheer volume. Premium products stand out through superior tobacco blends, advanced filter technologies, capsule innovations, slimmer formats, and enhanced packaging aesthetics. These features elevate perceived value and strengthen brand identity, even in highly regulated markets. Furthermore, the rising disposable incomes and changing consumer preferences in emerging economies are contributing to the expansion of the premium tobacco segment, as more consumers seek products that align with their lifestyle aspirations.

By End User: Women Smokers Narrow Gender Gap in Urban Markets

Men accounted for a dominant 75.65% of global tobacco users in 2025, positioning them as the primary demand-driving demographic in the global tobacco market. This dominance is influenced by behavioral, cultural, and social factors that continue to shape tobacco consumption patterns across regions. Tobacco use among men is strongly associated with long-standing social norms, peer influence, occupational stress, and lifestyle habits, particularly in emerging and developing markets where smoking is more socially accepted among males than females. Additionally, men exhibit higher initiation rates and stronger nicotine dependency, leading to more frequent and sustained consumption compared to other consumer groups. These factors collectively reinforce the significant role of men in driving the global tobacco market and underline their influence on market trends and demand patterns.

Women represent the fastest-growing consumer segment in the global tobacco market, with a projected CAGR of 4.08% through 2031. This indicates a gradual but significant shift in consumption dynamics. The growth is primarily driven by changing social norms, urbanization, and evolving lifestyle patterns, especially in emerging and middle-income markets where female workforce participation and social independence are on the rise. Tobacco use among women is increasingly associated with stress management, socialization, and aspirational lifestyle choices, particularly in urban areas where smoking is often perceived as a symbol of modernity or personal autonomy. These trends highlight the growing importance of women as a key demographic shaping the future of the global tobacco market, reflecting a transformative shift in consumer behavior and market opportunities.

By Distribution Channel: Online Retail Surges Despite Regulatory Friction

Convenience and grocery stores accounted for 52.47% of the global tobacco market in 2025, solidifying their position as the primary distribution channel. These stores are strategically located to ensure widespread accessibility, making them a preferred choice for consumers. Their ability to cater to impulse purchases and attract frequent customer visits has been instrumental in driving consistent sales volumes. As a result, convenience and grocery stores continue to play a pivotal role in the global tobacco distribution network, maintaining their dominance in the market.

On the other hand, online retail stores are rapidly emerging as the fastest-growing distribution channel, with a projected compound annual growth rate (CAGR) of 5.03% during the forecast period through 2031. This growth is fueled by the increasing penetration of digital platforms and a shift in consumer behavior favoring convenience and privacy in purchasing. E-commerce platforms offer a wider range of product options, competitive pricing, and the convenience of doorstep delivery, attracting a growing base of consumers. While online retail currently holds a smaller market share than traditional channels, its growing significance underscores the evolving dynamics of the tobacco distribution landscape.

Geography Analysis

Asia-Pacific accounted for 44.56% of the global tobacco market value in 2025 and is projected to grow at a CAGR of 3.68% through 2031, surpassing all other regions. This dominance is driven by high cigarette consumption, deeply rooted smoking cultures, robust domestic manufacturing capabilities, and extensive retail networks across formal and informal channels. The region remains the primary volume contributor to the global tobacco industry, supported by mass-market appeal and consistent daily consumption patterns. China plays a significant role in this scale, with the National Bureau of Statistics of China reporting cigarette production of approximately 2.46 trillion units in 2024, up from 2.44 trillion in 2023. This highlights the region's manufacturing strength and demand resilience, even amidst increasing regulatory pressures.

Europe represents a mature tobacco market experiencing structural volume declines due to stringent tobacco control measures, decreasing smoking prevalence, and robust public health initiatives. Despite lower cigarette volumes, value stability is maintained as consumers increasingly shift within the category rather than exiting it entirely. North America is characterized by a transition toward reduced-risk products, stringent regulatory oversight, and declining use of combustible tobacco. This has resulted in value growth concentrated in alternative products rather than traditional cigarettes. In contrast, South America remains dominated by mass-market cigarette consumption, informal trade, and inconsistent regulatory enforcement. While this sustains overall volumes, it limits the penetration of premium and alternative products in several countries.

The Middle East and Africa (MEA) region exhibits the highest growth volatility globally, influenced by regulatory inconsistencies, enforcement gaps, and significant disparities in consumer purchasing power and market structures. In parts of the Middle East, tobacco demand is supported by the social acceptance of smoking and waterpipe use. Meanwhile, certain African markets rely heavily on low-cost cigarettes and informal distribution networks. However, the region faces challenges such as abrupt regulatory changes, shifts in taxation policies, and inconsistent enforcement, which create uncertainty and hinder stable growth.

Competitive Landscape

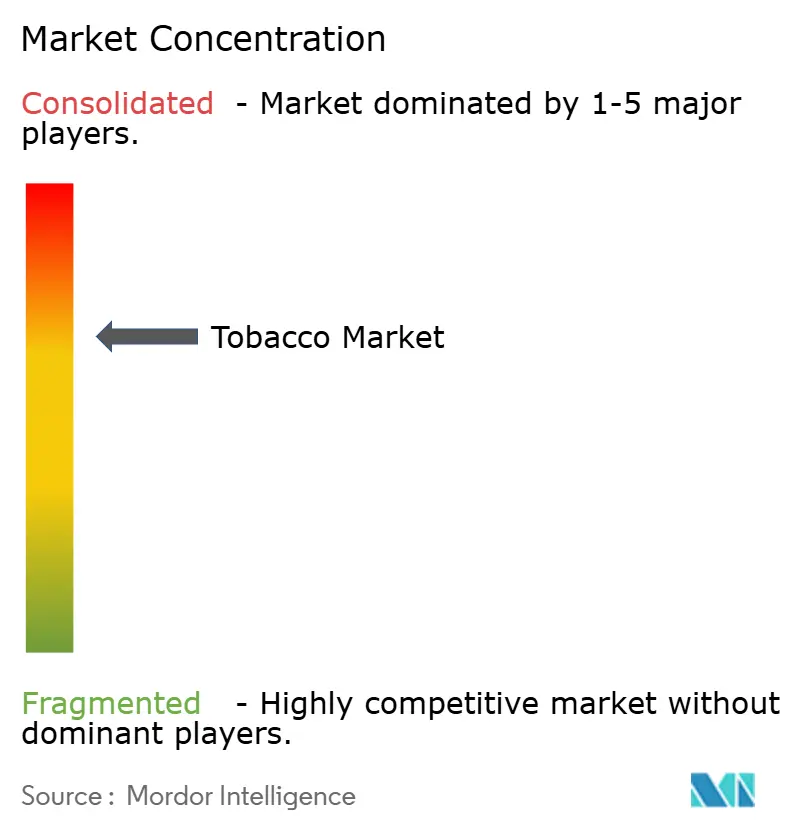

The global tobacco market is highly concentrated at the multinational level, with a few dominant players controlling a significant share of global volumes, value, and innovation pipelines. Key industry leaders include Philip Morris International Inc., British American Tobacco plc, Japan Tobacco Inc., Imperial Brands plc, and KT&G Corporation. These companies leverage extensive manufacturing capabilities, vertically integrated supply chains, and strong regulatory expertise to navigate complex compliance requirements while maintaining scale advantages. Their global presence, robust brand portfolios, and established distribution networks create substantial barriers to entry, particularly in the combustible tobacco segment, limiting competition from smaller players.

Technology has become a critical factor in differentiating competitors, with leading companies heavily investing in aerosol science, device miniaturization, and proprietary heating technologies to advance next-generation tobacco products. Heated tobacco systems and oral nicotine platforms are increasingly designed around closed-loop digital ecosystems. These ecosystems integrate proprietary devices, consumable refills, firmware updates, and companion applications, enhancing consumer retention and increasing brand-switching costs. Advanced Research and Development capabilities enable precise temperature control, optimized nicotine delivery, and consistent sensory experiences, supporting both regulatory compliance and consumer satisfaction. This technology-driven approach is shifting competition from traditional brand equity to science-based performance, device reliability, and ecosystem integration, particularly in markets with high adoption rates of reduced-risk products.

Despite the market's high concentration, opportunities remain in areas such as regulatory arbitrage and format innovation. Variations in regulatory frameworks across regions, such as differing classifications of heated tobacco, nicotine pouches, and smokeless products, allow companies to tailor product launches, prioritize favorable jurisdictions, and strategically sequence market entry. Additionally, format innovation, including hybrid nicotine systems, flavor-delivery technologies, and discreet oral formats, presents growth potential, particularly in markets with stringent smoking restrictions. These factors contribute to a competitive landscape that, while consolidated, remains strategically dynamic. Long-term competitive advantage in the global tobacco market will depend on scale, technological leadership, and regulatory adaptability.

Tobacco Industry Leaders

-

Philip Morris International Inc.

-

British American Tobacco plc

-

Japan Tobacco Inc.

-

Imperial Brands plc

-

KT and G Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: 22nd Century Group, Inc. has introduced its VLN reduced nicotine content cigarettes. This launch aligns with the FDA's proposed Tobacco Product Standard for Nicotine Yield.

- May 2025: BAT Rothmans has launched a new cigarette brand, Global Editions by Dunhill. The product line includes two King Size variants, such as the New York Edition and the Paris Edition, each featuring a dual capsule system that offers distinctive flavor combinations.

- March 2025: Philip Morris Launched IQOS Heated Tobacco Device. IQOS heats tobacco sticks rather than burning them, producing a nicotine-containing aerosol with significantly lower levels of harmful chemicals compared to cigarettes.

- January 2025: Ispire Technology Inc., a company specializing in vaping technology and precision dosing, has launched its BrkFst nicotine products in South Africa and Nigeria. This marks the company's first international nicotine license agreement and product launch.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global tobacco market as the annual value of finished tobacco and nicotine products sold for human consumption, including cigarettes, cigars, cigarillos, roll-your-own blends, smokeless formats, heated-tobacco sticks, and e-cigarettes that contain tobacco-derived nicotine.

Scope exclusion: vapor hardware sold without nicotine and raw leaf trade are outside this assessment.

Segmentation Overview

-

By Product Type

- Cigarettes

- Cigars and Cigarillos

- E- Cigarette

- Heated Tobacco Products

- Smokeless Tobacco

- Other Product Types

-

By Category

- Mass

- Premium

-

By End User

- Men

- Women

-

By Distribution Channel

- Convenience/Grocery Stores

- Specialty Stores

- Online Retail Stores

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with manufacturers, duty-free distributors, retail chains, and public-health advisers across Asia, Europe, the Americas, and Africa test volume assumptions, typical price ladders, and the pace at which smokers adopt heated products. Follow-up consumer surveys then validate penetration rates for premium and next-generation formats.

Desk Research

Mordor analysts first map the market using public statistics from the WHO tobacco atlas, UN Comtrade shipment codes, national excise dashboards, and World Bank household-income tables, which anchor population, duty-paid volume, and cross-border flows. Company filings, investor presentations, and audited financials fill revenue and average-selling-price gaps, while trade journals and association briefs explain channel shifts and regulatory moves. Paid assets such as D&B Hoovers and Dow Jones Factiva supply cross-checks on manufacturer turnover and brand launches. The sources listed are illustrative only; many additional publications helped with data gathering, validation, and clarification.

Market-Sizing & Forecasting

A top-down construct converts duty-paid unit sales, trade reconciliations, and prevalence data into a global demand pool before selective bottom-up roll-ups of sampled ASP × volume validate totals and adjust anomalies. Key inputs include adult smoking prevalence, excise tax per thousand sticks, manufacturer ASP, disposable-income growth, e-cigarette substitution rates, and regulatory bans. Multivariate regression projects values to 2030, and gap areas in bottom-up checks are bridged through channel interviews and regional weighting.

Data Validation & Update Cycle

Outputs pass automated variance scans, peer review within the vertical team, and a senior analyst sign-off. Reports refresh every twelve months, with interim updates if material policy shifts or demand shocks occur. A final pre-publish pass ensures clients receive the latest view.

Why Mordor's Tobacco Market Baseline Earns Trust

Published estimates often diverge because firms select different product baskets, currencies, and refresh cadences.

The largest gaps arise from whether e-cigarettes and heated units are counted, how non-duty-paid trade is handled, and the timing of ASP resets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 950 B (2025) | Mordor Intelligence | |

| USD 906 B (2024) | Global Consultancy A | Excludes e-cigarettes, older base year, biennial updates |

| USD 1 058 B (2025) | International Market Outlook B | Uses gross manufacturer turnover before excise, limited primary validation |

These contrasts show that Mordor's disciplined scope selection, yearly refresh, and dual-track validation give decision-makers a balanced baseline that is transparent, reproducible, and dependable.

Key Questions Answered in the Report

What is the current value of the tobacco products market?

The tobacco products market size reached USD 0.98 trillion in 2026 and is forecast to climb to USD 1.12 trillion by 2031.

Which product type is growing the fastest?

Heated tobacco units are projected to post the quickest growth, expanding at a 3.76% CAGR through 2031 as smokers migrate from combustibles.

Which region dominates sales?

Asia-Pacific commanded 44.56% of 2025 global revenue and is expected to maintain leadership with the highest regional CAGR of 3.68%.

Why are nicotine pouches gaining traction?

The December 2025 FDA authorization of six nicotine pouch products through the PMTA pathway validated the category, supporting shipment growth and strengthening regulatory acceptance versus combustible formats.

Page last updated on: