Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

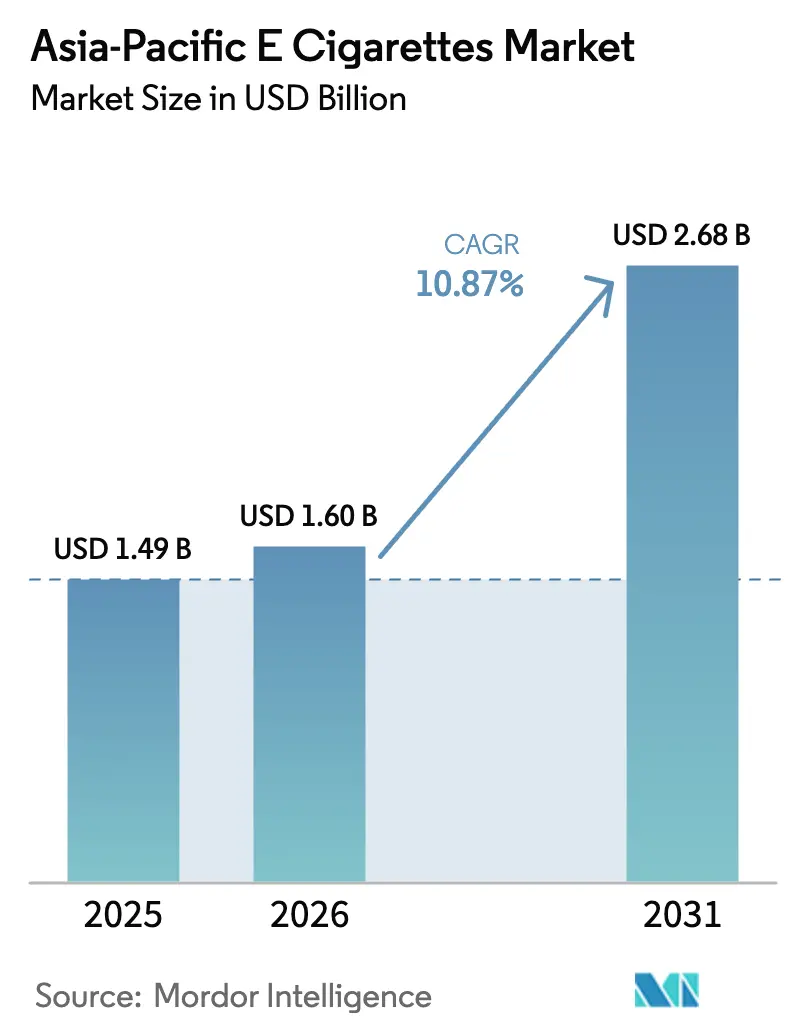

| Base Year Market Size (2025) | USD 1.49 Billion |

| Market Size (2026) | USD 1.60 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 10.87% CAGR |

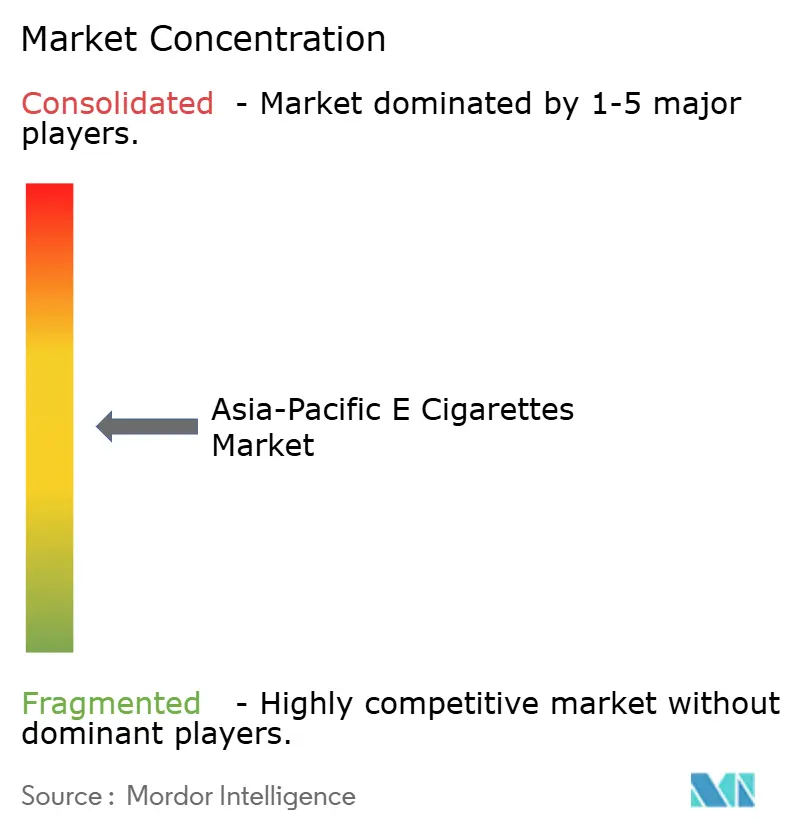

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific E Cigarettes Market Analysis by Mordor Intelligence

The Asia-Pacific e-cigarettes market size is expected to grow from USD 1.49 billion in 2025 to USD 1.60 billion in 2026 and is forecast to reach USD 2.68 billion by 2031 at a 10.87% CAGR over 2026-2031. Key drivers of this growth include clearer regulations in Indonesia and Malaysia, ongoing innovations from China's Shenzhen–Dongguan hardware hub, and a growing base of adult smokers turning to heated-not-burn devices. While Australia mandates pharmacy-only dispensing and China's State Tobacco Monopoly Administration imposes capacity caps, flavor bans in several advanced economies pose challenges. Yet, these hurdles also unveil unmet demands, which agile brands are now addressing with compliant, refillable systems. In Jakarta and Manila, enthusiast communities are driving e-liquid sales up by 11.80% annually. Meanwhile, AI-driven coil-control chipsets are not only boosting average selling prices but also cutting warranty costs. Competitive dynamics are evolving: Guangdong's white-label factories are now backing convenience-store private labels, leading to a drop in the top five players' market share in the Asia-Pacific e-cigarettes market from 48% two years ago to 42% in 2025.

Key Report Takeaways

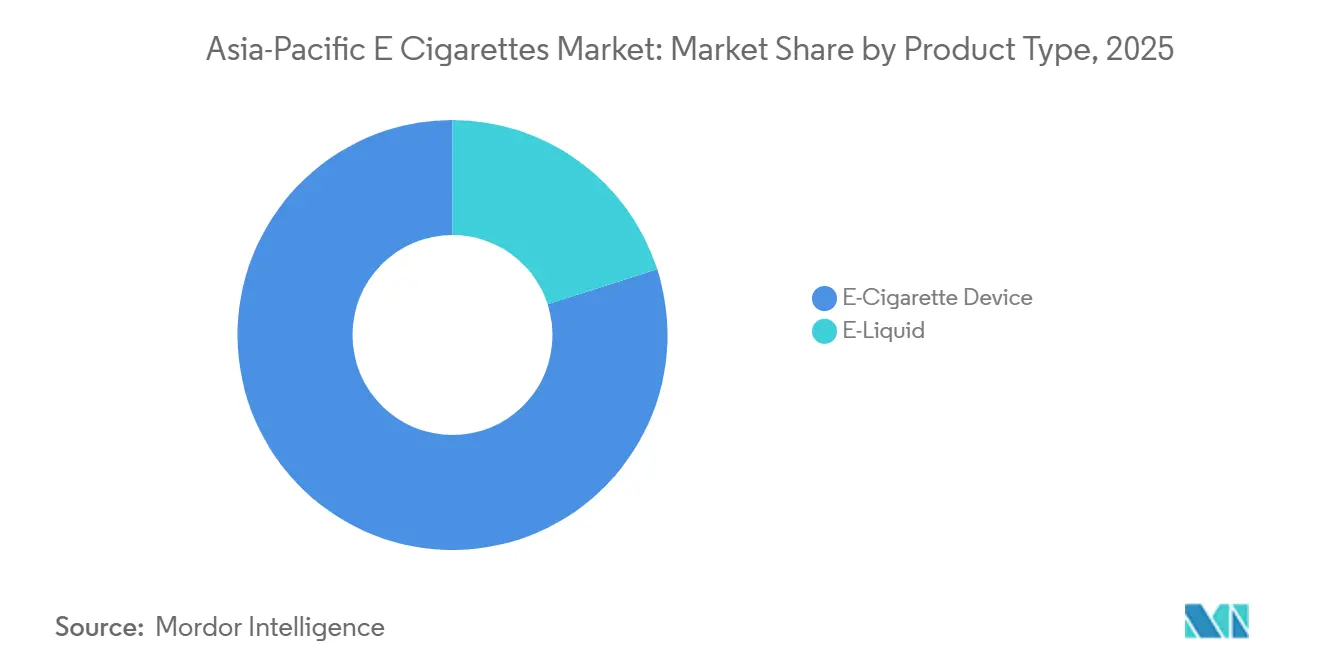

- By product type, e-cigarette devices accounted for 79.96% of 2025 revenue, and the e-liquid segment is forecast to expand at an 11.80% CAGR through 2031.

- By category, closed systems held 69.74% of the Asia-Pacific e-cigarettes market share in 2025, whereas open formats are poised to register 11.93% CAGR to 2031.

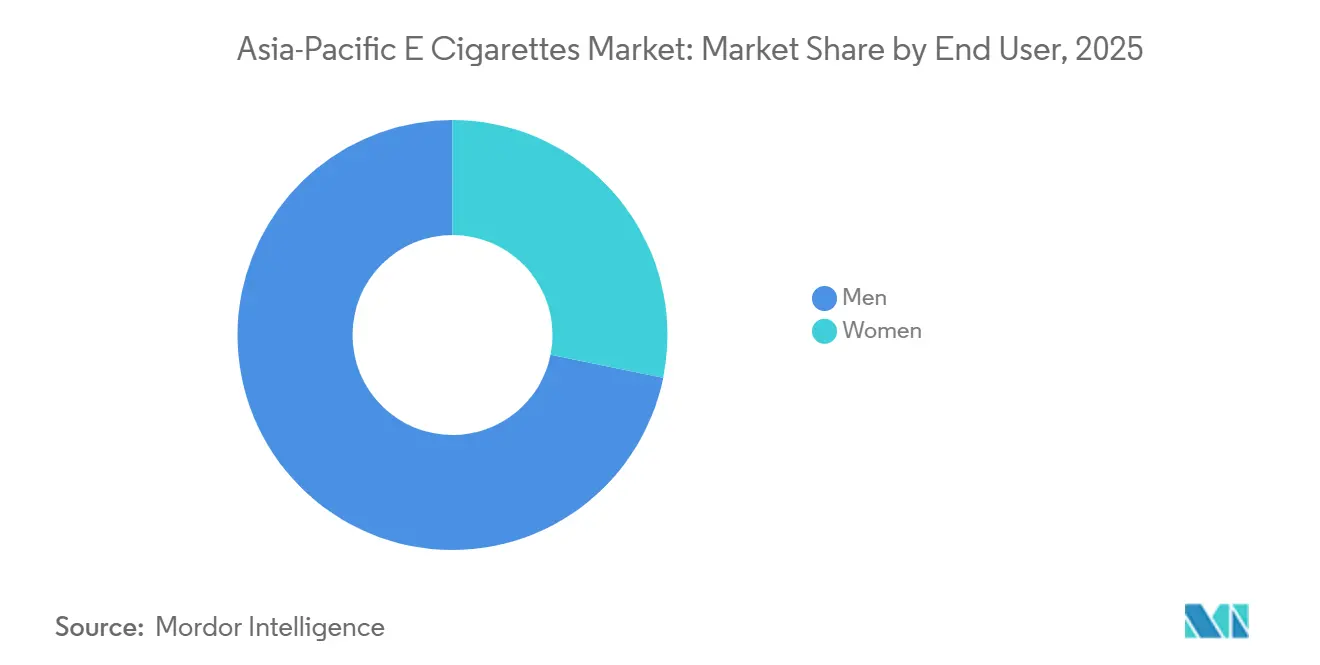

- By end user, men represented 71.82% of volume in 2025, while women constituted the fastest-growing segment at a 12.08% CAGR through 2031.

- By distribution channel, offline retail dominated with a 69.57% slice of the Asia-Pacific e-cigarettes market size in 2025; online retail is on track for a 12.36% CAGR to 2031.

- By geography, Australia accounted for 35.43% market share in 2025, while Indonesia is poised to register a 10.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific E Cigarettes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China's vape manufacturing hub drives innovation and capacity | +1.5% | Concentrated in Shenzhen and Dongguan, with spillover to Southeast Asian contract manufacturers | Medium term (2-4 years) |

| Formalized Southeast-Asian regulations boost compliant product demand | +1.3% | Indonesia, Malaysia, Philippines, Vietnam; limited impact in Singapore and Thailand due to bans | Short term (≤ 2 years) |

| Heated-not-burn device adoption among older smokers increases premium revenues | +1.2% | Japan, South Korea, Australia, New Zealand; early gains in urban Indonesia | Long term (≥ 4 years) |

| E-commerce removes retail-license barriers in Indonesia | +1.0% | Indonesia and the Philippines; India remains banned under the Prohibition of Electronic Cigarettes Act (PECA) | Short term (≤ 2 years) |

| AI-enabled coil control reduces burn risk and promotes brand switching | +0.9% | Premium segments in Australia, Japan, South Korea; gradual adoption in Indonesia and Malaysia | Medium term (2-4 years) |

| Biodegradable pods gain regulatory approval through ESG initiatives | +0.8% | Singapore, Australia, New Zealand; pilot programs in Malaysia and Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

China's manufacturing hub drives innovation and capacity

Shenzhen and Dongguan dominate the global vaping hardware landscape, accounting for a staggering 87% of the world's production capacity. Notably, industry giants Smoore International and Jwei Group have streamlined their operations, reducing the product development timeline to a mere 90 days, from initial concept to mass production. In a move that underscores its strategic importance, the State Tobacco Monopoly Administration has introduced a draft regulation in December 2025. This regulation, which prohibits the issuance of new production licenses, appears to be a protective measure for China National Tobacco Corp's domestic e-cigarette initiative. As a result, the regulation effectively freezes OEM capacity at 2025 levels. Brands now face a dilemma: either negotiate multi-year supply agreements or shift their tooling operations to neighboring Malaysia and Vietnam. This capacity limitation is set to drive up component costs, as brands vie for a limited number of production slots. Consequently, this scenario is likely to hasten the trend of vertical integration, especially among financially robust players like RELX and GeekVape. Furthermore, Shenzhen boasts a unique ecosystem advantage, housing a concentrated network of lithium-polymer battery suppliers, ceramic coil experts, and flavor chemists. This intricate cluster is something Southeast Asian manufacturing hubs will find challenging to replicate, estimating a timeline of 5-7 years to achieve similar quality and scale.

Formalized southeast-Asian regulations boost compliant product demand

In January 2024, Indonesia's Ministry of Finance rolled out a tiered cukai excise structure. The new rates set a charge of IDR 1,500 per milliliter for nicotine-infused e-liquids and IDR 35,000 (equivalent to USD 2.20) for each disposable device. By June 2025, this framework successfully integrated 47 brands into formal distribution channels. Meanwhile, Malaysia's Control of Tobacco Product and Smoking Act 2024 (Act 852) took strides in the vaping landscape. It sanctioned the sale of vaping products to adults aged 21 and older. Furthermore, manufacturers are now mandated to register their formulations with the Ministry of Health and prominently display health warnings, covering 40% of the packaging's surface area. Over in the Philippines, the Food and Drug Administration, in August 2024, rolled out Circular 2024-015. This directive necessitated pre-market notifications for all e-cigarette devices and e-liquids. By December 2025, this process had greenlit 112 SKUs and effectively curtailed an estimated 60% of gray-market imports. Such regulatory measures seem to tilt the scales in favor of multinational brands equipped with robust compliance infrastructures. As a testament, British American Tobacco and Philip Morris International boosted their share of Indonesia's formal retail channel to 34% in 2025, a significant leap from 19% in 2023, a period when the market largely evaded excise enforcement.

Heated-not-burn device adoption among older smokers increases premium revenues

In 2025, Philip Morris International's IQOS ILUMA platform raked in USD 890 million in the Asia-Pacific region. Notably, users aged 45-64 made up 52% of its user base, favoring its reduced odor and ash-free operation over the vapor clouds typical of traditional e-cigarettes. Meanwhile, Japan Tobacco unveiled its Ploom X Advanced in Tokyo in February 2025. This device boasts a dual-heating blade, elevating tobacco-stick temperatures to 295°C. Independent tests by the National Institute of Public Health confirm it offers a nicotine flux akin to combustible cigarettes, but with 90% fewer harmful compounds. In July 2024, Australia's Therapeutic Goods Administration designated heated-tobacco devices as Schedule 4 substances. This move, allowing prescription-based access, positions HnB products as medically supervised cessation tools. By December 2025, this regulatory shift drew in 47,000 registered users. While HnB devices come with a price tag thrice that of disposable vapes, their 18-month repurchase cycle and consumable stick sales promise significant lifetime customer value. This potential has led brands to heavily invest in direct-to-consumer subscription models.

E-commerce removes retail-license barriers in Indonesia

In March 2024, Indonesia's Ministry of Trade rolled out Regulation 50/2024, greenlighting online vape sales. The catch? Platforms must weave in the national age-verification system (NIK lookup) and ensure cukai excise is paid right at the sale. Thanks to this framework, by September 2025, major platforms like Tokopedia and Shopee welcomed 1,340 authorized vape merchants. This newfound regulatory clarity dismantled the retail-license hurdle, a barrier that had previously limited legal sales to 8,200 brick-and-mortar tobacconists. As a result, the number of distribution points surged 16-fold, leading to a 12-18% dip in consumer prices, since online sellers sidestepped traditional wholesale margins. In a parallel move, the Philippines' Department of Trade and Industry, in July 2025, mandated e-commerce platforms to authenticate seller business permits and FDA product registrations before vape listings. Lazada and Zalora seamlessly integrated this compliance check via API links to government databases. Meanwhile, India's 2019 Prohibition of Electronic Cigarettes Act (PECA) still stands, outlawing production, import, and sale. Yet, enforcement lapses have paved the way for cross-border e-commerce from Nepal and Bangladesh, catering to an estimated gray market of 2.3 million users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-flavor bans sweeping Australia, Hong Kong, and Singapore | -1.2% | Australia, Hong Kong, Singapore; spillover risk to New Zealand and Malaysia | Short term (≤ 2 years) |

| Chinese State Tobacco capacity caps squeeze OEM margins | -0.9% | Supply chain impact: acute pressure on brands without diversified manufacturing | Medium term (2-4 years) |

| Surge in counterfeit disposables erodes consumer trust | -0.7% | Australia, New Zealand, Indonesia; concentrated in convenience retail channels | Short term (≤ 2 years) |

| Lithium-ion battery fire incidents trigger insurance premium hikes | -0.6% | Australia, New Zealand, Japan; emerging concern in Indonesia and Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Zero-flavor bans sweeping Australia, Hong Kong, and Singapore

In July 2024, Australia's Therapeutic Goods Administration limited e-liquid flavors to just tobacco, menthol, and mint. This move eliminated fruit, dessert, and beverage flavors, which had previously made up 73% of sales before the regulation[1]Source: Department of Health and Aged Care, “Therapeutic Goods Administration Reforms,” health.gov.au. As a result of this policy change, 41% of casual users shifted to either nicotine pouches or combustible cigarettes within just six months. Meanwhile, Hong Kong's Smoking (Public Health) (Amendment) Ordinance, set to take effect in April 2026, introduces hefty penalties. Those caught with alternative smoking products, including e-cigarettes, heated-tobacco devices, and herbal vaporizers, face fines of HKD50,000 (approximately USD 6,400) and a potential 6-month jail term[2]Source: Hong Kong Department of Health, “Smoking (Public Health) Amendment Ordinance 2026,” dh.gov.hk . In Singapore, the Health Sciences Authority upheld the nation's 2018 ban on e-cigarette sales. In 2025 alone, they confiscated 38,000 devices and took legal action against 142 retailers, citing violations of the Tobacco (Control of Advertisements and Sale) Act. Such stringent bans across the region are causing fragmentation in product portfolios. Manufacturers are now compelled to maintain distinct SKU assortments for different markets, missing out on the benefits of bulk procurement for flavor concentrates. This added complexity is driving up costs by an estimated 8-12% for brands operating throughout the ASEAN region.

Chinese state tobacco capacity caps squeeze OEM margins

In December 2025, the State Tobacco Monopoly Administration unveiled a draft regulation that bars provincial governments from granting new e-cigarette production licenses. This move effectively freezes manufacturing capacity at 2025 levels, a strategy aimed at safeguarding the domestic market share of China National Tobacco Corp. As a result of this cap, OEM margins are set to tighten, intensifying competition among brands for the limited production slots. Notably, tier-2 manufacturers in Dongguan have already begun experiencing lead times of 6-9 months for orders placed in late 2025. In a significant industry shift, Smoore International and Jwei Group, responsible for a combined 34% of the global vaping hardware supply, revealed in November 2025 their intention to set up secondary production hubs in Malaysia and Vietnam. This strategic move, involving investments of USD 180 million, is projected to take 24-36 months to achieve quality standards on par with their Shenzhen facilities. Brands without diversified supply chains are navigating heightened risks. For instance, smaller entities like Innokin and KangerTech faced inventory shortages in Q3 2025, leading to a loss of shelf space to their vertically integrated rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: E-Liquids Gain Share as Open Systems Proliferate

From 2026 to 2031, e-liquids are projected to grow at an annual rate of 11.80%, surpassing the overall market's CAGR of 10.87%. This surge is largely attributed to price-sensitive users in Indonesia and the Philippines, who are increasingly adopting open systems, prioritizing cost per milliliter over device convenience. In 2025, e-cigarette devices accounted for a dominant 79.96% of the revenue, driven by the popularity of disposable formats in Australia and closed-pod systems in Japan. However, this dominance is set to wane due to escalating regulatory pressures targeting single-use plastics and battery waste. Indonesia's cukai excise framework imposes a tax of IDR 1,500 per milliliter on e-liquids, in stark contrast to IDR 35,000 levied on each disposable device. This creates a significant 60-70% cost advantage for refillable systems on a per-use basis, a pricing dynamic that propelled open-system sales to a 34% year-on-year increase in 2025[3]Source: Indonesian Ministry of Finance, “Cukai Regulation for E-Liquids,” customs.go.id.

In 2025, disposable devices dominated the e-cigarette segment, bolstered by Australia's pharmacy model favoring sealed, tamper-evident formats and Indonesia's convenience-store distribution. The latter is particularly notable given the unreliability of refrigerated supply chains for e-liquid storage. Meanwhile, non-disposable devices, including pod mods and box mods, are gaining popularity among enthusiasts. These users appreciate features like wattage customization and coil longevity. Notably, brands like GeekVape and SMOK highlighted that devices priced over USD 60 constituted 22% of specialty retail sales in 2025, a notable rise from 14% in 2023. In May 2025, British American Tobacco's Vuse ePod 2+ made its debut in Sydney, boasting Bluetooth connectivity. This feature not only tracks nicotine intake but also syncs with cessation apps, catering to Australia's prescription-oriented users who perceive vaping as a medically supervised intervention rather than a mere lifestyle choice.

By Category: Closed Systems Dominate, Yet Open Formats Capture Enthusiasts

In 2025, closed vaping systems captured 69.74% of the market revenue, driven by regulatory mandates in Australia and New Zealand for child-resistant, pre-filled cartridges and consumer preferences in Japan and South Korea for hassle-free, leak-proof designs. Open vaping systems are set to grow at an 11.93% CAGR through 2031, fueled by Indonesia's price-sensitive middle class and hobbyist communities in Manila and Bangkok, who prioritize flavor variety and vapor production over portability. Australia's Therapeutic Goods Administration, under its prescription model, permits only closed systems. This policy, enacted in July 2024, curtailed open-format sales in pharmacies and redirected enthusiasts to online imports from New Zealand and Malaysia.

In 2025, Philip Morris International's IQOS ILUMA, a closed heated-tobacco system, accounted for 38% of the company's Asia-Pacific reduced-risk product revenue. Japan and South Korea dominated, representing 71% of unit sales as older smokers transitioned from combustibles. Open systems appeal to users who refill tanks with third-party e-liquids, cutting per-milliliter costs by 50-65% compared to proprietary pods but requiring technical skills for coil replacement and wattage adjustments. Vape shops in Indonesia reported open-system users purchase 90 milliliters of e-liquid monthly, compared to 30 milliliters for closed-pod users, driving higher lifetime value despite lower device margins. Malaysia's Control of Tobacco Product and Smoking Act 2024 mandates health warnings covering 40% of packaging for both open and closed systems, leveling the regulatory field and enabling open-format brands to compete more on price than compliance complexity.

By End User: Women Drive Incremental Growth Through Discreet Formats

In 2025, men accounted for 71.82% of the end-user volume, driven by cultural norms and higher smoking rates in Indonesia, the Philippines, and Vietnam, where over 60% of men use tobacco compared to 3-8% of women. However, women are the fastest-growing segment, with a 12.08% CAGR through 2031. This growth is driven by discreet pod devices promoted by influencers on Instagram and TikTok in urban Indonesia and Thailand, and nicotine-salt formulations that deliver satisfaction at lower wattages with minimal vapor clouds, appealing to conservative markets. In March 2025, RELX launched its Infinity Plus in Jakarta, featuring a lipstick-sized design and pastel colors. It captured 19% of Indonesia's female user base within six months, prompting competitors to introduce gender-specific SKUs.

In Australia, pharmacies attracted more female vape users than gray-market outlets. In 2025, women formed a majority of prescription-based vape users, indicating that medical framing reduces stigma and positions vaping as a cessation tool. Japan Tobacco's Ploom X Advanced targeted women aged 30-45 through collaborations with fashion brands and limited-edition device skins, generating 31% of the product line's 2025 revenue from women, despite their 12% share of Japan's smoking population. In New Zealand, women aged 18-24 made up 42% of new vape users in 2025, driven by fruit and dessert flavors allowed under harm-reduction policies, contrasting with Australia's flavor ban, which reduced female participation. Social commerce platforms like WhatsApp and Facebook groups enabled peer-to-peer vape sales in Indonesia and the Philippines, appealing to women who prefer buying from trusted acquaintances over male-dominated vape shops. In 2025, an estimated 340,000 women purchased devices through these channels.

By Distribution Channel: Online Retail Surges as Platforms Integrate Compliance

In 2025, offline retail dominated with a 69.57% share, underscoring Australia's pharmacy-only sales mandate, which restricted legal sales to 5,800 registered pharmacies. Similarly, in Indonesia, brick-and-mortar tobacconists were mandated to verify buyer ages using national ID cards. Meanwhile, online retail is set to expand at an annual rate of 12.36% through 2031. This growth is spurred by Indonesia's Ministry of Trade Regulation 50/2024, which greenlit e-commerce platforms to sell vapes, provided they integrated NIK age-verification APIs. Additionally, the Philippines' Department of Trade and Industry has mandated platforms to confirm seller FDA registrations. By September 2025, Tokopedia and Shopee had onboarded 1,340 authorized vape merchants in Indonesia. This move amplified distribution points by 16 times and led to a 12-18% drop in consumer prices, as online sellers sidestepped traditional wholesale margins.

In Australia, a prescription requirement is stifling online growth. The Therapeutic Goods Administration has ruled that pharmacies can only dispense vapes post-prescription verification. This requirement clashes with the instant-checkout processes typical of e-commerce. In New Zealand, online vape sales are allowed for adults 18 and older. Retailers must employ third-party age-verification services that align with government databases. Members of the Vape Merchants Association have adopted this compliance measure, incurring an average cost of NZD 0.45 (USD 0.27) per transaction. In Japan and South Korea, offline retail reigns supreme. Convenience-store giants like 7-Eleven and FamilyMart keep heated-tobacco devices behind counters. They've trained staff to verify ages using point-of-sale prompts. This controlled-access strategy accounted for 78% of HnB device sales in 2025. In India, the 2019 Prohibition of Electronic Cigarettes Act outlaws both online and offline vape sales. Yet, enforcement lapses have paved the way for cross-border e-commerce from Nepal, catering to an estimated 2.3 million users through unregulated means.

Geography Analysis

In 2025, Australia held 35.43% of regional revenue, but this share is expected to decline. The Therapeutic Goods Administration's July 2024 prescription mandate shifted casual users to nicotine pouches and cigarettes, reducing pharmacy-dispensed vape volumes by 19% in Q4 2025 compared to pre-regulation levels. The pharmacy-only model eliminated convenience-store and tobacconist sales, centralizing supply through 5,800 pharmacies with dispensing fees of AUD 15-25, raising consumer costs to AUD 45-65 per device versus AUD 25-35 in the gray market. Counterfeit ELFBAR and RELX disposables flooded stores in late 2024, with 1.2 million units seized in H1 2025, representing 23% of consumption and disrupting compliant manufacturers' pricing. The July 2024 flavor restriction to tobacco, menthol, and mint eliminated 73% of pre-regulation sales, driving users toward heated-tobacco devices and nicotine pouches available in broader retail channels.

Indonesia is set to grow at 10.56% annually through 2031, driven by the Ministry of Finance's January 2024 cukai excise framework, which legitimized 47 brands and enabled platforms like Tokopedia and Shopee to onboard 1,340 merchants by September 2025. The excise structure, with IDR 1,500 per milliliter for e-liquids and IDR 35,000 per disposable device, boosted open-system adoption, with refillable devices capturing 41% of 2025 sales, up from 28% in 2023. Regulation 50/2024 allowed online vape sales via platforms using the national age-verification system, expanding distribution points 16-fold and reducing prices by 12-18%. However, 41% of vapes sold in 2025 lacked cukai excise stamps, costing the government IDR 780 billion (USD 49 million) annually and enabling gray-market operators to undercut distributors by 25-35%.

New Zealand maintained a harm-reduction stance, allowing vape sales to adults 18 and older without prescriptions, securing 8.2% of regional revenue in 2025 despite a population of 5.1 million. The Ministry for the Environment proposed a single-use vape ban in October 2025, targeting implementation by July 2027, prompting RELX and JUUL to accelerate recycling programs. In 2025, Customs seized 340,000 non-compliant devices, with 23% containing unsafe heavy metal levels, raising retailer liability concerns and driving consolidation toward ISO-certified brands. The rest of Asia-Pacific, including Vietnam, Thailand, Malaysia, and the Philippines, contributed 21.0% of 2025 revenue. Malaysia legalized sales in 2024, while Thailand and Vietnam maintained bans, pushing activity to gray markets supplied by cross-border e-commerce from China and Singapore.

Regulatory Landscape

Regulation across Asia-Pacific remains fragmented, with regimes diverging on pre-market controls, product standards, and age restrictions. Australia moved access further into a pharmaceutical-only pathway under Therapeutic Goods Administration reforms commencing 1 July 2024, and nicotine vaping product standards take effect from 1 July 2025. This concentrates legal sales through registered pharmacies and restricts product characteristics such as flavours. New Zealand updated its Smokefree Environments and Regulated Products Amendment Act (No 2) in December 2024, then tightened controls on disposables and safety requirements through 2025, raising compliance costs for importers and specialty retailers.

In Southeast Asia, enforcement tightens with Singapore's Tobacco and Vaporisers Control Act effective 1 May 2026, consolidating powers under the Ministry of Health and the Health Sciences Authority and reinforcing a prohibition-led stance on vaporisers and components. Hong Kong penalties come into force in April 2026, adding further regulatory oversight and mandatory traceability across the region.

Competitive Landscape

The Asia-Pacific e-cigarettes market is moderately concentrated, with the top five players - RELX Technology, Smoore International, Philip Morris International, British American Tobacco, and Japan Tobacco - projected to command a major market share. This shift is attributed to white-label manufacturers in Guangdong province catering to private-label brands for local convenience chains. Vertical integration has emerged as a key competitive edge, with RELX establishing proprietary manufacturing in Shenzhen and GeekVape taking charge of ceramic-coil production. These moves are seen as a buffer against the State Tobacco Monopoly Administration's December 2025 capacity freeze, which is anticipated to reduce OEM availability by 15-22% until 2027. Market-entry strategies are being influenced by regulatory nuances. British American Tobacco is focusing on Indonesia and Malaysia, where established excise frameworks favor compliant businesses. In contrast, smaller entities like ELFBAR and SKE Crystal are tapping into Australia's gray market, exploiting enforcement gaps to distribute in convenience stores, despite a pharmacy-only sales mandate.

Brand loyalty is increasingly swayed by technological advancements. In 2025, 18% of premium devices featured AI-driven coil-control chipsets, leading to a 23% drop in warranty claims and allowing brands to charge a 30% premium over their fixed-wattage counterparts. Patent filings shed light on industry priorities. Between 2024 and 2025, Philip Morris International lodged 47 heated-tobacco patents with the Japan Patent Office, zeroing in on blade-heating designs and aerosol-cooling methods. Meanwhile, GeekVape's 23 patents spotlight neural-network wattage controls and predictive coil-life sensors.

There's untapped potential in Indonesia's tier-2 cities and provincial markets in the Philippines. Here, the distribution density lags at under one retail point for every 5,000 adults. Local brands like Vapetasia are making inroads, leveraging Tagalog-language social media campaigns and cash-on-delivery options to navigate credit-card usage challenges. British American Tobacco is making strides in biodegradable pod development. Their PLA prototype, approved provisionally by Singapore's National Environment Agency in March 2025, gives them a 24-month lead over rivals. This advantage could be pivotal if New Zealand's potential single-use ban gains traction across ASEAN by 2028.

Asia-Pacific E Cigarettes Industry Leaders

RELX Technology

Smoore International

Philip Morris International

British American Tobacco p.l.c

Japan Tobacco Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Indonesia offers a clear route for commercializing age-gated, standards-compliant products under Government Regulation No. 28 of 2024 and the existing excise structure. This is shaping demand for registered SKUs, verified online commerce, and documented product content in the formal channel. The Philippines FDA pre-market notification pathway (Circular 2024-015), which cleared 112 SKUs by December 2025 and reduced gray-market imports materially, also points to an addressable need for brands that can maintain dossiers, testing, and ongoing compliance updates.

Portfolio shifts toward refillable or open systems and reduced-waste formats align with regulators focusing on plastics and battery externalities. BATs biodegradable pod work, including provisional approval in Singapore under an Extended Producer Responsibility framework (March 2025), supports continued investment in materials, collection, and recycling programs that can help brands remain listable as scrutiny increases.

Recent Industry Developments

- July 2026: Smoore International disclosed that EVE Battery received board approval to reduce its shareholding by up to 3.5% of total issued shares over the next year. The announcement points to a potential realignment of capital allocation at a key Asia-Pacific hardware supplier, with implications for supplier funding and technology investment dynamics.

- June 2026: Philip Morris International expanded the VEEV e-cigarette platform in South Korea by adding the VEEV inPRIME device and VEEBI inPRIME pods. The update broadens PMIs smoke-free portfolio in a major nicotine market and increases competitive pressure for compliant pod-based formats in North Asia.

- January 2024: Indonesia's Ministry of Finance introduced a tiered cukai excise structure for vaping, including per-milliliter charges on nicotine e-liquids and a per-unit levy on disposable devices. The tax design reinforced a cost advantage for refillable systems and accelerated the shift toward formal distribution by making excise-stamped, compliant products more economically differentiated from gray-market supply.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Asia Pacific e-cigarettes market is defined as revenue generated from e-cigarette devices and e-liquids sold through online and offline retail channels across the Asia Pacific region, measured in USD value terms.

Scope exclusions: The market size excludes heated tobacco products, traditional combustible cigarettes, and ancillary accessories that are not sold as devices or e-liquids.

Segmentation Overview

- Product Type

- E-Cigarette Device

- Disposable

- Non-Disposable

- E-Liquid

- E-Cigarette Device

- Category

- Open Vaping Systems

- Closed Vaping Systems

- End User

- Men

- Women

- Distribution Channel

- Offline Retail

- Online Retail

- Country

- Australia

- New Zealand

- Indonesia

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with getting the basic demand and policy context right, since usage and legality change quickly in this category. We typically review public sources such as national health ministries and regulators (for age rules, nicotine limits, and product legality), World Health Organization tobacco control updates, UN Comtrade trade statistics for relevant device and liquid HS codes, and World Bank macro indicators that help normalize spending across countries.

To anchor company activity and pricing signals, we also use sources such as company annual reports, earnings materials, investor decks, and official filings where available, followed by reputable press, distributor announcements, and association websites covering vapor or retail trade. Patent databases are selectively used to understand device form factor shifts (open vs closed systems) and the pace of product refresh. These examples are not exhaustive, and we reviewed many other public sources to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary inputs focus on aligning the model to real sell-through and channel behavior, since reported shipments and consumer interest do not always translate into steady retail revenue. We speak with a mix of manufacturers, importers, distributors, specialized retailers, and online channel participants across APAC so assumptions on pricing, margins, and category mix can be adjusted and then confirmed from more than one viewpoint.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 19% | |

| Mid tier: 43% | Functional/Unit leaders: 34% | |

| Smaller Players: 21% | Managers: 47% |

Market-Sizing & Forecasting

The market is primarily built using a top-down demand pool approach where adult nicotine user base, category legality, and retail availability are used to reconstruct the addressable spending by country, and then rolled up to the region. To keep the total realistic, results are cross-checked through selective bottom-up approximations such as sampled average selling price times estimated unit volumes by channel, and quick supplier and distributor roll-ups where disclosure is available.

Key inputs that shape the model include the share of open versus closed vaping systems, device replacement cycles, average e-liquid consumption patterns, channel mix split between offline retail and online retail, and observed price bands for devices and liquids by country. Since regulation is a major swing factor, assumptions are also adjusted for changes like nicotine caps, flavor restrictions, import controls, and enforcement intensity. Forecasting is done using scenario analysis, with a base case informed by interview consensus on regulatory direction and consumer switching trends, and then stress-tested with faster and slower adoption cases. Where country data points are missing, we use proxy indicators from similar markets in the region and re-validate the implied per-user spend during follow-up calls.

Data Validation & Update Cycle

Validation is handled through a repeatable set of checks that compare the modeled totals against independent signals, and then the variances are investigated before sign-off. We review country-level outliers by testing the implied per-adult spend, checking channel mix assumptions, and re-running the math with alternate price and volume inputs to confirm whether the result remains stable.

A second analyst review challenges key assumptions like category mix and the timing of regulatory changes, and any material gap triggers targeted re-contacts with regional experts. Reports are refreshed annually, and interim updates are made if a major policy shift, enforcement change, or supply disruption materially alters the expected demand. Before delivery, the latest news and public releases are re-scanned so clients receive an updated view that matches the current market context.

Mordor Intelligence's Asia Pacific E Cigarettes Market Market Size Compared With Other Published Estimates

Published market sizes for Asia Pacific e-cigarettes can vary widely, even when the same countries are being discussed. The main reasons are usually different product inclusions, how retail value is defined across channels, and the year used as the reference point for currency conversion and pricing.

Some estimates blend a wider vaping basket and apply high-growth adoption assumptions uniformly across countries, which can lift the starting value and steepen the forecast curve. In Mordor Intelligence, the count is limited to e-cigarette devices and e-liquids, and the regional roll-up is kept tied to open versus closed system mix, channel splits, and country-level legality checks so restricted markets do not get overstated.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.49 B (2025) | |

| Industry Research Publisher A | USD 13.73 B (2025) | Uses a broader category definition that appears to include a wider set of vaping product types and assumptions on adoption and pricing across several large countries, which can inflate the addressable revenue pool for the same year. |

| Global Research Publisher B | USD 6.50 B (2023) | Uses an earlier base year and a combined e-cigarette plus vape framing with fewer visible checks on country legality and product scope, so the value can shift due to year selection, currency timing, and category blending. |

Taken together, the spread in published values is mainly explained by scope choices and base-year alignment, followed by how aggressively prices and adoption are projected. By keeping inputs traceable to channel revenue logic, system-type mix, and country-by-country market access, our estimate stays easier to reproduce and to update when policy or pricing changes.

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific e-cigarettes market by 2031?

The Asia-Pacific e-cigarettes market size is expected to grow from USD 1.49 billion in 2025 to USD 1.60 billion in 2026 and is forecast to reach USD 2.68 billion by 2031 at a 10.87% CAGR over 2026-2031.

Which segment is expanding fastest within the Asia-Pacific e-cigarettes?

E-liquids, driven by refillable open systems, are growing at an 11.80% CAGR through 2031.

Why is Indonesia considered a key growth engine for e-cigarettes?

The country’s excise clarity and NIK-verified e-commerce lifted distribution points sixteenfold and will drive a 10.56% CAGR.

How are AI-driven chipsets influencing device demand?

Neural-network coil control reduces dry-hits by 68% and supports a 30% price premium, boosting premium device uptake.

What regulatory trend poses the greatest near-term risk?

Flavor bans in Australia, Hong Kong, and Singapore could trim regional CAGR by 1.2% over the next two years.

Page last updated on: