Food Grade Phosphoric Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

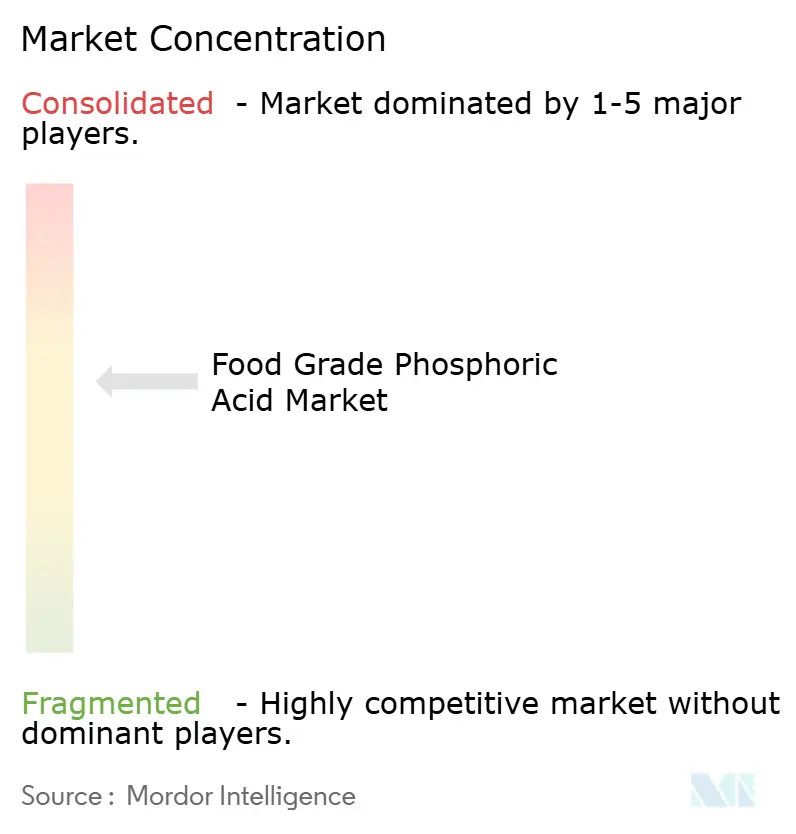

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Grade Phosphoric Acid Market Analysis by Mordor Intelligence

The food-grade phosphoric acid market was valued at USD 2.62 billion in 2025 and is expected to reach USD 2.76 billion in 2026, with projections indicating it will grow to USD 3.55 billion by 2031. This represents a compound annual growth rate (CAGR) of 5.16% during the forecast period from 2026 to 2031. The market's growth is driven by the continued reliance of beverage formulators on the acid's sharp flavor profile and buffering properties, while food processors benefit from its dual functionality as an emulsifier and microbial-control agent. Cola remains the largest application segment; however, the use of food-grade phosphoric acid is expanding in processed cheese, ready-to-eat meat, and shelf-stable dairy products, where alternative acidulants fail to provide the same level of pH precision. Investments in high-purity "green" production facilities in countries such as Canada, India, and Egypt indicate a willingness among brand owners to pay a premium for low-impurity grades that facilitate regulatory compliance. Concurrently, regulators in the United States and Europe are exploring phosphogypsum reuse and implementing stricter impurity limits, prompting producers to adopt cleaner wet-process production methods.

Key Report Takeaways

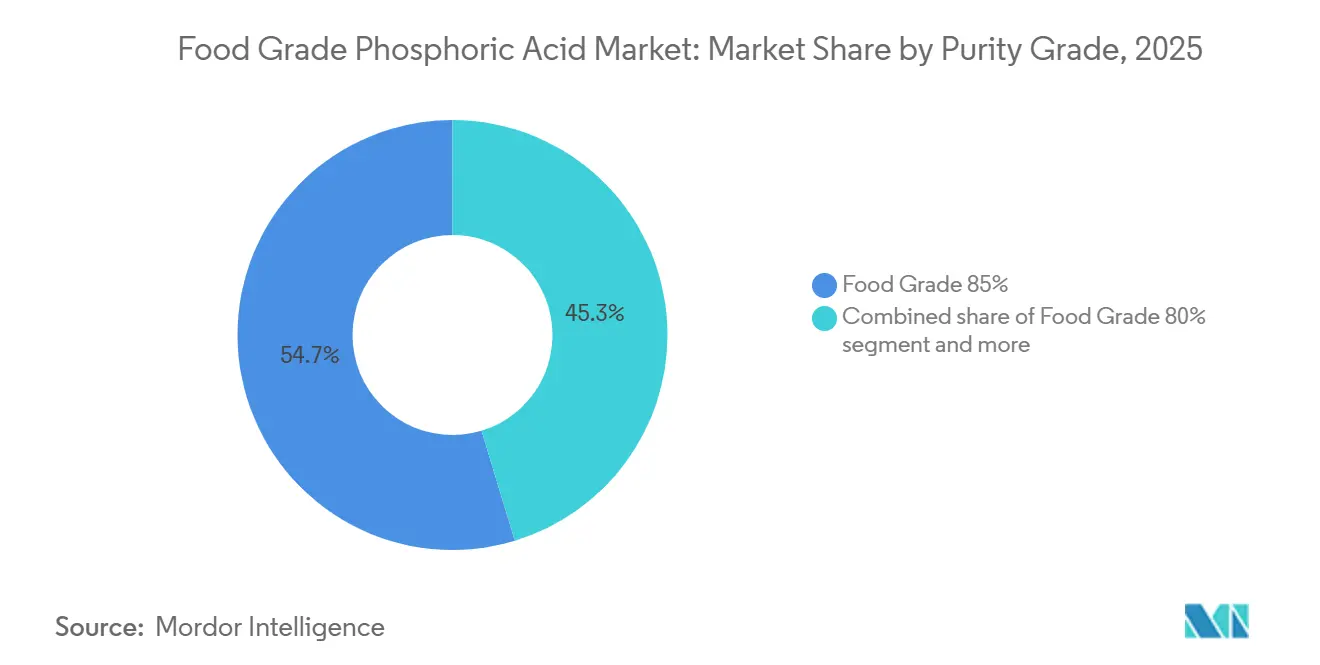

- By purity grade, food grade 85% captured 54.69% share in 2025; food grade 80% registers the fastest 5.95% CAGR to 2031.

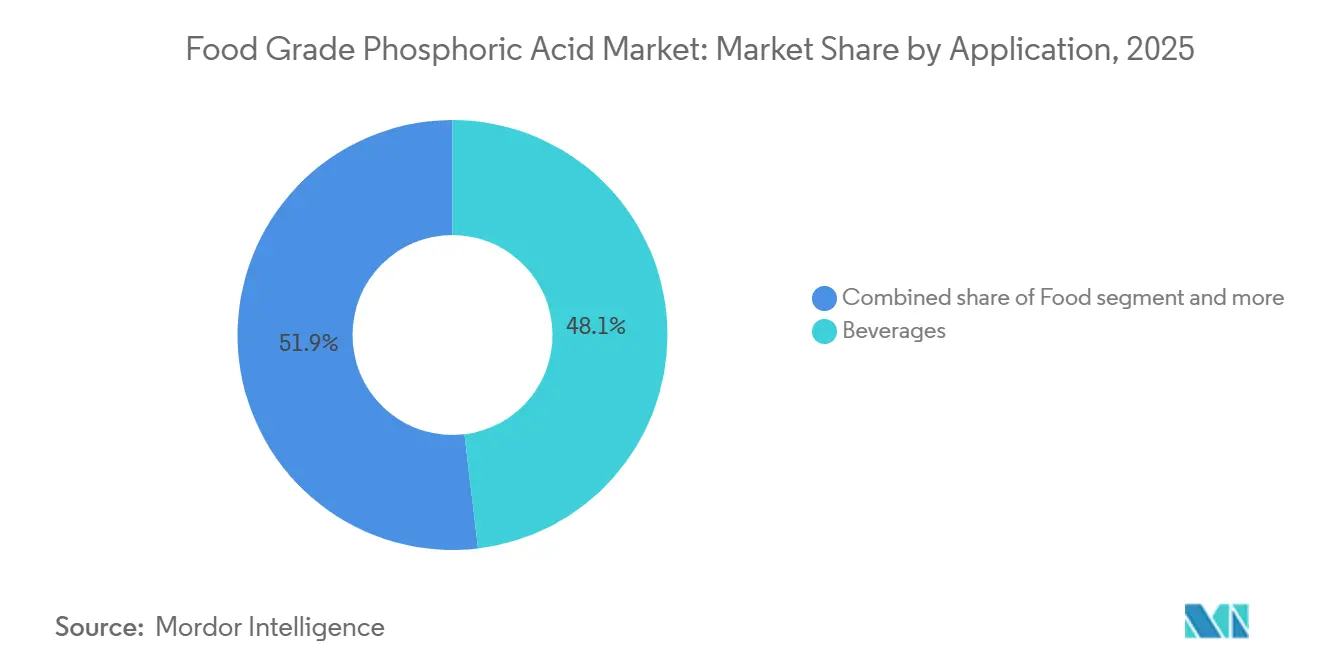

- By application, beverages led with 48.10% of food-grade phosphoric acid market share in 2025, while the food segment is projected to expand at a 6.89% CAGR through 2031.

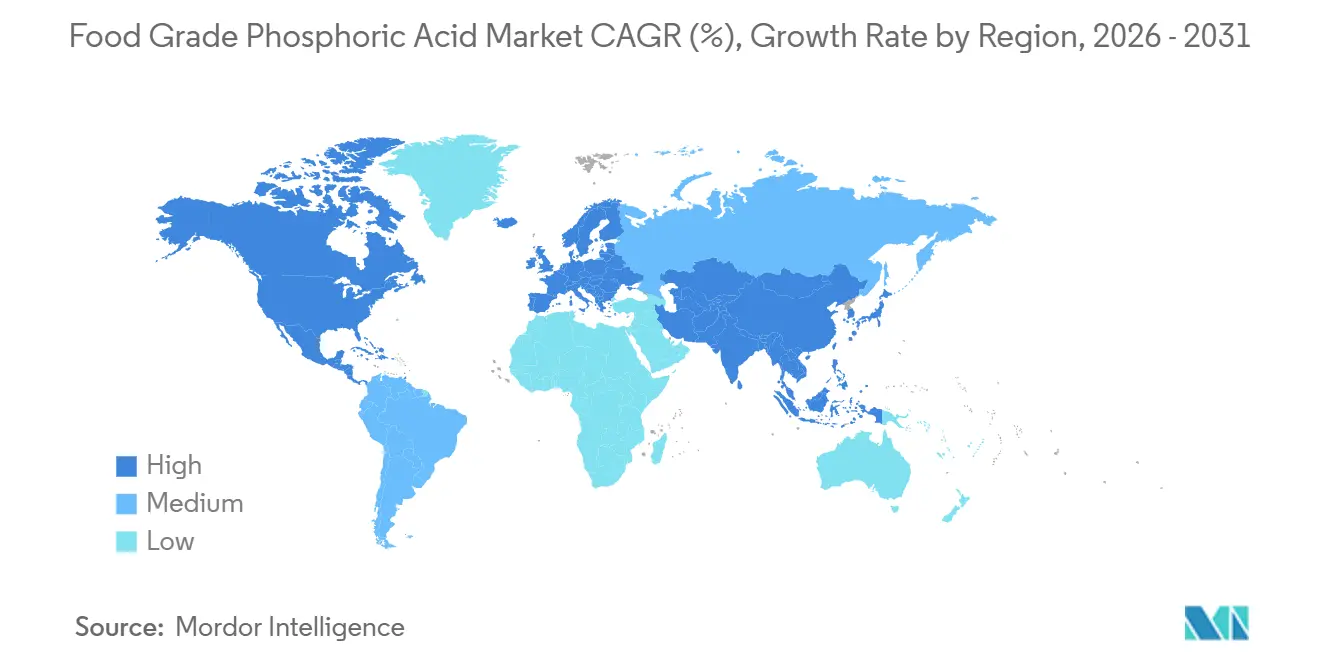

- By geography, North America accounted for 28.56% share in 2025, yet Asia-Pacific is advancing at the highest 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Grade Phosphoric Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of carbonated soft drinks | +0.7% | Global, with concentration in North America, Latin America, and Middle East | Medium term (2-4 years) |

| Growth in ready-to-eat and packaged foods | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Demand for multifunctional clean-label acidulants | +0.6% | North America and Europe, early adoption in urban Asia-Pacific | Short term (≤ 2 years) |

| Investments in high-purity "green" phosphoric production | +0.5% | Global, led by Europe and North America, emerging in China and India | Long term (≥ 4 years) |

| L12: Trade-policy shifts favoring regional supply security | +0.4% | Europe (anti-dumping), Asia-Pacific (import substitution), North America (nearshoring) | Medium term (2-4 years) |

| Compliance with GRAS status for food applications | +0.3% | Global, baseline requirement for market access | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising consumption of carbonated soft drinks

The rising global demand for carbonated soft drinks is a significant driver for the food-grade phosphoric acid market. Phosphoric acid is extensively used to impart tangy flavor, acidity, and preservative properties to sodas and other fizzy beverages. The increasing consumer preference for ready-to-drink and sweetened carbonated beverages, particularly in regions such as Europe and North America, continues to support the demand for high-purity, food-grade phosphoric acid. Additionally, beverage manufacturers are diversifying their product offerings to include sugar-free, flavored, and functional carbonated drinks, further boosting the reliance on phosphoric acid to ensure consistent taste and extended shelf life. Data from the British Soft Drinks Association indicates that total soft drink consumption in the United Kingdom increased to 15,707 million liters in 2024, compared to 15,443 million liters in 2023[1]Source: British Soft Drinks, "2024 ANNUAL REPORT, " britishsoftdrinks.com. This growth underscores the enduring popularity of carbonated beverages and highlights the ongoing demand for food-grade phosphoric acid as a critical ingredient in the beverage industry.

Growth in ready-to-eat and packaged foods

The growing demand for ready-to-eat (RTE) and packaged food products is driving increased usage of food-grade phosphoric acid beyond its traditional applications in beverages. Manufacturers are utilizing phosphoric acid as a pH regulator, preservative, and emulsifying agent in items such as processed cheese, dairy-based snacks, shelf-stable meals, and processed meats. Its role in stabilizing texture, preventing fat separation, and extending shelf life is becoming increasingly important as urbanization and fast-paced lifestyles fuel consumer preference for convenient, ready-to-consume foods. In 2024, 82% of adults in the United States reported consuming ultra-processed foods, highlighting the growing reliance on packaged and convenient food options[2]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY," ific.org. This trend is directly influencing the demand for phosphoric acid, as food processors depend on it to maintain product quality, consistency, and safety in large-scale production within the ready-to-eat and packaged food markets.

Demand for multifunctional clean-label acidulants

The growing consumer preference for natural and clean-label ingredients is driving the demand for multifunctional acidulants, such as food-grade phosphoric acid, which offer multiple benefits within a single ingredient. In the United States, 36% of consumers favor foods labeled as natural, emphasizing a focus on authenticity, traceability, and perceived health advantages[3]Source: Ayana Bio, "SURVEY DATA REVEALS TWO-THIRDS OF AMERICAN ADULTS WOULD EAT MORE AND PAY MORE FOR ULTRA-PROCESSED FOODS THAT INCLUDE MORE NUTRITIOUS INGREDIENTS," ayanabio.com . Food manufacturers are addressing this trend by utilizing acidulants that not only regulate pH and enhance flavor but also serve as preservatives, stabilizers, and emulsifiers, thereby reducing reliance on synthetic additives. This multifunctionality supports the clean-label movement, allowing producers to streamline ingredient lists while ensuring product quality and shelf life, particularly in beverages, dairy products, and ready-to-eat (RTE) food categories.

Investments in high purity "green" phosphoric production

Sustainability pressures are influencing capital allocation toward wet-process purification technologies that minimize heavy-metal contamination and reduce the carbon intensity of food-grade phosphoric acid production. Traditional wet-process methods produce phosphoric acid with concentrations ranging from 30% to 54%, containing impurities such as cadmium, arsenic, and fluoride. These impurities require multi-stage purification to meet food-grade standards of ≥75% assay and arsenic levels below 3 milligrams per kilogram. First Phosphate's December 2024 licensing agreement with Prayon for a 600-tonne-per-day purified phosphoric acid plant in Canada, which employs Prayon's proprietary solvent-extraction technology, highlights the transition toward integrated, low-impurity production processes that eliminate legacy purification challenges. These investments address stricter food-safety standards and brand-owner requirements for traceability, while also reflecting a strategic expectation that premium-priced, low-carbon phosphoric acid will offer margin advantages as carbon border adjustment mechanisms expand in Europe and North America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative acids (citric, lactic, malic) | -0.6% | Global, most intense in Europe and North America | Medium term (2-4 years) |

| Health concerns from excessive consumption | -0.5% | North America and Europe, emerging in urban Asia-Pacific | Long term (≥ 4 years) |

| Stringent regulatory restrictions on allowable concentrations | -0.3% | Global, led by FDA and EFSA frameworks | Short term (≤ 2 years) |

| Stringent effluent and phosphogypsum regulations | -0.4% | North America and Europe, tightening in China and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from alternative acids (citric, lactic, malic)

Citric, lactic, and malic acids are gaining market share in applications where the sharp acidity and mineral aftertaste of phosphoric acid are less critical. These include fruit-flavored beverages, sports drinks, and organic food products. Citric acid, produced through fermentation and perceived as a natural ingredient, is the preferred acidulant for clean-label reformulations. Lactic acid, with its dual functionality as an acidulant and antimicrobial agent, is increasingly used in meat and dairy preservation. Malic acid, although more expensive, is being adopted in premium beverage lines due to its smoother acidity profile and ability to enhance fruit-forward flavors, particularly in sparkling waters and functional drinks aimed at health-conscious consumers. The competitive challenge is most pronounced in Europe and North America, where regulatory standards and consumer preferences favor natural acids. However, phosphoric acid maintains advantages in cola and certain dairy applications due to its unique chemistry, particularly its ability to complex with calcium ions without causing precipitation, which remains difficult to replicate.

Health concerns from excessive consumption

Epidemiological studies linking phosphoric acid consumption to health issues, such as bone density loss, kidney stone formation, and dental erosion, are limiting demand growth in developed markets and influencing global regulatory discussions. This constraint affects the market in two ways: directly, by reducing volumes as consumers shift to citric acid-based alternatives, and indirectly, by exerting margin pressure as beverage manufacturers reformulate premium product lines to avoid negative health perceptions. Consequently, phosphoric acid is increasingly confined to value-tier products with lower pricing power. The impact is most significant in North America and Europe, where health awareness is high. However, similar reformulation trends are emerging in urban areas of China and India, driven by middle-class consumers prioritizing wellness attributes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Purity Grade: Concentration Drives Application Fit

Food grade 85% phosphoric acid accounted for 54.69% of the market share in 2025, highlighting its role as the standard concentration for applications such as cola syrup production, processed cheese emulsification, and precise pH adjustment in pharmaceutical-grade food ingredients. This concentration offers a balance between handling efficiency, where higher concentrations reduce shipping costs per unit of active ingredient, and formulation flexibility, as it can be diluted on-site to meet specific application needs without requiring specialized storage facilities.

Food grade 80% phosphoric acid is projected to be the fastest-growing segment, with a CAGR of 5.95% through 2031. This growth is driven by its adoption in cost-sensitive markets, where the 5-percentage-point difference in concentration provides cost savings while maintaining functionality in less demanding applications, such as pH adjustment in processed meats and certain dairy desserts. Regulatory oversight from organizations like the FDA and EFSA ensures that competition in purity grades focuses on meeting or exceeding minimum standards rather than pursuing ultra-high concentrations. This dynamic benefits established producers with advanced purification capabilities over low-cost entrants relying on minimal processing.

By Application: Beverages Dominate, Food Accelerates

Beverages accounted for 48.10% of the market share in 2025, driven by cola's continued reliance on phosphoric acid for its distinct flavor profile. However, the food segment is projected to grow at a compound annual growth rate (CAGR) of 6.89% through 2031, surpassing beverages due to the increasing use of phosphoric acid in dairy, processed meat, and ready-to-eat meal applications, particularly in Asia-Pacific and Africa. Within the beverage segment, cola represents the majority of phosphoric acid usage, with typical formulations containing 0.05% to 0.08% phosphoric acid by volume to maintain pH levels between 2.4 and 2.6.

This range ensures microbial stability while preserving palatability. However, health-conscious reformulations are limiting growth in the beverage segment, as premium brands shift to citric or malic acids to avoid negative health perceptions. As a result, phosphoric acid usage remains concentrated in value-tier cola and traditional formulations. The "Other Applications" category, which includes fats, shortenings, and jellies, is experiencing modest growth as phosphoric acid's antioxidant properties are utilized to prevent rancidity in lipid-rich formulations.

Geography Analysis

North America accounted for 28.56% of the market share in 2025, supported by the United States' extensive wet-process phosphoric acid infrastructure and established cola consumption patterns. However, the region's growth is slowing due to health-conscious reformulations and the substitution of alternative acids, which are reducing demand for beverage-grade phosphoric acid. Canada is emerging as a niche player in high-purity production. In December 2024, First Phosphate licensed Prayon technology for a 600-tonne-per-day plant aimed at premium food-grade markets. This initiative leverages Canada's low-carbon electricity grid to produce "green" phosphoric acid with a distinct sustainability profile.

The Asia-Pacific region is the fastest-growing market, with a CAGR of 6.18% projected through 2031. Growth is driven by the simultaneous expansion of domestic production capacity in China and India, alongside increasing demand for packaged foods and beverages. Japan and South Korea represent mature, high-value markets where stringent food safety standards favor imports from established producers. However, local demand in these countries is constrained by aging populations and declining per-capita beverage consumption. In Australia, the market remains import-dependent due to the absence of significant domestic phosphoric acid production. Nevertheless, Australia's role as a major phosphate rock exporter to Asia-Pacific presents opportunities for downstream integration if regional demand justifies investment.

Europe's market is influenced by stringent environmental regulations and health-driven reformulations. The European Food Safety Authority's quantum satis designation for phosphoric acid (E338) provides regulatory flexibility, but consumer preferences are increasingly shifting toward citric and lactic acids in premium product lines. South America's market is primarily supported by Brazil's large beverage industry and Argentina's processed food sector. However, both countries rely heavily on imports from Morocco and the United States due to limited domestic phosphoric acid production capacity.

Competitive Landscape

The food-grade phosphoric acid market is moderately consolidated, with a few vertically integrated phosphate producers, Mosaic, OCP, ICL, and Ma'aden, dominating significant wet-process capacity. These companies leverage their scale and integration to maintain a stronghold in the market. However, regional specialists and toll manufacturers continue to carve out competitive niches, particularly in high-purity and specialty-grade segments. This balance between large-scale producers and regional players creates a dynamic market environment where innovation and specialization play critical roles in maintaining competitiveness. Patent activity in the market underscores a focus on improving wet-process efficiency and reducing impurities, with notable advancements such as Ecophos' U.S. Patent 8,425,872 B2. This patent details methods for producing high-purity phosphoric acid from low-grade phosphate rock, a process that not only reduces feedstock costs but also meets stringent food safety standards, highlighting the industry's emphasis on cost efficiency and regulatory compliance.

Emerging disruptors in the market include regional producers in India and Southeast Asia, who are increasingly investing in food-grade production capacity. These investments aim to address growing import-substitution demand in their respective regions, enabling these producers to reduce reliance on imports while catering to local markets. This shift is creating competitive pressure on established exporters, who are now compelled to differentiate themselves through enhanced service offerings, traceability, and technical support rather than relying solely on price competitiveness. The entry of these regional players is reshaping the competitive landscape, as they bring localized expertise and cost advantages to the market, challenging the dominance of traditional exporters and encouraging innovation across the supply chain.

The competitive intensity is particularly high in commodity-grade concentrations of 75% to 80%, where Chinese exports exert significant downward pressure on prices. This segment is characterized by price sensitivity and high-volume demand, making it a challenging space for producers to maintain margins. In contrast, premium-grade 85% and ultra-high-purity segments remain relatively insulated from such pressures due to technical barriers and stringent brand-owner qualification processes. These segments favor incumbents with established track records and proven expertise, as customers prioritize quality, reliability, and compliance with strict standards. As a result, producers in these premium segments benefit from higher margins and long-term customer relationships, reinforcing their position in the market despite the competitive challenges in lower-grade segments.

Food Grade Phosphoric Acid Industry Leaders

-

Brenntag AG

-

OCP SA

-

Guangxi Qinzhou Capital Success Chemical Co. Ltd

-

Aditya Birla Group

-

Innophos Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Prayon inaugurated a new sodium hexametaphosphate (SHMP) production unit at its Engis site in Belgium. This development represents a significant capacity expansion for one of its key phosphate derivatives, widely used in food, beverage, and industrial applications. The facility, built with an investment exceeding EUR 30 million, adds 10,000 tonnes per year of production capacity, effectively doubling Prayon’s SHMP output alongside its existing site in France.

- June 2023: Gujarat Alkalies and Chemicals Ltd. (GACL) began commercial production of purified phosphoric acid at its Dahej chemical complex. This marked a major expansion of its specialty phosphates portfolio to include high-purity, food-grade phosphoric acid suitable for food and beverage applications. By December 2023, GACL dispatched its first consignment of food-grade phosphoric acid, demonstrating the facility’s successful transition from commissioning to commercial supply and its ability to meet the quality and regulatory standards required by food manufacturers.

- January 2023: Prayon successfully completed the acquisition of Febex, enhancing its position in high-purity phosphoric acid production and facilitating entry into the electronics and pharmaceutical markets. This strategic acquisition broadens Prayon’s portfolio beyond traditional industrial and food-grade phosphates to include sectors requiring exceptionally high chemical purity and technical performance.

Global Food Grade Phosphoric Acid Market Report Scope

Phosphoric acid is a strong inorganic acid that is colorless and odorless. It is an indispensable additive, often found in colas and other dark-colored carbonated sodas. The strength and flavor hold a neutral profile of food-grade phosphoric acid, making it a desirable choice for low-pH foods and beverages.

The food-grade phosphoric acid market is segmented by application and geography. Based on the application, the market is segmented into food, beverage, and pharmaceutical. The study also covers an analysis of the major regions such as North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Food Grade 85% |

| Food Grade 75% |

| Food Grade 80% |

| Others |

| Food | Dairy Products |

| Processed Meat | |

| Others | |

| Beverages | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Purity Grade | Food Grade 85% | |

| Food Grade 75% | ||

| Food Grade 80% | ||

| Others | ||

| By Application | Food | Dairy Products |

| Processed Meat | ||

| Others | ||

| Beverages | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the food-grade phosphoric acid market in 2031?

The market is expected to reach USD 3.55 billion by 2031.

Which application currently dominates demand?

Beverages, primarily cola formulations, held 48.10% share in 2025.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to post a 6.18% CAGR, supported by capacity additions in China and India.

Why is Food Grade 85% important?

It combines high assay with versatility, delivering 54.69% market share in 2025 and meeting stringent impurity limits.

Page last updated on: