Philippines Remittances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

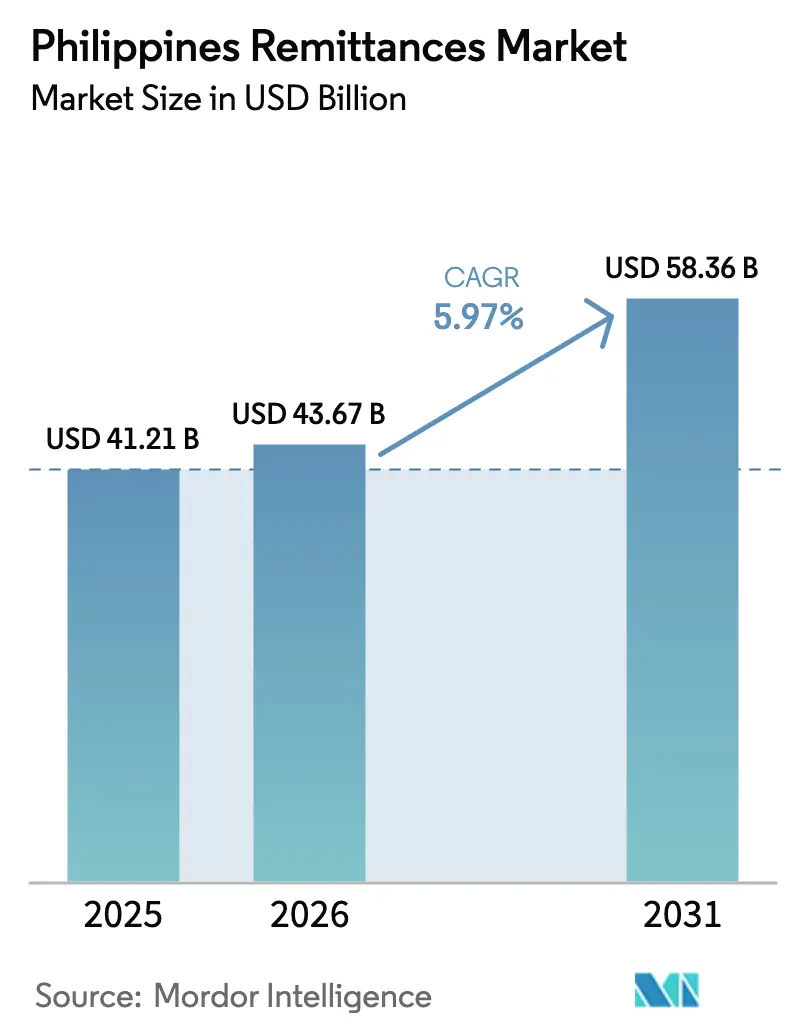

| Base Year Market Size (2025) | USD 41.21 Billion |

| Market Size (2026) | USD 43.67 Billion |

| Market Size (2031) | USD 58.36 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Remittances Market Analysis by Mordor Intelligence

The Philippines remittances market size was valued at USD 41.21 billion in 2025 and estimated to grow from USD 43.67 billion in 2026 to reach USD 58.36 billion by 2031, at a CAGR of 5.97% during the forecast period (2026-2031). Foreign exchange gains from peso weakness, strong global demand for Filipino labor, and rising digital wallet adoption underpin the growth outlook. A large global diaspora exceeding 2.1 million overseas Filipino workers (OFWs) continues to remit steadily, making the corridor the world’s fourth-largest and supporting 8.3% of national GDP[1]Bangko Sentral ng Pilipinas, “Overseas Filipinos’ Cash Remittances 2024,” bsp.gov.ph. Rapid channel digitalization—digital payments already captured 52.8% of domestic retail transactions in 2024—lowers transfer friction and attracts new users. Geographic concentration in the United States, Singapore, and Saudi Arabia remains high, yet emerging corridors across the Gulf Cooperation Council (GCC) and ASEAN are expanding on the back of new labor agreements and infrastructure projects.

Key Report Takeaways

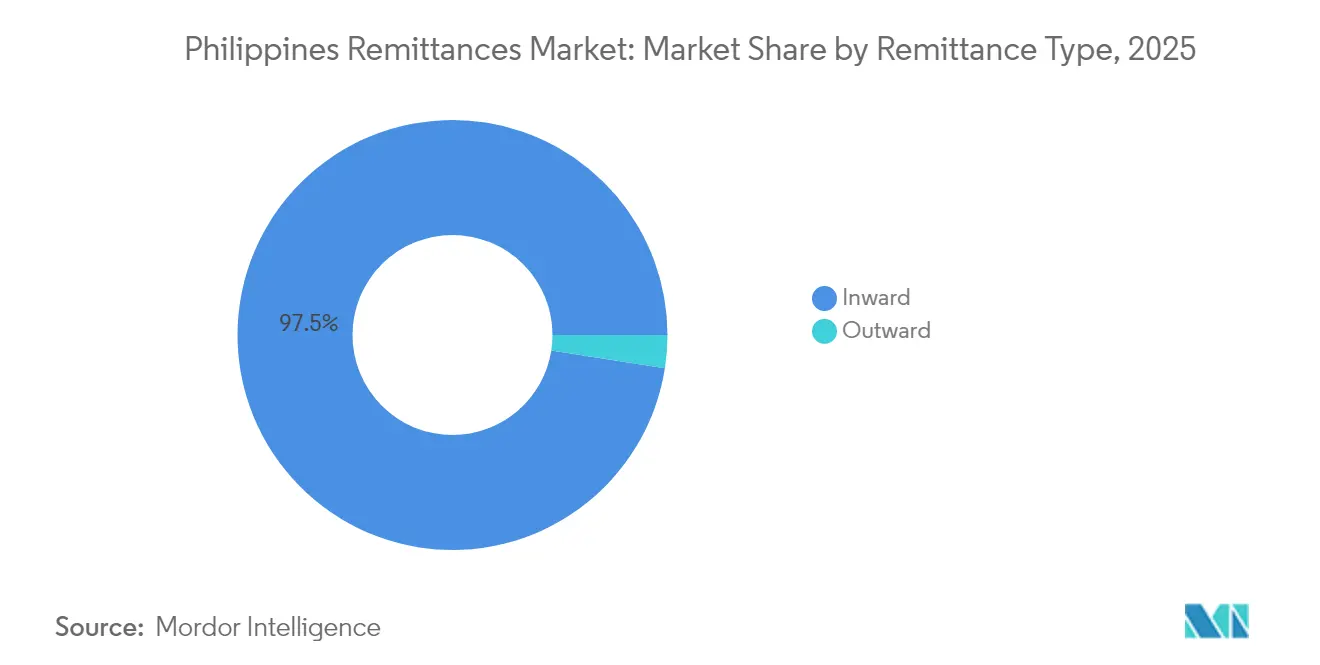

- By remittance type, inward flows commanded 97.52% of the Philippines' remittances market share in 2025, while outward flows are expected to expand at a 6.88% CAGR through 2031.

- By channel, bank transfers led with a 46.55% share of the Philippines' remittances market in 2025; digital wallets are set to grow at a 12.18% CAGR over 2026-2031.

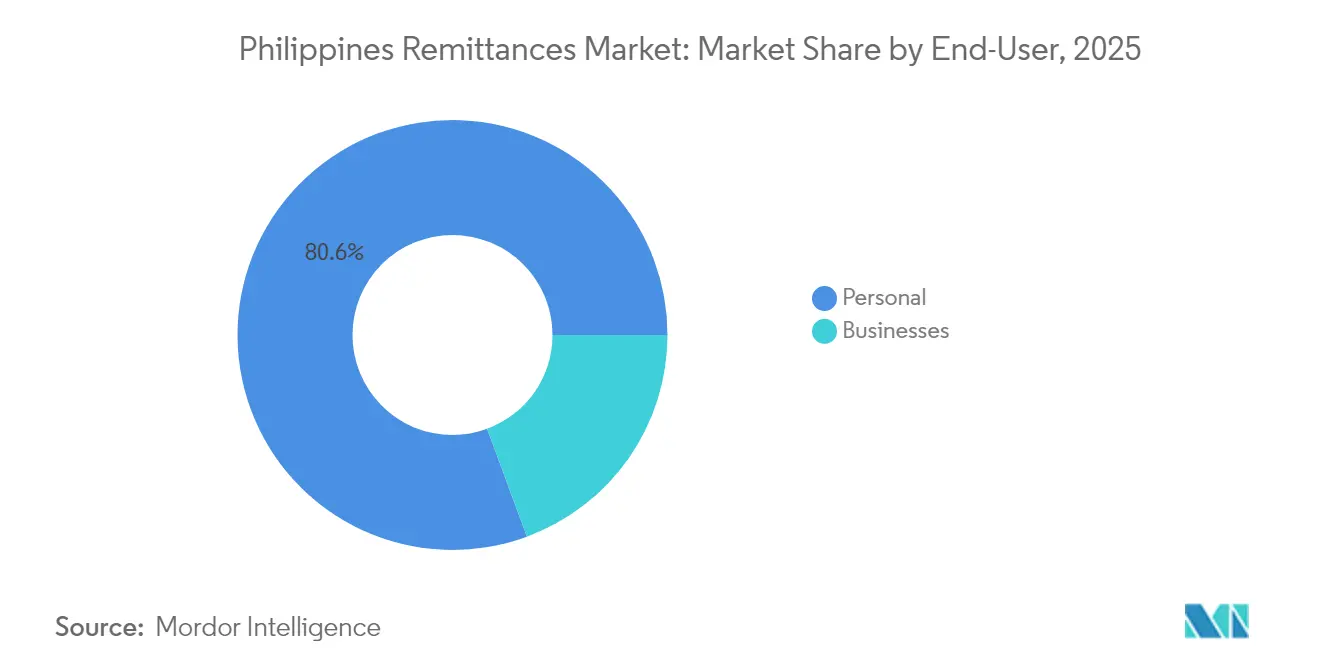

- By end-user, personal transfers accounted for 80.63% of the Philippines' remittances market size in 2025, whereas business transfers are projected to rise at an 8.05% CAGR through 2031.

- By mode of transfer, online channels secured 49.12% of the total value of the Philippines' remittances market in 2025 and are forecasted to post a 9.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Philippines representing one among them. The global report on remittance market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Philippines Remittances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large overseas Filipino workforce | +1.8% | Global, concentrated in US, GCC, ASEAN | Long term (≥ 4 years) |

| Strong demand for Filipino workers abroad | +1.2% | GCC, Singapore, healthcare sectors globally | Medium term (2-4 years) |

| Peso weakness amplifying peso-value of US-dollar remittances | +0.9% | US-Philippines corridor primarily | Short term (≤ 2 years) |

| Rapid adoption of digital wallets & bank-to-wallet rails | +1.5% | National, urban centers leading rural adoption | Medium term (2-4 years) |

| ASEAN “Nexus” instant cross-border payment rail (live 2026) | +0.7% | ASEAN region, spillover to broader Asia-Pacific | Long term (≥ 4 years) |

| Diaspora-backed micro-finance & local-investment schemes | +0.4% | Rural Philippines, provincial centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Large Overseas Filipino Workforce

Over 2.1 million OFWs were deployed worldwide in 2024, underpinning long-run stability for the Philippines' remittances market [2]Department of Migrant Workers, “OFW Stock Estimate 2024,” dmw.gov.ph. Government programs diversify destinations beyond traditional markets, mitigating corridor risk while unlocking new wage opportunities in healthcare, maritime, and engineering. Higher-skilled OFWs now remit larger average ticket sizes, lifting aggregate volumes. Land-based workers on multi-year contracts provide predictable flows that smooth domestic consumption cycles. The workforce’s global spread cushions the market from single-country shocks, sustaining long-term growth momentum.

Strong Demand for Filipino Workers Abroad

Persistent nursing shortfalls in developed economies and large GCC infrastructure projects create robust demand for Filipino expertise. Singapore’s healthcare build-out and maritime hub status similarly attract Filipino professionals through streamlined deployment programs. Wage premiums elevate per-capita remittances, reinforcing household income security at home. Filipino seafarers, who constitute roughly 25% of the global merchant fleet, ensure a constant pipeline of maritime transfers. The resulting employment visibility supports optimistic forecasts for the Philippines' remittances market.

Peso Weakness Amplifying Peso-Value of US-Dollar Remittances

Continued peso volatility boosts local purchasing power for USD-denominated transfers, effectively increasing real income for recipient families without higher nominal sends. The central bank’s managed-float policy allows currency flexibility, keeping this amplification channel intact. OFWs respond by timing transfers through real-time digital platforms to capture favorable rates. Rising peso value of inflows also strengthens the country’s balance-of-payments position, reinforcing macroeconomic stability, which is essential to the Philippines' remittances market expansion[3]International Monetary Fund, “Philippines: External Sector Report 2024,” imf.org.

Rapid Adoption of Digital Wallets & Bank-to-Wallet Rails

Digital payments exceeded half of retail transactions in 2024, a landmark for nationwide financial inclusion. Platforms such as GCash surpassed profitability targets while processing multibillion-dollar volumes, validating the fintech model. The National Retail Payment System mandates interoperability, encouraging wallet-to-wallet remittances that settle instantly. Over 15,000 cash agents extend digital services to rural areas, narrowing the urban-rural gap. These factors elevate user confidence and accelerate channel migration inside the Philippines remittances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High transaction costs vs 3% UN SDG target | -1.1% | Global corridors, particularly smaller MTOs | Medium term (2-4 years) |

| Limited access to formal financial services in rural areas | -0.8% | Rural Philippines, provincial areas | Long term (≥ 4 years) |

| Host-country labour-localisation policies (e.g., GCC, SG) | -0.6% | GCC countries, Singapore, selective markets | Medium term (2-4 years) |

| Surge in cyber-fraud & account-takeover attacks on OFWs | -0.9% | Global, digital-first channels primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Transaction Costs vs 3% UN SDG Target

Average corridor fees exceeded 4% in 2024, well above the 3% UN goal, and global costs averaged 6.4%[4]World Bank, “Remittance Prices Worldwide, Issue 43,” worldbank.org. Lower-income OFWs feel the greatest burden, driving some to informal, untracked channels. Regulatory compliance costs and legacy infrastructure pressures keep traditional money-transfer fees high. The Bangko Sentral ng Pilipinas (BSP) has capped small-value fees, but adoption across all providers is uneven, diluting market impact. Until broader fee harmonization materializes, cost friction will temper the Philippines remittances market velocity.

Surge in Cyber-Fraud & Account-Takeover Attacks on OFWs

A 13.4% digital-fraud rate placed the Philippines second globally in 2024, resulting in PHP 409 million in losses. Fraudsters target OFWs through phishing and scams, undermining trust in digital channels. Providers now invest heavily in AI-driven monitoring, elevating operating expenses that squeeze smaller players. Government agencies have launched joint cybercrime initiatives, yet adversaries continuously evolve tactics. Persistent fraud exposure remains a near-term drag on digital uptake within the Philippines remittances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Remittance Type: Inward Dominance Sustains Growth Prospects

Inward remittances commanded 97.52% of the Philippines' remittances market share in 2025, underscoring the market’s net-recipient nature. This predominance stems from deep family ties that compel OFWs to remit regularly for household support. The Philippines' remittances market size tied to inward flows is forecast to climb alongside wage gains and corridor diversification. Outward remittances, though small, are projected to grow at 6.88% CAGR as diaspora entrepreneurs fund overseas ventures and educational expenses. Providers that develop two-way transfer capabilities stand to capture emerging outward-flow opportunities.

Outward activity reflects the diaspora’s transition from pure labor supply to global business participation. Digital wallets now offer real-time outward services, enabling Filipino entrepreneurs to pay suppliers abroad without conventional bank delays. Such bidirectional tools blur the boundary between remittance and trade finance. As the economic profile of OFWs matures, the Philippines' remittances market will increasingly encompass capital-flow diversity beyond household support, reinforcing overall resilience.

By Channel: Digital Wallets Narrow the Lead

Bank transfers held a 46.55% share of the Philippines' remittances market in 2025, benefiting from legacy trust, robust compliance frameworks, and suitability for higher-value transactions. However, digital wallets are projected to grow at a 12.18% CAGR, steadily closing the gap and redefining user expectations for speed and cost. The Philippines remittances market size routed through wallets is set to expand as interoperability rules reduce switching friction. Traditional banks respond by integrating wallet rails, signaling converging channel models. Money-transfer operators (MTOs) face shrinking margins as fintech rivals scale at lower cost.Digital platforms leverage intuitive interfaces, instant credit, and ancillary services—such as micro-insurance—to deepen customer stickiness. Partnerships between wallets and global MTOs further extend reach, especially in high-volume corridors like the United States. As cash-to-wallet services expand in rural regions, the Philippines' remittances industry realigns around omnichannel ecosystems where digital and physical outlets coexist.

By End-User: Household Transfers Remain Core, Business Flows Accelerate

Personal transfers accounted for 80.63% of the Philippines' remittances market in 2025, reflecting cultural obligations for family support. These flows finance consumption, education, and healthcare, injecting stable demand into local economies. Business remittances, though smaller, are forecasted to grow at 8.05% CAGR through 2031 as Filipino-owned enterprises scale abroad. Formalizing trade payments through regulated channels reduces counterparty risk, encouraging SMEs to shift away from informal arrangements.Growth in business flows is amplified by bilateral trade agreements that simplify cross-border documentation. Digital providers cater to SMEs with real-time dashboards, invoice matching, and multicurrency settlement, features often absent from traditional MTO services. As entrepreneurship among overseas Filipinos rises, the Philippines' remittances market gains a new demand layer that complements household transfers.

By Mode of Transfer: Online Channels Achieve Parity

Online transfers captured 49.12% of the Philippines' remittances market share in 2025, nearly matching offline channels, and are projected to expand at a 9.86% CAGR. Pandemic-induced behavioral shifts normalized digital use, and improved broadband penetration sustains momentum. Hybrid models allow users to initiate a transfer digitally and collect cash at an agent, blending convenience with liquidity. Offline channels retain relevance among cash-preferring recipients in rural areas, but assisted-digital kiosks are narrowing the divide.Government-backed cash-agent networks now offer digital onboarding and biometric verification, accelerating rural inclusion. As smartphone adoption climbs, user familiarity with QR payments further supports online channel growth. The Philippines' remittances market will likely see online volumes surpass 60% of the total value before 2030 if current trajectories hold.

Geography Analysis

North America maintains primacy within the Philippines' remittances market, with the United States contributing a significant amount of total inflows in 2024, thanks to a large Filipino-American population and robust healthcare recruitment. Singapore follows as a key node, leveraging geographic proximity and bilateral employment agreements that streamline worker deployment. The GCC region—led by Saudi Arabia and the United Arab Emirates—complements the top corridors by channeling infrastructure-related wages back home.

Regional diversification is accelerating. ASEAN neighbors such as Malaysia and Thailand now host growing Filipino professional communities, fostered by the forthcoming ASEAN Nexus payment rail that promises sub-3% fees and real-time settlement. Europe’s United Kingdom attracts nurses and maritime officers, adding another stable corridor. Scandinavian and Eastern European countries, grappling with aging demographics, are opening new demand for Filipino caregivers, further spreading corridor risk.

Emergent destinations in Africa and Latin America remain modest but strategically important. Filipino educators, oil-and-gas engineers, and IT professionals are venturing into Nigeria, Brazil, and Chile under targeted recruitment schemes. This broadening footprint underpins the Philippines' remittances market against localized economic downturns. Digital platforms adapt by tailoring corridor-specific pricing and compliance protocols, ensuring seamless transfers regardless of destination. The International Monetary Fund highlights such geographic spread as a buffer for external-sector stability, reinforcing confidence in remittance-led foreign-currency inflows.

Competitive Landscape

The market remains fragmented, yet channel disruption is re-sorting competitive tiers. Traditional MTOs still command strong brand awareness, but rising compliance costs and flat volume growth compress margins. Local pawnshops and courier groups leverage extensive branch networks to retain cash-preferring customers, especially in provincial areas where 70% of towns lack a bank branch. Domestic banks, including BDO Unibank, which posted PHP 82 billion in 2024 profit, have the balance-sheet strength to invest in end-to-end remittance platforms.

Fintech scale-ups such as GCash and Maya capture younger, mobile-native users through low fees, instant credit, and ancillary financial services. Strategic partnerships—GCash with Ria Money Transfer and Viamericas, Maya with TerraPay—expand reach to 160 countries while preserving wallet-based convenience. Regulatory convergence via the National Retail Payment System enforces interoperability, commoditizing raw transaction processing and shifting competition toward value-added services like micro-loans and insurance.

Rural penetration remains a battleground. Over 15,000 agent outlets now enable cash-in and cash-out for digital wallets, challenging rural pawnshops for foot traffic. New entrants such as Higala build inclusive instant-payment systems targeting bank co-op networks, threatening established gateway providers. Competitive pressure is expected to intensify once the ASEAN Nexus rail launches, as domestic players must match region-wide cost efficiencies to defend their Philippines remittances market positions.

Philippines Remittances Industry Leaders

Western Union

MoneyGram

Ria / Euronet

BDO Unibank

WorldRemit Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Higala secured USD 2.8 million seed funding to scale an inclusive instant-payment network for Philippine FIs.

- February 2025: GCash partnered with Viamericas to enable real-time transfers from the United States and Canada directly into GCash wallets, reinforcing its lead in the largest corridor to the Philippines.

- January 2025: GCash rolled out Express Send with a 100% refund guarantee for unauthorized transactions, bolstering user confidence in digital channels.

- March 2024: Visa and Western Union expanded their collaboration to streamline cross-border money transfers worldwide.

Philippines Remittances Market Report Scope

The Philippines Remittances Market is defined as the financial system facilitating the transfer of money from Overseas Filipino Workers (OFWs) and expatriates back to their families in the Philippines.

The Philippines Remittances Market is segmented into remittance type, channel, end-use, and mode of transfer. By remittance type, the market is segmented into inward remittances and outward remittances. By channel, the market is segmented into bank transfers, money transfer operators, digital wallets and mobile payment platforms, and other channels. By end-use, the market is segmented into personal, businesses, and others. By mode of transfer, the market is segmented into online and offline. The report offers market size and forecasts in terms of value in (USD) for all the above segments.

| Inward |

| Outward |

| Bank Transfers |

| Money Transfer Operators (MTOs) |

| Digital Wallet and Mobile Payment Platforms |

| Other Channels |

| Personal |

| Businesses |

| Online |

| Offline |

| By Remittance Type | Inward |

| Outward | |

| By Channel | Bank Transfers |

| Money Transfer Operators (MTOs) | |

| Digital Wallet and Mobile Payment Platforms | |

| Other Channels | |

| By End-User | Personal |

| Businesses | |

| By Mode of Transfer | Online |

| Offline |

Key Questions Answered in the Report

What is the current value of the Philippines' remittances market?

The market is valued at USD 43.67 billion in 2026 and is projected to rise to USD 58.36 billion by 2031.

How fast is the Philippines' remittances market growing?

The market is forecasted to expand at a 5.97% CAGR between 2026 and 2031, supported by digitalization and sustained OFW deployment.

Which channel is growing the fastest?

Digital wallets and mobile payments are expected to advance at a 12.18% CAGR, outpacing bank transfers and traditional MTO outlets.

What share do personal transfers hold?

Personal remittances represented 80.63% of the total value in 2025, reflecting the continued importance of family support among OFWs.

How will the ASEAN Nexus payment rail affect costs?

The rail, due in July 2026, targets corridor fees below 3%, which would materially lower transfer costs from current averages above 4%.

Why are cybersecurity risks a restraint for market growth?

A 13.4% fraud rate in 2024 raised compliance and security expenses for providers and undermined user trust, slowing digital-channel adoption.

Page last updated on: