Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

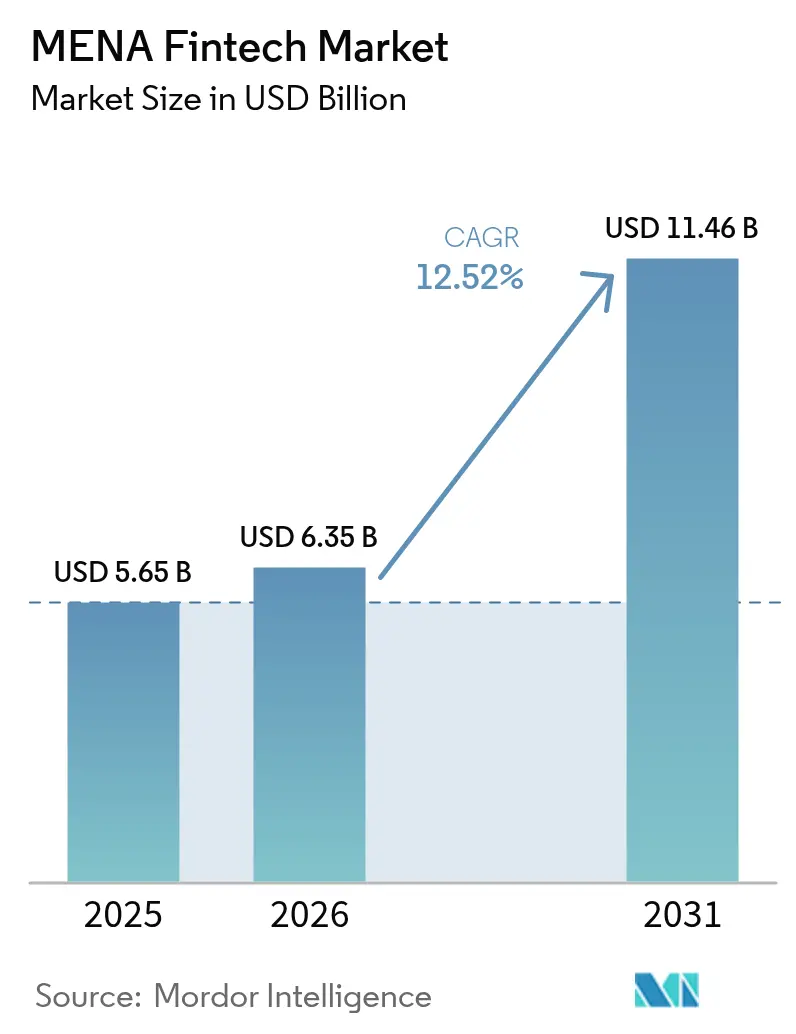

| Base Year Market Size (2025) | USD 5.65 Billion |

| Market Size (2026) | USD 6.35 Billion |

| Market Size (2031) | USD 11.46 Billion |

| Growth Rate (2026 - 2031) | 12.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MENA Fintech Market Analysis by Mordor Intelligence

MENA fintech market size in 2026 is estimated at USD 6.35 billion, growing from 2025 value of USD 5.65 billion with 2031 projections showing USD 11.46 billion, growing at 12.52% CAGR over 2026-2031. A surge in cash-lite policy mandates, broad smartphone availability, and growing venture-capital inflows are expanding the addressable base for digital financial services. Central-bank digital-currency (CBDC) pilots in the GCC and Egypt are modernizing payment rails, while regulatory sandboxes in Saudi Arabia, the UAE, and Jordan shorten product launch cycles. At the same time, e-commerce, gig-economy, and remittance corridors are fuelling embedded-finance use cases. Industry participants respond through platform diversification and cross-border partnerships that create new revenue streams and consolidate fragmented positions.

Key Report Takeaways

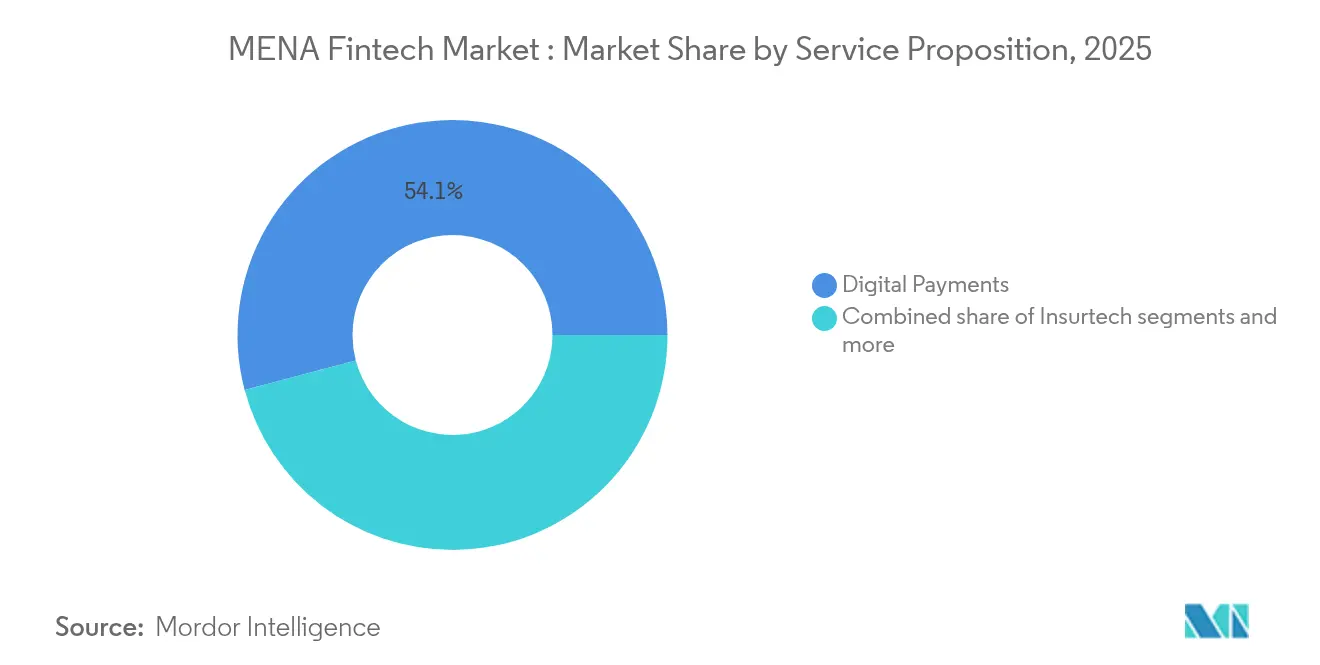

- By service proposition, digital payments captured 54.12% of the MENA fintech market share in 2025, while the MENA fintech market size for digital lending and financing is expected to grow fastest at a CAGR of 17.74% during 2026–2031.

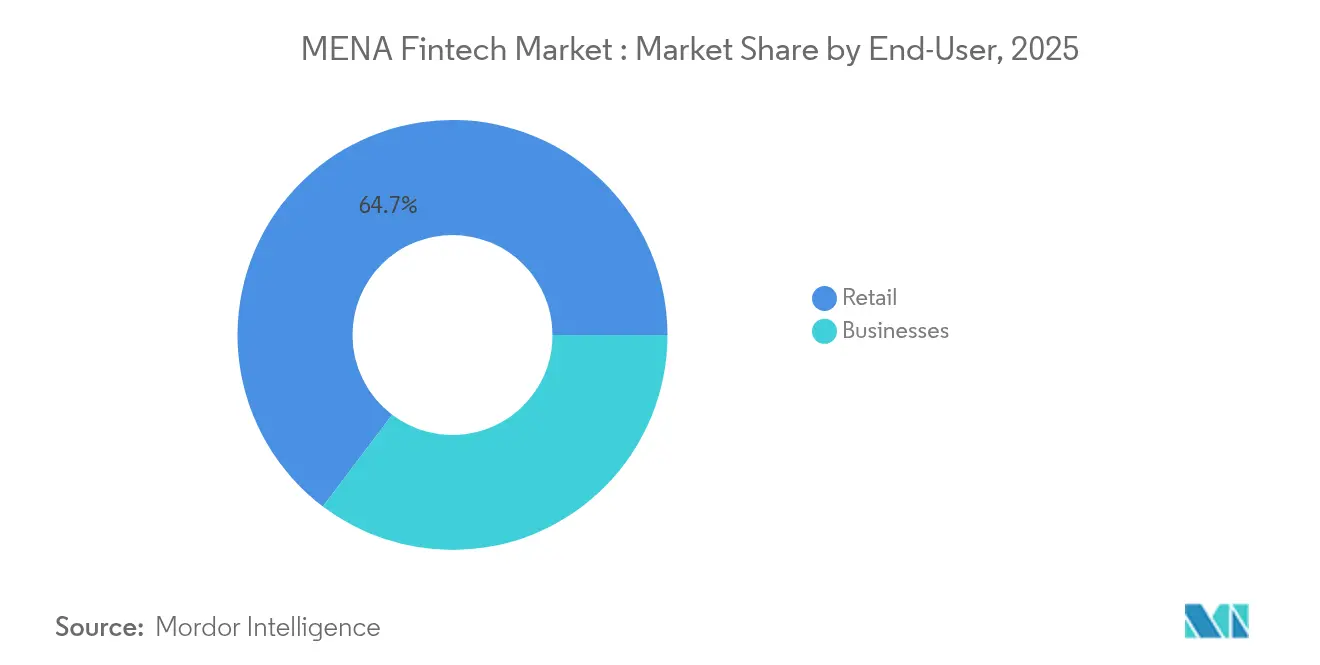

- By end-user, retail accounted for 64.70% of the MENA fintech market share in 2025, with the MENA fintech market size for businesses projected to rise at the highest CAGR of 14.18% through 2031.

- By user interface, mobile apps represented 79.62% of the MENA fintech market share in 2025, while the MENA fintech market size for POS/IoT devices is forecast to expand at a CAGR of 16.60% between 2026 and 2031.

- By geography, GCC countries held 62.75% of the MENA fintech market share in 2025, while the MENA fintech market size in North Africa is anticipated to grow at the fastest rate of 17.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MENA Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cash-lite & financial-inclusion mandates | +2.1% | GCC and North Africa core, Levant secondary | Medium term (2-4 years) |

| Mobile & internet penetration surge | +1.8% | Whole MENA, strongest in GCC | Short term (≤ 2 years) |

| VC funding & sandbox momentum | +1.5% | GCC primary, North Africa emerging | Medium term (2-4 years) |

| CBDC pilots enabling cross-border rails | +1.2% | GCC and Egypt primary, regional spill-over | Long term (≥ 4 years) |

| Embedded-finance demand from e-commerce & gig platforms | +0.9% | Urban centers across MENA, GCC leading | Short term (≤ 2 years) |

| Instant-payment rails unlocking alternative lending data | +0.8% | GCC and Egypt advanced, North Africa following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Cash-Lite & Financial-Inclusion Mandates Accelerate Fintech Demand

Saudi Arabia targets 70% cashless transactions by 2030, Egypt aims to bank 50% of adults by 2025, and the UAE streamlined licensing in 2024. These targets provide clear metrics for adoption and reduce go-to-market friction for private players[1]AlHuda CIBE, “The Outlook of Islamic Finance in 2025 Appears Promising,” alhudacibe.com. . Sandboxes in Jordan further cut regulatory risk, helping startups scale without prohibitive compliance spend. As governments digitize payroll and welfare transfers, consumer familiarity with e-wallets rises, lowering acquisition costs. The policy push also incentivizes retailers to deploy contactless acceptance, enlarging acceptance networks. Collectively, mandates create a virtuous circle that widens the MENA fintech market.

Mobile & Internet Penetration Surge Enables Mobile-First Financial Access

Smartphone penetration tops 80% in GCC states, turning mobiles into the default banking channel[2]MeaWallet, “The State of Tokenization in MENA,” meawallet.com. . The UAE already sees digital wallets covering 18% of POS spend, on track for 33% by 2027. Egypt and Morocco extend reach through telco-based agent models, bypassing branch infrastructure and shrinking operating costs. Gen Z users account for 23% of regional e-commerce spend via digital wallets, establishing lasting payment habits. Growing 4G/5G coverage in rural North Africa enables remote KYC onboarding, unlocking new customer pools. The mobile-first model thus propels rapid share gains across consumer cohorts.

VC Funding & Sandbox Momentum Fuel Startup Formation

Venture capital funding peaked at USD 4.2 billion in 2023 across Middle East fintech, creating capital availability that enables startup formation and scale-up activities across the region. Regulatory sandboxes in Saudi Arabia, UAE, and Jordan provide controlled environments for fintech innovation, with SAMA approving multiple neobanking licenses in 2024. The emergence of 4 regional fintech unicorns - Tabby, Tamara, MNT-Halan, and Papara - demonstrates investor confidence in MENA market potential and creates precedent for future funding rounds. Y Combinator's investment in 30+ MENA fintechs signals international investor interest and provides startups with Silicon Valley expertise and network access that accelerates product development cycles.

CBDC Pilots Enabling Cross-Border Rails Create Common API Infrastructure

Central bank digital currency initiatives across the UAE, Saudi Arabia, Qatar, and Egypt establish an interoperable payment infrastructure that reduces cross-border transaction costs and settlement times. Saudi Arabia joined the mBridge project in 2024, which establishes a multi-CBDC platform for international settlements that bypasses traditional correspondent banking networks and reduces transaction costs by up to 80%. UAE's successful completion of first CBDC payments in 2024 demonstrates technical feasibility and regulatory readiness for broader implementation, creating precedent for regional adoption. These CBDC rails enable fintech providers to offer instant cross-border remittances and trade finance solutions without maintaining correspondent banking relationships, reducing operational complexity and capital requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory fragmentation across jurisdictions | -1.9% | Pan-MENA, peak impact on cross-border players | Medium term (2-4 years) |

| Cash-centric habits inflating CAC in N. Africa | -1.4% | North Africa primary, rural GCC secondary | Long term (≥ 4 years) |

| Scarcity of Arabic AI/ML risk-scoring datasets | -1.1% | Arabic-speaking markets, North Africa core | Medium term (2-4 years) |

| Legacy core-bank IT bottlenecks | -0.7% | Established banking markets, GCC and Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Fragmentation Across Jurisdictions Increases Compliance Burden

Nineteen different licensing regimes require fintechs to form market-specific entities, adding 15-25% to overheads versus unified frameworks. Disparate capital and data-localization rules hinder passporting and delay regional scaling. Larger incumbents absorb the cost but startups face resource strain, limiting innovation diversity. Lack of mutual recognition also hampers cross-border open-API linkage, creating integration dead-zones. Investors price the risk into valuations, nudging consolidation as a workaround for multi-country reach.

Cash-Centric Habits Inflate Customer-Acquisition Costs in North Africa

Cash still dominates more than 80% of Egyptian retail spending, forcing digital players to fund education campaigns and cash-in/out agent grids[3]Arabian Business, “Cross-Border Remittances – Latest News,” arabianbusiness.com. . Marketing outlays inflate CAC by up to 60% against GCC benchmarks. Hybrid models that accept cash erode gross margins, extending breakeven timelines. In rural Morocco, low digital literacy slows wallet activation despite growing 4G coverage. Fintechs must also invest in fraud guarantees to offset trust deficits, further compressing unit economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Digital Payments Dominate While Lending Scales Fast

Digital payments controlled 54.12% of MENA fintech market share in 2025, underpinned by near-ubiquitous smartphone wallets and aggressive merchant-acquiring incentives. The sub-segment added new rails such as QR and tokenized wallet checkout, further cementing stickiness. Digital lending, though smaller, is growing at an 17.74% CAGR on the strength of real-time alternative-data scoring. Fawry’s EGP 1 billion disbursement surge in 2025 illustrates payments-to-credit adjacency.

Robo-advisory and insurtech expand via API-first distribution, while neobanks like STC Bank convert wallet bases into full-service accounts. Regulatory sandboxes allow parametric and usage-based policies, fostering experimentation. Cross-sell synergies emerge as payments brands add credit, investment, and insurance tabs within the same app, stretching user lifetime value. The diversification push points to escalating platform convergence across the MENA fintech market.

By End-User: Retail Remains Core but Business Uptake Accelerates

Retail users held 64.70% of segment spend in 2025, anchored by mass-market wallets and BNPL checkout adoption. Yet business demand is climbing at 14.18% CAGR as SMEs adopt embedded-finance modules for invoicing, payroll, and supply-chain finance. Gig-economy platforms integrate instant pay and micro-loans, smoothing irregular earnings cycles. Merchant dashboards import real-time POS data into credit-scoring engines, shortening loan approval to minutes. Enterprises favor fintech rails for cross-border vendor payouts, leveraging CBDC corridors in the GCC. As a result, the MENA fintech market sees a steady re-balance toward B2B monetization.

By User Interface: Mobile Leads, POS & IoT Ascend

Mobile apps captured 79.62% of interface traffic in 2025, reflecting user preference for on-demand micro-transactions. Tokenization upgrades cut fraud rates and raise wallet-checkout share to a projected 34% of e-commerce spend by 2027. Meanwhile, smart-POS and IoT terminals grow at 16.60% CAGR as merchants deploy contactless tap-to-phone and soft-POS solutions. Fawry’s dual CPoC/MPoC accreditation in 2024 positions it to scale software-only acceptance. Vehicle-based toll and parking payments illustrate IoT expansion, hinting at ambient commerce experiences.

Browser portals keep niche traction for wealth-management dashboards where larger screens aid analysis. Voice and biometric interfaces remain experimental but benefit from regional language-model improvements. The interface mix thus broadens reach while deepening data capture within the MENA fintech market.

Geography Analysis

The GCC represented 62.75% of transactional value in 2025 on the back of high GDP per capita and cohesive regulatory backing. Saudi Arabia green-lit multiple neobanks in 2024, boosting competition and spurring wider digital adoption. Dubai’s DIFC supports tokenized bond pilots, drawing global innovators seeking a proving ground. Bahrain and Qatar extend complementary sandboxes, promoting cross-GCC passportability. CBDC proof-of-concepts across these states align settlement standards, simplifying regional scaling for fintech issuers.

North Africa, clocking a 17.29% CAGR to 2031, benefits from Egypt’s 104 million population and expansive unbanked base. Thirteen Egyptian fintechs made Forbes ME’s Fintech 50, signalling ecosystem maturity. Morocco’s Casablanca Finance City anchored new regulations that fast-track e-money licensing, while Tunisia leverages telco agents to reach rural users. Network International’s partnership with Money Fellows shows GCC-North Africa infrastructure synergy.

The Levant segment is smaller but strategically positioned. Jordan’s sandbox routes present a clear regulatory runway, while Lebanon’s diaspora remittances sustain sizable FX flows despite domestic turmoil. Fintechs link GCC salary corridors to Levantian wallets, cutting fees versus legacy transfer options. Cross-regional platforms thus treat the Levant as a hub to stitch together north-south remittance and trade lanes within the broader MENA fintech market.

Competitive Landscape

The MENA fintech market is characterized by fragmented competition, with the top five players holding a significant share in 2024. This fragmentation signals strong consolidation potential, as seen in recent M&A activities like MNT-Halan’s acquisition of Turkish lender Tam Finans and Disruptak’s purchase of CIB’s stake in Khazna. Unlike mature fintech markets, market concentration in MENA remains low due to diverse regulatory frameworks and the rise of country-specific champions. These local players leverage in-depth market knowledge and strong regulatory ties to fend off international competition. Successful regional firms such as Fawry exemplify a strategic shift toward platform expansion and cross-border scaling, branching out from payments into BNPL, microfinance, and B2B services to diversify revenue and boost customer lifetime value.

White-space opportunities are emerging in areas such as Islamic fintech, particularly products aligned with ESG mandates that are gaining traction in the region. There is also untapped potential in streamlining cross-border remittance corridors between the GCC and North Africa, along with embedded finance solutions tailored for underserved SMEs. These SMEs often lack access to traditional banking, making fintech innovation crucial for financial inclusion. Technology adoption trends include AI-driven credit scoring, blockchain-enabled cross-border payments, and open banking APIs that support third-party integrations and foster ecosystem growth. The partnership between TAMAM, ZainTECH, FICO, and Lean Technologies exemplifies how strategic collaborations can merge telecom, data analytics, and open banking to build competitive full-service fintech platforms.

Emerging fintech disruptors are utilizing mobile-first platforms and alternative data sources to reach the unbanked and underbanked populations. These new entrants are reshaping access to financial services, especially in underserved markets with high mobile penetration but low traditional banking infrastructure. In response, established players are pursuing acquisition and partnership strategies to accelerate their digital transformation and retain market relevance. The emphasis is increasingly on ecosystem-building through strategic alliances and product diversification rather than isolated service offerings.

MENA Fintech Industry Leaders

Fawry

PayTabs

Checkout.com

Tabby

STC Pay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fawry completed three strategic acquisitions (Virtual CFO, CodeZone, and Dirac Systems) for undisclosed amounts to expand its business services ecosystem and strengthen digital transformation capabilities for Egyptian SMEs to support Fawry's diversification strategy.

- February 2025: Fawry completed three strategic acquisitions (Virtual CFO, CodeZone, and Dirac Systems) for undisclosed amounts to expand its business services ecosystem and strengthen digital transformation capabilities for Egyptian SMEs to support Fawry's diversification strategy.

- January 2025: Network International partnered with Money Fellows to provide a Digital Payments as a Service platform for Money Fellows' new offering in Egypt, leveraging advanced fraud prevention and secure payment functionality to support regional expansion across the Middle East and Africa.

- January 2025: AlHuda Centre projected Islamic finance assets to surpass USD 5 trillion in 2025, with Islamic fintech market forecast to grow from USD 138 billion to USD 306 billion by 2027 at 17.3% CAGR. The emergence of "Islamic environment fintech", combining digital innovation, sustainability, and Sharia compliance, represents a major growth driver for 2025 AlHuda CIBE.

MENA Fintech Market Report Scope

Fintech is one of the most widely anticipated and quickly adopted fields of financial services as people adopt urbanization and smart connectivity. The MENA fintech market is segmented by service proposition and by country. By service proposition, the market is segmented into money transfer and payments, savings and investments, digital lending and lending marketplaces, online insurance and insurance marketplaces, and other service propositions. By country, the market is segmented into United Arab Emirates, Saudi Arabia, Bahrain, Qatar, Iran, Egypt, Israel, and Rest of the Middle East and North Africa. The report offers market sizes and forecasts for the MENA fintech market in terms of value in USD for all the above segments.

By Service Proposition

| Digital Payments |

| Digital Lending & Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

By End-User

| Retail |

| Businesses |

By User Interface

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

By Geography

| GCC | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Bahrain | |

| Kuwait | |

| Oman | |

| North Africa | Egypt |

| Morocco | |

| Algeria | |

| Tunisia | |

| Levant | Jordan |

| Lebanon |

| By Service Proposition | Digital Payments | |

| Digital Lending & Financing | ||

| Digital Investments | ||

| Insurtech | ||

| Neobanking | ||

| By End-User | Retail | |

| Businesses | ||

| By User Interface | Mobile Applications | |

| Web / Browser | ||

| POS / IoT Devices | ||

| By Geography | GCC | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Bahrain | ||

| Kuwait | ||

| Oman | ||

| North Africa | Egypt | |

| Morocco | ||

| Algeria | ||

| Tunisia | ||

| Levant | Jordan | |

| Lebanon | ||

Key Questions Answered in the Report

What is the current value of the MENA fintech market?

The market stands at USD 6.35 billion in 2026 and is projected to reach USD 11.46 billion by 2031.

Which service segment leads spending?

Digital payments contribute 54.12% of 2025 revenue, reflecting widespread wallet and merchant acceptance.

Where is growth fastest geographically?

North Africa posts the highest projected CAGR of 17.29% through 2031 due to large unbanked populations.

What factors accelerate adoption?

Government cash-lite mandates, surging smartphone penetration, and record VC funding rounds are the core drivers.

Which restraint has the biggest drag on growth?

Regulatory fragmentation across 19 jurisdictions lifts compliance costs and slows cross-border scaling.

Page last updated on: