Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

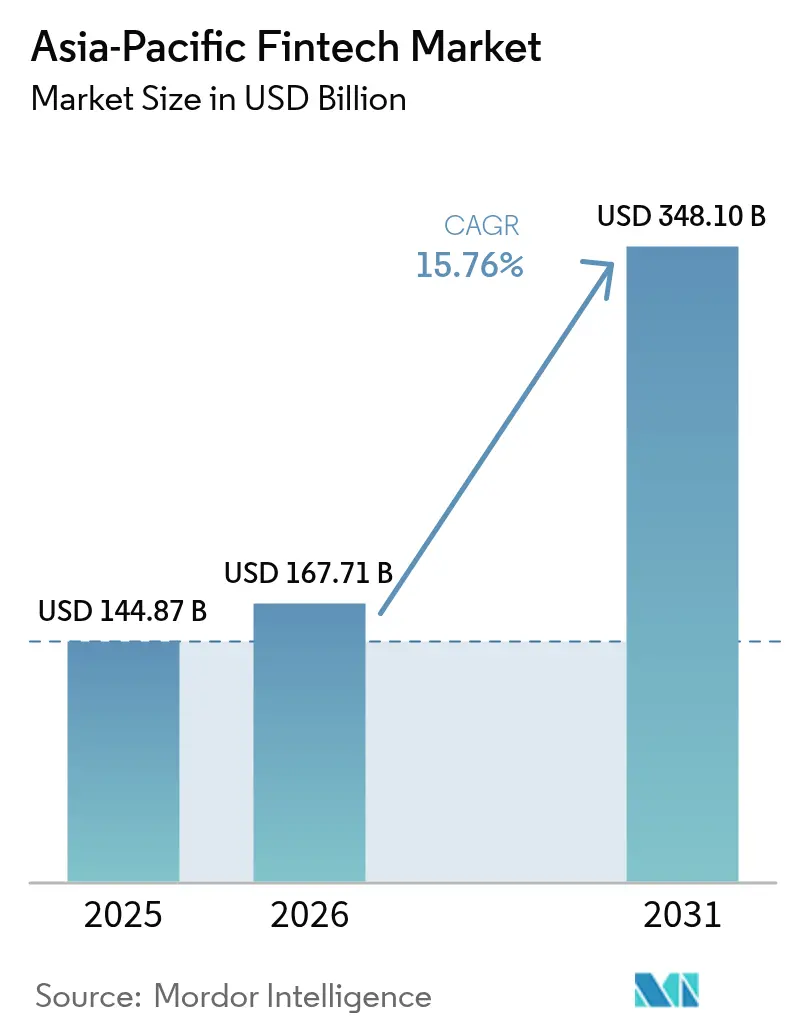

| Base Year Market Size (2025) | USD 144.87 Billion |

| Market Size (2026) | USD 167.71 Billion |

| Market Size (2031) | USD 348.1 Billion |

| Growth Rate (2026 - 2031) | 15.76% CAGR |

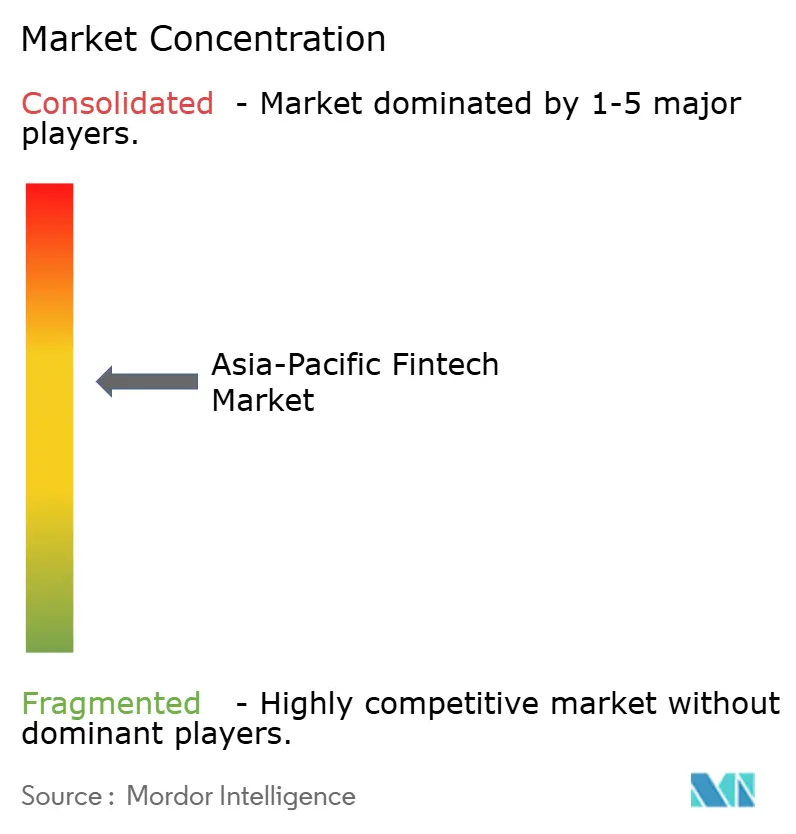

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Fintech Market Analysis by Mordor Intelligence

Asia-Pacific fintech market size in 2026 is estimated at USD 167.71 billion, growing from 2025 value of USD 144.87 billion with 2031 projections showing USD 348.1 billion, growing at 15.76% CAGR over 2026-2031. Growth stems from three structural forces: entrenched mobile-first behavior, government investment in real-time digital rails, and a visibly lighter licensing regime for cloud-native banks. These factors shorten customer onboarding cycles, cut transaction fees, and encourage capital inflows from both venture and incumbent financial institutions. Super-apps continue to fold payments, lending, investing, and insurance into single interfaces, locking in daily engagement and elevating lifetime value per user. Cross-border corridors are also scaling rapidly as Project Nexus threads India’s UPI, Singapore’s PayNow, and Thailand’s PromptPay into one settlement fabric, bringing down remittance costs and opening high-margin revenue for B2B platforms[1]Bank for International Settlements, “Project Nexus Expands Cross-Border Payment Network,” bis.org. . Shifting policies on digital identity and e-KYC have further widened addressable populations; Indonesia, the Philippines, and Bangladesh alone add over 400 million newly verifiable adults, catalyzing aggressive go-to-market moves by regional neobanks.

Key Report Takeaways

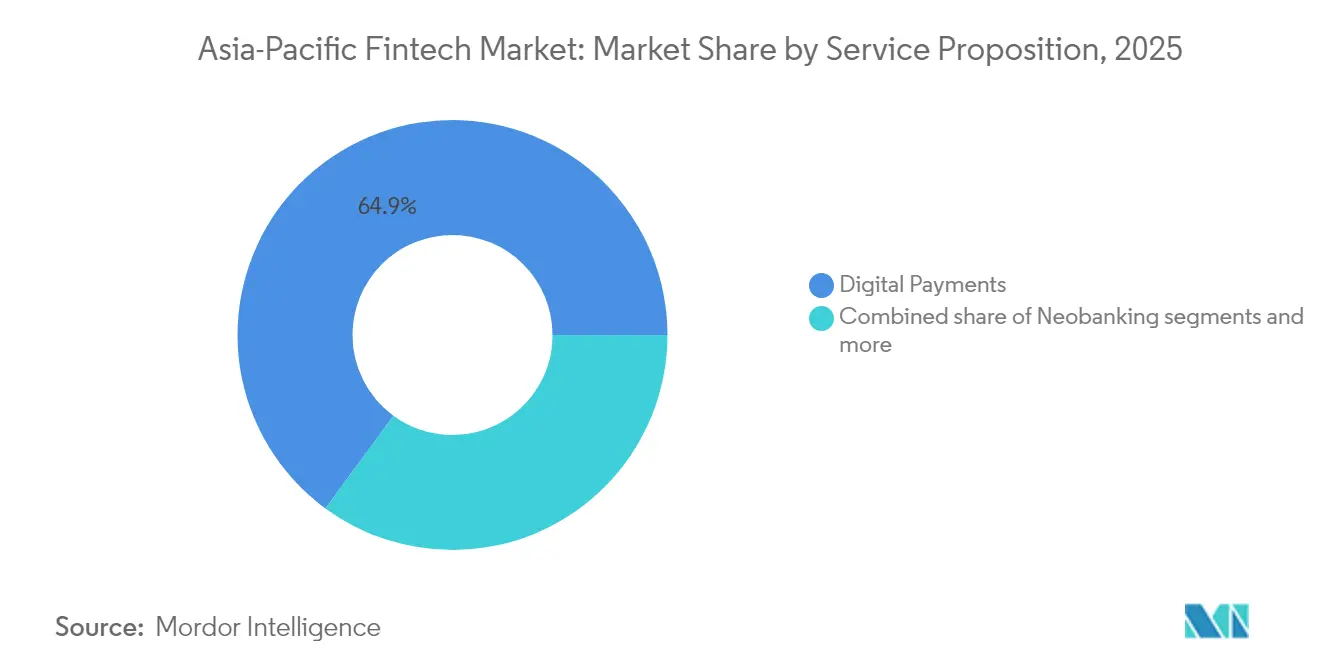

- By service proposition, digital payments captured 64.93% of the Asia-Pacific fintech market share in 2025, while neobanking is projected to grow fastest at a CAGR of 30.46% between 2026 and 2031.

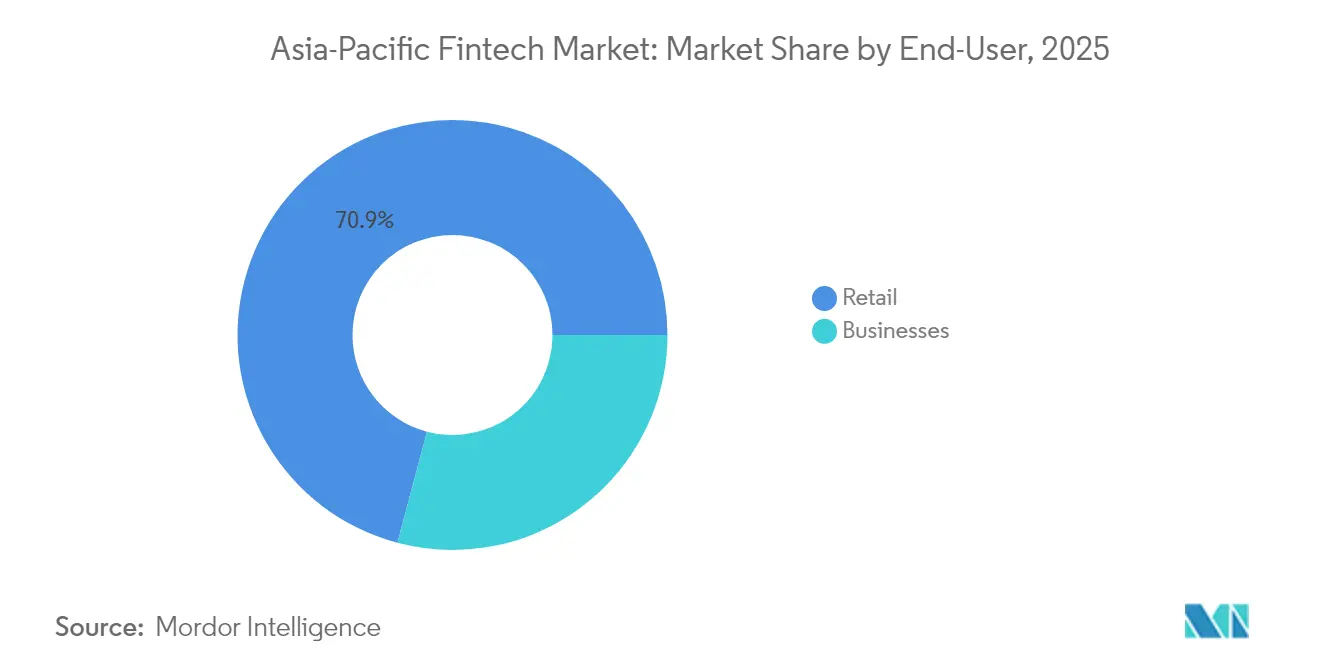

- By end-user, retail accounted for 70.88% of the Asia-Pacific fintech market share in 2025, with businesses expected to post a growth rate of 25.47% CAGR through 2031.

- By user interface, mobile applications held 72.62% of the Asia-Pacific fintech market share in 2025, while POS/IoT devices are forecast to expand at a 23.72% CAGR during 2026–2031.

- By geography, China led with 40.12% of the Asia-Pacific fintech market share in 2025, while India is anticipated to grow fastest at a CAGR of 27.25% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-time payment rails proliferation across APAC | 3.2% | India, Singapore, Thailand, Malaysia, Philippines | Medium term (2-4 years) |

| Government-led financial inclusion & e-ID programs | 2.8% | India, Indonesia, Philippines, Vietnam, Bangladesh | Long term (≥ 4 years) |

| Mobile-first super-app ecosystems accelerating adoption | 2.5% | China, Southeast Asia, India | Short term (≤ 2 years) |

| Renewed VC & corporate funding momentum post-2024 | 2.1% | Global APAC, concentrated in Singapore, Hong Kong | Short term (≤ 2 years) |

| Retail CBDC pilots unlocking programmable-payment use cases | 1.8% | China, Hong Kong, Singapore, Australia, Thailand | Long term (≥ 4 years) |

| ESG-linked fintech modules driven by disclosure mandates | 1.4% | Australia, Hong Kong, Singapore, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Real-Time Payment Rails Proliferation Across APAC

The rollout of instant payment networks such as India’s UPI, Singapore’s PayNow, and Thailand’s PromptPay removes settlement lags, reduces interchange fees, and shifts consumer preference away from cash. UPI processed 131 billion transactions worth USD 1.8 trillion in 2024[2]National Payments Corporation of India, “UPI Transaction Statistics 2024,” npci.org.in. . PayNow and PromptPay achieved bilateral interoperability, allowing Singaporean tourists in Thailand to pay merchants at mid-market FX rates without card surcharges. Real-time rails consequently become embedded layers that fintech applications can tap through open APIs, creating low-code paths to launch P2P remittance, payroll, and merchant settlement products. Merchants favor QR rails for lower device costs and faster cash conversion, resulting in cannibalization of card volumes, especially under USD 25 ticket sizes. Governments continue subsidizing POS upgrades, signaling that instant push payments will remain the default standard by mid-decade.

Government-Led Financial Inclusion & e-ID Programs

Digital ID frameworks materially lower KYC friction, cut onboarding times from days to minutes, and thereby expand the Asia-Pacific fintech market addressable base. India’s Aadhaar underpins over 1.3 billion biometric IDs, enabling one-tap verification across banking, insurance, and investment apps[3]Unique Identification Authority of India, “About UIDAI,” uidai.gov.in.. Indonesia’s e-ID scheme follows suit for 270 million citizens, while the Philippines targets 50 million unbanked adults by 2028. These programs standardize data fields, which allows regional interoperability and supports cross-border financial products. Providers reduce customer acquisition costs by up to 40%, reallocating savings toward product R&D and geographic expansion. The inclusion wave also drives account ownership among women and rural micro-enterprises, linking public welfare transfers directly into wallet accounts.

Mobile-First Super-App Ecosystems Accelerating Adoption

Super-apps from Ant Group, Tencent, Grab, and GoTo integrate ride-hailing, food delivery, and e-commerce with payments, credit, and investment modules. Alipay and WeChat Pay surpassed card networks on domestic volume, sustaining daily usage frequency and making financial exits rare. Grab handled over USD 20 billion in payments through embedded financial services across Southeast Asia. Such ecosystems lower customer acquisition costs and raise retention metrics, reinforcing the Asia-Pacific fintech market’s network effects. The model proves particularly sticky in emerging markets where app real estate is limited and consumers value all-in-one functionality. Super-apps also deploy data analytics on user behavior, enabling hyper-personalized offers and risk-based pricing that conventional banks cannot quickly replicate.

Renewed VC & Corporate Funding Momentum Post-2024

Capital availability reversed its 2022–2023 slump. KPay’s USD 55 million Series A became the year’s largest global payments raise. Banks such as DBS and OCBC launched dedicated CVC arms, backing startups in wealthtech and insurtech. The funding uptick lets platforms widen product suites and enter tier-2 cities without compromising unit economics. Investors show preference for EBITDA-positive growth, rewarding fintechs that monetize B2B workflows or subscription models. Liquidity also fuels M&A, visible in Airwallex’s purchase of CTIN Pay to accelerate cross-border settlement reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented multi-jurisdiction compliance burden | -2.3% | Global APAC, particularly cross-border operators | Medium term (2-4 years) |

| Escalating cyber-fraud incidents and associated losses | -1.9% | India, Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Data-localization/cloud-sovereignty rules hindering scale | -1.6% | Indonesia, Vietnam, India, China | Long term (≥ 4 years) |

| Nascent AI-model-risk regulations raising deployment costs | -1.2% | Singapore, Hong Kong, Australia, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Multi-Jurisdiction Compliance Burden

Each Asia-Pacific jurisdiction prescribes its own payment licenses, capital ratios, and AML tests. Indonesia mandates local data storage and higher reserve thresholds, clashing with Singapore’s risk-based MAS framework[4]Bank Indonesia, “New Financial Services Regulations,” bi.go.id.. Cross-border payment providers face particular challenges as each jurisdiction maintains distinct AML/CTF requirements, forcing platforms like Wise and Remitly to implement country-specific compliance systems that increase operational costs by an estimated 15-20% compared to single-market operations. The fragmentation particularly impacts smaller fintech startups that lack resources to navigate multiple regulatory regimes, creating competitive advantages for established players with dedicated compliance teams.

Escalating Cyber-Fraud Incidents and Associated Losses

Digital payment fraud incidents surge across APAC markets as transaction volumes increase, with India reporting USD 1.3 billion in digital payment fraud losses during 2024 and the Philippines experiencing 40% year-over-year growth in cybercrime cases targeting financial services. Identity theft and account takeover attacks particularly impact mobile-first platforms, as fraudsters exploit SMS-based authentication weaknesses and social engineering tactics to compromise user accounts. Fintech providers increase security spending by an average of 25-30% annually to implement multi-factor authentication, behavioral analytics, and real-time transaction monitoring systems that add operational costs while potentially reducing user experience quality. The fraud escalation forces regulatory authorities to impose stricter liability

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Neobanking Redefines Deposit Gathering

Neobanking represents the fastest-growing service segment at 30.46% CAGR through 2031, despite digital payments commanding 64.93% market share in 2025. This growth differential reflects regulatory liberalization across Australia, Hong Kong, and Singapore that enables new banking licenses for digital-first providers, while established payment networks reach maturity in core markets. Tonik Bank in the Philippines achieved 2 million customers within 3 years of launch by offering 6% annual savings rates enabled by lower operational costs, while Australia's Judo Bank focuses exclusively on SME lending through digital channels to capture market share from traditional business banking. Digital lending and financing maintain steady growth as regulatory clarity improves, particularly in India, where RBI guidelines enable fintech-bank partnerships for co-lending arrangements.

Digital investments and insurtech segments benefit from wealth accumulation trends across middle-class populations in China, India, and Southeast Asia. Robo-advisory platforms like Singapore's StashAway and Indonesia's Bibit democratize investment access through low minimum thresholds and automated portfolio management, while insurtech providers embed coverage within e-commerce and mobility platforms to reach previously underserved segments. The integration of financial services within super-app ecosystems accelerates adoption rates, as users access investment and insurance products through familiar interfaces rather than standalone applications.

By End-User: SMEs Gain Digital Momentum

Business users drive the fastest segment growth at 25.47% CAGR through 2031, though retail users maintain 70.88% market share in 2025. This acceleration reflects SME digitization trends accelerated by pandemic-era operational changes and government initiatives promoting cashless transactions across APAC markets. Cross-border payment solutions particularly benefit from B2B adoption, as export-oriented manufacturers in Vietnam, Thailand, and Malaysia seek alternatives to traditional correspondent banking for international settlements that can take 3-5 business days.

Embedded finance solutions gain traction among business users as e-commerce platforms and supply chain management systems integrate lending, payments, and working capital financing. Funding Societies' acquisition of CardUp in 2024 creates integrated B2B payment and lending capabilities across Southeast Asia, while Airwallex's expansion into expense management and corporate cards demonstrates the convergence of business financial services. Retail segment growth moderates as smartphone penetration approaches saturation levels in developed APAC markets, though rural and elderly demographics represent untapped opportunities for simplified financial products designed for basic smartphones and feature phones.

By User Interface: Payment Density Spreads to Devices

Mobile applications dominate with 72.62% market share in 2025, yet POS and IoT devices achieve the fastest growth at 23.72% CAGR through 2031 as contactless payment infrastructure expands across retail environments. This shift reflects merchant adoption of integrated payment terminals that accept QR codes, NFC payments, and biometric authentication without requiring separate hardware investments. Singapore's hawker centers and Malaysia's wet markets increasingly deploy smartphone-based POS systems that enable small merchants to accept digital payments without traditional card terminal costs, while Indonesia's warung (small shops) adopt QR code displays that integrate with multiple payment networks simultaneously.

Web and browser interfaces maintain stable market positions as desktop-based B2B transactions require comprehensive dashboards for treasury management, reporting, and multi-user access controls that mobile apps cannot effectively replicate. IoT device integration accelerates through connected car payments, smart home appliances, and wearable devices that enable contextual financial services. The interface diversification creates opportunities for fintech providers to capture transaction volume across multiple touchpoints while reducing dependency on smartphone-based interactions that face increasing competition from super-app ecosystems.

Geography Analysis

China maintains 40.12% market share in 2025 through Ant Group's Alipay and Tencent's WeChat Pay dominance, yet regulatory restrictions on data sharing and cross-border transactions limit growth potential compared to other regional markets. India emerges as the fastest-growing geography at 27.25% CAGR through 2031, driven by UPI transaction volume exceeding 100 billion annually and RBI initiatives promoting digital lending through co-lending frameworks. The country's fintech ecosystem benefits from English-language advantages that facilitate international expansion, while regulatory sandboxes enable innovative product development without full licensing requirements initially.

Southeast Asian markets collectively represent 25% of regional activity, with Singapore serving as the regulatory innovation hub through MAS's progressive approach to digital banking licenses and cross-border payment facilitation. Indonesia drives volume growth through its 270 million population base and government initiatives promoting financial inclusion, while the Philippines benefits from overseas remittance flows that create demand for digital money transfer services. Australia and Japan represent mature markets with established regulatory frameworks that enable fintech innovation while maintaining consumer protection standards, creating opportunities for premium financial services targeting affluent demographics.

Competitive Landscape

The Asia-Pacific fintech market is moderately concentrated, with the top players accounting for a significant share of transaction value. Despite this, the presence of hundreds of specialized providers fosters ongoing competition across different countries and fintech segments. Super-app giants like Ant Group and Tencent use integrated lifestyle services to lock in users and increase switching costs. Meanwhile, regional leaders such as Grab Financial Group and GCash succeed by tailoring services to local needs and navigating regulatory environments more effectively than global players. The strategic focus is shifting toward embedded finance, cross-border payments, and B2B solutions as platforms diversify beyond traditional consumer payment models.

New opportunities are emerging in SME lending, digital insurance distribution, and wealth management—especially for growing middle-class populations in emerging APAC markets. As fintech players explore these areas, success hinges on understanding local financial behaviors and unmet needs. Key technological advancements support this growth, particularly AI-powered risk analytics, real-time fraud prevention, and blockchain-based settlements that enhance speed, security, and compliance. The acquisition of CTIN Pay by Airwallex in 2024 illustrates the region’s consolidation trend, with platforms choosing strategic acquisitions over slow organic expansion. These moves allow players to quickly scale across borders and enhance their product portfolios.

Disruptive entrants are reshaping the landscape by addressing underserved markets with innovative models. Neobanks are focusing on SME clients excluded from traditional financial systems, while insurtech firms embed coverage within digital commerce platforms. Cross-border payment startups are taking advantage of real-time infrastructure to bypass outdated correspondent banking networks. Regulatory frameworks are also becoming a crucial factor in competitive success, favoring firms with established licenses and strong local alliances. International entrants often struggle with the complexity of multi-jurisdictional compliance, giving well-positioned regional players a significant edge.

Asia-Pacific Fintech Industry Leaders

Ant Group (Alipay)

Tencent (WeChat Pay)

Paytm

Grab Financial Group

Kakao Pay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ant Group announced the expansion of Alipay+ cross-border payment network to include 15 new Southeast Asian e-wallets, enabling Chinese tourists to use domestic payment methods across Thailand, Malaysia, and Singapore without currency conversion fees.

- December 2024: GXS Bank acquired Validus Capital for USD 120 million, creating Southeast Asia's largest digital SME lending platform with over USD 2 billion in loan origination capacity. The acquisition enables GXS Bank to expand beyond Singapore into Indonesia and Vietnam while leveraging Validus's AI-powered credit assessment technology for supply chain financing solutions.

- November 2024: Syfe completed the acquisition of Selfwealth for USD 85 million, establishing the largest robo-advisory platform in Australia and Singapore with combined assets under management exceeding USD 3 billion.

- October 2024: Funding Societies acquired CardUp for USD 45 million, integrating B2B payment and lending services across Southeast Asia to serve over 100,000 SME customers. The strategic combination enables cross-selling opportunities while reducing customer acquisition costs through integrated financial service offerings for business clients.

Asia-Pacific Fintech Market Report Scope

Fintech refers to the integration of technology into offerings by financial services companies to improve their use and delivery to consumers. It primarily works by unbundling offerings by such firms and creating new markets for them.

The Asia-Pacific fintech market is segmented by service proposition and geography. By service proposition, the market is sub-segmented into money transfer and payments, savings and investments, digital lending & lending marketplaces, online insurance & insurance marketplaces, and other service propositions. By geography, the market is sub-segmented into China, India, Australia, Singapore, Hong Kong, and the Rest of Asia-Pacific.

The report offers market size and forecasts for the Asia-Pacific fintech market in terms of revenue (USD) for all the above segments.

By Service Proposition

| Digital Payments |

| Digital Lending and Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

By End-User

| Retail |

| Businesses |

By User Interface

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

By Geography

| India | |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | Singapore |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific |

| By Service Proposition | Digital Payments | |

| Digital Lending and Financing | ||

| Digital Investments | ||

| Insurtech | ||

| Neobanking | ||

| By End-User | Retail | |

| Businesses | ||

| By User Interface | Mobile Applications | |

| Web / Browser | ||

| POS / IoT Devices | ||

| By Geography | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | Singapore | |

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the 2026 valuation of the Asia-Pacific fintech market?

The Asia-Pacific fintech market size is USD 167.71 billion in 2026.

How fast will regional fintech revenue grow this decade?

Aggregate revenue is forecast to rise at a 15.76% CAGR and reach USD 348.1 billion by 2031.

Which service segment expands the quickest?

Neobanking grows at 30.46% CAGR, driven by new digital bank licenses across Australia, Hong Kong, and Singapore.

Which user group offers the highest growth upside?

Business users, especially SMEs, record a 25.47% CAGR through 2031 as embedded finance gains traction.

Where is transaction volume increasing the fastest geographically?

India leads with a 27.25% CAGR on the back of UPI’s international rollout and supportive RBI policy.

What role do super-apps play in APAC fintech?

Super-apps integrate payments, lending, and insurance into lifestyle platforms, lowering acquisition costs and boosting user retention across the region.

Page last updated on: