Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

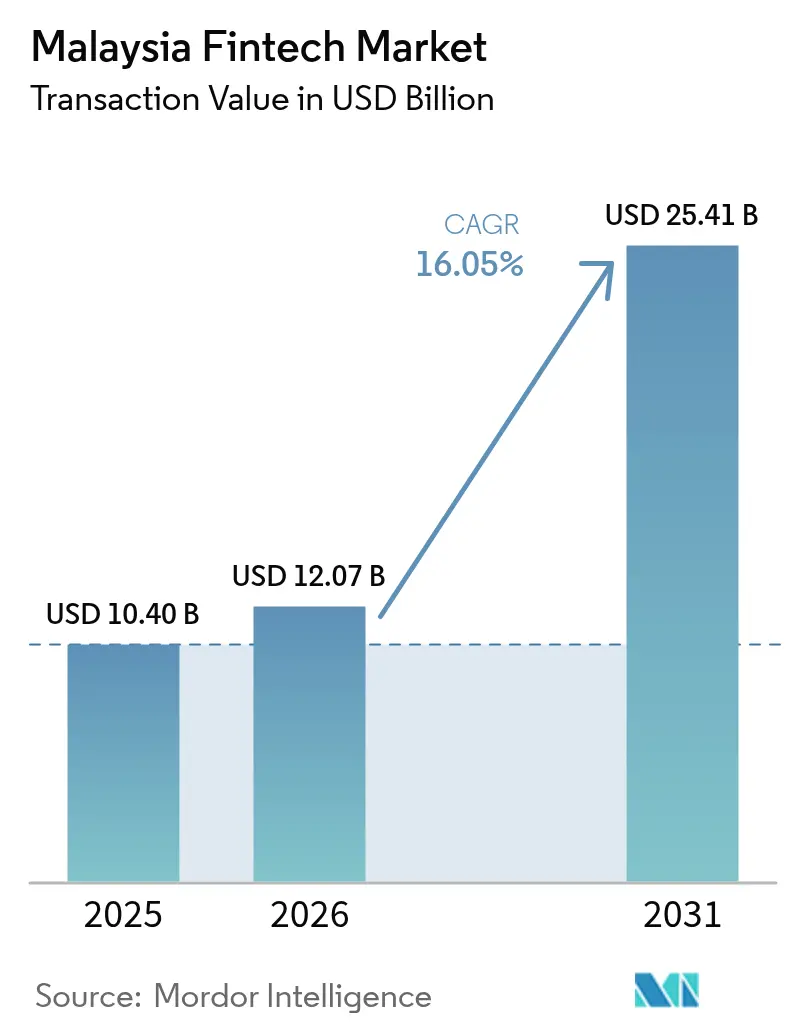

| Base Year Market Size (2025) | USD 10.40 Billion |

| Market Size (2026) | USD 12.07 Billion |

| Market Size (2031) | USD 25.41 Billion |

| Growth Rate (2026 - 2031) | 16.05% CAGR |

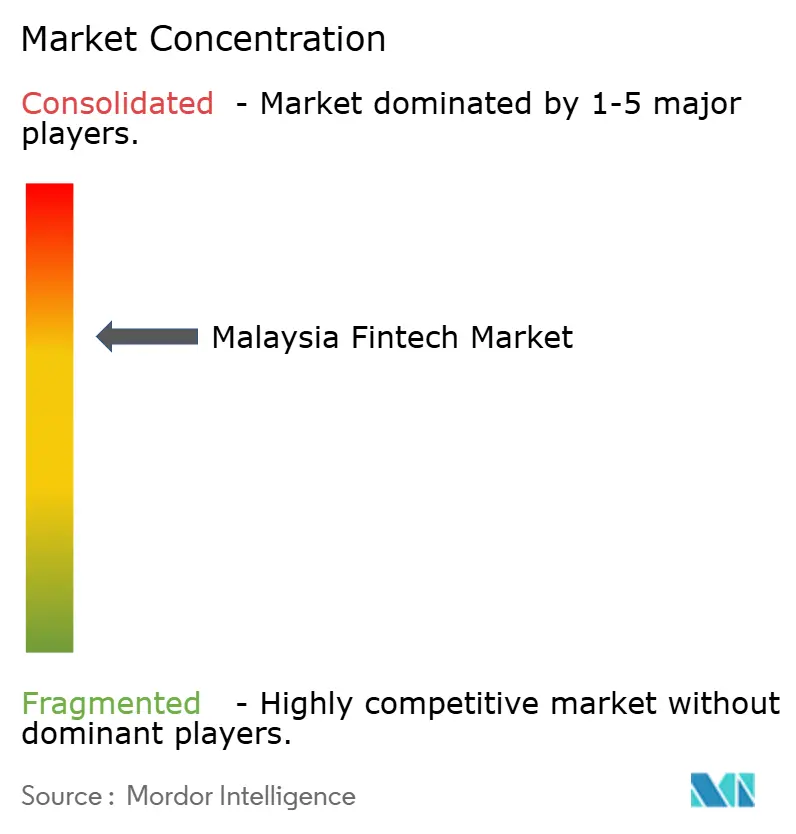

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Fintech Market Analysis by Mordor Intelligence

The Malaysia fintech market size was valued at USD 10.40 billion in 2025 and estimated to grow from USD 12.07 billion in 2026 to reach USD 25.41 billion by 2031, at a CAGR of 16.05% during the forecast period (2026-2031). Malaysia’s role as Southeast Asia’s Islamic finance hub, combined with an expanding digital‐first consumer base and supportive sandbox regulations, underpins this growth. Continued licensing of digital banks, such as KAF Digital Bank and AEON Bank, has broadened service offerings while lowering acquisition costs[1]Bank Negara Malaysia, “Digital Banking Licenses,” BNM.gov.my. . Cross-border QR payment links with Cambodia and Singapore elevate transaction volumes and position local providers for regional expansion. Public cloud and data-center investments across Sarawak and Penang strengthen the underlying infrastructure, enabling real-time payments and compliance analytics. As the Malaysia fintech market matures, competitive strategies increasingly revolve around super-app ecosystems, Islamic-compliant innovations, and embedded finance integrations into retail and SME workflows.

Key Report Takeaways

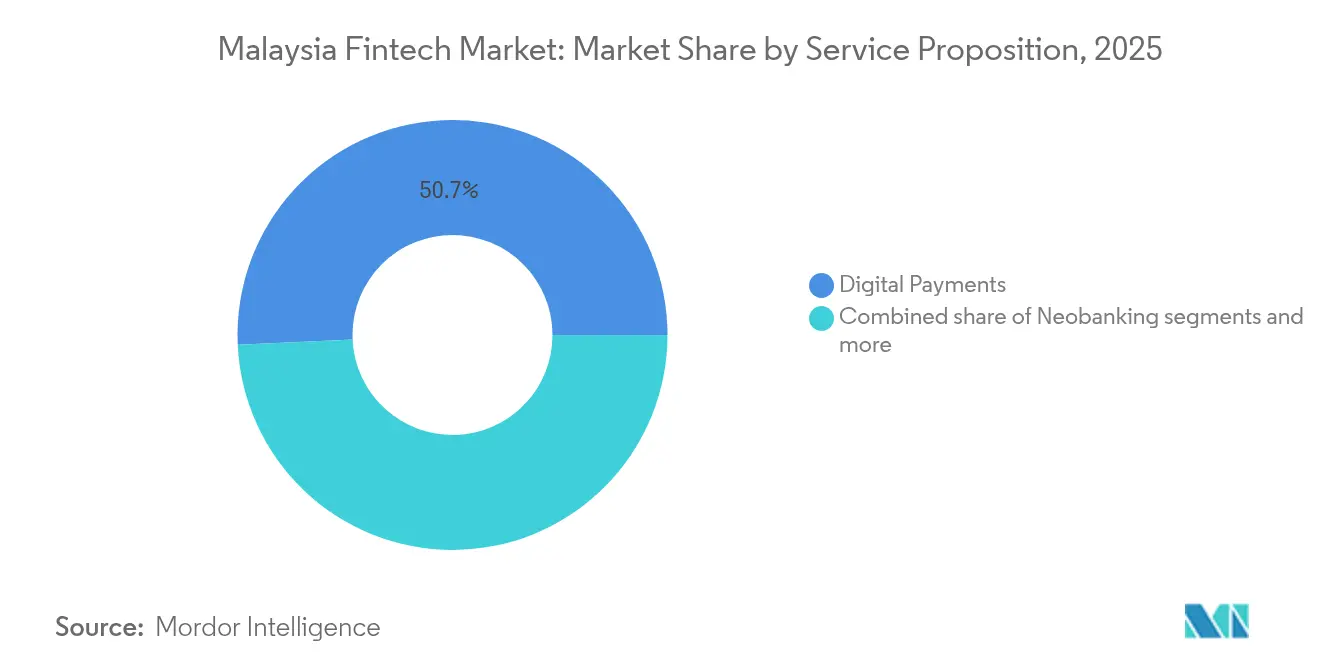

- By service proposition, digital payments captured 50.72% of the Malaysia fintech market share in 2025, while neobanking is projected to expand fastest at a CAGR of 26.12% during 2026-2031.

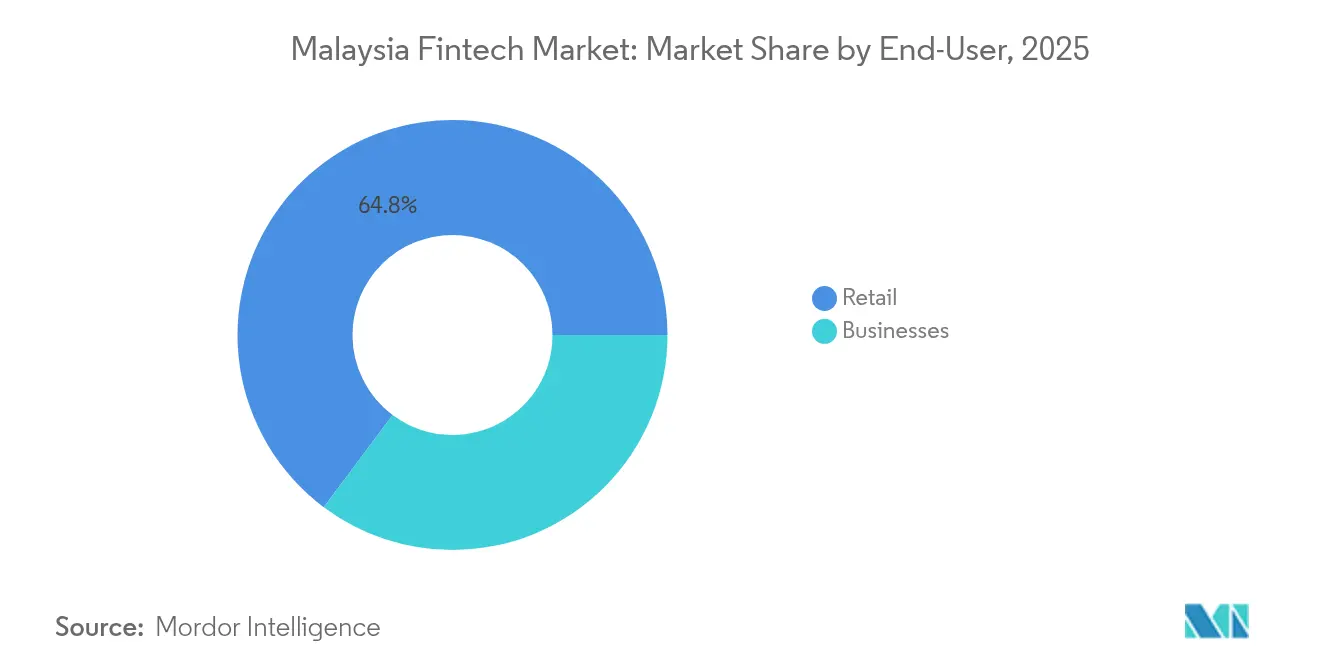

- By end-user, the retail segment accounted for 64.78% of the Malaysia fintech market share in 2025, with business users expected to post the highest CAGR of 22.55% over 2026-2031.

- By user interface, mobile apps comprised 56.10% of the Malaysia fintech market share in 2025, while POS/IoT devices are forecast to grow at a 24.6% CAGR through 2031.

- By geography, King Valley comprised 47.10% of the Malaysia fintech market share in 2025, while East Malaysia is forecast to grow at a 23.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High smartphone & internet penetration | +2.8% | National, with urban concentration in Klang Valley | Short term (≤ 2 years) |

| Government's MyDigital & FSB initiatives | +3.2% | National, with pilot programs in northern states | Medium term (2-4 years) |

| E-commerce boom | +2.1% | National, with Klang Valley and Southern Region leadership | Short term (≤ 2 years) |

| Favourable sandbox & digital bank licences | +2.4% | National, with regulatory oversight from Kuala Lumpur | Medium term (2-4 years) |

| Rising demand for Islamic fintech | +1.8% | National, with stronger adoption in East Coast | Long term (≥ 4 years) |

| ASEAN cross-border QR-code integration | +1.6% | Border regions, tourism corridors, and business hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Smartphone & Internet Penetration Drives Addressable Market Expansion

Malaysia’s smartphone penetration surpasses 85% and internet connectivity reaches 90% of residents, growing the digital-ready customer pool for fintech services[2]The Edge Malaysia, “MDEC Intensifies Push for 25.5% Digital Economy Contribution,” Theedgemalaysia.com. . Touch ’n Go Digital expects its first full-year profitability in 2025 after securing USD 75 million from strategic investors, a milestone enabled by this mobile reach. E-wallet usage already touches 40%, outpacing traditional banking access. Google Pay’s 2024 tie-up with ShopeePay and TNG eWallet illustrates how infrastructure maturity accelerates ecosystem partnerships that deepen wallet stickiness. Younger cohorts dominate adoption, with 90% of users aged 40 and below forming the core target for upcoming product launches.

Government MyDigital & Financial Sector Blueprint Initiatives Catalyze Ecosystem Development

The MyDigital roadmap aims for the digital economy to contribute 25.5% of GDP by end-2025, supported by MYR 163.6 billion (USD 34.36 billion) in approved digital investments in 2024, a 250% jump year-on-year[3]The Edge Malaysia, “RM16.2b in Investments Bagged Under Malaysia Digital,” Theedgemalaysia.com. . More than 3,891 Malaysia Digital-status firms now operate nationwide, buoyed by tax incentives granting 0% on IP income for a decade. The Financial Sector Blueprint’s 75% cashless-transaction goal releases subsidies for payment terminals and data-protection upgrades. Regional expansion is evident as the Digital Ministry opened its northern office in Penang to funnel incentives and technical mentorship beyond Klang Valley.

E-commerce Boom Amplifies Payment Volume Growth

Malaysia's e-commerce sector demonstrates exceptional momentum, with Shopee Malaysia reporting 8x sales growth during the 10.10 festival and 170% growth during Raya celebrations in 2024. This e-commerce expansion directly feeds payment volume for fintech rails, as digital transactions become the preferred settlement method for online retail. The sector's gross merchandise value CAGR exceeding 18% creates a multiplier effect for payment processors, particularly benefiting e-wallet providers and digital payment facilitators. Cross-platform integration between e-commerce and fintech services, exemplified by Shopee's partnership with Takaful IKHLAS for Shariah-compliant motor insurance, demonstrates how payment volume growth extends into adjacent financial services. The e-commerce boom also drives demand for embedded finance solutions, as merchants seek integrated payment, lending, and insurance products to enhance customer experience and increase transaction values.

Favourable Sandbox & Digital Bank Licences Lower Entry Barriers

Bank Negara Malaysia's progressive regulatory approach granted digital banking licenses to 5 institutions, including Malaysia's first Islamic digital bank, AEON Bank, fundamentally altering the competitive landscape. The Securities Commission Malaysia's regulatory sandbox, opening applications in April 2025, provides a controlled environment for fintech innovation testing under tailored regulatory requirements. This regulatory liberalization enables challenger banks to compete directly with incumbents, as evidenced by Boost Bank's rapid deposit accumulation of MYR 700 million (USD 147 million) within 6 months of launch. Digital banks benefit from lower operational costs and agile technology stacks, creating pricing advantages that pressure traditional institutions to accelerate their own digital transformation. The sandbox framework particularly benefits Islamic fintech innovations, with Securities Commission Malaysia's dedicated Islamic Capital Market Department supporting Shariah-compliant product development and market entry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-fraud concerns | −1.9% | Urban centers nationwide | Short term (≤ 2 years) |

| Reliance on incumbent banking rails | −1.4% | Nationwide legacy dependencies | Medium term (2-4 years) |

| Shortage of deep-tech fintech talent | -2.7% | National, with severe gaps in Tier-2 cities and East Malaysia | Medium to long term (2-5 years) |

| Regional digital tax complexity | -2.1% | National, with disproportionate effects on cross-border and SME fintech operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-fraud Concerns Erode User Trust and Increase Compliance Costs

Rising cybersecurity threats and digital fraud incidents create significant headwinds for fintech adoption, with compliance costs increasing 25% year-on-year across the industry. Bank Negara Malaysia and Bank of Thailand signed a memorandum of understanding in April 2025 for cybersecurity and digital fraud cooperation, highlighting the cross-border nature of these threats. Malaysian banks responded by adding malware shielding to mobile applications, while BNM's National Fraud Portal launch reduced fraud tracing time by 75%, demonstrating both the severity of the problem and institutional responses. GXBank's introduction of Cyber Fraud Protect insurance products reflects how fintech companies are monetizing security concerns while addressing customer risk aversion.

Reliance on Incumbent Banking Rails Limits Fintech Uptime Guarantees

Malaysia's fintech ecosystem remains dependent on legacy banking infrastructure for core settlement and clearing functions, creating systemic vulnerabilities that limit service reliability guarantees. When incumbent bank systems experience downtime, fintech applications lose functionality despite having modern user interfaces and robust mobile platforms. This dependency becomes particularly problematic during high-volume periods or system maintenance windows, when fintech companies cannot provide the always-on service expectations of digital-native customers. CelcomDigi and PayNet's partnership to strengthen DuitNow payment security through SIM-based authentication represents efforts to enhance reliability, yet the fundamental infrastructure bottleneck persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Digital Payments Sustain Lead While Neobanking Accelerates

Digital payments captured 50.72% of Malaysia fintech market share in 2025, anchored by Touch ’n Go Digital’s multi-modal transport and retail integrations. Government cashless incentives and regional QR interoperability continue to widen this moat. Digital lending ranks second at 21.03%, boosted by Funding Societies’ USD 27 million raise that broadened Shariah-compliant SME lines. Insurtech holds 15.05%, validated by PolicyStreet’s USD 15.4 million Series B and a 5 million-strong user base.

Neobanking, though only 7.35% in 2025, is projected to grow at a 26.12% CAGR, narrowing gaps with incumbents through fee-free accounts and rapid onboarding. Digital investments stand at 5.85%, where StashAway’s launch of Bitcoin and Ethereum ETFs alongside Shariah portfolios diversifies revenue. The Securities Commission’s Digital Innovation Fund has co-financed 15 pilots, signalling future service-mix shifts.

By End-User: Retail Dominance Meets Business Upswing

Retail users accounted for 64.78% of the Malaysia fintech market in 2025, supported by a youthful demographic and high mobile penetration. Versa’s 270,000 users—59% under 30—mirror this skew. Islamic-compliant savings tools and micro-insurance maintain momentum among mass-market consumers.

Business users, currently 35.22%, are the fastest riser at 22.55% CAGR to 2031. Boost Bank and CGC Digital’s MYR 130 million (USD 27.30 million) facility illustrates demand for alternative credit among MSMEs. The MYR 1.5 billion (USD 315 million) Business Digitalisation Initiative supplies subsidies and technical training, further catalysing SME uptake of payroll, invoicing, and supply-chain finance modules.

By User Interface: Mobile Apps Dominate, POS/IoT Devices Gain Traction

Mobile channels command 56.10% of interactions, underscoring Malaysia’s mobile-first financial habits. Grab, MAE, and TNG integrate ride-hailing, transfers, and micro-investments to amplify session frequency. Browser interfaces cover 28.45%, catering to corporate dashboards and wealth-management tasks requiring multi-screen analysis.

POS and IoT endpoints, though only 10.95% now, are forecast to grow 24.6% CAGR, propelled by Soft Space’s tap-to-phone rollout and GHL Systems’ merchant acquirer upgrades. Smart city pilots and Industry 4.0 incentives further embed payments into connected devices, paving the way for frictionless checkout experiences.

Geography Analysis

Klang Valley captured 47.10% of Malaysia fintech market share in 2025, reflecting its dense network of regulators, venture investors, and tech talent. Headquarters of Touch ’n Go Digital, PolicyStreet, and Jirnexu cluster here, creating virtuous knowledge spillovers and rapid prototyping cycles. Superior fiber and 5G coverage underpin real-time KYC and analytics workloads.

The Southern Region accounts for a significant share is projected to grow at a higher CAGR, buoyed by the Johor–Singapore Special Economic Zone that channels cross-border flows via PayNow-DuitNow rails. Data-center proposals in Iskandar position the region for disaster recovery and latency-sensitive fintech workloads.

East Malaysia represents the fastest-growing geography at 23.7% CAGR through 2031, as Sarawak Digital Corporation's initiatives and substantial data center investments create digital infrastructure foundations for fintech expansion. The region's growth reflects government efforts to distribute digital economy benefits beyond Peninsular Malaysia, with targeted investments in connectivity and digital skills development addressing historical infrastructure gaps.

The Northern Region carries a 21.08% share, leveraged by manufacturing supply chains in Penang that need trade-finance and cross-border remittance solutions. Penang’s MYR 1.23 billion (USD 258.3 million) in Malaysia Digital investment approvals and the opening of an MDEC office concentrate support services and talent. East Coast, at 9.32%, leverages cultural affinity for Islamic finance to pilot new Shariah-compliant wallets and takaful offerings targeting domestic tourism corridors.

Competitive Landscape

The Malaysia fintech market shows a moderate level of concentration, with a few major players holding a significant share of the industry. Touch 'n Go Digital stands out as the market leader, benefiting from its deep integration with transportation services and strong ties to government initiatives. At the same time, Maybank MAE exemplifies how traditional banks are adapting to the digital age, using their large customer base and digital transformation efforts to maintain relevance. This balance of established dominance and new growth signals a dynamic and evolving competitive environment. The market's competitive intensity is increasing, particularly with the entry of digital banking license holders like Boost Bank, which accumulated MYR 700 million (USD 147 million) In deposits within six months by focusing on technology and enhanced customer experience.

Strategically, fintech players in Malaysia are increasingly shifting toward super-app models and embedded finance solutions. This allows them to diversify revenue streams while strengthening customer loyalty through integrated services. GrabPay Malaysia, with its 15.2% market share, exemplifies this trend by combining payments with ride-hailing, food delivery, and financial services, thus boosting transaction volume and customer lifetime value. These integrated platforms offer a seamless user experience, positioning themselves as essential daily tools. As a result, companies that successfully blend multiple financial and lifestyle services are gaining a competitive edge in user retention and monetization.

Amid this evolution, white-space opportunities are emerging in specialized and underserved areas such as Islamic fintech. Platforms like Wahed Invest and Shariah-compliant lending startups are addressing unmet market needs, particularly among Muslim consumers seeking ethical finance solutions. Traditional players are also responding; for example, Hong Leong Bank's alliance with WeBank Technology Services in January 2025 illustrates a growing trend of incumbents partnering with tech-driven specialists to accelerate AI adoption and boost efficiency. At the same time, emerging disruptors like CapBay (supply chain finance), MoneyMatch (cross-border remittances), and Oyen (pet insurance) are targeting niche verticals. These innovators are challenging the status quo by delivering tailored solutions, leveraging superior technology, and offering exceptional customer experiences.

Malaysia Fintech Industry Leaders

Touch ‘n Go Digital

Maybank MAE

GrabPay Malaysia

CIMB OCTO & Boost

BigPay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Boost Bank partnered with CGC Digital to provide MYR 130 million (~USD 29 million) in financing solutions to micro, small, and medium enterprises, leveraging Credit Guarantee Corporation Malaysia's guarantee capabilities to de-risk MSMEs.

- March 2025: The Digital Ministry unveiled a MYR 1.5 billion (USD 315 million) Business Digitalization Initiative spearheaded by MDEC, providing MSMEs with financial aid, training, mentorship, and access to subsidized digital solutions, including e-commerce, cloud, and AI-driven business management tools.

- March 2025: CelcomDigi and PayNet announced a strategic partnership to strengthen DuitNow payment security through SIM-based authentication and integration with the National Fraud Portal, enabling real-time fraud intelligence sharing and enhanced transaction verification.

- February 2025: Securities Commission Malaysia released guidelines for its Regulatory Sandbox with applications opening in April 2025, providing a controlled environment for testing fintech innovations under tailored regulatory requirements to support innovation while managing risks.

Malaysia Fintech Market Report Scope

Malaysia Fintech is one of the largest Fintech industries as businesses and people are more preferring digitized means of driving financial products. It is for their investment evaluation and payments through various FinTech platforms for financial products. The report covers a complete background analysis of the Malaysia Fintech Market. It includes an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles. The Malaysia Fintech Market is segmented by service proposition (money transfer and payment, savings and investment, digital lending & lending investment, online insurance & insurance marketplaces, and others). The report offers market sizes and forecasts for the Malaysia fintech market in value (USD) for all the above segments.

By Service Proposition

| Digital Payments |

| Digital Lending & Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

By End-User

| Retail |

| Businesses |

By User Interface

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

By Geography

| Klang Valley |

| Northern Region |

| Southern Region |

| East Coast |

| East Malaysia |

| By Service Proposition | Digital Payments |

| Digital Lending & Financing | |

| Digital Investments | |

| Insurtech | |

| Neobanking | |

| By End-User | Retail |

| Businesses | |

| By User Interface | Mobile Applications |

| Web / Browser | |

| POS / IoT Devices | |

| By Geography | Klang Valley |

| Northern Region | |

| Southern Region | |

| East Coast | |

| East Malaysia |

Key Questions Answered in the Report

What is the current value of the Malaysia fintech market?

The market is valued at USD 12.07 billion in 2026.

How fast is the Malaysia fintech market expected to grow by 2031?

It is projected to expand at a 16.05% CAGR, reaching USD 25.41 billion by 2031.

Which service line holds the largest share in Malaysia’s fintech scene?

Digital payments lead with 50.72% revenue share in 2025.

Which region in Malaysia shows the quickest fintech growth outlook?

East Malaysia is forecast to record 23.7% CAGR through 2031, the fastest nationwide.

What factor most accelerates SME adoption of fintech services in Malaysia?

Government’s RM 1.5 billion (USD 315 million) Business Digitalisation Initiative subsidizes digital tools and financing, spurring SME uptake.

How concentrated is competition among Malaysia’s fintech providers?

The top five firms control 75.8% of market value, indicating moderate concentration.

Page last updated on: