Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

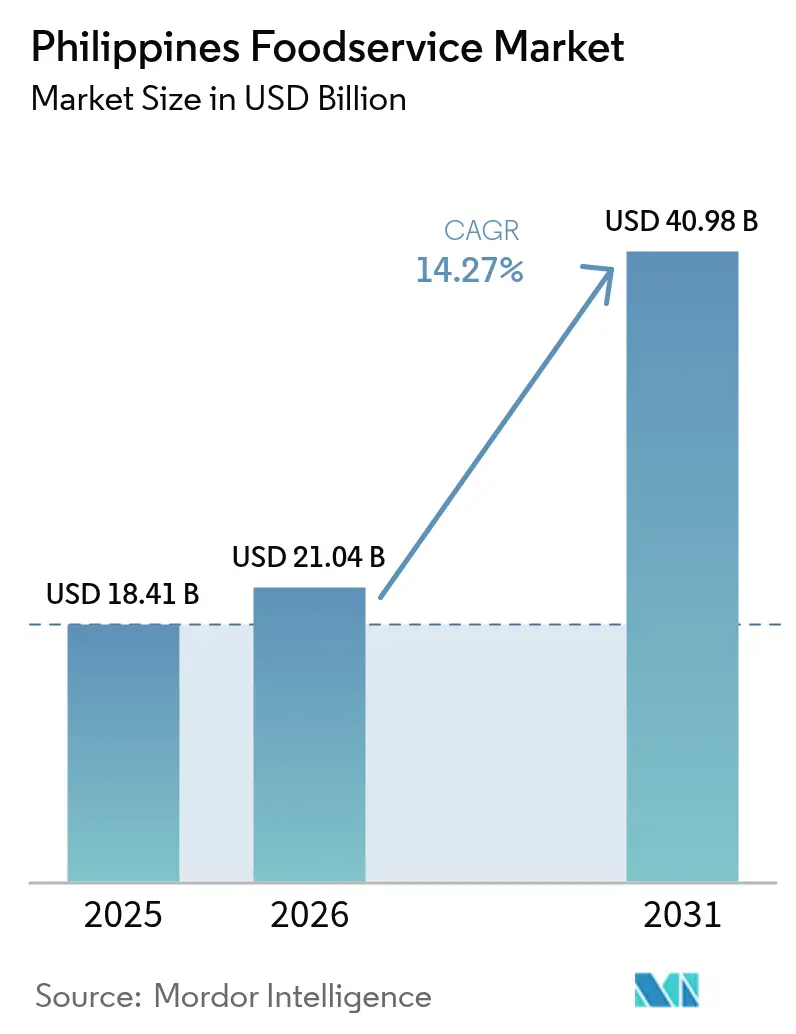

| Base Year Market Size (2025) | USD 18.41 Billion |

| Market Size (2026) | USD 21.04 Billion |

| Market Size (2031) | USD 40.98 Billion |

| Growth Rate (2026 - 2031) | 14.27% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Philippines Foodservice Market Analysis by Mordor Intelligence

The Philippines foodservice market size is expected to grow from USD 18.41 billion in 2025 to USD 21.04 billion in 2026 and is forecast to reach USD 40.98 billion by 2031 at 14.27% CAGR over 2026-2031. This growth translates to a robust CAGR of 14.52%, outpacing many of its Southeast Asian counterparts. Factors such as sustained urban migration, a burgeoning middle class with increased purchasing power, and heightened smartphone penetration are driving traffic in both physical and digital realms. This dynamic environment is ripe for innovative formats and expansive franchising. Operators adept at omnichannel fulfillment, stringent supply-chain management, and menu localization are reaping significant rewards, particularly in the densely populated areas of Metro Manila. As landlords reassess retail spaces, cloud kitchens are transitioning from niche players to mainstream contenders. Meanwhile, dine-in spaces, designed for social media appeal, are capitalizing on consumers' desire for Instagram-worthy experiences. In this competitive landscape, technology adoption, spanning from kitchen automation to AI-driven promotions, is proving to be the key differentiator for securing repeat business.

Key Report Takeaways

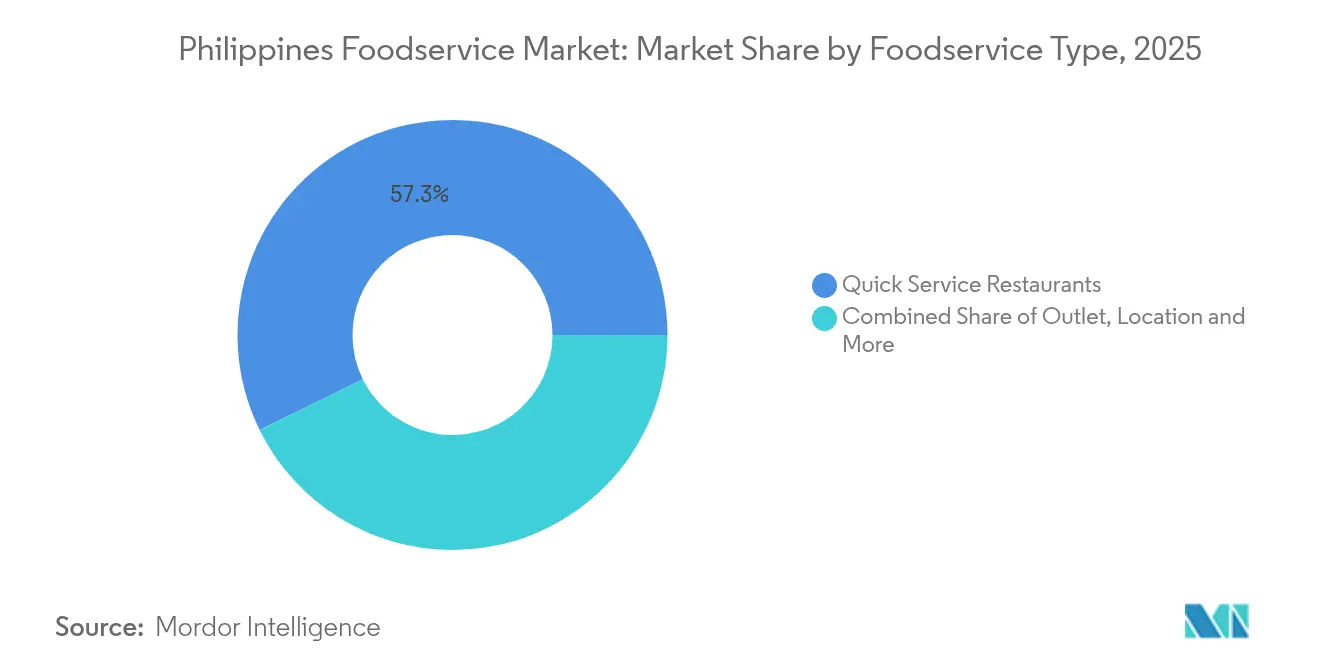

- By foodservice type, Quick Service Restaurants led with 57.28% revenue share in 2025, while Cloud Kitchens are forecast to expand at a 24.85% CAGR through 2031.

- By outlet, independent operators held 74.42% of the Philippines' foodservice market share in 2025, yet chained concepts are advancing at a 14.18% CAGR to 2031.

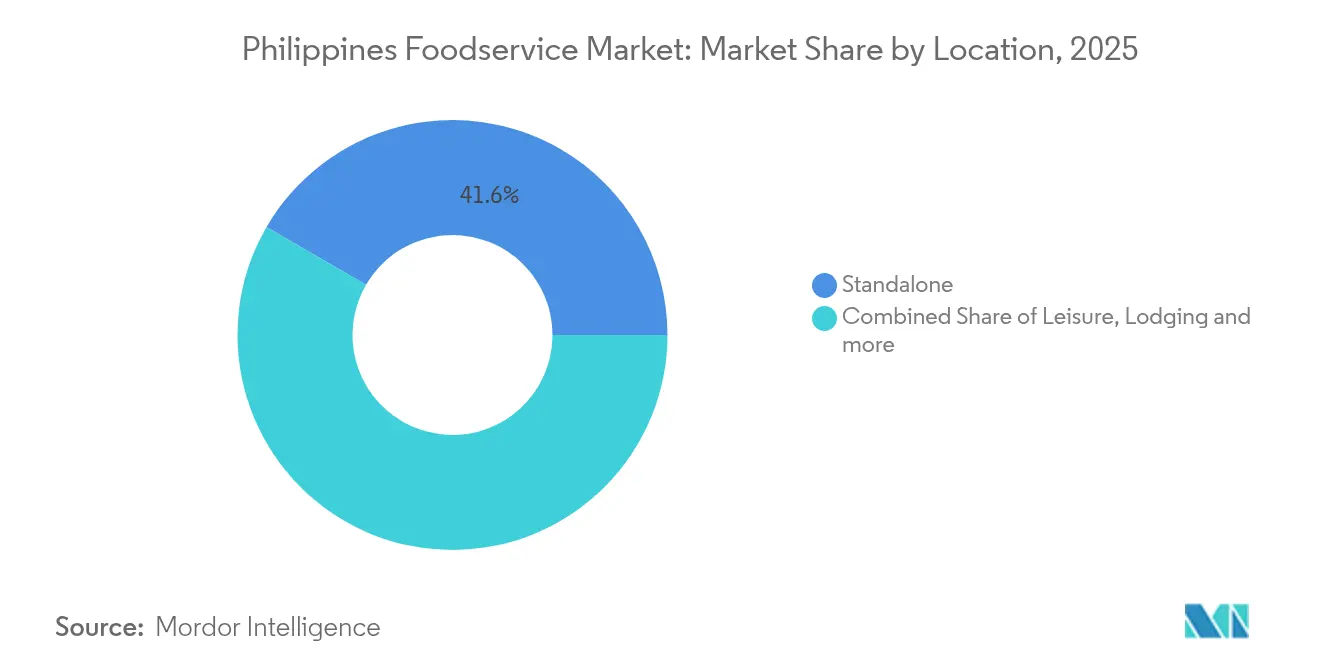

- By location, standalone stores captured 41.63% of spend in 2025, whereas lodging-based venues are projected to grow at a 14.9% CAGR through 2031 as tourism spending rebounds.

- By service type, dine-in maintained a 52.64% share in 2025, but delivery is accelerating at a 15.78% CAGR on the back of digital platform reach and gains in curbside pickup infrastructure.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Cloud and Virtual Kitchens in Major Cities | +3.2% | Metro Manila, Cebu, Davao with spillover to provincial cities | Medium term (2-4 years) |

| Experiential, Social-Media-Friendly Dine-in Formats | +2.8% | Urban centers nationwide, concentrated in NCR and regional hubs | Short term (≤ 2 years) |

| Strong Café Culture and Modern Tea Concepts Boosting Dayparts | +2.1% | National, with early gains in Manila, Cebu, Baguio | Medium term (2-4 years) |

| Omnichannel Formats and Curbside/Pick-Up Infrastructure | +2.4% | Metro Manila and major urban centers, expanding to Tier 2 cities | Short term (≤ 2 years) |

| Sustainability Focus: Food-Waste Reduction and Responsible Sourcing | +1.9% | National implementation, led by major chains | Long term (≥ 4 years) |

| Personalization and Build-Your-Own Formats Driving Loyalty | +2.6% | Urban millennials and Gen Z demographics nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Cloud and Virtual Kitchens in Major Cities

Cloud kitchens are transforming the foodservice industry in the Philippines by eliminating the need for front-of-house operations and enabling multiple brands to operate from a single production facility. This model significantly reduces capital investment by 40-50% compared to traditional restaurants, allowing businesses to test new ideas with lower financial risk. The growing preference for online-to-offline (O2O) models, with the majority of consumers favoring this approach, has driven GrabFood to focus on integrated omnichannel experiences. This shift has created a strong demand for cloud kitchens, particularly in the densely populated urban areas of Metro Manila. Additionally, the Department of Trade and Industry, in partnership with Jollibee Foods Corporation, is supporting the growth of micro, small, and medium enterprises (MSMEs) by introducing cloud kitchen frameworks. These frameworks provide smaller operators with access to delivery platforms, which is especially important in a market where independent outlets account for 75% of the market share but often lack the resources to establish traditional storefronts in high-traffic areas.

Experiential, Social-Media-Friendly Dine-in Formats

Restaurants are transforming into spaces designed for content creation, driven by the fact that most consumers rely on in-app reviews before choosing where to dine, and younger audiences are heavily influenced by user-generated content. A notable example is Jollibee's September 2024 launch of its JolliBrews coffee concept, which combines high-quality beverages with visually appealing, Instagram-friendly interiors to encourage social media sharing. According to operators, locations optimized for social media attract 25-30% more foot traffic and can charge higher prices for unique experiences that traditional QSR formats cannot offer. This shift goes beyond just aesthetics, incorporating interactive dining, personalized food presentations, and theatrical meal preparation, all of which turn dining into shareable experiences. In Metro Manila's highly competitive market, this approach has proven effective, as creating memorable and engaging experiences now plays a more critical role in attracting customers than simply competing on price or convenience.

Strong Café Culture and Modern Tea Concepts Boosting Dayparts

The café culture in the Philippines is rapidly evolving, filling gaps in consumption occasions that traditional quick-service and full-service restaurants have not fully addressed. These gaps are most evident during mid-morning and afternoon periods when office workers seek alternatives to standard meal options. Jollibee's USD 340 million acquisition of Compose Coffee in October 2024 highlights the growing importance of premium coffee in capturing these specific time slots. Compose Coffee, South Korea's second-largest coffee chain with over 2,400 stores, represents a strategic move to strengthen Jollibee's position in this market. Filipino consumers are becoming more knowledgeable about coffee, showing interest in factors like origin, brewing techniques, and flavor profiles. This shift has fueled the growth of modern tea concepts and specialty coffee shops, which are capitalizing on the premiumization trend. Expanding into these time slots is particularly profitable in commercial areas, where steady foot traffic throughout the day provides opportunities to generate revenue beyond the usual lunch and dinner peaks.

Sustainability Focus: Food-Waste Reduction and Responsible Sourcing

Jollibee has partnered with SWAPP and Nutricycle to convert 1,572 metric tons of food waste into fertilizer. This initiative not only highlights the operational scale required to achieve meaningful sustainability but also reduces costs by lowering disposal fees. Similarly, Mang Inasal has reached zero-waste-to-landfill status at its commissary operations, setting a high standard for the industry. However, smaller operators may find it challenging to replicate this achievement without substantial capital investment. The World Food Programme has identified climate-related risks that threaten food security in the Philippines, emphasizing the need for responsible sourcing practices to strengthen supply chain resilience rather than focusing solely on short-term cost reductions. Additionally, consumer awareness of environmental issues is growing, particularly among urban millennials who increasingly consider sustainability when choosing where to dine. This trend provides a competitive advantage to businesses that can genuinely demonstrate their environmental efforts while also raising the overall expectations for all market participants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perishable Supply Chain Gaps and Cold-Chain Limitations | -1.8% | National, acute in provincial areas and island provinces | Medium term (2-4 years) |

| Food Safety, Traceability, and Sustainability Compliance Overhead | -1.4% | National implementation, higher impact on smaller operators | Long term (≥ 4 years) |

| Consumer Pushback on Ultra-Processed Items | -1.2% | Urban centers, spreading to provincial markets | Medium term (2-4 years) |

| Labor Shortages and High Staff Turnover | -1.5% | National, most acute in Metro Manila and tourist destinations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Perishable Supply Chain Gaps and Cold-Chain Limitations

The Philippines' archipelagic geography creates significant logistics challenges, with temperature-controlled shipping costs rising 15-25% compared to ambient transportation across its 7,641 islands. This cost disparity complicates the movement of perishable goods, particularly for businesses reliant on cold-chain logistics. The World Food Programme's analysis of climate vulnerabilities and food security risks highlights the fragile nature of the supply chain, which directly impacts the availability of ingredients and the stability of pricing. Although the Department of Agriculture introduced Administrative Order No. 20 in April 2024 to simplify agricultural import procedures, it does not address the lack of adequate cold storage infrastructure in provincial areas[1]The Lawphil Project, "Strengthening Administrative Procedures And Policies, And Eliminating Non-tariff Barriers On Agricultural Imports", lawphil.net. This shortfall disrupts menu consistency for operators managing multiple locations. Smaller operators are disproportionately affected, as they lack the resources to invest in dedicated cold-chain systems or negotiate better rates with logistics providers.

Labor Shortages and High Staff Turnover

The Philippines' foodservice sector continues to face significant labor challenges, even with its large working-age population. These challenges stem primarily from competition with the business process outsourcing (BPO) sector, which attracts workers by offering higher pay and better working conditions. To address workforce issues, McDonald's has partnered with TESDA to create a specialized training program for quick-service restaurants (QSRs), signaling the industry's recognition of the need for systematic workforce development. High employee turnover, especially in entry-level positions, remains a critical issue. This turnover drives up training expenses and negatively impacts service quality during periods when new employees are still learning operational processes. The problem is more pronounced in Metro Manila and key tourist destinations, where rising living costs outpace wage growth. As a result, many workers are forced to take on multiple jobs or relocate to more affordable areas. The adoption of remote cashier services, where Philippine-based staff serve international markets, showcases how technology can help mitigate labor shortages. However, this solution is largely limited to larger operators with the financial resources to invest in advanced systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: QSR Dominance Meets Cloud Innovation

In 2025, Quick Service Restaurants (QSRs) hold a commanding 57.28% market share, driven by local players who effectively combine affordability with cultural relevance to appeal to Filipino consumers. Jollibee Foods Corporation exemplifies this approach by offering localized menu options and expanding its presence through approximately 200,000 franchise outlets nationwide. This strategy highlights how QSR operators achieve operational efficiency while catering to regional taste preferences. The segment benefits from well-established supply chain networks, standardized employee training programs, and strong brand loyalty, which collectively lower customer acquisition costs compared to newer competitors. The QSR model remains resilient by meeting the needs of busy urban consumers who value speed and consistency over elaborate dining experiences, ensuring stable revenue even during economic challenges.

Cloud Kitchens are emerging as the fastest-growing segment, with a projected CAGR of 24.85% through 2031. This model is transforming foodservice economics by eliminating front-of-house expenses, which typically account for 30-40% of a traditional restaurant's budget. By focusing on delivery, operators can test multiple brand concepts from a single kitchen, reducing capital investment by 40-50% compared to conventional restaurants, while still offering diverse menu options to meet varied consumer preferences. The Department of Trade and Industry, in partnership with Jollibee Foods Corporation, is supporting MSME growth by introducing cloud kitchen frameworks. These frameworks provide smaller operators with access to delivery platforms, bypassing the high costs associated with traditional storefronts. In densely populated areas like Metro Manila, where high real estate costs make traditional restaurant spaces unaffordable for new brands, cloud kitchens offer a practical solution. The segment's rapid growth reflects shifting consumer habits, with majority of consumers now preferring omnichannel options that prioritize convenience over the social aspects of dining out.

By Outlet: Independent Resilience Amid Chain Consolidation

In 2025, independent outlets dominate the Philippine foodservice market with a 74.42% share, reflecting the country's strong entrepreneurial dining culture. These family-owned establishments act as community hubs, preserving regional culinary traditions that chains struggle to replicate. Their flexibility allows quick menu adjustments based on seasonal ingredients, local festivals, and neighborhood preferences, avoiding the delays of corporate processes. Low entry barriers and Filipinos' preference for supporting local businesses give independents a lasting competitive edge. They offer authentic regional dishes like Bicol Express and Lechon, maintaining cultural authenticity and sourcing practices that chains find hard to standardize.

Chained outlets are growing at a 14.18% CAGR through 2031, driven by demand for consistent quality, standardized service, and reliable brands. Fruitas Holdings' USD 12.8 million investment in August 2024, including a 60% stake in Mang Bok's roasted chicken chain, highlights strong investor confidence in scalable models. Chains benefit from 10-15% cost savings on ingredients through supply chain efficiencies and use technology for inventory, customer management, and menu optimization. Consolidation is accelerating as chains leverage brand recognition to secure prime locations in malls and commercial districts. Kuya J Food Group's PHP 100 million (USD 1.8 million) expansion plan in June 2024, along with openness to investor partnerships, underscores the importance of scaling to compete with market leaders.

By Location: Standalone Flexibility Versus Lodging Growth

In 2025, standalone locations hold a 41.63% market share, highlighting operators' focus on brand control and flexibility. This strategy helps restaurants build unique identities, set their own hours, and quickly adapt to market changes without relying on mall or hospitality approvals. By mid-2025, food and beverage operators led retail demand, favoring standalone sites for their ability to offer tailored dining experiences. This format works well for local chains and independent operators, who prioritize community connections and customized menus over the foot traffic benefits of malls or hotels.

Lodging-based establishments are growing the fastest, with a 14.9% CAGR through 2031, driven by tourism recovery and infrastructure improvements. The hotel sector’s pipeline includes 158 establishments with 40,084 rooms, creating significant opportunities for foodservice operators. Tourism, expected to contribute 21.3% to the national economy by 2024, drives demand for dining options that cater to both hotel guests and locals seeking premium experiences. Lodging partnerships provide steady demand and a platform to showcase Filipino cuisine to international visitors, who may promote the brand abroad. Retail, leisure, and travel locations serve distinct needs: retail benefits from shopping center traffic, leisure captures recreational spending, and travel caters to transportation hub audiences.

By Service Type: Dine-In Stability Meets Delivery Acceleration

In 2025, dine-in services command a 52.64% market share, a testament to Filipino cultural values that prioritize communal dining, family gatherings, and the social connections fostered during shared meals. This preference underscores a tradition where dining transcends mere sustenance; Filipinos often linger for 2-3 hours at restaurants during weekend family gatherings, a stark contrast to the 30-45 minute average for weekday meals. Jollibee's September 2024 debut of its JolliBrews coffee concept underscores a trend: operators are curating dine-in experiences with social-media-friendly interiors, aiming to boost dwell times and user-generated content, thereby elevating brand visibility. Traditional dine-in formats typically see transaction values 20-30% higher than delivery orders, capitalizing on opportunities to upsell beverages, desserts, and premium items, especially when diners are in groups. The dine-in segment thrives on experiential elements—like live cooking demos, tableside service, and an ambiance enriched by music and décor—that delivery can't replicate.

Delivery services are on an upward trajectory, boasting a 15.78% CAGR through 2031. This growth is fueled by a 90% consumer preference for omnichannel experiences, bolstered by digital platform penetration and infrastructure enhancements that broaden delivery coverage across Metro Manila's bustling urban corridors. McDonald's 2024 rollout of chatbots for recruitment across 635 stores highlights the tech investments essential for delivery operations. These investments ensure quality during transport and adeptly manage order volumes, which can surpass dine-in capacity during peak times. The burgeoning delivery segment paves the way for niche delivery-only brands and cloud kitchens. These entities can fine-tune kitchen layouts for swift order fulfillment, sidestepping the need for dining space.

Geography Analysis

Metro Manila remains the Philippines' foodservice market leader, but secondary cities are gaining traction with rising investments and consumer spending. The National Capital Region's dense population, advanced infrastructure, and higher disposable incomes make it ideal for premium dining and international brands. However, in the first half of 2025, majority of food and beverage retail demand came from outside Metro Manila, highlighting growing interest in provincial markets with less competition and better real estate costs.

Cebu and Davao are becoming key secondary markets, driven by a growing middle class, improved infrastructure, and regional economic growth. Dining concepts once exclusive to Manila are now expanding into these cities. Chooks-to-Go's plan to open 1,900 outlets nationwide reflects the shift toward geographic diversification to reduce reliance on Metro Manila's competitive and costly environment. The Department of Trade and Industry supports this expansion with technical and financial assistance for operators entering underserved areas. Infrastructure projects improving transportation and logistics further support this regional growth.

Tourism recovery is creating new opportunities in destinations like Boracay, Palawan, and Bohol, where international visitors drive demand for premium and experiential dining. A USD 4.5 billion hotel investment, signals sustained demand for foodservice catering to travelers. Geographic diversification helps operators capture growth in emerging regional centers while maintaining a presence in Metro Manila. Provincial markets also offer lower labor costs and less competition for talent, addressing challenges like high staff turnover and wage pressures in Metro Manila.

Competitive Landscape

The Philippines foodservice market is moderately consolidated, with a mix of international chains, domestic brands, and regional players competing across quick-service, full-service, and café segments. Leading players such as Jollibee Foods Corporation, Alliance Global Group, Inc. (McDonald’s PH), Max’s Group, Inc., Shakey’s Pizza Asia Ventures, Inc., Starbucks Corporation maintain a strong foothold through extensive outlet networks, efficient supply chains, and consistent product innovation. Their established brand equity and economies of scale enable them to dominate urban centers, while local chains continue to strengthen their presence by catering to regional taste preferences and offering affordable menu options.

Technology adoption emerges as a key competitive differentiator, with leading operators implementing AI systems, self-ordering kiosks, and integrated omnichannel platforms that enhance operational efficiency while improving customer experiences. Jollibee Group's AI implementation and McDonald's chatbot deployment across 635 stores demonstrate the scale of technological transformation required to maintain competitive advantages in an increasingly digital marketplace.

White-space opportunities exist in underserved segments like premium casual dining, health-focused concepts, and regional cuisine specialization, where operators can establish market leadership before larger competitors recognize these niches. The regulatory environment, overseen by the Department of Trade and Industry and Philippines FDA, creates compliance frameworks that favor operators with established quality systems while potentially limiting market entry for undercapitalized competitors.

Philippines Foodservice Industry Leaders

-

Jollibee Foods Corporation

-

Starbucks Corporation

-

Max’s Group, Inc.

-

Shakey’s Pizza Asia Ventures, Inc.

-

Alliance Global Group, Inc. (McDonald’s PH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Malaysia’s OldTown White Coffee announced its plan of P400 million expansion in the Philippines focused on Visayas and Mindanao over the next five years, anchored by its Philippine licensee Del Mundo Group and a growing presence starting with Zamboanga City openings. According to the company, the investment will fund 20 new outlets—split evenly between Mindanao and Visayas—building on the brand’s 11-store footprint since its 2023 debut and targeting emerging regional hubs beyond Metro Manila.

- March 2025: Eat Pizza has opened its second Philippine branch at SM Mall of Asia after debuting at SM North EDSA, signaling a steady buildout of the Korean 10‑inch “slide” pizza concept locally in 2025. The MOA store sits on the 3rd floor of the North Entertainment Mall. It showcases the brand’s individual rectangular pizzas and Korean‑inspired flavors, with management indicating more locations are slated this year as momentum builds.

- February 2025: Malaysia’s ZUS Coffee announced its plans to add 150 new Philippine stores in 2025, accelerating after surpassing 100 outlets roughly 16 months post‑entry and positioning as one of the market’s fastest‑growing coffee chains.

- October 2024: Jollibee Foods Corporation completed its USD 340 million acquisition of Compose Coffee, South Korea's second-largest coffee chain with over 2,400 stores, marking the company's largest international acquisition and strategic entry into the premium coffee segment across Asia-Pacific markets.

Philippines Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.

Foodservice Type

| Cafes & Bars | By Cuisine | Bars & Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee & Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

Outlet

| Chained Outlets |

| Independent Outlets |

Location

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

Service Type

| Dine-in |

| Takeaway |

| Delivery |

| Foodservice Type | Cafes & Bars | By Cuisine | Bars & Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee & Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| Outlet | Chained Outlets | ||

| Independent Outlets | |||

| Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms