Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

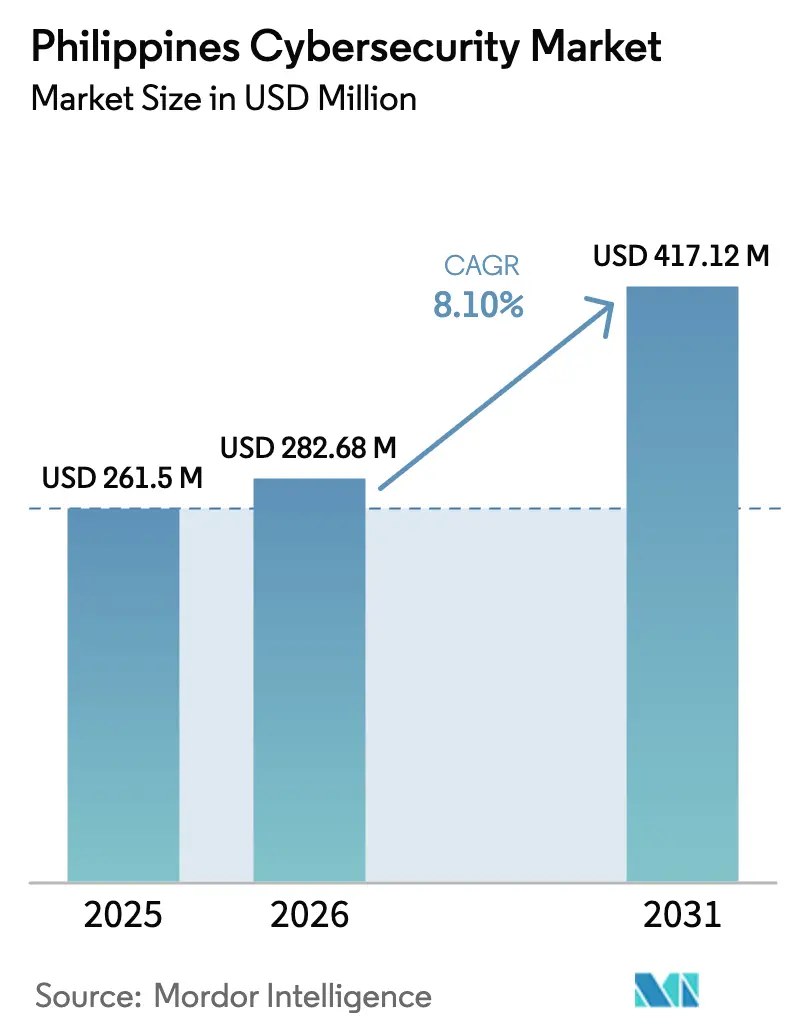

| Base Year Market Size (2025) | USD 261.5 Million |

| Market Size (2026) | USD 282.68 Million |

| Market Size (2031) | USD 417.12 Million |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Cybersecurity Market Analysis by Mordor Intelligence

The Philippines cybersecurity market size in 2026 is estimated at USD 282.68 million, growing from 2025 value of USD 261.5 million with 2031 projections showing USD 417.12 million, growing at 8.10% CAGR over 2026-2031. This trajectory stems from heightened digitization, 5G build-outs, and a national focus on cyber-resilience, even as state-sponsored attacks multiply. A closer reading of the spending patterns shows that cybersecurity is shifting from a discretionary information-technology line item to a foundational pillar of nationwide digital infrastructure. Banking, business-process outsourcing, and telecommunications operators treat effective cyber defenses as prerequisites for revenue growth because service reliability now underpins customer trust. Meanwhile, continued talent shortages, overlapping regulations, and the high price of sophisticated threat-intelligence tools dilute adoption among smaller firms and provincial agencies.

Key Report Takeaways

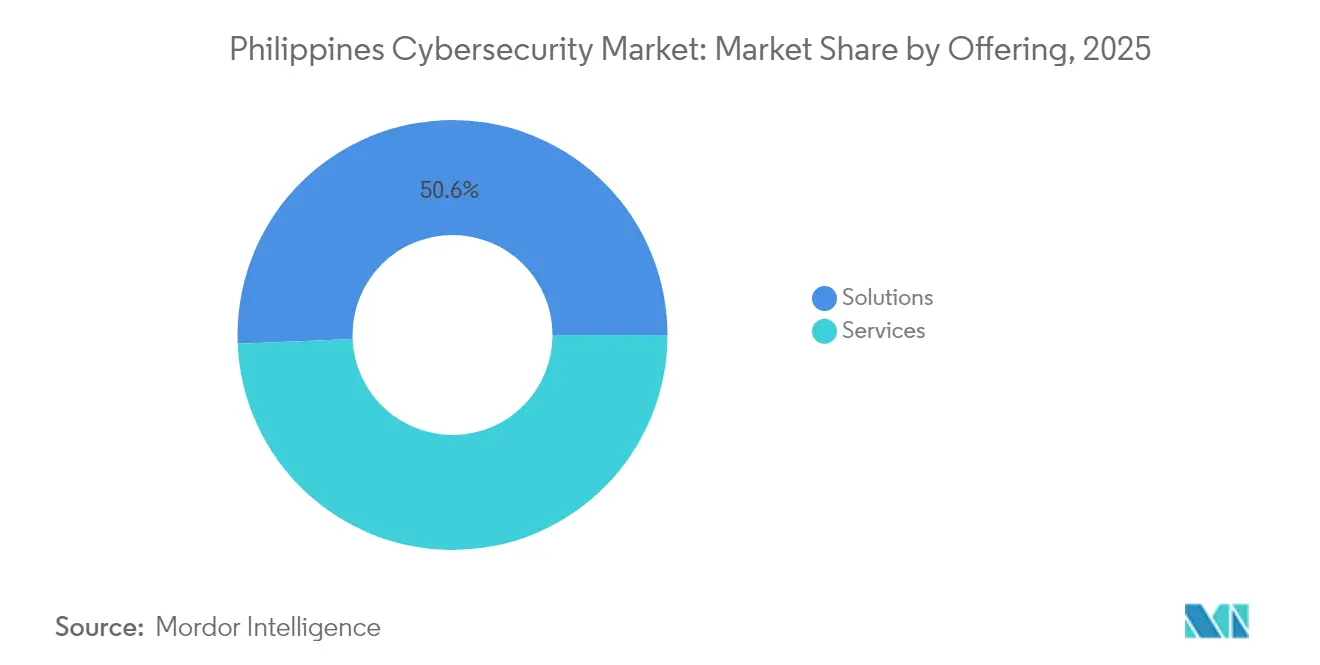

- By offering, solutions captured 50.65 % of Philippines cybersecurity market share in 2025, while services are expected to log the fastest 9.45 % CAGR through 2031.

- By deployment mode, on-premise installations led with 53.90 % revenue share in 2025; cloud deployments are forecast to expand at 10.95 % CAGR to 2031.

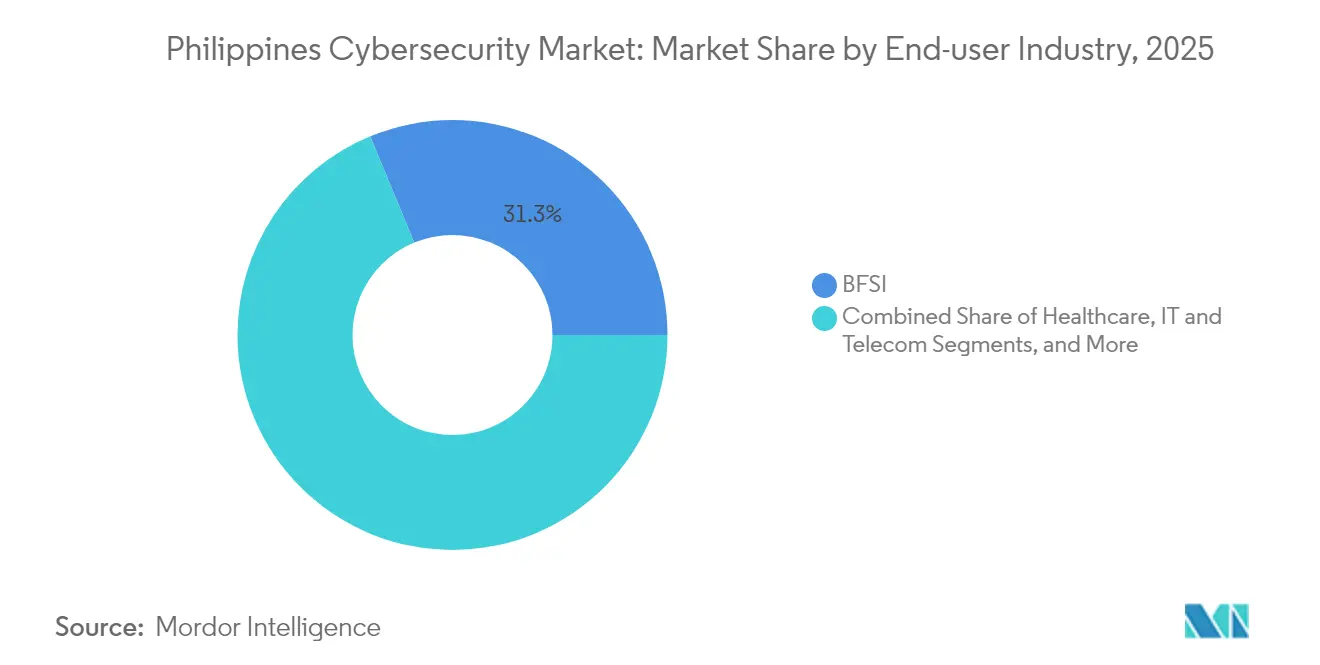

- By end-user industry, the BFSI segment held 31.25 % of the Philippines cybersecurity market size in 2025; healthcare is poised for the highest 11.35 % CAGR across the forecast period.

- By end-user enterprise size, large enterprises commanded 62.10 % share of the Philippines cybersecurity market size in 2025, whereas SMEs are projected to grow at a 10.05 % CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cybersecurity Plan 2022-2028 funding boosts enterprise security procurement | +2.5 % | Metro Manila, Cebu, Davao | Medium term (2-4 years) |

| Expansion of IT-BPM and BPO exports demanding compliance with global security frameworks | +2.1 % | NCR, Cebu, Clark | Short term (≤ 2 years) |

| Rapid e-wallet and digital banking adoption accelerating threat-surface in BFSI | +1.8 % | Urban centers nationwide | Short term (≤ 2 years) |

| 5G rollout and IoT pilots in smart cities raising critical-infrastructure protection spend | +1.5 % | Metro Manila, planned smart cities | Medium term (2-4 years) |

| Surge in ransomware attacks on healthcare and public agencies forcing incident-response investments | +2.3 % | Nationwide | Short term (≤ 2 years) |

| AI-led incident-response platforms | +1.2 % | NCR, regional SOC hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Cybersecurity Plan 2022-2028 funding boosts enterprise security procurement

The Philippine government’s National Cybersecurity Plan 2023-2028 establishes workforce-development, policy, and critical-infrastructure milestones that accelerate private procurement cycles. Enterprises formerly hesitant to upgrade are now aligning projects with the plan’s compliance checkpoints, redirecting capital from discretionary pilots to full production roll-outs. The clarity of mandated controls—rather than sheer budget volume—has become the primary catalyst for action, especially among government suppliers seeking contract eligibility. Early beneficiaries include domestic managed security service providers that deliver monitoring and incident response aligned to public-sector benchmarks. The plan’s visibility also unlocks multilateral funding for cyber-capacity-building in rural jurisdictions.

Expansion of IT-BPM and BPO exports demanding compliance with global security frameworks

Global clients increasingly require SOC 2 and ISO 27001 attestation from Philippine outsourcing vendors, recasting cybersecurity as a revenue-gatekeeper instead of a back-office safeguard. Large BPOs have responded by embedding security operations centers into bid proposals and by allocating dedicated compliance squads to sustain audit readiness. Mid-tier providers follow suit to avoid losing high-value contracts, driving security investments beyond Manila into secondary hubs such as Cebu and Clark. This dynamic positions cybersecurity certifications as non-tariff trade barriers: without them, service providers struggle to penetrate regulated verticals like healthcare or financial services. Consequently, even cost-sensitive firms now budget for continuous monitoring and third-party risk management.

Rapid e-wallet and digital banking adoption accelerating threat-surface in BFSI

Digital payment transactions surpassed the 50 % threshold and reached 52.8 % of volume in 2024, exposing banks and e-wallet operators to sophisticated fraud schemes [1]Department of Information and Communications Technology, “National Cybersecurity Plan 2023-2028,” dict.gov.ph. Financial institutions deploy AI-based analytics for real-time anomaly detection, partner with anti-fraud specialists, and roll out customer education campaigns to curb account takeover incidents. The Bangko Sentral ng Pilipinas advances new cybersecurity guidelines that require robust risk-management frameworks for electronic money issuers. These combined pressures foster a notable shift from perimeter-centric tools toward identity and access management, zero-trust network access, and secure mobile SDKs. The net effect is an enlarged budget line for authentication and behavior-analytics software within bank technology roadmaps.

5G rollout and IoT pilots in smart cities raising critical-infrastructure protection spend

Nationwide 5G coverage and flagship projects like the 407-hectare New Manila Bay – City of Pearl create an interwoven operational-technology (OT) ecosystem that expands the threat landscape. Telecommunications carriers such as Globe Telecom allocate USD 12–15 million annually to cybersecurity upgrades, embedding OT firewalls and secure IoT gateways in their capital-expenditure plans [2]Palo Alto Networks, “Globe Investing USD 12-15 Million Annually in Cybersecurity,” paloaltonetworks.com. Municipal planners now stipulate cybersecurity controls at the blueprint stage, reversing historic tendencies to retrofit defenses post-deployment. This pre-emptive approach shifts procurement toward integrated platforms capable of monitoring both IT and OT domains from a single dashboard.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of GIAC/CISSP-certified talent inflating project lead-times | −1.9 % | Nationwide | Medium term (2-4 years) |

| Cyber-security budgets of Philippine SMEs remain below 2% of IT spend | −1.5 % | Provinces | Medium term (2-4 years) |

| Fragmented data-privacy rules (DICT, BSP, NPC) complicate compliance roadmaps | −1.2 % | Nationwide | Short term (≤ 2 years) |

| High capex for threat-intel platforms deterring adoption outside top-tier banks | −0.8 % | Tier-2/3 financial institutions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of GIAC/CISSP-certified talent inflating project lead-times

The Philippines has fewer than 300 GIAC or CISSP-certified cybersecurity professionals in active roles, compared with roughly 3,000 in Singapore, creating a sharp supply-demand gap that stalls complex implementation projects. Lengthy recruitment cycles push deployment timelines beyond planned windows, prompting some enterprises to shelve upgrades or down-scope feature sets to fit the available workforce. The scarcity also inflates salary premiums, raising total cost of ownership for on-premise solutions that require in-house administration. Domestic experts are frequently recruited by overseas employers offering higher pay, deepening the local deficit and eroding institutional knowledge. As a result, organizations pivot toward cloud security services and automation tools that reduce reliance on specialist talent while still meeting baseline compliance obligations.

Cyber-security budgets of Philippine SMEs remain below 2% of IT spend

Small and medium enterprises collectively allocate less than 2 % of their IT budgets to security, despite forming a large share of the national business base. Executives in this segment often believe they are unlikely targets, overlooking their role as potential entry points into larger supply chains. Limited budgets restrict adoption to basic endpoint protection, leaving gaps in network monitoring, backup hygiene, and incident response readiness. Recent outreach programs by telcos and insurers tie cyber-insurance eligibility to the implementation of fundamental controls, but uptake remains inconsistent because many SMEs view compliance as an avoidable overhead. Consequently, attackers exploit these softer targets to harvest data or pivot into higher-value enterprises, illustrating how underinvestment at the grassroots level undermines the broader national security posture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Outpace Solutions as Talent Gap Widens

Solutions retained 50.65 % Philippines cybersecurity market share in 2025, but services are projected to outgrow them at a 9.45 % CAGR through 2031. Enterprises prefer external expertise to compensate for the country’s pool of fewer than 300 certified specialists. Network and cloud security products remain foundational, while identity-and-access management gains board attention amid soaring account-takeover fraud. Professional services—especially consulting and advisory—see brisk demand as firms navigate overlapping mandates from the Department of Information and Communications Technology, the National Privacy Commission, and the central bank.

Managed security services record double-digit growth and absorb work once handled by in-house security operations centers. Integration projects often face delays because of limited engineering headcount, steering customers toward turnkey cloud-delivered platforms. Vendors differentiate by embedding automation, reducing reliance on scarce human analysts. The talent shortage therefore functions as both a restraint on do-it-yourself deployments and a growth lever for service revenue.

By Deployment Mode: Cloud Dominance Reflects Digital-First Strategy

On-premise architectures led the market with 53.90 % share in 2025, yet cloud deployments are slated to expand at 10.95 % CAGR, the fastest among all modes. Banks, retailers, and government portals adopt cloud-native security to exploit elastic scaling and rapid patch cycles. This progression reframes cloud economics from cost minimization to risk mitigation: constantly updated controls trump capex savings. Hybrid blends appeal to conglomerates with legacy data centers, providing control over crown-jewel workloads while consuming SaaS analytics for broad visibility.

As nationwide talent shortages persist, many enterprises portray cloud security as a workaround that outsources labor-intensive maintenance to specialized providers. Compliance teams, once wary of offshore data residency, now leverage regionally hosted clouds that satisfy local sovereignty stipulations. Consequently, cloud adoption has matured into a strategic pillar, not a tactical stopgap.

By End-user Industry: BFSI Leads While Healthcare Shows Highest Growth

The BFSI sector held 31.25 % of the Philippines cybersecurity market size in 2025, reinforced by central-bank mandates and aggressive digital banking expansion. UnionDigital, for example, achieved profitability within its first year by intertwining AI-driven fraud detection with user experience design . Security investments now emphasize identity orchestration, behavioral biometrics, and API security to protect open-banking interfaces.

Healthcare is forecast to grow fastest at 11.35 % CAGR as hospitals and insurers scramble to close gaps revealed by large-scale ransomware events such as the PhilHealth breach that exposed data of 42 million individuals. Rising regulatory penalties, combined with the life-and-death stakes of medical service continuity, catalyze spending on immutable backups, endpoint detection and response, and network micro-segmentation. Government and defense retain double-digit growth momentum, pushed by tri-lateral cyber-defense agreements and expanded civilian recruitment into military cyber units.

By End-user Enterprise Size: SMEs Accelerate Adoption Despite Budget Constraints

Large enterprises controlled 62.10 % of the Philippines cybersecurity market size in 2025, driven by strict governance and publicly disclosed multimillion-dollar security allocations. Their priority is platform consolidation to achieve single-pane-of-glass visibility across fragmented subsidiaries. SMEs, although reluctant to funnel more than 2 % of IT spend into security, are projected to grow at 10.05 % CAGR amid heightened breach publicity and bundling of cyber-insurance with telco connectivity.

Cloud-priced, pay-as-you-go offerings resonate with SME cash-flow realities. Partnerships, such as a 2024 deal between an insurtech provider and Globe Telecom, offer discounted premiums for firms that implement baseline controls. This linkage between insurance eligibility and security practice nudges smaller organizations toward adopting modern defenses, particularly endpoint protection, secure email gateways, and basic SOC-as-a-service.

Geography Analysis

Metro Manila anchors demand, housing headquarters of major banks, telcos, and ministries. Its dense concentration of commercial data centers and universities supports a vibrant ecosystem of security integrators and start-ups. Policy moves issued in the capital quickly cascade to provincial offices, setting baselines for procurement specifications. The proximity of regulators also streamlines audit cycles, encouraging enterprises to pilot cutting-edge tools before broader rollout.

Secondary hubs—Cebu, Davao, and Clark—experience rising cybersecurity outlays as global BPO operators add seats and cloud providers build regional data centers. Local governments embed cyber-resilience clauses into smart-city contracts, spurring demand for OT-specific firewalls and asset-visibility solutions. MSSPs open satellite SOCs in these cities to guarantee low-latency incident response, positioning themselves closer to client premises and regional universities for talent pipelines.

Rural provinces, though currently a smaller slice of the Philippines cybersecurity market, show steady uptake driven by digital public-service portals and financial-inclusion initiatives. Micro-finance institutions roll out secure mobile apps to reach unbanked citizens, demanding baseline encryption and anti-malware capabilities. Universal-service funds earmarked for broadband expansion now include cyber-awareness modules, seeding future demand among local government units. Over time, decentralization of economic activity is likely to spawn federated security architectures that balance central guidance with regional autonomy.

Competitive Landscape

The competitive environment is moderately concentrated, with the top five vendors estimated to hold significant Philippines cybersecurity market share. Cisco leads, leveraging a broad MSSP ecosystem and deep bench in network security appliances. Fortinet follows at winning mid-market accounts via channel partners that bundle SD-WAN with firewall subscriptions. Trend Micro, anchored by its Manila R&D center, controls substantial share through strong endpoint and cloud workload offerings.

Telecommunications providers intensify competition by embedding security in connectivity packages. Globe Business and PLDT Enterprise market cloud-delivered secure web gateways, DDoS scrubbing, and threat-intelligence feeds. Their network vantage points grant them real-time telemetry, enhancing anomaly detection for customers without dedicated SOCs. Partnerships with hyperscale cloud platforms further elevate their credibility among multinational tenants seeking seamless cloud-to-network protection.

Talent scarcity shapes product road maps: automation, managed detection and response, and low-touch SaaS modules dominate new releases aimed at lowering total cost of ownership. Vendors increasingly differentiate on operational efficacy—mean time to detect, analyst augmentation, and contextual alerting—rather than feature checkbox depth. Future consolidation is likely to favor providers that marry AI-driven analytics with strong local support, mitigating the structural skills deficit that constrains enterprise security teams.

Philippines Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems Inc.

Fortinet Inc.

Trend Micro Inc.

Palo Alto Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: In Manila, Philippines, the Australian Defence Force (ADF) teamed up with the Philippine Army for a joint defensive cyber operation, aiming to bolster regional cybersecurity efforts.

- July 2025: The Philippines has introduced the Cybersecurity Council, a groundbreaking initiative that brings together leaders from government, business, and academia to establish a national strategy for cybersecurity.

- January 2025: BlueVoyant reported that 84 % of surveyed Philippine organizations suffered at least one breach in 2024, averaging 3.13 incidents.

- November 2024: Viettel Cyber Security (VCS) has launched a pioneering free cyber threat check service in the Philippines, addressing the pressing need for organizations to bolster their defenses.

Philippines Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware, malware, and phishing to maintain data confidentiality.

The Philippines cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current Philippines cybersecurity market size?

The market stands at USD 282.68 million in 2026 and is projected to reach USD 417.12 million by 2031.

How fast is the Philippines cybersecurity market expected to grow?

Analysts forecast an 8.10 % CAGR between 2026 and 2031, fueled by digital-payment adoption, 5G rollouts, and national-level cyber initiatives.

Which segment currently leads by market share?

Solutions held 50.65 % of revenue in 2025, though services are positioned for faster growth as firms outsource expertise.

Why are managed security services popular in the Philippines?

A shortage of certified professionals pushes enterprises to outsource monitoring, incident response, and compliance tasks to MSSPs.

Page last updated on: