Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 196.33 Billion |

| Market Size (2031) | USD 268.37 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

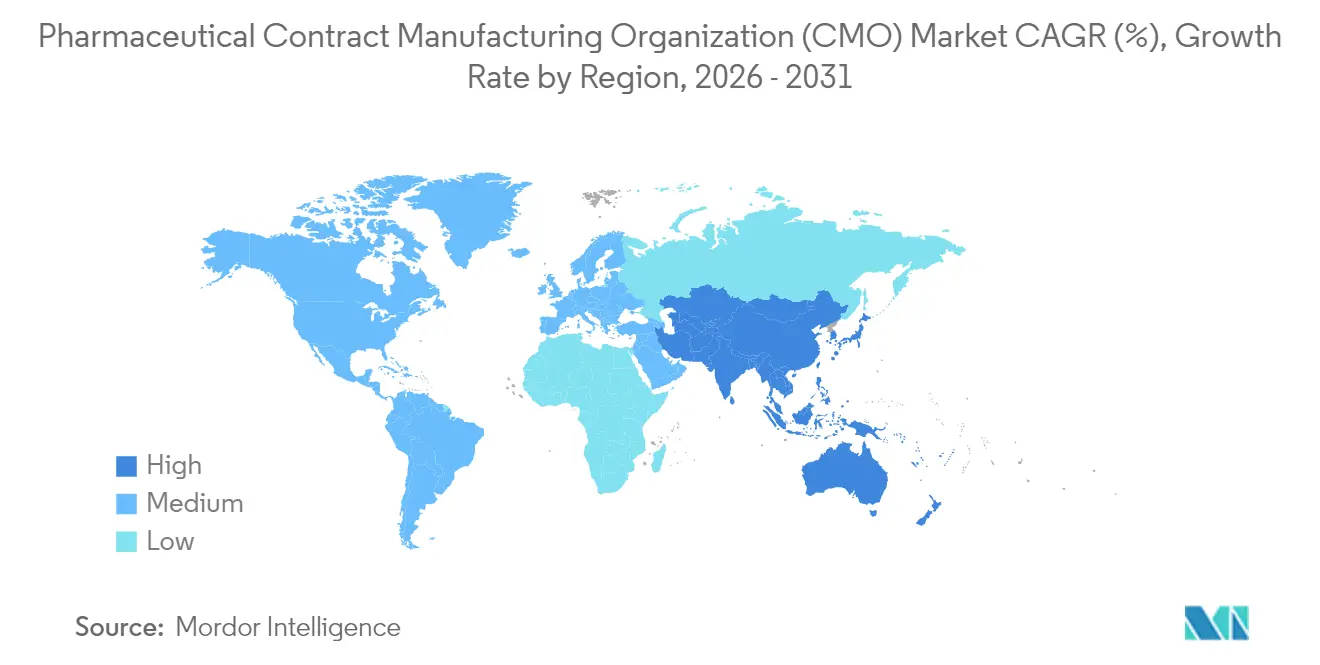

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

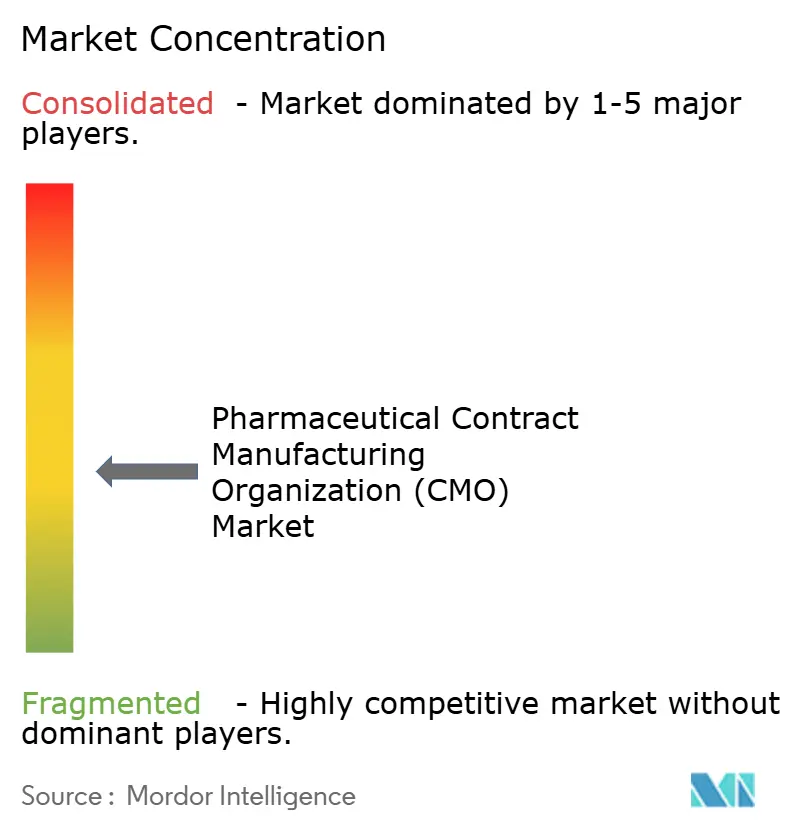

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Contract Manufacturing Organization (CMO) Market Analysis by Mordor Intelligence

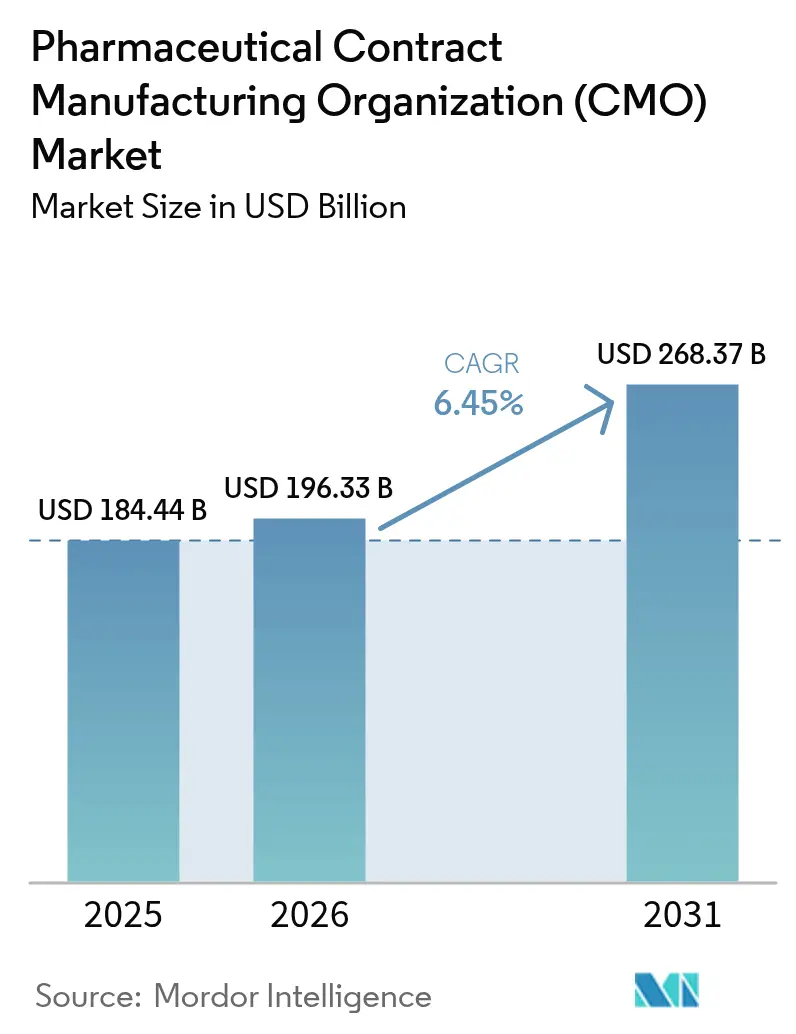

The pharmaceutical contract manufacturing organization market size is expected to grow from USD 184.44 billion in 2025 to USD 196.33 billion in 2026 and is forecast to reach USD 268.37 billion by 2031 at 6.45% CAGR over 2026-2031. Momentum stems from the industry’s strategic realignment toward core discovery and commercialization tasks, leaving complex production activities to specialized partners. Venture-capital inflows into virtual biotechs, record approvals of advanced therapies, and expanding high-potency API pipelines are reinforcing the shift toward external capacity. Meanwhile, cost pressures, regulatory scrutiny, and the need for state-of-the-art technologies are motivating big pharma, specialty players, and generics alike to deepen collaboration with qualified contract manufacturers. Providers able to bundle development, scale-up, and fill-finish services while maintaining global quality standards continue to capture disproportionate opportunities within the pharmaceutical contract manufacturing organization market. [1]“FDA Announces Enhanced Inspection Protocols for 2024,” U.S. Food and Drug Administration, fda.gov

Key Report Takeaways

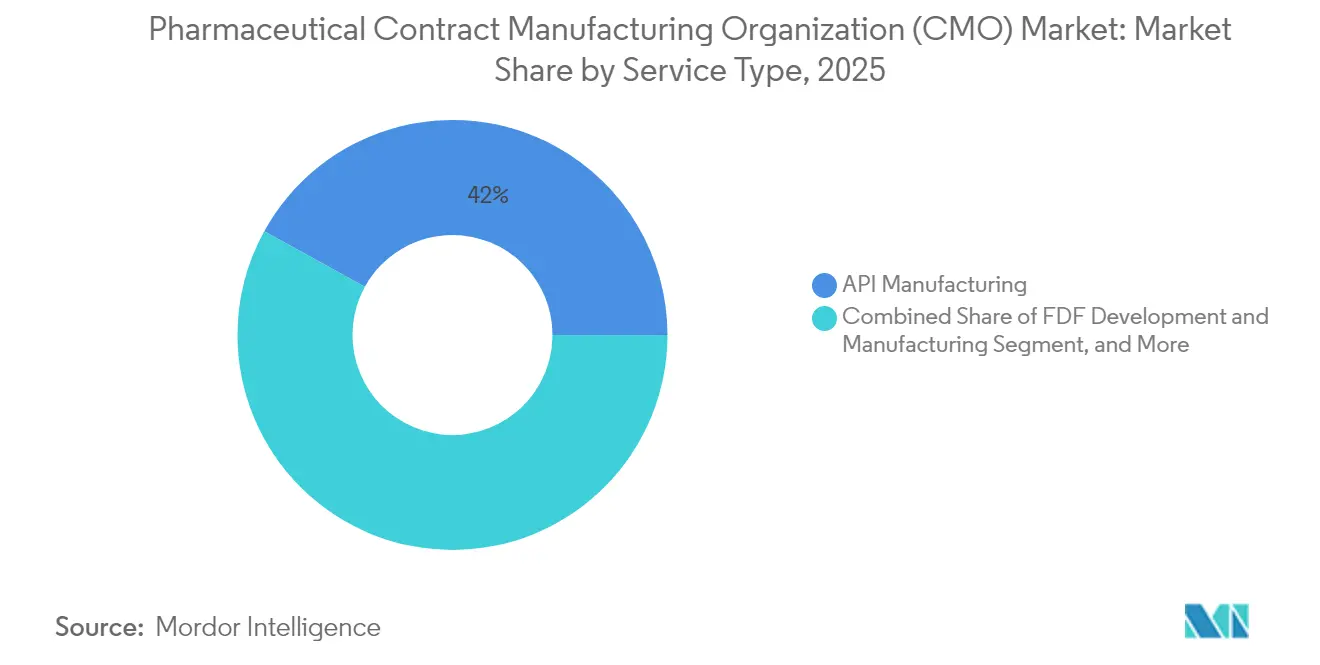

- By service type, API manufacturing led with 41.98% of the pharmaceutical contract manufacturing organization market share in 2025, at a 6.44% CAGR through 2031.

- By scale of operation, commercial-scale agreements delivered 61.75% of 2025 revenue, and clinical-phase manufacturing is advancing at a 7.74% CAGR through 2031.

- By drug molecule, Small molecules still accounted for 56.85% of 2025 revenue, and advanced therapies are projected to expand at an 8.22% CAGR to 2031.

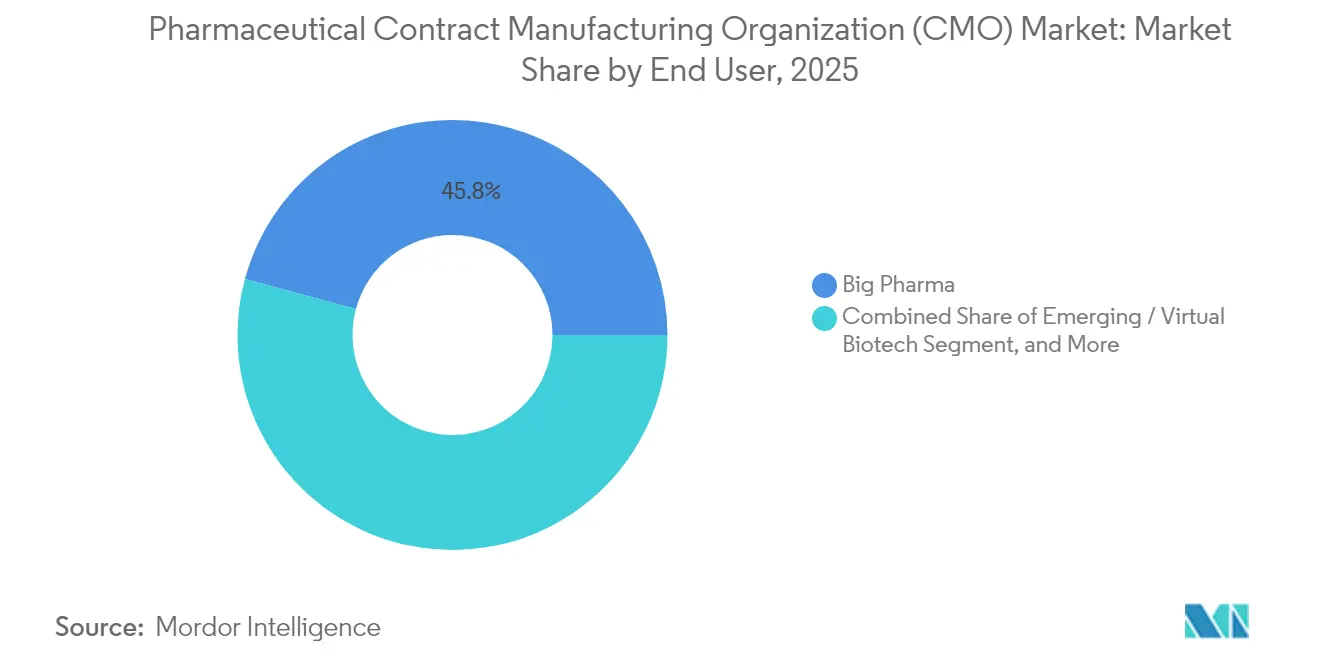

- By end user, large pharmaceutical sponsors represented 45.80% of revenue in 2025. However, emerging and virtual biotechs are rising fastest at a 6.89% CAGR to 2031.

- By therapeutic area, oncology generated 38.10% of 2025 revenue, central nervous system assets are accelerating at 8.88% CAGR to 2031.

- By geography, North America held 39.85% of 2025 revenue, and Asia-Pacific is recording the highest regional CAGR at 8.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Contract Manufacturing Organization (CMO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating small and mid-sized pharma outsourcing | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Rising biologics pipeline complexity | +1.5% | Global, with APAC manufacturing hubs gaining share | Long term (≥ 4 years) |

| Increasing venture-capital funded virtual biotechs | +0.8% | North America and Europe primary, APAC secondary | Short term (≤ 2 years) |

| Demand spike for high-potency APIs (HPAPIs) | +0.9% | Global, with specialized facilities in developed markets | Medium term (2-4 years) |

| Growth of cell and gene therapy CDMO capacity | +1.1% | North America and Europe leading, APAC emerging | Long term (≥ 4 years) |

| ESG-linked supply chain qualification | +0.4% | Global, with stricter requirements in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Small and Mid-Sized Pharma Outsourcing

Escalating compliance costs after the FDA’s 2024 inspection overhaul elevated annual quality expenses by USD 2-5 million for mid-tier plants. The capital burden is steering resource-constrained sponsors toward strategic outsourcing across oncology and rare-disease portfolios. Contract manufacturers with integrated development and commercial capabilities benefit from predictable pipeline inflows, while hybrid fee-for-service and risk-sharing models are gaining traction.

Rising Biologics Pipeline Complexity

Multi-specific antibodies, antibody-drug conjugates, and autologous cell therapies require distinctive upstream cell culture, purification, and cold-chain infrastructure that few innovators can justify in-house. Samsung Biologics committed USD 2.4 billion in 2024 to expand single-use bioreactor capacity, signaling the scale of investment necessary for modern biologics production.[2]“Samsung Biologics Announces USD 2.4 Billion Capacity Expansion,” Samsung Biologics, samsungbiologics.com Providers offering turnkey process development, viral clearance, and fill-finish services are now critical partners across biologics life cycles.

Increasing Venture-Capital-Funded Virtual Biotechs

Venture investors poured USD 15 billion into asset-light biotech startups during 2024, many of which operate without brick-and-mortar laboratories. These companies favor agile, milestone-based contracts, encouraging CDMOs to provide modular suites, real-time batch visibility, and tech-transfer readiness across multiple production sites. Flexible capacity allocation and rapid scale-up remain central differentiators for winning virtual biotech mandates.

Demand Spike for High-Potency APIs (HPAPIs)

Targeted oncology drugs, hormones, and immunomodulators increasingly rely on sub-microgram dosing regimens that mandate stringent containment and sophisticated occupational-exposure controls. Greenfield HPAPI suites often exceed USD 50 million per facility, prompting sponsors to rely on specialized contractors. CDMOs with closed isolator systems and validated cleaning protocols capture premium pricing and multi-year contracts as HPAPI pipelines grow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capacity bottlenecks in fill-finish lines | -0.7% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Escalating regulatory inspections and remediation costs | -0.5% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Volatile single-use-systems supply | -0.3% | Global, affecting biologics manufacturing primarily | Short term (≤ 2 years) |

| Currency-driven cost inflation in emerging hubs | -0.4% | APAC and emerging markets primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capacity Bottlenecks in Fill-Finish Lines

Utilization above 85% and lead times exceeding 18 months for complex injectables limit CDMOs’ ability to absorb new biologics programs. Sterile suites, advanced robotics, and serialization upgrades demand multi-year investments that delay relief, keeping short-term supply tight and potentially constraining near-term revenue realization.

Escalating Regulatory Inspections and Remediation Costs

The FDA’s enhanced framework lengthened average audits by 40% while expanding data-integrity checks. Observations linked to electronic batch records or aseptic deviations can trigger remediation costs up to USD 50 million, eroding margins for smaller providers and driving consolidation in the pharmaceutical contract manufacturing organization market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: API Manufacturing Remains Foundational

API manufacturing held 41.98% of pharmaceutical contract manufacturing organization market share in 2025, underpinning broad generic and branded drug demand. While small-molecule volumes stay dominant, biologics and HPAPI capacity additions are shifting revenue mix toward higher-value offerings. Clients increasingly seek integrated services that co-locate synthesis, purification, and final dosage manufacturing to eliminate supply handoffs.

Contractors offering both solid-dose and injectable dose formulation capture economies of scope. Digital serialization, continuous manufacturing, and predictive maintenance are reshaping operating cost curves, creating new competitive thresholds for entry. Integration with packaging services, particularly tamper-evident and track-and-trace solutions, further differentiates providers.

By Drug Molecule Type: Advanced Therapies Lead Growth

Small molecules still accounted for 56.85% of 2025 revenue, yet advanced therapies pushed the fastest expansion at an 8.22% CAGR. Viral vector production, cell expansion know-how, and cryogenic storage now dominate CAPEX priorities as developers chase one-time curative potential. The pharmaceutical contract manufacturing organization market size for advanced therapies is projected to broaden as more approved products transition from autologous to allogeneic processes, necessitating larger, standardized manufacturing runs.

Biologics occupy an intermediate growth position thanks to biosimilar adoption and novel antibody formats. Sustained investment across all molecule classes affirms the strategic imperative for CDMOs to maintain diversified technology portfolios rather than single-platform specialisms.

By Scale of Operation: Clinical Manufacturing’s Rising Weight

Commercial-scale agreements delivered 61.75% of 2025 revenue, reflecting entrenched blockbuster supply contracts. Yet clinical-phase work is expanding at 7.74% CAGR, powered by record global R&D outlays of USD 244 billion in 2024. Flexible batch sizes, rapid changeovers, and regulatory filing support define success factors as clients demand speed over unit cost in early development.

Clinical services increasingly serve as first touchpoints that evolve into long-term commercial partnerships, locking in share of wallet throughout product life cycles in the pharmaceutical contract manufacturing organization market.

By End User: Virtual Biotech Momentum

Large pharmaceutical sponsors represented 45.80% of revenue in 2025, leveraging hybrid make-or-buy models to preserve capital and manage peaks in demand. However, emerging and virtual biotechs are rising fastest at a 6.89% CAGR, attracted to CDMOs with integrated discovery-to-commercial platforms. Their need for project management, regulatory documentation, and global supply orchestration positions full-service providers ahead of niche players.

Generics and specialty pharma sustain steady volumes, but price competition underscores the need for operational excellence and continuous improvement within the pharmaceutical contract manufacturing organization industry.

By Therapeutic Area: Oncology Still Commands the Largest Slice

Oncology generated 38.10% of 2025 revenue, riding immunooncology, antibody-drug conjugate, and precision medicine breakthroughs. Central nervous system assets are accelerating at 8.88% CAGR following approvals of Alzheimer’s and rare neurology treatments. CDMOs with capability in blood-brain-barrier-penetrating formulations gain share in this emerging opportunity space.

Cardiovascular and infectious disease programs remain important but grow more slowly. Therapeutic diversification shields the pharmaceutical contract manufacturing organization market from single-area cyclicality while pressuring providers to maintain broad technology arsenals.

Geography Analysis

North America held 39.85% of 2025 revenue, supported by strong intellectual property frameworks, proximity to drug innovators, and deep regulatory expertise. Ongoing investment in continuous manufacturing and cell-therapy infrastructure keeps the region a preferred partner location, though high labor costs limit incremental capacity additions.

Asia-Pacific is the fastest-growing region at a 8.91% CAGR, propelled by scale investments in China, India, and South Korea. Samsung Biologics’ USD 2.4 billion build-out exemplifies regional commitment to state-of-the-art biologics capacity. Currency volatility and evolving quality expectations pose operational challenges, yet lower fixed costs and government incentives sustain its attractiveness within the pharmaceutical contract manufacturing organization market.

Europe enjoys stable demand thanks to established clusters in Germany, Ireland, Switzerland, and Scandinavia. Harmonized EMA regulations foster cross-border supply chains, particularly in advanced therapies. Middle East and Africa remain nascent but show potential as governments pursue medicine security and local manufacturing mandates.

Competitive Landscape

The market remains moderately fragmented as no single provider controls more than 10% share. Lonza, Catalent, and Samsung Biologics leverage scale and integrated offerings to stay ahead, while mid-tier specialists focus on HPAPI, sterile injectables, or viral vectors. Recent vertical integration moves such as Novo Holdings acquiring Catalent aim to create end-to-end platforms spanning discovery, development, and manufacturing.

Technology adoption is a decisive differentiator. Continuous manufacturing, digital twins, and AI-driven predictive quality management are moving from pilot to routine deployment. Providers with validated electronic batch records and advanced analytics improve real-time release testing, trimming cycle times and winning premium contracts.

Regulatory rigor is heightening. Adherence to ICH Q12 lifecycle guidance and FDA data-integrity expectations is now base-level entry criteria.[3]“International Council for Harmonisation Guidelines Update 2024,” ICH, ich.org Smaller providers facing rising compliance expenses are increasingly exploring mergers or divestitures, feeding a consolidation trend in the pharmaceutical contract manufacturing organization market.

Pharmaceutical Contract Manufacturing Organization (CMO) Industry Leaders

Lonza Group Ltd.

Catalent Inc.

Thermo Fisher Scientific Inc.

Samsung Biologics Co. Ltd

WuXi Biologics (Cayman) Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Samsung Biologics completed the first phase of its USD 2.4 billion expansion in Songdo, adding 180,000 L of biologics capacity.

- September 2025: Novo Holdings finalized the USD 16.5 billion acquisition of Catalent, creating a top-tier integrated services platform.

- August 2025: Lonza Group announced a EUR 1.2 billion (USD 1.3 billion) investment in cell and gene therapy suites across Europe and North America.

- July 2025: WuXi Biologics inaugurated a USD 500 million facility in Ireland with 24,000 L capacity for European clients.

Global Pharmaceutical Contract Manufacturing Organization (CMO) Market Report Scope

The study tracks and analyzes the demand for outsourcing CMO activities within the pharmaceutical industry based on current trends and market dynamics. The market numbers are derived by tracking the revenue generated by the players operating in the market who are providing CMO services. The study provides a detailed breakdown of the various types of service types. This report analyzes the factors based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The pharmaceutical CMO market is segmented by service type (active pharmaceutical ingredient (API) manufacturing (small molecule, large molecule, and high potency API (HPAPI)), finished dosage formulation (FDF) development and manufacturing (solid dose formulation (tablets and others), liquid dose formulation, and injectable dose formulation), and secondary packaging) and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe), Asia Pacific (China, India, Japan, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| API Manufacturing | Small Molecule |

| Large Molecule | |

| High-Potency API (HPAPI) | |

| FDF Development and Manufacturing | Solid Dose |

| Liquid Dose | |

| Injectable Dose | |

| Secondary Packaging |

By Drug Molecule Type

| Small Molecule |

| Biologics |

| Advanced Therapies (Cell and Gene) |

By Scale of Operation

| Clinical-Phase Manufacturing |

| Commercial-Scale Manufacturing |

By End User

| Big Pharma |

| Generic Pharma |

| Emerging / Virtual Biotech |

| Specialty Pharma |

By Therapeutic Area

| Oncology |

| Cardiovascular |

| Central Nervous System (CNS) |

| Infectious Disease |

| Other Therapeutic Areas |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Service Type | API Manufacturing | Small Molecule | |

| Large Molecule | |||

| High-Potency API (HPAPI) | |||

| FDF Development and Manufacturing | Solid Dose | ||

| Liquid Dose | |||

| Injectable Dose | |||

| Secondary Packaging | |||

| By Drug Molecule Type | Small Molecule | ||

| Biologics | |||

| Advanced Therapies (Cell and Gene) | |||

| By Scale of Operation | Clinical-Phase Manufacturing | ||

| Commercial-Scale Manufacturing | |||

| By End User | Big Pharma | ||

| Generic Pharma | |||

| Emerging / Virtual Biotech | |||

| Specialty Pharma | |||

| By Therapeutic Area | Oncology | ||

| Cardiovascular | |||

| Central Nervous System (CNS) | |||

| Infectious Disease | |||

| Other Therapeutic Areas | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the pharmaceutical contract manufacturing organization market in 2026?

The market stands at USD 196.33 billion in 2026 and is projected to reach USD 268.37 billion by 2031.

Which service category generates the highest revenue?

API manufacturing leads, holding 41.98% of 2025 revenue within the pharmaceutical contract manufacturing organization market.

Which region is expanding fastest?

Asia-Pacific posts the highest CAGR at 8.91% through 2031 thanks to cost advantages and substantial capacity investments.

What bottleneck most constrains near-term growth?

Fill-finish capacity shortages, with utilization above 85% and 18-month lead times, currently limit quick onboarding of new injectable programs.

Why are virtual biotechs important to CDMOs?

Virtual biotechs rely entirely on outsourced partners for manufacturing, driving demand for flexible, integrated services and accelerating contract volumes.

Page last updated on: