Bioplastics Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.54 Billion |

| Market Size (2031) | USD 18.89 Billion |

| Growth Rate (2026 - 2031) | 20.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioplastics Packaging Market Analysis by Mordor Intelligence

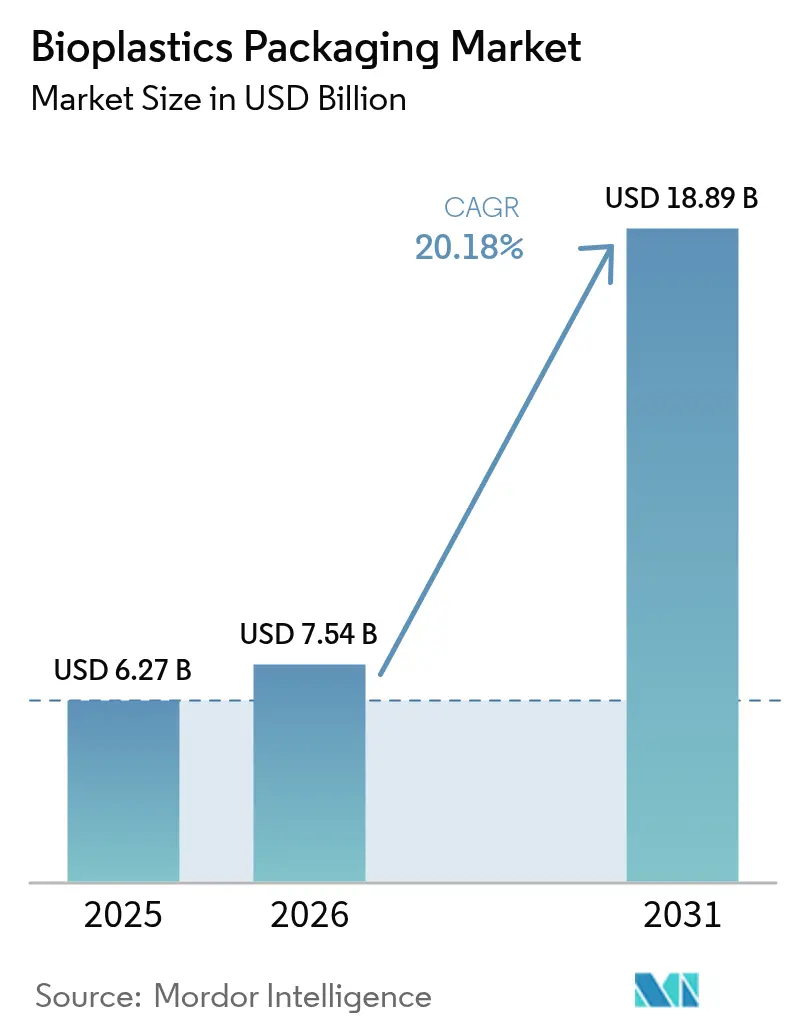

The bioplastic packaging market size is expected to grow from USD 6.27 billion in 2025 to USD 7.54 billion in 2026 and is forecast to reach USD 18.89 billion by 2031 at 20.18% CAGR over 2026-2031. Rising Extended Producer Responsibility (EPR) fees, cost-efficient bio-feedstock processing, and consumer preference for low-carbon materials are redefining supplier economics across the bioplastic packaging market. New European Union recycling targets, India’s traceability mandate, and China’s express-parcel standards are synchronizing regulatory timetables, while large PLA and Bio-PET capacity additions in the United Arab Emirates and Thailand remove legacy supply constraints. Global food-service chains and luxury personal care brands now treat bioplastic formats as mainstream, accelerating innovation in coatings, multilayer films, and barrier performance. These converging forces confirm a structural shift in packaging material choice that favors renewable feedstocks over fossil-based polymers.

Key Report Takeaways

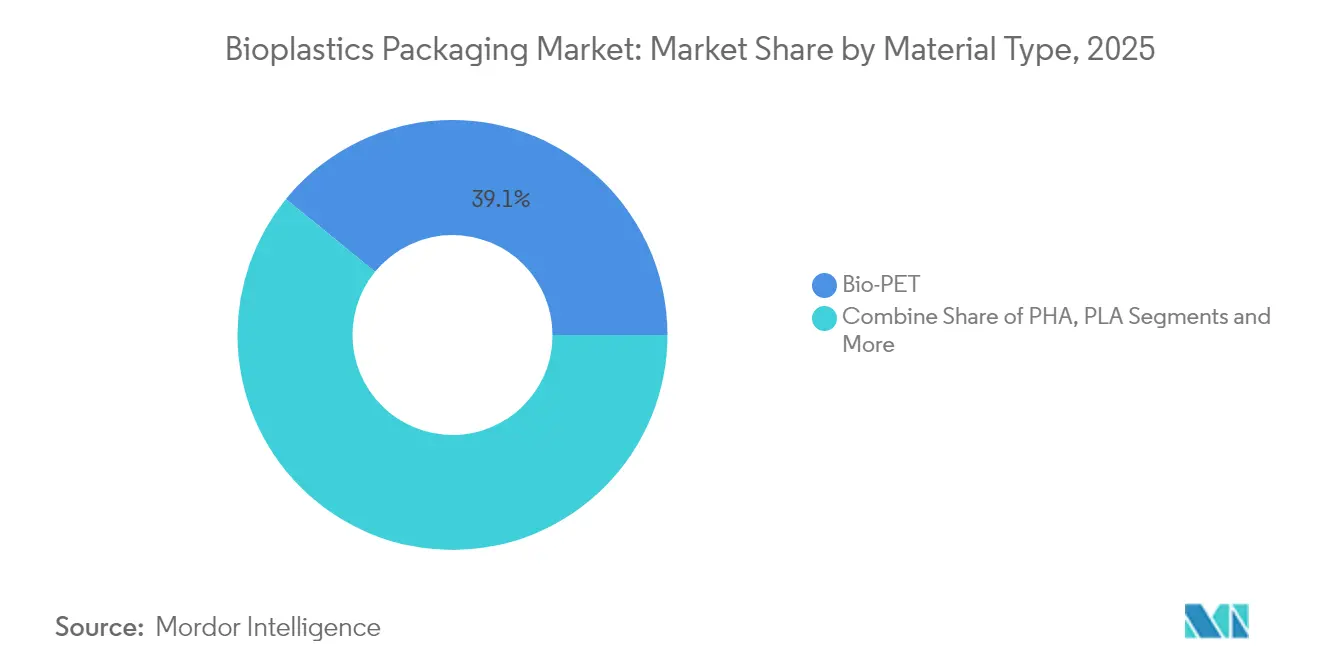

- By material type, Bio-PET led with 39.10% of bioplastic packaging market share in 2025, whereas PHA is forecast to grow at 21.65% CAGR through 2031

- By product type, flexible packaging held 57.62% revenue share in 2025 and is set to expand at a 21.05% CAGR to 2031

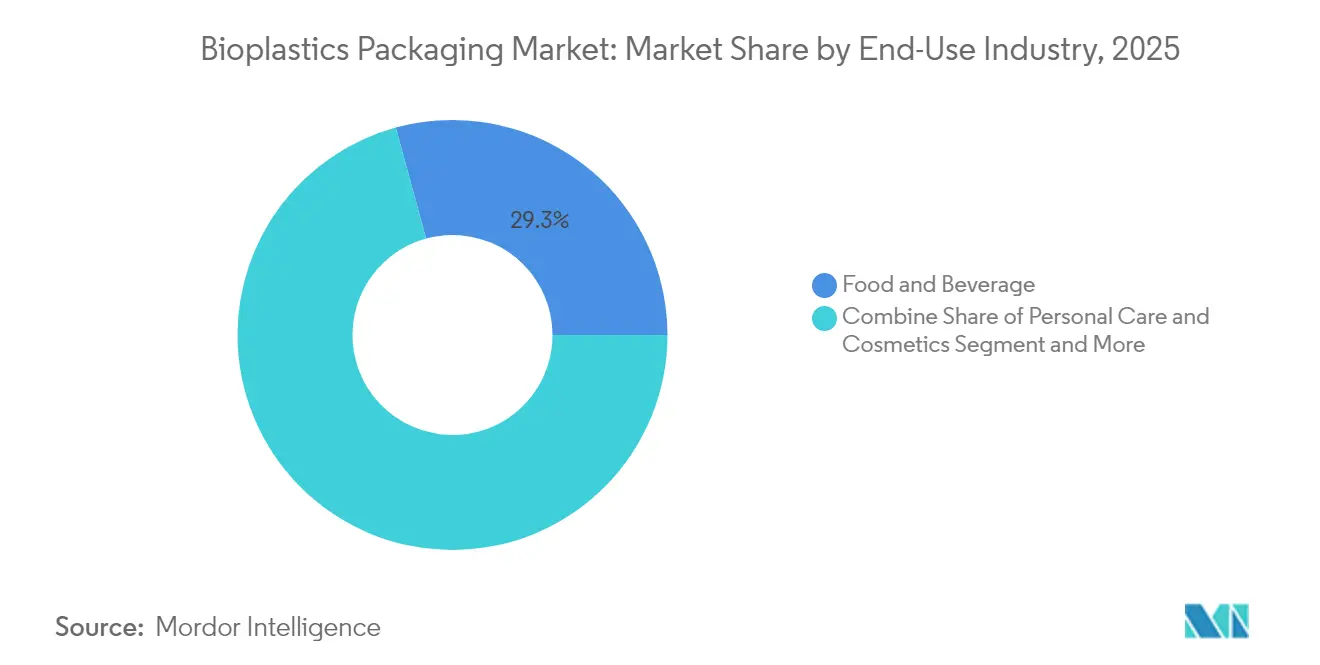

- By end-use industry, food and beverage accounted for 29.25% of the bioplastic packaging market size in 2025; personal care and cosmetics is projected to post a 20.58% CAGR between 2026-2031

- By distribution channel, direct sales captured 59.55% share of the bioplastic packaging market in 2025, while indirect channels record the fastest 20.74% CAGR through 2031

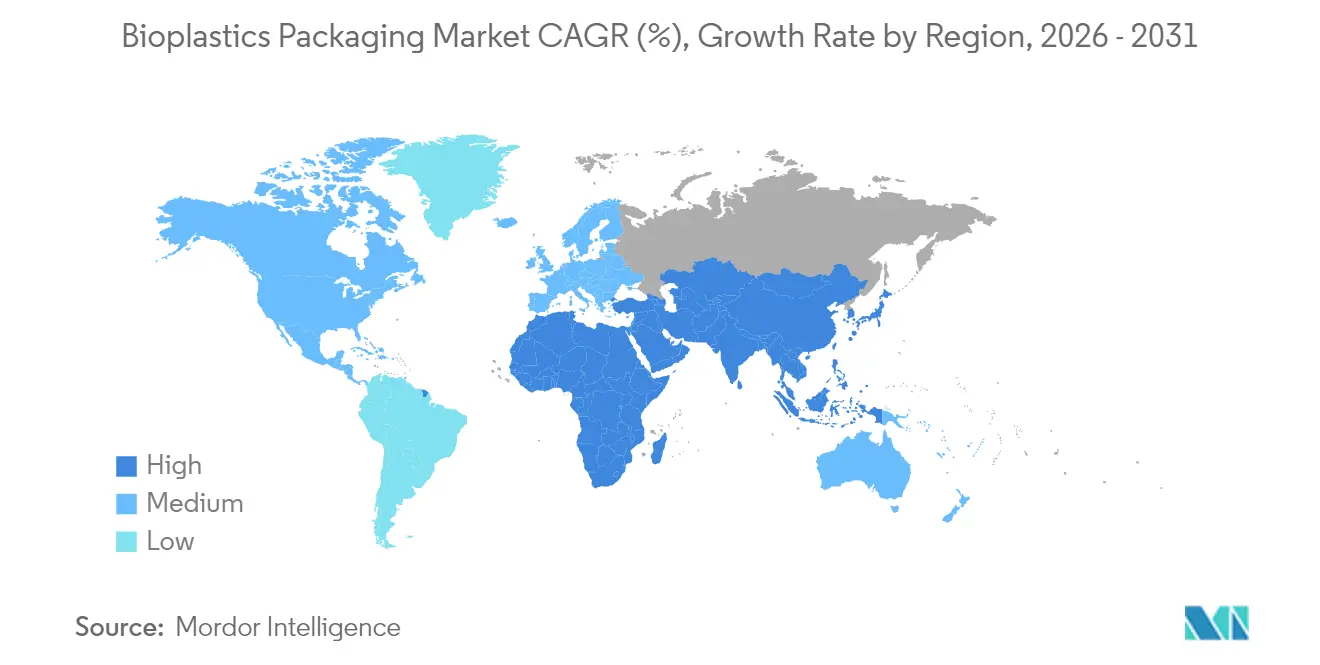

- By geography, Europe dominated with 37.95% share in 2025, whereas Asia-Pacific is the fastest-growing region at 21.93% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioplastics Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global EPR Legislation Driving Bio-Based Packaging Adoption | +4.2% | Global, with early implementation in EU, North America, and APAC | Medium term (2-4 years) |

| Demand for bioplastic packaging surges as multinational food-service chains embrace compostable packaging | +3.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Asia-Pacific Policy Shifts Creating Momentum for Bioplastic Packaging | +3.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expansion of global Bio-PET and PLA production is lowering cost barriers to adoption | +2.9% | Global, with major capacity additions in UAE, Thailand, and India | Long term (≥ 4 years) |

| Increasing adoption of bioplastic packaging among Luxury and personal care brands | +2.3% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Government Investment in Composting Infrastructure Accelerating Downstream Adoption | +1.9% | North America & EU, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global EPR legislation driving bio-based packaging adoption

Mandatory EPR schemes in California, the European Union, and Kenya internalize end-of-life costs, creating direct financial incentives to switch from conventional plastics to renewable alternatives. [1]California Legislative Information, “Senate Bill No. 54 - Plastic pollution producer responsibility,” leginfo.legislature.ca.gov Producers now face differentiated fees based on recyclability, compostability, and recycled content, making bioplastic materials more cost-competitive in the bioplastic packaging market. Harmonized reporting deadlines beginning March 2025 simplify cross-border compliance, encouraging multinational brand owners to standardize sustainable formats. Fee modulation policies that penalize non-recyclable substrates further enlarge the addressable bioplastic packaging market. As regulatory timelines converge with the start-up of large PLA plants in Thailand and the UAE, predictable supply and lower prices reinforce adoption momentum.

Demand surge from multinational food-service chains

Leading restaurant brands accelerated trials and roll-outs of compostable formats, catalyzing new volume streams in the bioplastic packaging market. McDonald’s cups now use a 50% biopolymer blend, while Starbucks has extended molded-fiber cold-cup pilots across several US states. These firms leverage procurement scale to compress per-unit resin costs and validate consumer acceptance. Operational benefits—simpler sorting, reduced landfill fees, and brand equity gains—reinforce repeat purchasing. Their rapid adoption signals to converters that bioplastic stock-keeping units can match the throughput of conventional substrates without retooling bottlenecks.

Asia-Pacific policy shifts creating momentum

India’s QR code traceability requirement beginning July 2025 and China’s GB 43352-2023 standard impose tighter controls on heavy metals and specific additives. Coupled with Japanese procurement mandates favoring bamboo and other bio-based inputs, these rules promote regional manufacturing clusters supplying the global bioplastic packaging market. Government capital subsidies, such as India’s 50% investment grant for bioplastic projects, compress payback periods on new polymer assets. Accelerated policy harmonization reduces regulatory risk, supports trade flows, and encourages multinational converters to localize flexible packaging lines closer to feedstock sources.

Capacity expansion in Bio-PET and PLA

Sulzer’s process technology underpins Emirates Biotech’s 120,000 tpa PLA mega-site, while NatureWorks secured USD 350 million to add 75,000 tpa in Thailand. Braskem boosted biopolymer output 30% in Brazil, and Toray will introduce biomass-based ABS in 2025. The resulting scale economies could narrow the historical USD 300-500/t cost gap versus petroleum PET, eroding a key barrier for the bioplastic packaging market. Geographic diversification also mitigates freight volatility and geopolitical supply risks, providing brand owners with multi-regional sourcing options to manage inventory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic shortage of bio-based feedstock owing to competing biofuel demand | -2.8% | Global, particularly acute in Brazil, USA, and EU | Long term (≥ 4 years) |

| Inconsistent industrial composting infrastructure hindering end-of-life claims | -2.1% | Global, with infrastructure gaps in developing markets | Medium term (2-4 years) |

| Functional performance limitations in high-temperature applications | -1.6% | Global, affecting food packaging and industrial applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic shortage of bio-based feedstock

Record ethanol runs in Brazil and rising US Renewable Fuel Standard volumes intensify feedstock competition, inflating corn and sugar prices that underpin PLA and Bio-PET production. Biofuel producers often win allocation battles thanks to legislated demand quotas and tax credits. While NatureWorks explores cassava and lignocellulosic routes, feedstock scarcity remains a structural headwind to the bioplastic packaging market until non-crop inputs reach scale.

Inconsistent industrial composting infrastructure

Only 185 US composters currently accept certified packaging, and many EU facilities fail to meet EN 13432 temperature thresholds. Jurisdictional inconsistencies undermine consumer trust and raise producer liability. California’s AB 1201 will enforce tighter compostability labeling in 2026, compelling converters to verify facility accessibility before mass launches. Without synchronized infrastructure upgrades, the bioplastic packaging market risks perception gaps between environmental claims and actual end-of-life outcomes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bio-PET dominance faces PHA innovation

Bio-PET held 39.10% share of the bioplastic packaging market in 2025 as producers leveraged existing PET recycling streams for rapid drop-in substitution. The segment benefits from biomass-based PTA supply chains certified under ISCC PLUS. Coca-Cola’s EUR 180 million European transition illustrates how large buyers exert downward pressure on resin premiums, supporting stable bioplastic packaging market size expansion. PHA, while only a niche share today, is forecast at 21.65% CAGR as consolidation stabilizes and specialty grades target marine-degradable applications.

Starch blends remain the volume leader among biodegradable polymers, with maize, potato, and cassava feedstocks offering price hedging flexibility. PLA capacity from Thailand and the UAE boosts regional supply, while PBAT and PBS gain traction in films requiring enhanced toughness at lower processing temperatures. Dual-sourcing strategies protect converters from resin volatility, keeping the bioplastic packaging market resilient to price shocks.

By Product Type: Flexible packaging innovation drives growth

Flexible formats commanded 57.62% of 2025 revenue and are projected to lead at a 21.05% CAGR. Films, wraps, and pouches align well with the mechanical and barrier properties of PLA and Bio-PE. Nestlé’s CHF 120 million European retrofit shows the capital needed to switch over but also demonstrates consumer acceptance premiums that offset higher resin prices. Accredo’s sugarcane-based pouch series underscores carbon-reduction gains that drive procurement decisions.

Rigid containers lag due to higher heat-deflection standards, yet multilayer PLA-cellulose structures now approach oxygen barrier levels suitable for ambient sauces. Technology spillover from flexible to rigid applications is narrowing the performance delta, opening new revenue pockets inside the broader bioplastic packaging market.

By End-Use Industry: Food sector leadership enables personal care growth

Food and beverage accounted for 29.25% revenue in 2025, underpinned by quick-service restaurant conversions and retailer own-label initiatives. Compostable serviceware simplifies waste sorting in arenas and campuses, adding high-volume outlets to the bioplastic packaging market. Personal care and cosmetics are set to post a 20.58% CAGR as L’Oréal, Estée Lauder, and Unilever channel more than USD 1 billion toward sustainable container redesigns.

Pharmaceutical use cases emerge where controlled degradation offers tamper evidence and reduced residue risk. Luxury beauty brands, producing an estimated 120 billion units annually, supply premium margins that underwrite R&D for color stability and fragrance-barrier enhancements, reinforcing long-term growth in the bioplastic packaging market.

By Distribution Channel: Direct sales efficiency supports indirect growth

Direct sales retained 59.55% share because converters require hands-on technical guidance to tailor resin blends and process settings. Amcor’s USD 45 million global partner-training spend illustrates the consultative workload behind every tonne sold. As quality grades standardize, indirect distributors are scaling at 20.74% CAGR, expanding access in secondary cities.

Digital ordering platforms now quote live carbon-footprint dashboards, allowing small brands to benchmark savings instantly. Tiered pricing still favors high-volume direct deals, yet streamlined e-commerce portals bridge the gap for emerging labels, broadening the addressable bioplastic packaging market.

Geography Analysis

Europe remained the largest regional contributor with 37.95% of the bioplastic packaging market in 2025, driven by the Packaging and Packaging Waste Regulation that mandates universal recyclability by 2030 and bans PFAS in food contact articles. Germany’s VerpackG imposed EUR 2.1 billion EPR fees in 2024, prompting brand owners to select bio-based formats that earn 30% fee discounts. Southern Europe witnesses swift adoption in fresh-produce films, while Northern markets focus on rigid yoghurt cups that meet cold-chain specifications.

Asia-Pacific is the fastest-growing region, projected at 21.93% CAGR through 2031. India’s traceability rule, China’s GB 43352-2023, and Japanese government procurement of biodegradable alternatives align policy levers with investment stimuli. NatureWorks and Balrampur Chini Mills supply domestic converters, cutting freight costs and hedging against currency swings. Proximity to agricultural feedstocks positions ASEAN nations as strategic export bases to high-demand EU markets, amplifying the bioplastic packaging market size in the region.

North America shows robust momentum as California, Oregon, and Colorado finalize EPR fee schedules that escalate annually. Food-service pilot programs at McDonald’s and Starbucks accelerate downstream converter qualifications. Federal grants worth USD 75 million for composting build-outs signal impending infrastructure parity, a critical enabler for bioplastic packaging market penetration beyond coastal cities. Canada and Mexico adopt harmonized labeling to protect cross-border supply chains, ensuring regulatory clarity for integrated brand roll-outs.

Competitive Landscape

The competitive field remains moderately fragmented. Global packaging majors integrate renewable substrates into existing lines while specialized bioplastic start-ups chase property breakthroughs. Amcor surpassed its interim target by sourcing more than 10% post-consumer resin, demonstrating how incumbents convert scale into sustainability milestones. [3] Amcor, “Sustainability Report 2024,” amcor.com Novolex’s USD 6.7 billion purchase of Pactiv Evergreen extends channel breadth to 39,000 SKUs, giving the combined firm powerful bargaining leverage with retailers.

Technology alliances dominate strategy. Amcor’s partnership with Bloom Biorenewables injects plant-waste chemistry into PET supply, while Toray and Idemitsu collaborate on biomass ABS to diversify away from sugar feedstocks . Patent filings climbed to 847 in 2024, with 34% focused on barrier improvement. Venture funding concentrates on enzymes that accelerate composting and catalysts that cut polymerization energy by 30%, hinting at a future cost step-change across the bioplastic packaging market.

Regulatory compliance deadlines from 2025 onward encourage capacity pre-booking, tightening near-term spot supply despite new plant announcements. Consequently, suppliers that guarantee on-spec resin and deliver life-cycle data win multi-year contracts. Market participants capable of backward-integrating into feedstock or forward-integrating into collection services establish defensible moats as the bioplastic packaging market pivots from niche to mainstream.

Bioplastics Packaging Industry Leaders

BASF SE (Badische Anilin- und Soda-Fabrik)

TAGHLEEF INDUSTRIES GROUP

Mitsubishi Chemical Corporation

Alpagro Packaging

Amcor Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novolex completed its USD 6.7 billion acquisition of Pactiv Evergreen, creating a diversified sustainable-packaging leader

- March 2025: Emirates Biotech broke ground on a 120,000 tpa PLA facility in the UAE with Sulzer technology

- February 2025: NatureWorks secured USD 350 million financing for its Thailand Ingeo PLA plant

- January 2025: Braskem completed a 30% biopolymer expansion, adding 60,000 tpa capacity in Brazil.

Global Bioplastics Packaging Market Report Scope

Bioplastics are plastics derived from organic sources such as corn starch and are often polylactic acid (PLA). These plastics are increasingly being adopted in the packaging industry due to their ability to break down easily and quickly compared to standard plastics. Bioplastics Packaging Market is segmented by Material Type (BIO - PET, BIO - PE, BIO - PA, Starch Blends, PLA, PBAT, PHA), Product Type (Rigid Plastic Packaging, Flexible Packaging), End-user Industries (Food, Beverage, Pharmaceuticals, Personal Care & Household Care), and Geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Non-Biodegradable Bioplastics | Bio-PET |

| Bio-PE | |

| Other Non-Biodegradable Bioplastics | |

| Biodegradable Bioplastics | Starch Blends |

| Polylactic Acid (PLA) | |

| Poly(Butylene Adipate-co-Terephthalate) (PBAT) | |

| Polybutylene Succinate (PBS) | |

| Polyhydroxyalkanoates (PHA) | |

| Other Biodegradable Bioplastics |

| Rigid Packaging | Bottles and Jars |

| Trays and Containers | |

| Other Rigid Packaging | |

| Flexible Packaging | Films and Wraps |

| Pouches and Bags | |

| Other Flexible Packaging |

| Food |

| Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Other End - Use Industry |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Non-Biodegradable Bioplastics | Bio-PET | |

| Bio-PE | |||

| Other Non-Biodegradable Bioplastics | |||

| Biodegradable Bioplastics | Starch Blends | ||

| Polylactic Acid (PLA) | |||

| Poly(Butylene Adipate-co-Terephthalate) (PBAT) | |||

| Polybutylene Succinate (PBS) | |||

| Polyhydroxyalkanoates (PHA) | |||

| Other Biodegradable Bioplastics | |||

| By Product Type | Rigid Packaging | Bottles and Jars | |

| Trays and Containers | |||

| Other Rigid Packaging | |||

| Flexible Packaging | Films and Wraps | ||

| Pouches and Bags | |||

| Other Flexible Packaging | |||

| By End-Use Industry | Food | ||

| Beverages | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Other End - Use Industry | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the bioplastic packaging market?

The bioplastic packaging market reached USD 7.54 billion in 2026 and is set to climb to USD 18.89 billion by 2031.

Which region leads the bioplastic packaging market?

Europe leads with a 37.95% share in 2025, driven by stringent EU recycling and content mandates.

Which material type dominates the market today?

Bio-PET dominates with a 39.10% share thanks to compatibility with existing PET recycling infrastructure.

Why are flexible formats growing fastest?

Flexible packaging aligns well with PLA and Bio-PE material properties and supports quick-service and e-commerce applications, driving a 21.05% CAGR through 2031.

What is the biggest restraint to wider adoption?

Feedstock competition from biofuels limits bio-based polymer supply, subtracting 2.8 percentage points from the forecast CAGR.

Page last updated on: