Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

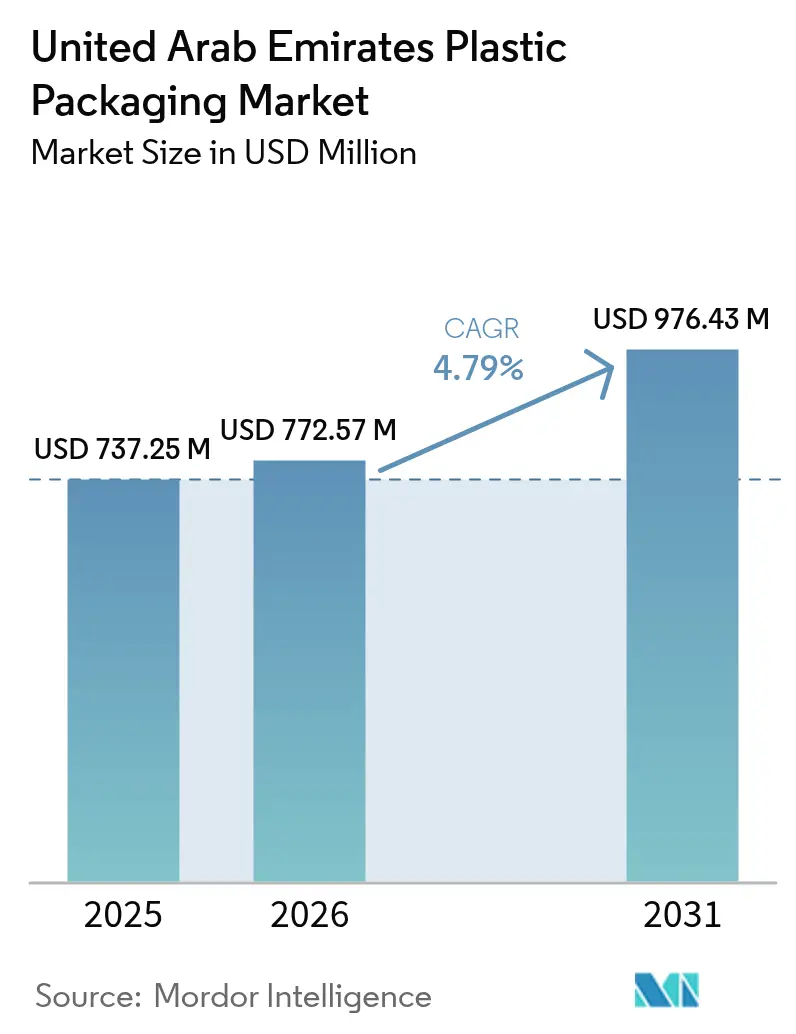

| Base Year Market Size (2025) | USD 737.25 Million |

| Market Size (2026) | USD 772.57 Million |

| Market Size (2031) | USD 976.43 Million |

| Growth Rate (2026 - 2031) | 4.79% CAGR |

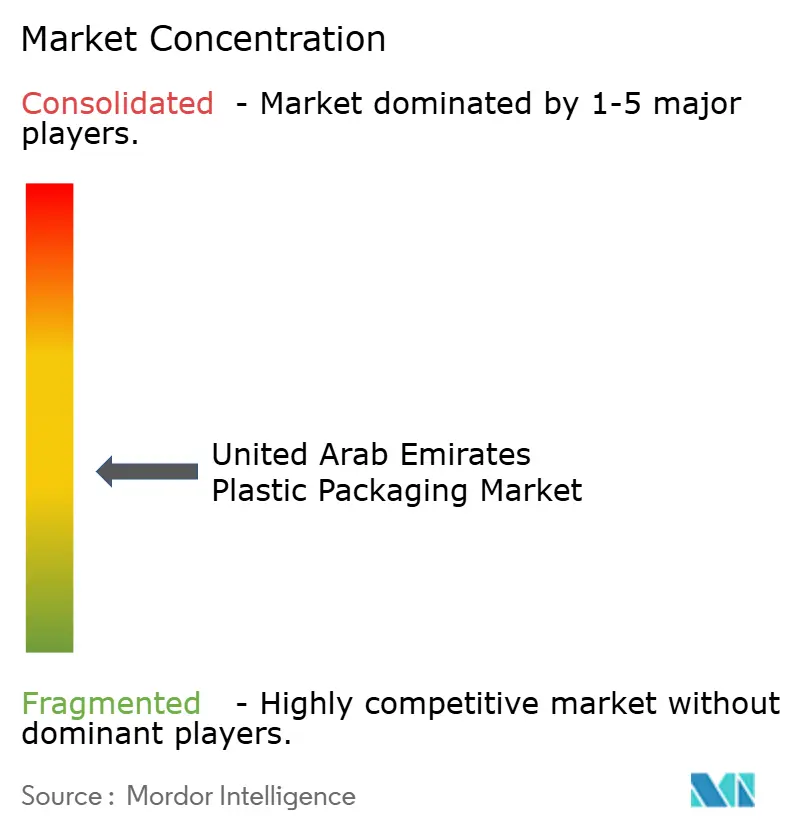

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Plastic Packaging Market Analysis by Mordor Intelligence

The United Arab Emirates plastic packaging market size was valued at USD 737.25 million in 2025 and estimated to grow from USD 772.57 million in 2026 to reach USD 976.43 million by 2031, at a CAGR of 4.79% during the forecast period (2026-2031). Robust demand from food, beverage, and e-commerce channels, coupled with regulatory incentives for sustainable materials, underpins this expansion. Rigid formats, anchored by polyethylene terephthalate (PET) bottles, account for the largest revenue stream; yet, converters are steadily diversifying toward flexible pouches, stand-up bags, and mono-material laminates that reduce weight and improve recyclability. The federal Operation 300bn industrial program, which targets AED 300 billion (USD 81.6 billion) in manufacturing value-added by 2031, is translating directly into new packaging opportunities for domestic food processors, pharmaceutical producers, and fast-moving consumer goods brands. Rising household incomes support premiumization, while the 2025 nationwide ban on single-use plastics is accelerating investments in recyclable and bio-based alternatives. Concurrently, the formation of Borouge Group International through the ADNOC-OMV-Nova Chemicals transaction delivers a captive resin supply, helping local converters mitigate price swings in imported feedstocks.

Key Report Takeaways

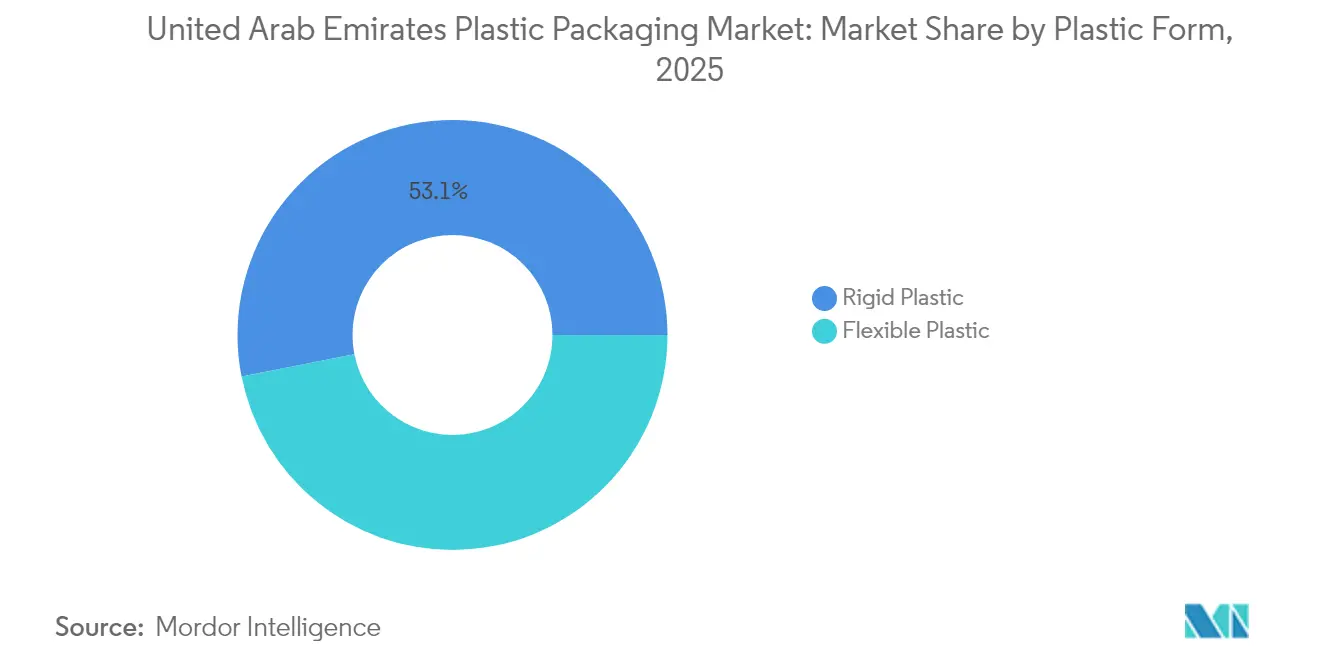

- By plastic form, rigid plastics led with 53.10% revenue share in 2025; flexible formats are projected to advance at a 7.37% CAGR through 2031.

- By product, bottles held 33.75% of the United Arab Emirates plastic packaging market share in 2025, while pouches are forecast to expand at 6.12% CAGR to 2031.

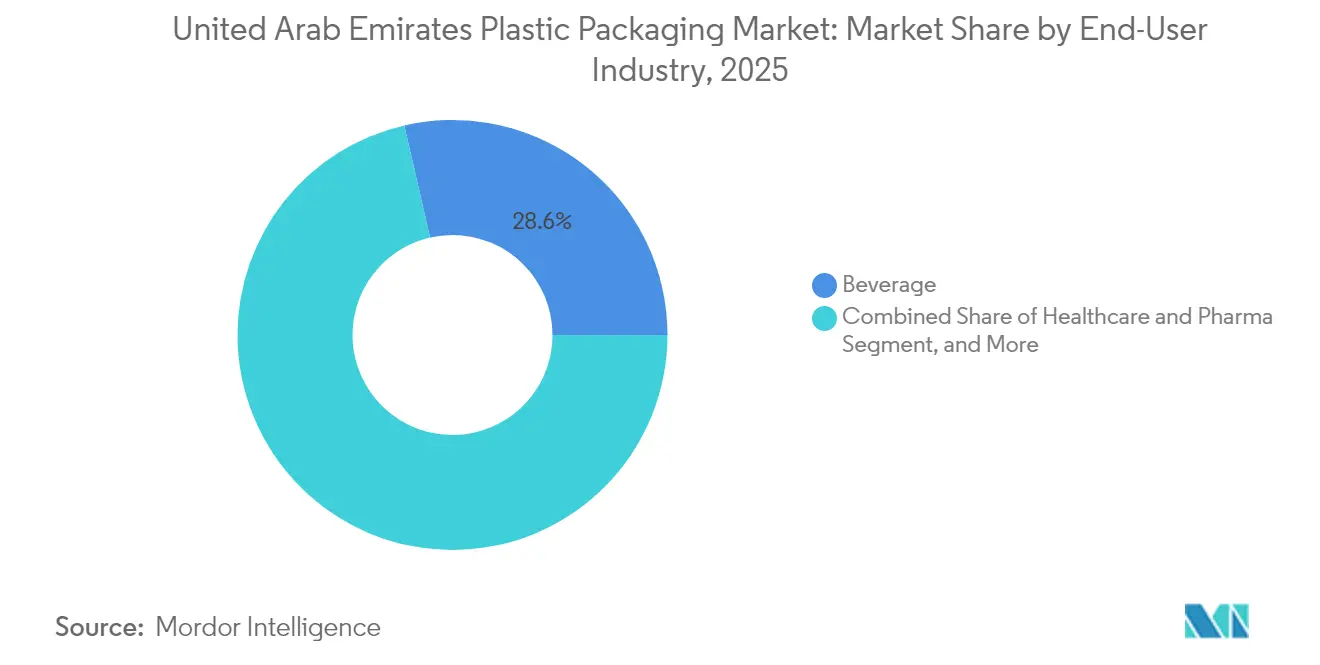

- By end-user, beverage applications captured a 28.60% share of the United Arab Emirates' plastic packaging market size in 2025, and healthcare packaging is expected to advance at a 6.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising per-capita income and premiumization | +1.2% | Nationwide, strongest in Dubai | Medium term (2-4 years) |

| Booming online grocery and delivery demand | +1.8% | Urban centers country-wide | Short term (≤ 2 years) |

| Operation 300bn F&B capacity expansion | +1.5% | National industrial zones | Long term (≥ 4 years) |

| Single-use plastic bans and mono-material push | +0.9% | All emirates, phased roll-out | Medium term (2-4 years) |

| Tadweer EPR pilot for design-for-recycling | +0.6% | Abu Dhabi and Dubai first | Long term (≥ 4 years) |

| Abu Dhabi PLA megaproject for bio-plastics | +0.8% | Nationwide with export potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Per-Capita Income and Premiumization

Higher disposable incomes channel consumers toward value-added packaging that signals freshness, convenience, and brand quality. Confectionery, snack, and dairy brands are shifting from plain films to stand-up pouches and resealable multi-layer wraps that lengthen shelf-life and support on-the-go consumption. Retailers are reporting double-digit growth in demand for portion-controlled packs, encouraging converters to invest in high-barrier co-extrusion lines that can maintain product integrity in the United Arab Emirates’s hot climate. Premiumization also lifts average selling prices, enabling producers to recoup investments in recyclable and bio-based substrates.

Booming Online Grocery and Food-Delivery Demand

A steep increase in online grocery orders after 2021 permanently raised expectations for robust, temperature-resistant packaging that protects contents over multiple hand-offs. Food-aggregator platforms now stipulate leak-proof pouches and insulated films that can endure heat spikes above 45 °C during last-mile transit. Converters are responding with two-layer PE films laminated to metalized BOPP for condensation control, while brand owners pilot RFID-tagged containers that enable package-level traceability during delivery runs. This digital commerce tailwind amplifies the addressable volume for flexible formats within the United Arab Emirates plastic packaging market.

Operation 300bn F&B Capacity Expansion

The federal AED 300 billion (USD 81.6 billion) push to raise industrial GDP is unlocking sizeable packaging off-take. Emirates Development Bank has earmarked AED 30 billion (USD 8.16 billion) in concessional loans for food-processing plants that require primary, secondary, and tertiary wraps. [1]UAE Government, “Waste-to-Energy,” u.aeFlagship builds, such as IFFCO’s AED 1 billion breakfast cereal plant in Dubai Industrial City, will increase demand for PET jars, multilayer films, and high-barrier trays as soon as commercial production begins in 2026. As more processors reshore production to comply with food-security directives, localized sourcing of packaging inputs gains priority, boosting opportunities for small and mid-sized converters.

Single-Use Plastic Bans and Mono-Material Packs

Sweeping prohibitions on single-use carrier bags, foamware, and cutlery, enforced from January 2025 with fines up to AED 50,000 (USD 13,600), accelerate the shift toward mono-material PE, PP, or PET laminates that can enter existing recycling streams. Dubai’s earlier phase-out of polystyrene has already prompted fast-food chains to shift toward polypropylene clamshells and PET salad bowls. Incentives such as tax rebates on recycled-content packs and grants for lightweight designs are helping to soften the cost gap vis-à-vis virgin resin. Brand-owner compliance with the United Arab Emirates climate law’s Scope 3 reporting clauses further reinforces demand for low-carbon packaging solutions. [2]The ESG Institute, “The UAE Climate Law Is Here,” the-esg-institute.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resin price volatility for imported feedstock | -1.1% | Nationwide | Short term (≤ 2 years) |

| Limited recycling capacity for flexible films | -0.8% | Most acute in Northern Emirates | Medium term (2-4 years) |

| EU carbon border levy on plastic-rich exports | -0.4% | Export-oriented converters | Long term (≥ 4 years) |

| Gate-fee surcharges from under-performing MRFs | -0.6% | Waste-management zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Resin Price Volatility for Imported Feedstock

Converters import polyolefins and PET valued at USD 6.4 billion in 2023, leaving procurement budgets exposed to sharp cost swings amid geopolitical disruptions. Smaller firms lacking hedging lines face margin compression when contract prices reset quarterly, and brand owners increasingly demand price-lock agreements. While Borouge’s newly integrated supply chain is expected to cushion local price spikes for certain grades, dependency on overseas PET and specialty additives still limits predictability.

Limited Recycling Capacity for Flexible Films

Nationwide, material-recovery facilities currently achieve only a 4% diversion of plastic waste, with flexible laminates being the most underserved fraction. AI-enabled optical sorters reach 91% accuracy on rigid bottles but struggle with films thinner than 50 microns, forcing brand owners to pay higher gate fees for energy-from-waste disposal. Planned 100 MW waste-to-energy plants in Abu Dhabi and Dubai will treat hard-to-recycle residues, but cannot close the loop for value-chain circularity. The infrastructure deficit restrains momentum toward fully circular flexible packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Plastic Form: Flexible Formats Spark Rapid Uptake

Flexible materials are on a fast track, expanding at 7.37% CAGR through 2031 as e-commerce and food delivery services specify lighter, space-efficient packs. In contrast, the rigid stream still contributes the largest 2025 revenue slice at 53.10%, sustained by PET water bottles and high-density polyethylene (HDPE) dairy jugs. Lightweight pouches help brand owners lower logistics emissions because each kilogram of product uses as little as 30 grams of film, while an equivalent volume in glass would weigh 1.5 kilograms. Regulatory incentives that reward mono-material PE-PE or PP-PP laminates over aluminum-lined sachets further tip the scales toward flexible constructions.

Converters are also trialing bio-sourced polylactic acid (PLA) films ahead of Emirates Biotech’s mega-plant start-up in 2028, anticipating cost declines once domestic supply scales. As a result, compostable salad bags and coffee capsules are entering retail shelves, offering tangible proof points of the United Arab Emirates plastic packaging market commitment to circularity. Rigid PET remains indispensable for carbonated soft drinks, yet producers increasingly incorporate up to 25% recycled PET flake to satisfy eco-label criteria and meet municipal mandates.

By Product Types : Bottles Retain Dominance as Bags and Pouches Surge

Bottles accounted for 33.75% revenue in 2025, propelled by the Gulf’s distinctive preference for packaged drinking water amid desert temperatures. Dairy processors similarly standardize on multilayer white PET for light-barrier protection. Nonetheless, bags and Pouches are the fastest-rising SKU, growing at 6.12% CAGR to 2031. Coffee, baby food, and condiments now leverage pouch formats that deliver convenience and a lower overall package-to-product ratio. While caps, closures, and lids form a niche, they enjoy recurring order volumes because dispensing innovations drive brand differentiation in the personal care sector.

Trays and clamshells serve the chilled ready-meal aisle, which grew swiftly during the pandemic-era remote working period, but environmental scrutiny is prompting a pivot from polystyrene to polypropylene. Converter R&D pipelines list microwave-safe PP-paper hybrids that combine heat-resistance with improved recyclability. Overall, diversification spreads risk for suppliers who traditionally over-indexed on hollow containers within the United Arab Emirates plastic packaging market.

By End-User Industry: Healthcare Registers the Fastest CAGR

Beverage applications led the pack with a 28.60% share of the United Arab Emirates' plastic packaging market in 2025, reflecting the country’s high reliance on packaged drinking water and its expanding dairy and juice portfolios. Bottled-water fillers favor lightweight polyethylene terephthalate (PET) containers that strike a balance between strength and reduced resin use, while dairy processors increasingly specify multilayer white PET to block ultraviolet light and extend shelf life in climates that routinely exceed 45 °C. Demand also benefits from nationwide hospitality and travel flows, which lift single-serve formats across carbonated soft drinks, iced tea, and functional beverages. Brand owners are steadily increasing recycled-content percentages to meet single-use regulations, and tethered closures are being adopted ahead of export market mandates. Collectively, these moves keep bottle preform and cap lines running at high utilization rates, thereby anchoring converter revenues within the United Arab Emirates' plastic packaging market.

Healthcare and pharmaceutical packaging is the fastest-growing end-user vertical, with the segment’s United Arab Emirates plastic packaging market size projected to expand at a 6.89% CAGR from 2026 to 2031. The new federal medical-products law streamlines approvals and encourages multinational drug makers to base fill-finish operations in Abu Dhabi’s Khalifa Economic Zones, driving sustained orders for sterile blister packs, vials and unit-dose sachets. Polypropylene and cyclic-olefin copolymer containers dominate parenteral drugs because they resist breakage and chemical migration, while high-barrier multilayer films protect humidity-sensitive tablets. Suppliers offering ISO-certified clean-room molding, gamma-sterilization compatibility and traceable raw materials gain preferred-vendor status as pharma customers tighten compliance audits. With biologics pipelines growing and regional vaccine production on the rise, converters that can deliver precision molding and tamper-evident closures are well positioned to capture incremental volume in the years ahead.

Geography Analysis

The United Arab Emirates plastic packaging market, though national in scope, exhibits remarkable emirate-level variation. Dubai and Abu Dhabi together account for close to 69% of total demand owing to their interplay of consumer density, advanced logistics and large-scale manufacturing clusters. Dubai’s Jebel Ali port and free zone act as a re-export springboard into Africa and the Levant, inflating throughput for corrugated outers and stretch films that safeguard transit cargo. Abu Dhabi’s AED 2.72 billion (USD 2.72 billion) manufacturing-expansion roadmap targets doubling the emirate’s industrial GDP by 2031, creating consistent offtake for pharmaceutical vials, PET preforms, and injection-molded closures.In Sharjah, Ajman, and Ras Al Khaimah, rising population and SME food-processing clusters fuel incremental demand, albeit from a smaller base. These northern emirates also house value-priced flexo-printing facilities that attract orders for snack-food wraps seeking cost efficiency. Free-zone incentives allow 100% foreign ownership, prompting multinational converters to locate region-servicing hubs within the United Arab Emirates plastic packaging market. However, the decentralized approach to single-use plastic enforcement, with Dubai leading, and Fujairah yet to formalize bans, necessitates agile compliance strategies from suppliers.

Geographic proximity to Asian resin giants ensures short sea-freight transit but also exposes the domestic market to external currency swings that influence resin import costs. Meanwhile, federal climate-law mandates apply to all emirates, obliging factories to collect Scope 1 and Scope 2 emissions data-sets from May 2025 onward. Waste-management infrastructure remains uneven; Dubai’s integrated strategy commits AED 74.5 billion (USD 20.26 billion) across waste-segregation, mechanical recycling and energy-from-waste assets, whereas Umm Al Quwain relies on landfill until a regional processing hub comes online

Competitive Landscape

The United Arab Emirates plastic packaging market is characterized by moderate fragmentation. Hotpack Packaging Industries headlines at 15.2%, leveraging 10 domestic plants and a growing export pipeline to 100 countries. Its USD 100 million New Jersey factory, inaugurated in May 2025, underscores a strategic pivot toward dollar-denominated revenues that hedge foreign-exchange exposure. Falcon Pack follows at 11.8%, focusing on disposables that comply with Dubai’s single-use ban through the early adoption of mono-material polypropylene.

Vertical integration is a clear theme: Borouge’s polymer-to-preform model shortens lead times for beverage bottlers, while Alpla’s January 2025 share consolidation in Taba secures blown-mold capacity across three emirates. Technology partnerships reinforce competitive edges. Borouge and Bericap co-develop tethered caps that meet the requirements of EU Directive 2019/904 for export markets, whereas AptarGroup supplies silicon-valve dispensing closures that target premium condiments produced in Jebel Ali.

Sustainability credentials now influence tender awards. Converters offering traceable 30% rPET content obtain preferred-supplier status with retailers that publicly report packaging footprints. Firms lagging on emissions disclosure face higher financing costs under green-bond covenants issued by regional banks. Collectively, these dynamics shape an ecosystem where scale and circularity competence determine long-term viability inside the United Arab Emirates plastic packaging market.

United Arab Emirates Plastic Packaging Industry Leaders

Amber Packaging Industries LLC

Huhtamaki Flexibles UAE

Mondi plc

Integrated Plastics Packaging LLC

Al Amana Plastic Bottles & Containers Manufacturing LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Borouge announced USD 100 million in new supply agreements with Bericap, Taghleef Industries and Alpla to co-engineer recycled-content solutions for beverages and flexible films.

- January 2025: Alpla acquired remaining shares in Taba, unifying its Middle East blow-molding platform.

- January 2025: Songwon and Altek formed a partnership to grow PVC stabilizer offerings targeting regional packaging converters.

- December 2024: Emirates Biotech selected Sulzer technology for a PLA complex that will enter construction in 2025 and begin production by early 2028.

United Arab Emirates Plastic Packaging Market Report Scope

The market for the study is defined as the revenue incurred from the sales of plastic packaging products in the United Arab Emirates. The market tracks the consumption trends of plastic packaging products in terms of value and volume. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the glass packaging market in terms of drivers and restraints.

The UAE plastic packaging market is segmented by plastic form (rigid plastic and flexible plastic), products (bottles, cans, jars, pouches), and end-user industry (food, beverage, healthcare, retail, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Plastic Form

| Rigid Plastic | PET Bottles |

| HDPE/PP Containers | |

| Flexible Plastic | PE Films and Wraps |

| Stand-up Pouches | |

| Sachets and Stick Packs |

By Product Types

| Bottles |

| Jars and Containers |

| Bags and Pouches |

| Trays and Clamshells |

| Other Product Types |

By End-user Industry

| Food | Fresh Produce |

| Meat and Seafood | |

| Confectionery and Snacks | |

| Other Food Types | |

| Beverage | Bottled Water |

| Dairy and Juices | |

| Other Beverages Types | |

| Healthcare and Pharma | |

| Personal Care and Cosmetics | |

| Retail and E-commerce | |

| Other End-user Industries |

| By Plastic Form | Rigid Plastic | PET Bottles |

| HDPE/PP Containers | ||

| Flexible Plastic | PE Films and Wraps | |

| Stand-up Pouches | ||

| Sachets and Stick Packs | ||

| By Product Types | Bottles | |

| Jars and Containers | ||

| Bags and Pouches | ||

| Trays and Clamshells | ||

| Other Product Types | ||

| By End-user Industry | Food | Fresh Produce |

| Meat and Seafood | ||

| Confectionery and Snacks | ||

| Other Food Types | ||

| Beverage | Bottled Water | |

| Dairy and Juices | ||

| Other Beverages Types | ||

| Healthcare and Pharma | ||

| Personal Care and Cosmetics | ||

| Retail and E-commerce | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the current value of the United Arab Emirates plastic packaging market?

The market size is USD 772.57 million in 2026.

How fast is demand for flexible plastic formats growing?

Flexible formats are forecast to post a 7.37% CAGR through 2031.

Which end-user sector presents the fastest growth opportunity?

Healthcare and pharmaceutical applications show the highest momentum at 6.89% CAGR through 2031.

How will the single-use plastic ban affect converters?

Effective 2025, fines up to AED 50,000 push suppliers to pivot toward mono-material and recyclable designs, spurring rapid material innovation.

What role does Borouge Group International play in the market?

Borouge integrates upstream resin and downstream preform capacity, giving local converters steadier polymer pricing and supply security.

Why is the PLA facility in Abu Dhabi significant?

With production slated for 2028, the world-scale plant will create domestic sources of compostable PLA, reducing import dependence and enabling bio-based packaging growth.

Page last updated on: