Pet Sitting Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

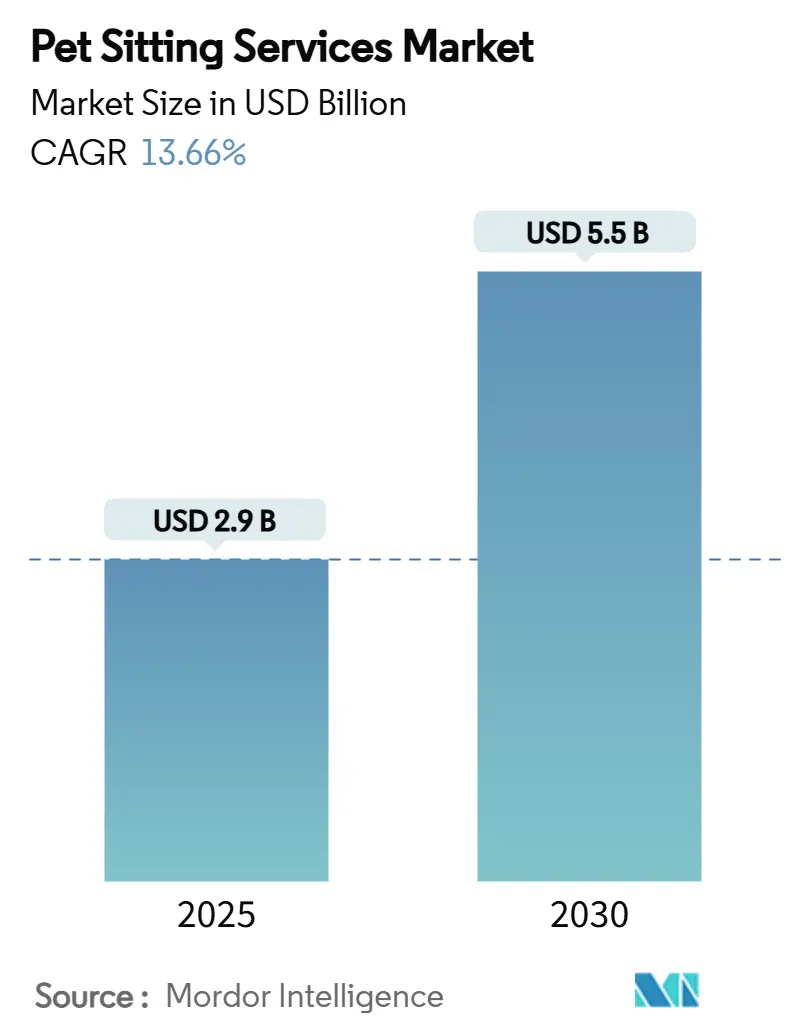

| Market Size (2025) | USD 2.9 Billion |

| Market Size (2030) | USD 5.5 Billion |

| Growth Rate (2025 - 2030) | 13.66% CAGR |

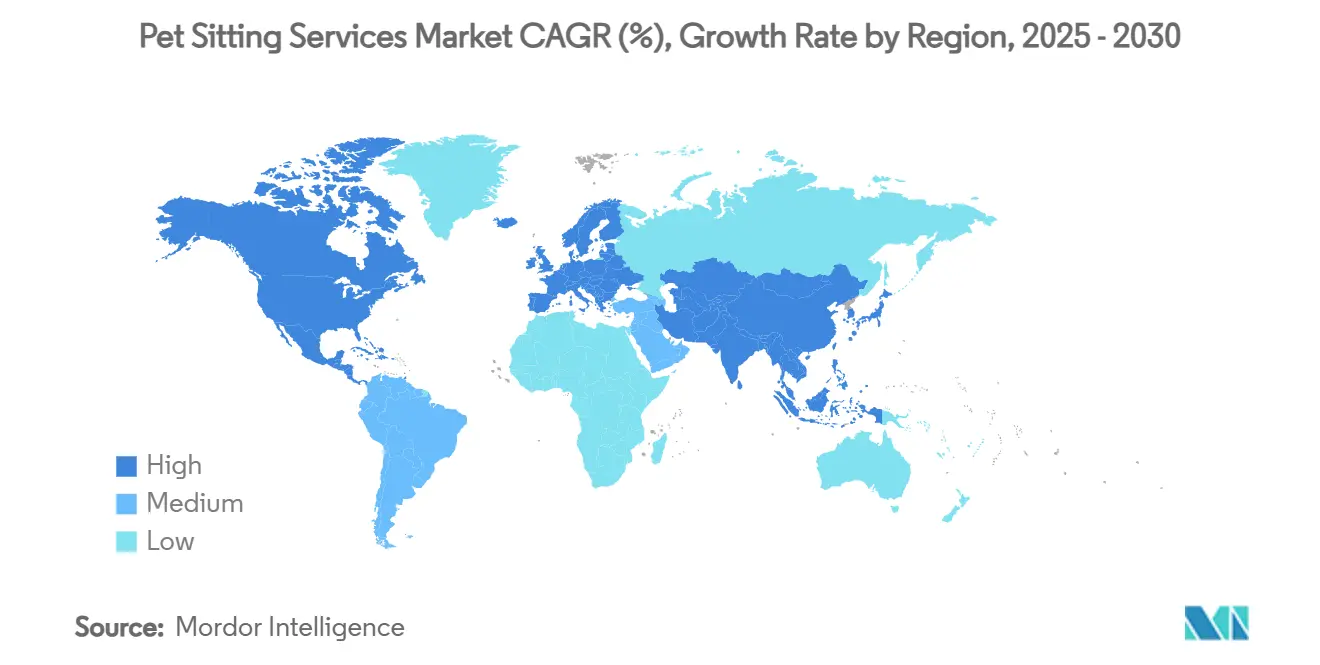

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Sitting Services Market Analysis by Mordor Intelligence

The pet sitting services market size is valued at USD 2.9 billion in 2025 and is forecast to expand to USD 5.5 billion by 2030, translating into a 13.66% CAGR over the period. The upward trajectory rests on three pillars: sustained growth in pet ownership, strong adoption of premium care models that mirror childcare standards, and the ease with which digital platforms match supply to near-real-time demand. Millennials and Gen Z pet parents increasingly outsource routine care while they commute or travel, anchoring weekday demand and lifting average order values. Employer-subsidized pet-care benefits, now used as a talent-retention tool, further widen the buyer pool. A tightening of U.S. independent-contractor rules and intensifying local price competition represent the two main structural challenges. Yet, neither is expected to offset the long-term structural tailwinds that expand the overall revenue base of the pet sitting services market.

Key Report Takeaways

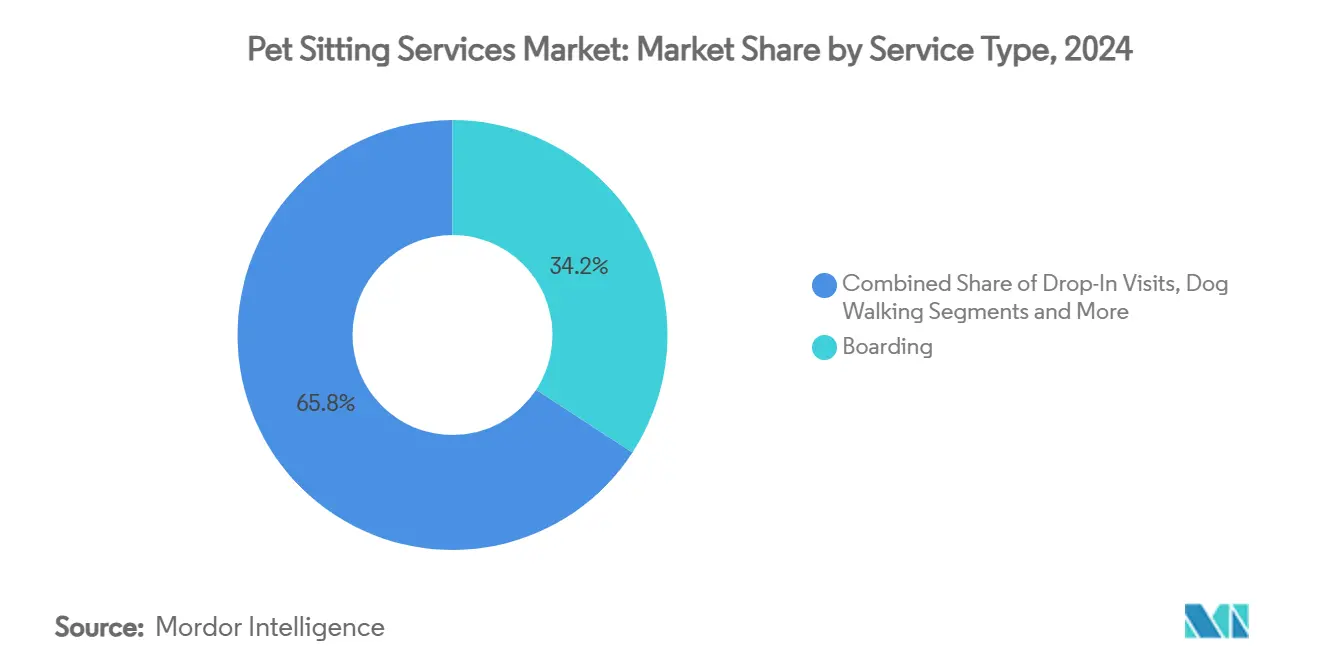

- By service type, boarding led with 34.2% of the pet sitting services market share in 2024, while daycare and drop-in visits recorded the fastest 11.3% CAGR through 2030.

- By pet type, dogs accounted for 62.8% share of the pet sitting services market size in 2024; exotic pets and small mammals post the highest 8.8% CAGR for the same horizon.

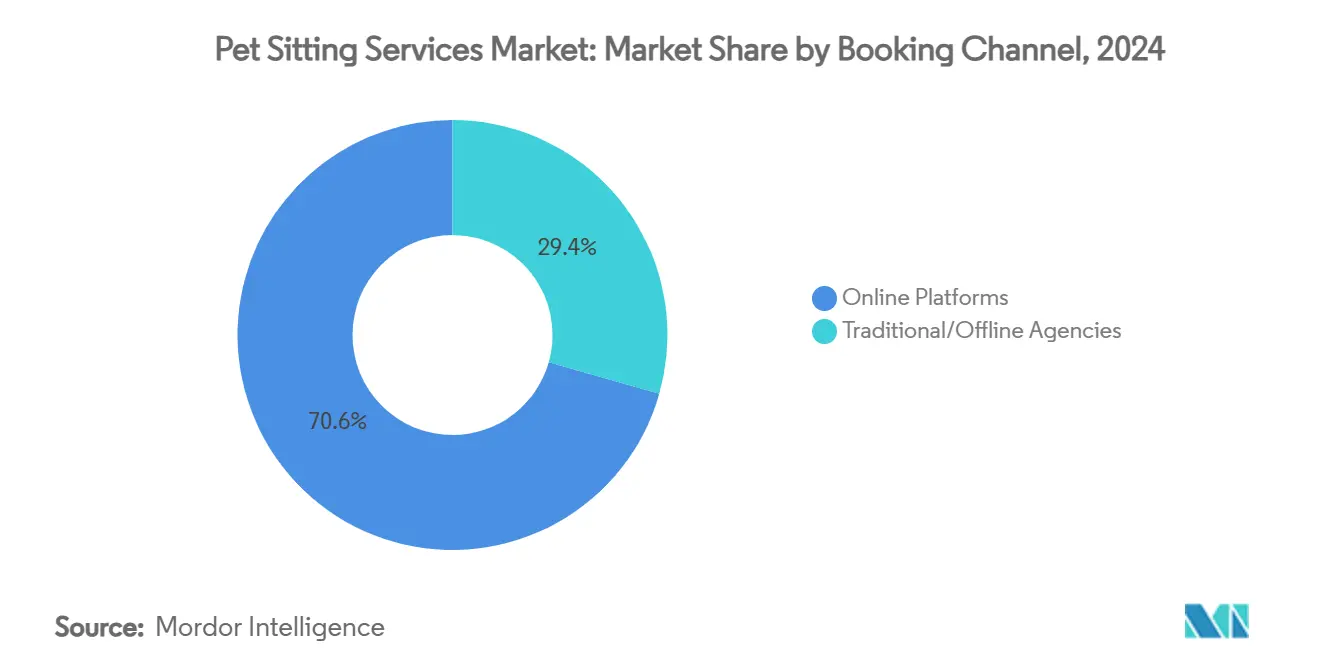

- By booking channel, online platforms and apps captured 70.6% of the pet sitting services market share in 2024 and are growing at a 12.5% CAGR due to rising smartphone penetration and trust features such as GPS tracking and verified reviews.

- By region, North America accounted for 35.5% of the pet sitting services market share in 2024, whereas Asia Pacific is projected to expand at a 9.6% CAGR through 2030.

Global Pet Sitting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Pet Ownership Rates | +3.40% | Global, with strongest impact in North America & APAC | Long term (≥ 4 years) |

| Increasing Humanization Of Pets And Spending On Premium Services | +4.10% | Global, led by developed markets | Medium term (2-4 years) |

| Growth Of Gig-Economy & On-Demand Pet-Sitting Apps | +2.70% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Return-To-Office Trends Post-Pandemic Boosting Day-Time Care Demand | +2.00% | North America & EU primarily | Short term (≤ 2 years) |

| Employer-Funded Pet-Care Benefit Programs | +1.40% | North America, early adoption in EU | Medium term (2-4 years) |

| Growth In Cross-Border Pet Travel Fueling International Sitters | +1.10% | Global, concentrated in high-mobility regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Pet Ownership Rates

Surging ownership underpins long-term demand. U.S. households, for instance, added over 3 million pets between 2020 and 2024, and 65% of owners cite access to professional carers as essential when work schedules tighten, according to SHRM.[1]Society for Human Resource Management, “2024 Employee Benefits Survey,” shrm.org Parallel growth is visible in China, where an urban pet population of 120 million in 2024 has fed a national pet economy now exceeding CNY 300 billion (USD 41.8 billion). As first-time owners lean on professional sitters to compensate for a lack of informal care networks, the pet sitting services market benefits from recurring, high-frequency bookings rather than occasional peaks. Expansion is further entrenched by urban dwelling patterns that favour service outsourcing over informal neighbourly help.

Increasing Humanization of Pets and Spending on Premium Services

Consumer mindset now places animal well-being close to that of children. Rover’s 2024 “True Cost of Pet Parenthood” survey puts a dog’s annual essentials spend at USD 3,120, up 14% year-on-year, with specialized services—overnight sitting, behavioral coaching, wellness monitoring—moving from optional to mainstream. Owners in Asia echo the premium trend; 60% report willingness to pay extra for advanced care, a stance that is steering the pet sitting services market toward bundled offerings that include real-time video updates and in-home enrichment activities. As discretionary spend rises, operators able to demonstrate professional credentials and robust safety protocols secure higher margins.

Growth of Gig-Economy & On-Demand Pet-Sitting Apps

Marketplace platforms lower search and trust friction. They now facilitate 70.6% of all bookings, helped by transparent pricing, user ratings, and embedded insurance. Wag! Group lifted 2023 revenue 52.9% to USD 83.9 million after enhancing subscription tiers that bundle wellness add-ons. Nonetheless, the U.S. Department of Labor’s March 2024 six-factor test could force reclassification of many sitters as employees, potentially adding social-security and overtime costs of 20–30% per booking.[2]United States Department of Labor, “Employee or Independent Contractor Classification Under the Fair Labor Standards Act,” dol.gov Operators with diversified revenue streams and scalable technology are best positioned to absorb the shift without heavy price inflation.

Return-to-Office Trends Post-Pandemic

Hybrid work revives weekday demand peaks. Two-thirds of owners worry about separation anxiety as offices reopen, translating into higher utilization of midday walks and extended daycare. Providers respond with flexible check-in windows and multi-pet discounts to balance the weekday load. Corporate clients also expand subsidy schemes, and 44% of employees consider switching employers if policies are not pet-friendly, creating a new institutional demand funnel. The immediate effect is a lift in average weekly booking frequency, accelerating revenue conversion for the pet sitting services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly fragmented provider landscape | −2.5% | Global; most intense in mature markets | Short term (≤ 2 years) |

| Safety & liability concerns | −1.6% | North America & EU | Medium term (2–4 years) |

| Gig-worker reclassification risks | −1.1% | North America; expanding to EU | Short term (≤ 2 years) |

| Growing remote-work adoption | −0.8% | Global; concentrated in developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Highly Fragmented Provider Landscape Driving Price Competition

Privately owned businesses account for 75% of industry revenue, and 99% of firms employ fewer than five people, fostering a race-to-the-bottom on pricing, as per the Pet Sitters International.[3]Pet Sitters International, “Member Business Survey 2024,” petsit.comThe average PSI-member gross of USD 100,537 in 2023 underscores small-scale operations that lack the leverage to set premium rates. While private-equity-led consolidation—Blackstone’s USD 2.3 billion Rover acquisition—signals appetite for scale, the inherently local nature of service keeps entry barriers low. Margin erosion slows investment in training, technology, and insurance, dampening quality differentials that could otherwise support higher average selling prices.

Safety & Liability Concerns Among Pet Owners

Care errors carry high reputational and financial costs. Standard homeowners or renters insurance seldom covers third-party pet incidents, obliging sitters to purchase specialized coverage that can exceed USD 1,000 annually. Rising veterinary fees elevate potential claim sizes, amplifying owner anxiety. Sitters, therefore, adopt bonding schemes, GPS tracking, and live-stream cameras to reassure clients’ investments that raise operating expenses. Trust barriers remain most acute in novel service categories such as exotic-pet care and overnight in-home stays, moderating near-term uptake and trimming two points off the otherwise robust CAGR for the pet sitting services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Boarding Holds the Lead While Daycare Accelerates

Boarding generated 34.2% of 2024 revenue, making it the cornerstone of the pet sitting services market. The segment appeals to owners seeking an all-inclusive solution during extended travel, offering structured play, round-the-clock supervision, and often medical oversight. Revenue resilience comes from longer average booking durations and supplemental upsells such as grooming or enrichment sessions. Yet boarding’s growth pace now trails daycare, reflecting shifting work practices that demand flexible, hour-based options rather than week-long stays.

Daycare and drop-in services post an 11.3% CAGR through 2030, riding the hybrid work wave that reconfigures weekday routines. Large franchise networks illustrate scalability: Camp Bow Wow reported USD 198 million revenue in 2022 before its 2024 sale to Propelled Brands, evidencing strong investor confidence in structured daycare formats. Mid-day attendance spikes also reduce kennel occupancy risk, making capacity utilization more predictable. Operators that offer bundled subscription passes capture repeat business and lift customer lifetime value, reinforcing the growth premium in this slice of the pet sitting services market.

By Pet Type: Dogs Dominate While Exotics Gain Traction

Dogs commanded a 62.8% revenue share in 2024, a testament to high ownership prevalence and the canine need for regular exercise and socialization, which in turn creates frequent purchase cycles. Their adaptability to group settings simplifies service delivery and underpins cost-efficient capacity planning for providers. Routine services such as walks, playgroups, and overnight boarding form the revenue bedrock and ensure the pet sitting services market retains a dog-centric operational model.

Exotic pets and small mammals log the fastest 8.8% CAGR to 2030. Rising urban interest in unique companions such as birds, reptiles, and hedgehogs fuels demand for carers with specialized know-how. Barriers to entry are higher: temperature-controlled habitats, species-specific diets, and often bespoke insurance. Providers are able to furnish certification and targeted liability coverage and command premium rates, boosting per-visit margins even if absolute volumes remain smaller. Cat services occupy a middle ground; Pet Sitters International notes that 96% of its members care for felines, signaling a large capacity yet lower visit frequency than with dogs. The overall effect is a diversifying portfolio that broadens the revenue foundation of the pet sitting services industry without diluting core dog-centric economics.

By Booking Channel: Digital Marketplaces Reshape Access

Online channels secured 70.6% of the 2024 transaction value and are growing at a 12.5% CAGR. Marketplace platforms deploy algorithms that match owners' needs with carer availability in minutes, embed real-time GPS tracking, and offer on-platform insurance. Such reassurance collapses search cost and speeds first-time adoption, giving the pet sitting services market its most powerful growth catalyst since 2018. Significant data insights also enable dynamic pricing of weekday midday slots, for example, which are discounted to smooth demand while holiday periods command surge rates that lift network-wide yield.

Offline agencies still serve high-net-worth owners who prefer curated, long-term relationships, especially for pets requiring medical supervision. These agencies maintain tenured staff capable of administering medication or post-surgery care and thus extract premium fees. The coexistence of both channels suggests a segmented equilibrium rather than outright digital displacement; however, funding flows and customer acquisition trends heavily favor tech-driven models likely to account for an even larger slice of the pet sitting services market by decade-end.

Geography Analysis

North America retained its position as the largest regional contributor with 35.5% of 2024 revenue, supported by high pet penetration, disposable income, and cultural acceptance of paid pet care. Pet Sitters International alone generated USD 440 million from more than 22 million assignments in 2024, and average revenue per member rose 25% versus 2020, as per Pet Sitters International. Crucially, regulatory clarity around bonding, insurance, and animal welfare has fostered professional standards that build consumer trust, enabling high repeat-booking rates.

Europe presents the next sizable opportunity. Over 91 million households keep pets, feeding a pet-care economy already exceeding USD 40 billion and expected to grow 6% annually through 2027. Germany leads pet imports at 18% of intra-EU trade, followed by the UK and France, reflecting mature demand patterns and recognizing pet sitting as an essential rather than discretionary spend. Tightened GDPR privacy requirements, however, increase compliance costs for app-based platforms, slightly moderating the margin outlook versus North America.

Asia Pacific is the fastest climber with a projected 9.6% CAGR to 2030 for the pet sitting services market. China alone is set to reach CNY 756.5 billion (USD 104 billion) in overall pet-sector spend by 2030, growing 12.9% annually. Urbanization and smaller household sizes spur demand for external care services, while digital payment ubiquity accelerates platform uptake. South Korea and India echo the trend: both saw double-digit gains in pet ownership among 18- to 34-year-olds in 2024, suggesting a long runway for premium, technology-enabled models. Obstacles remain fragmented by provincial regulations and lower per-visit spend, but rising middle-class incomes and rapid smartphone diffusion offset the headwinds.

Competitive Landscape

The pet sitting services market remains highly fragmented, with privately held firms controlling 75% of revenue and the top five players capturing less than 15% combined. This structure keeps local entry barriers minimal, encouraging thousands of micro-entrepreneurs yet complicating standardization efforts. Technology integration is the primary lever for scale; Rover’s network now spans 600,000 sitters and generated USD 230 million in 2024 revenue before its USD 2.3 billion sale to Blackstone, signaling institutional optimism about asset-light marketplace economics.

Regulation increasingly shapes competitive moats. The U.S. Department of Labor’s updated worker-classification test may raise labour costs by double digits for platforms that cannot redesign engagement models fast enough. Players with robust balance sheets and subscription-based revenue will navigate the transition better, potentially triggering a wave of consolidation that lifts the pet sitting services market concentration over time. Alongside the larger mergers, niche startups target white spaces—international pet travel, exotic-animal care, and AI-driven wellness monitoring—seeking differentiation in an otherwise homogenized service mix.

Service innovation also defines competitive advantages. Wag! Group augmented its marketplace with a wellness membership tier that bundles 24/7 tele-vet access, insurance, and discounts on prescription refills, deepening customer lock-in and boosting cross-sell opportunities. Traditional in-home agencies counter by emphasizing certified training, one-to-one continuity of carer, and specialized care for ageing or medically fragile pets. As macro demand stays buoyant, the principal battleground is not volume but share of wallet; firms that convert single-service bookings into multi-service relationships secure a disproportionate slice of the pet sitting services market growth.

Pet Sitting Services Industry Leaders

Rover Group, Inc.

Wag! Group Co.

Fetch! Pet Care, Inc.

PetBacker

Holidog

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Rover expanded its European footprint by acquiring “Cat in a Flat,” a specialist cat-sitting marketplace.

- March 2025: Wag! Group posted USD 83.9 million in 2023 revenue, a 52.9% jump over 2022, driven by wellness subscriptions and ancillary service expansion.

- February 2025: Propelled Brands acquired Camp Bow Wow, a daycare franchise with 200+ locations and USD 198 million in 2022 revenue.

- February 2025: Rover completed a USD 2.3 billion acquisition by Blackstone, marking one of the largest private-equity transactions in pet services history.

Global Pet Sitting Services Market Report Scope

| In-Home Sitting |

| Boarding / Kennel Services |

| Drop-In Visits |

| Dog Walking |

| Daycare |

| Dogs |

| Cats |

| Birds |

| Small Mammals |

| Reptiles & Exotics |

| Online Platforms & Apps |

| Traditional/Offline Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | In-Home Sitting | |

| Boarding / Kennel Services | ||

| Drop-In Visits | ||

| Dog Walking | ||

| Daycare | ||

| By Pet Type | Dogs | |

| Cats | ||

| Birds | ||

| Small Mammals | ||

| Reptiles & Exotics | ||

| By Booking Channel | Online Platforms & Apps | |

| Traditional/Offline Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the pet sitting services market expected to grow?

Between 2025 and 2030 the market is projected to advance at a 13.66% CAGR, taking revenue from USD 2.9 billion to USD 5.5 billion.

Which service segment is expanding the quickest?

Daycare and drop-in visits post an 11.3% CAGR through 2030 as hybrid work schedules create weekday demand spikes.

What role do digital platforms play?

Online marketplaces already handle 70.6% of bookings and grow at 12.5% annually, thanks to instant matching, embedded insurance, and consumer trust features.

Are regulatory changes a material risk?

Yes. The U.S. Department of Labor’s new independent-contractor test could raise labour costs by 20–30%, challenging gig-dependent platforms.

Which regions offer the strongest upside?

Asia Pacific is forecast to grow 9.6% a year on urbanisation and rising disposable income, while Europe adds steady 6% annual growth from a large pet-owning base.

How fragmented is the industry?

Privately owned firms control 75% of revenue, and the top five players hold less than 15% combined, indicating a highly fragmented landscape with ample consolidation potential.

Page last updated on: