Pet Funeral Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

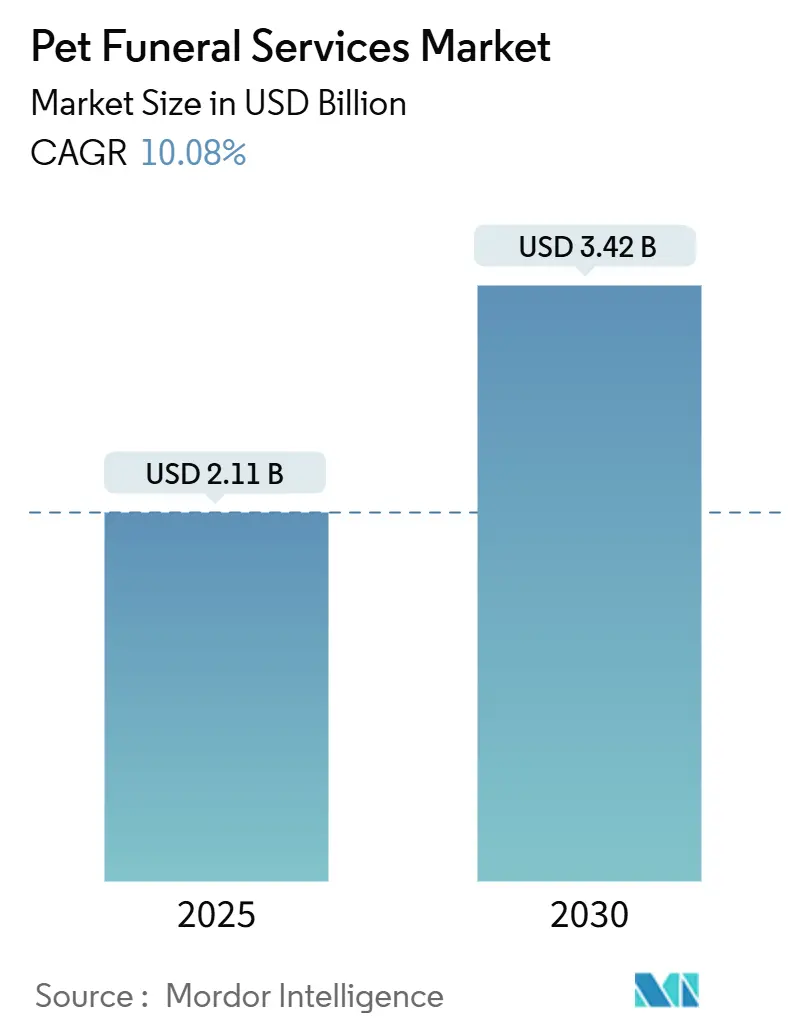

| Market Size (2025) | USD 2.11 Billion |

| Market Size (2030) | USD 3.42 Billion |

| Growth Rate (2025 - 2030) | 10.08% CAGR |

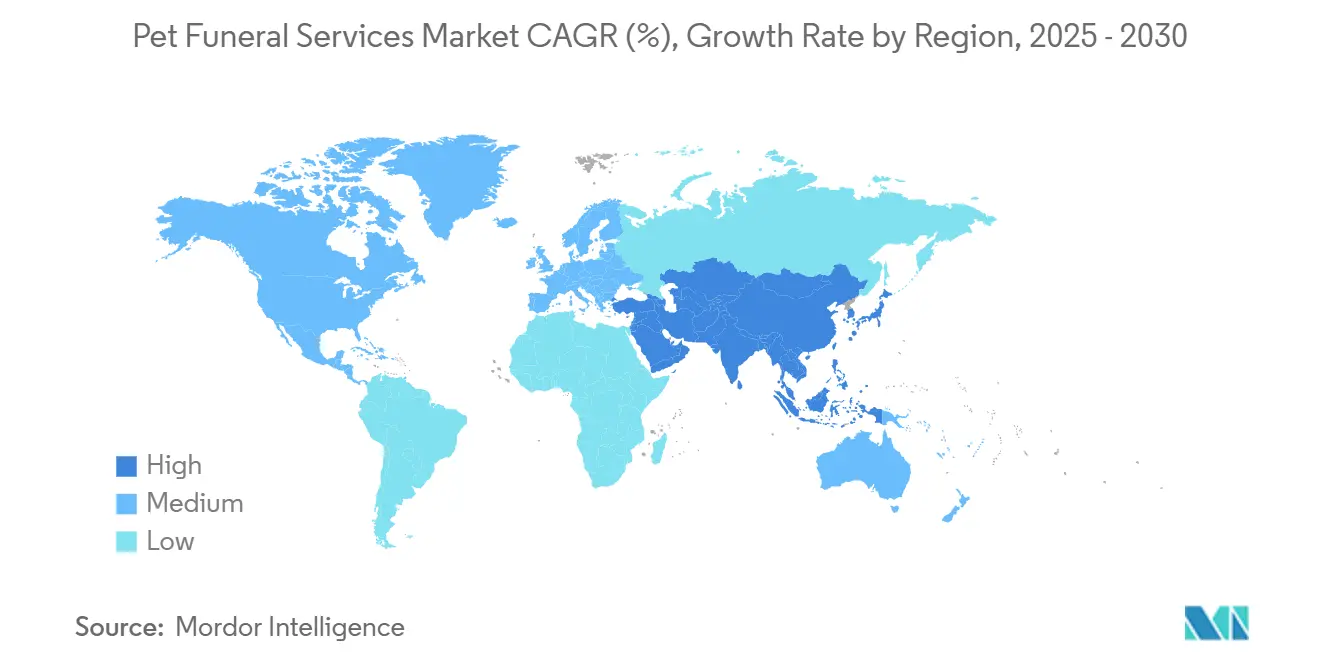

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Funeral Services Market Analysis by Mordor Intelligence

The pet funeral services market size stood at USD 2.11 billion in 2025 and is forecast to reach USD 3.42 billion by 2030, expanding at a 10.08% CAGR during the period. Demand for dignified end-of-life care is no longer discretionary because 97% of owners globally regard pets as family members, a mindset that fuels sustained spending even in slower economies.[1]Cremation Association of North America, “Pet Cremation,” cremationassociation.org Higher urban density, limited burial plots, and growing environmental awareness are steering households toward cremation, while digital memorials keep memories alive beyond the service transaction. Consolidation among traditional human funeral chains, coupled with technology investments such as remote-monitored cremation equipment, is reshaping price structures and service quality. Government rule-making—from Texas burn-rate limits to new USPS packaging protocols—raises compliance costs but rewards early adopters of cleaner systems and certified handling practices.

Key Report Takeaways

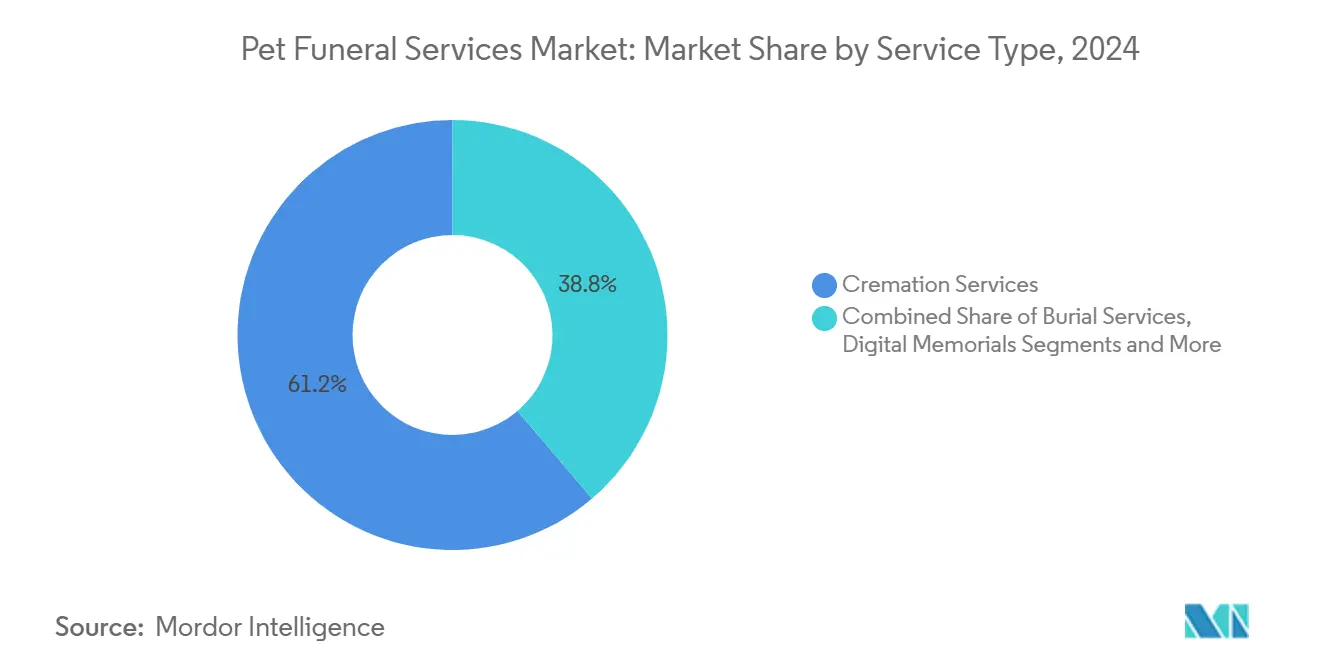

- By service type, cremation services retained 61.24% of the pet funeral services market share in 2024, whereas digital memorials are expanding fastest at a 13.83% CAGR through 2030.

- By pet type, dogs led with 46.82% revenue share in 2024, while cats are projected to post the strongest growth at a 12.88% CAGR to 2030.

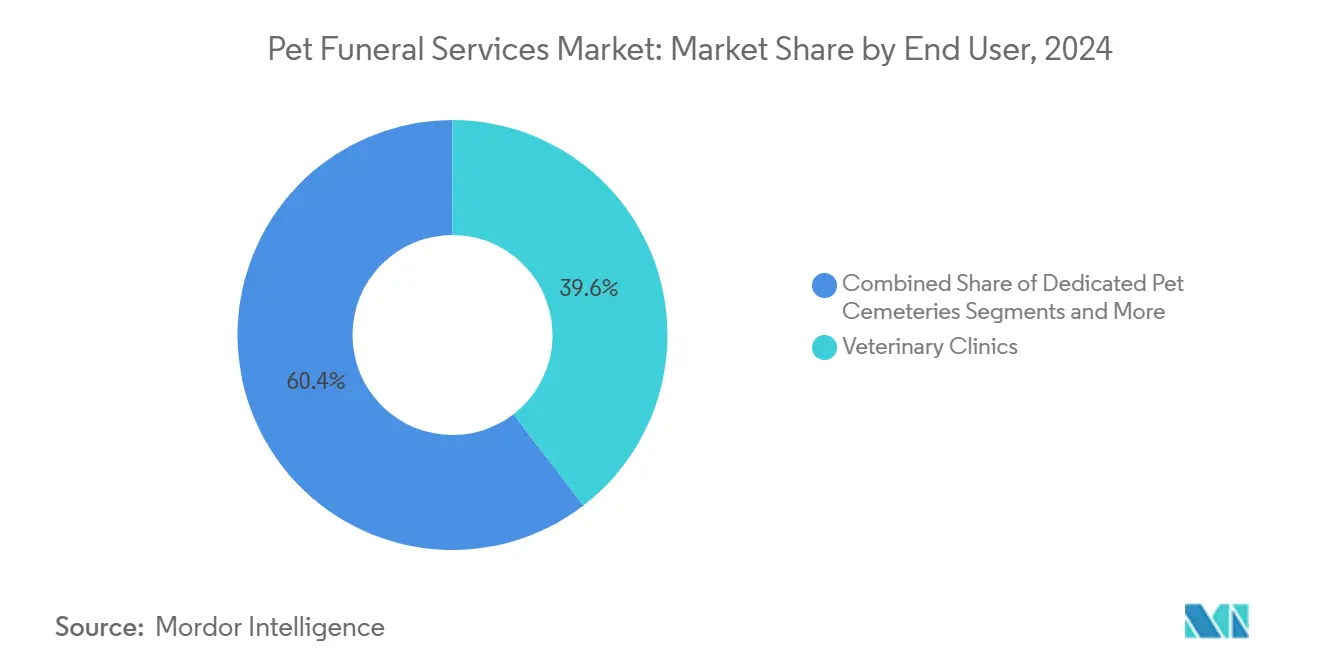

- By end user, veterinary clinics and hospitals held 39.58% of the pet funeral services market size in 2024; direct-to-consumer channels are forecast to advance at a 13.55% CAGR through 2030.

- By distribution channel, offline providers—including funeral homes and veterinary clinics—accounted for 69.37% share in 2024, but online booking platforms are on track for a 14.72% CAGR to 2030.

- By geography, North America commanded 35.71% share of the pet funeral services market in 2024, whereas Asia-Pacific is expected to register the highest regional expansion at a 12.57% CAGR through 2030.

Global Pet Funeral Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet-humanization sentiment | +2.8% | Worldwide; strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Increasing global pet ownership & spending | +2.1% | Global with emerging-market acceleration | Long term (≥ 4 years) |

| Growing preference for cremation over burial | +1.9% | North America & Europe; spreading to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of human funeral chains into pet segment | +1.6% | North America & Europe | Medium term (2-4 years) |

| Subscription-based digital memorial platforms | +1.2% | Technology-adopting markets worldwide | Short term (≤ 2 years) |

| Accreditation & training standards for crematoria | +0.4% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet-Humanization & “Family-Member” Sentiment

Japanese families now spend up to 9,880 yuan on bespoke farewell rituals that mirror human funerals. Kannouji Temple has presided over more than 4,000 pet services in two decades, underscoring how spiritual institutions are normalizing elaborate ceremonies.[2]Hideo Suzuki, “Grieving and Finding Solace After Loss of Pet,” mainichi.jp Emotional intensity is such that 40% of owners report grief levels equal to or greater than those felt after a human loss, boosting demand for counseling. The resulting shift positions full-service packages—complete with viewing rooms and clergy-led rites—as essentials rather than luxuries. Operators able to reconcile cultural nuance with professional standards capture higher basket sizes and stronger retention through anniversary memorials. Premium pricing therefore stems from emotional necessity rather than discretionary indulgence.

Increasing Global Pet Ownership & Spending Levels

Millennial and Gen Z consumers in Asia treat veterinary wellness, insurance, and end-of-life care as interconnected commitments, lifting premium uptake across the cycle. In the United States, roughly 70% of households keep at least one companion animal, a ratio that held firm during recent downturns. China’s accelerating funeral sector reveals how first-time urban pet parents rapidly adopt paid services once exposure occurs. Higher disposable incomes and later family formation reinforce the trend, making the pet funeral services market resilient to broad economic swings. For providers, rising ownership volumes translate into predictable demand curves and justify regional expansion even in tightening credit environments.

Growing Preference for Cremation Over Burial

Cremation now accounts for more than 59% of companion animal dispositions in North America, aided by urban zoning restrictions and eco-concerns. Multi-chamber systems like Matthews’ MPYRE 3 process up to 60 individual pets daily while offering mobile monitoring, demonstrating throughput and transparency gains.[3]Matthews Environmental Solutions, “Pet Cremation Equipment,” matthewsenvironmentalsolutions.com Alternatives such as alkaline hydrolysis cut energy use by 90%, and partnerships between AquaCrossings and veterinary clinics allow clinics to position “green farewell” options at point of care. Space shortages, especially in dense Asian metros, place further logistical pressure on burial, accelerating adoption of portable urns and shared columbaria. Facilities that combine low-emission technology with digital tracking ease regulatory approval and build consumer trust through verified chain-of-custody data.

Expansion of Human Funeral Chains into Pet Segment

Service Corporation International injected USD 181 million into 26 funeral homes and six cemeteries possessing dual-service capability in 2024. The company converts idle cremators during off-peak human volumes to handle pets, optimizing asset utilization and cross-selling grief services. Suburban properties benefit most because established community presence reduces acquisition hurdles and marketing costs. Bundling human-pet memorial plans also appeals to older owners who wish to keep family remains together. Competitors respond either by launching in-house pet brands or signing referral contracts to avoid losing share to integrated chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulation & inconsistent quality | −1.8% | Global, especially emerging markets | Medium term (2-4 years) |

| Price sensitivity in emerging economies | −1.4% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Cultural or religious reluctance toward cremation | −1.1% | Asia-Pacific & Middle East traditional communities | Long term (≥ 4 years) |

| Environmental scrutiny of cremator emissions | −0.9% | North America & Europe; expanding worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulation & Inconsistent Service Quality

In China’s rapidly expanding market, absence of uniform rules leads to variable handling practices, undermining owner confidence and depressing repeat purchases. Cross-border chains struggle to synchronize SOPs when local licensure and waste-disposal laws differ widely. Voluntary guidelines from trade bodies help but lack enforcement teeth, prolonging compliance gaps. Larger groups lobby for standardized permits to lower due-diligence costs during acquisitions. Until harmonization rises, quality discrepancies remain a brake on growth.

Price Sensitivity in Emerging Markets

Households in parts of Southeast Asia and Latin America often earn less than USD 10,000 annually, making premium funeral packages out of reach. Operators introduce tiered offerings, from communal cremations with minimal ceremonies to full-service rites, yet margins thin at the budget end. Government subsidies are scarce, and cultural norms sometimes favor home burials despite urban constraints, slowing volume uplift. Currency volatility further clouds pricing strategy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Memorials Lead Innovation Wave

Cremation retained 61.24% of the pet funeral services market share in 2024, supported by widespread installation of MPYRE 3 systems offering app-based controls. Digital memorials, however, are forecast to climb 13.83% CAGR, the fastest within the pet funeral services market. The shift reflects owner desire for perpetual remembrance without storage constraints.

Operators increasingly bundle online galleries, live-streamed services, and blockchain-verified ashes tracking. This integration extends engagement beyond the event, transforming a one-off fee into subscription revenue. Traditional burial lags yet remains relevant for rural communities. Keepsake jewelry gains momentum as temples in Japan embed ashes into bio-jewel stones, blending spirituality with personalization.

By Pet Type: Cats Surge as Indoor Ownership Rises

Dogs generated 46.82% of revenue in 2024, reflecting higher average body weight and perceived companionship depth. Cats, however, are accelerating at a 12.88% CAGR, narrowing the gap within the pet funeral services market size.

Rising high-rise living favors smaller animals whose remains also cost less to cremate, making premium add-ons affordable. Specialized operators now accept birds, reptiles, and even insects, expanding the addressable base. Facilities display multi-species ovens and tailored urn designs to emphasize care regardless of pet type.

By End User: Direct-to-Consumer Channels Accelerate

Veterinary practices accounted for 39.58% of the pet funeral services market size in 2024 because grieving owners trust their primary caregivers. Yet direct-to-consumer bookings via platforms like CodaPet, where veterinarians earn USD 370 per in-home euthanasia visit, are expanding 13.55%.

Hybrid models merge clinic referrals with online self-service scheduling, allowing families to choose providers by name and read certified-quality reviews. Funeral homes that cultivate veterinary partnerships through CE-credited seminars sustain volume while building brand recognition among pet owners.

By Distribution Channel: Online Platforms Transform Access

Offline channels—funeral homes and clinics—commanded 69.37% share in 2024, underscoring the tactile needs of bereavement. Online bookings, however, forecast a 14.72% CAGR as digital-native owners demand 24/7 convenience.

Subscription plans bundle grief-counseling chatlines and anniversary reminders, turning the pet funeral services industry from a transactional model into a long-term service relationship. Certification bodies now offer hybrid online modules, lowering training barriers and accelerating global standards.

Geography Analysis

North America led with 35.71% share in 2024 thanks to established cremation norms, 70% household pet ownership, and Service Corporation International’s USD 181 million acquisition spree that added facilities equipped for companion animals. Environmental compliance is strict; new USPS rules effective February 2025 require tamper-evident containers and absorbent linings when shipping ashes. Providers embracing eco-friendly equipment and certified handling therefore strengthen brand equity.

Europe follows with mature yet innovative markets where regulatory pressure hastens adoption of low-emission or water-based dispositions. Matthews Environmental Solutions reports more than 5,000 system installs across the region, testifying to retrofit momentum. Consumer sentiment aligns with sustainability, encouraging providers to highlight carbon-offset programs and renewable-powered facilities.

Asia-Pacific, the fastest-growing region at 12.57% CAGR, benefits from cultural normalization as temples and luxury brands embrace pet rites. Korea’s Skypet received top honors at the 2025 Korea Luxury Brand Awards for services that blend ceremonial halls, memorial rooms, and bio-jewel products. Japan’s Kannouji Temple offers joint graves for pets and owners, reflecting deep integration of pet memorials into mainstream practices. China’s rapid urbanization spurs large-scale private crematories despite uneven regulation, signaling expansive upside once standards unify.

Competitive Landscape

The pet funeral services market displays moderate fragmentation yet accelerating consolidation. Top human funeral chains leverage operational synergies to add companion-animal services, illustrated by Service Corporation International’s 12% year-over-year earnings jump after integrating 26 dual-purpose properties. CVS Group exited its crematoria arm, selling to Anima Care for GBP 42.4 million, underscoring that veterinary multinationals prefer medical-care focus while specialized players scale niche expertise.

Technology leadership differentiates brands; Matthews International’s MPYRE 3 combines IoT sensors, predictive maintenance, and remote control to cut downtime and labor cost, empowering operators in more than 5,000 locations worldwide. Online-first networks like CodaPet expand veterinarian earning potential and geographic reach without investing in brick-and-mortar, positioning themselves as asset-light disruptors.

Accreditation gains strategic weight. Facilities with CANA or IAOPCC credentials market verified chain-of-custody and grief-support capabilities, attracting veterinary referrals and commanding premium fees. Smaller independents either join buying groups to access capital for compliance upgrades or serve hyperlocal niches where personal relationships outweigh certification status.

Pet Funeral Services Industry Leaders

Veternity

Anima Care

InvoCare Ltd

Service Corporation International (SCI)

Pets in Peace

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Korea’s Skypet won the grand prize in the pet mutual aid service category at the 2025 Korea Luxury Brand Awards, honoring its specialized funeral halls, memorial rooms, and bio-jewel services.

- April 2025: CVS Group sold its pet crematoria estate to Anima Care for GBP 42.4 million, marking a strategic exit to focus on core veterinary medicine.

- February 2025: Service Corporation International confirmed USD 181 million in 2024 acquisitions of 26 funeral homes and six cemeteries, many featuring integrated pet crematories.

Global Pet Funeral Services Market Report Scope

| Burial Services |

| Cremation Services |

| Memorial Products & Keepsakes |

| Digital / Virtual Memorials |

| Dogs |

| Cats |

| Small Mammals |

| Birds |

| Other Pets |

| Veterinary Clinics & Hospitals |

| Direct-to-Consumer / Pet Owners |

| Dedicated Pet Cemeteries |

| Funeral Homes with Pet Services |

| Animal Shelters & Rescues |

| Offline (Funeral Homes, Vets) |

| Online Booking Platforms |

| Subscription / Membership Plans |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Burial Services | |

| Cremation Services | ||

| Memorial Products & Keepsakes | ||

| Digital / Virtual Memorials | ||

| By Pet Type | Dogs | |

| Cats | ||

| Small Mammals | ||

| Birds | ||

| Other Pets | ||

| By End User | Veterinary Clinics & Hospitals | |

| Direct-to-Consumer / Pet Owners | ||

| Dedicated Pet Cemeteries | ||

| Funeral Homes with Pet Services | ||

| Animal Shelters & Rescues | ||

| By Distribution Channel | Offline (Funeral Homes, Vets) | |

| Online Booking Platforms | ||

| Subscription / Membership Plans | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the pet funeral services market in 2025?

The pet funeral services market size reached USD 2.11 billion in 2025 and is projected to climb to USD 3.42 billion by 2030.

What is the expected CAGR for pet end-of-life services by 2030?

The market is forecast to expand at a 10.08% CAGR between 2025 and 2030.

Which service type is growing fastest?

Digital memorial platforms are advancing at a 13.83% CAGR thanks to subscriptions that extend remembrance beyond the ceremony.

Which region offers the highest growth potential?

Asia-Pacific leads with a forecast 12.57% CAGR as cultural acceptance and government support rise.

Why are cremation services dominant?

Urban land scarcity, environmental concerns, and advanced multi-chamber systems make cremation a practical, eco-aware choice for most owners.

Page last updated on: